Kelly Sullivan

The cybersecurity sector has quietly seen some of its relative premium evaporate in the past quarter. This came in spite of strong results from Palo Alto Networks (NASDAQ:PANW), which has shown that it can continue to grow its top-line at an aggressive pace while also driving solid operating leverage. It is impressive that PANW can do this in the face of a tough macro backdrop and that is testament to the mission-critical nature of cybersecurity products. The most recent selloff has helped the valuation become more palatable, leading me to finally recommend the stock without reservations on the valuation.

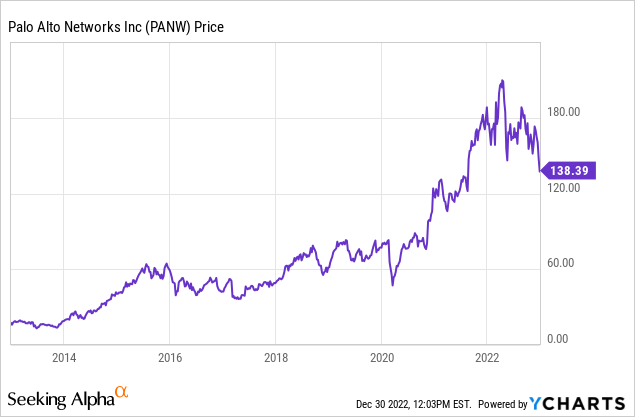

PANW Stock Price

PANW has been a durable long-term performer even accounting for the tech stock crash.

I last covered PANW in August where I found the stock buyable ahead of earnings but noted that the stock traded at a notable premium to peers. After a 20% fall since then, some of that relative premium has faded. I should note that PANW also underwent a 3-for-1 stock split on September 14th, 2022.

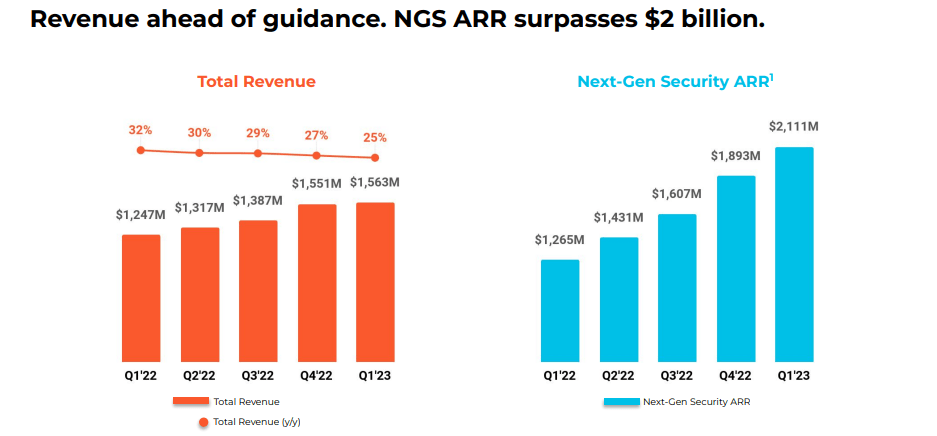

PANW Stock Key Metrics

The most recent quarter saw PANW deliver 25% revenue growth to $1.56 billion – ahead of guidance of $1.535 billion to $1.555 billion. Billings also outperformed with 27% growth to $1.75 billion, a sizable beat over the $1.68 billion to $1.7 billion guidance.

FY23 Q1 Presentation

The company also delivered operating leverage, with operating profits swinging from negative $82.7 million to positive $15.2 million on a GAAP basis. On a non-GAAP basis (the main adjustment being equity-based compensation), operating margins expanded from 18% to 20.6%.

On the conference call, management noted that cybersecurity deals are getting more scrutiny, with customers asking for increased discounting and payment terms. That has led deal cycles to elongate. Like peers, PANW views such deals as delayed, not canceled.

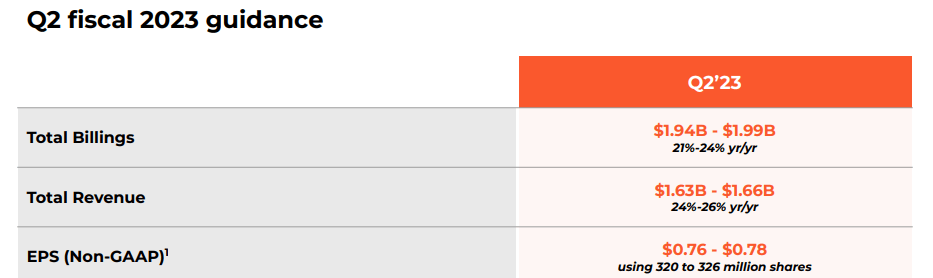

Looking ahead, PANW expects revenue to grow 26% YOY to $1.66 billion, representing some sequential acceleration.

FY23 Q1 Presentation

Management noted that much of that expected acceleration is due to expected outperformance in shipping product revenue that had previously been held back by supply chain constraints. Product revenue is expected to grow in the double-digits in the quarter.

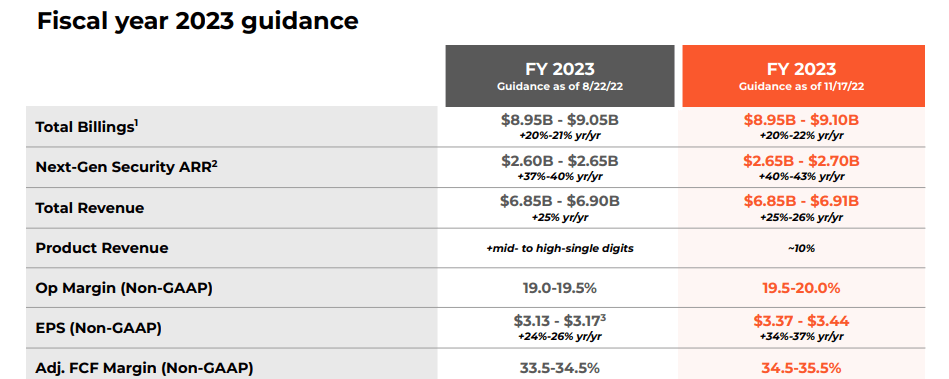

PANW also lifted full-year guidance, with revenues now expected to grow 26% to $6.91 billion and non-GAAP earnings to come in at $3.44 per share.

FY23 Q1 Presentation

Management noted that the company had previously invested aggressively in growth, leading to operating income to grow slower than revenues. But operating income is now expected to grow substantially faster as the company finally realizes operating leverage.

PANW ended the quarter with $5.9 billion of cash versus $3.7 billion of convertible notes, representing a solid net cash position. Those convertible notes are already convertible and I would not be surprised if the company uses shares to settle the impending maturities.

On a similar note, the company did not repurchase any stock in the quarter. I found such a decision to reflect a welcome dose of humility – management noted that they are looking for M&A possibilities amidst the crash in tech stocks.

Is PANW Stock A Buy, Sell, Or Hold?

Over the years, PANW has assembled a complete cybersecurity offering bolstered through M&A. Many of its products are highly ranked in the industry, making PANW a compelling choice for customers looking for a quick cybersecurity fix.

FY23 Q1 Presentation

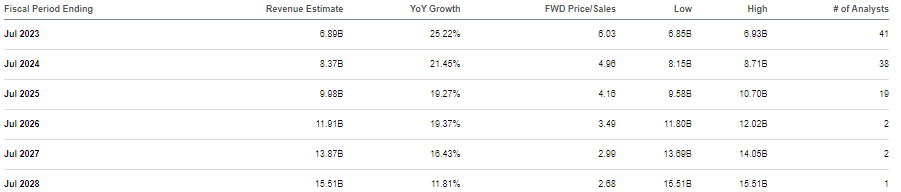

PANW has seen its valuation finally dip into more reasonable levels with the stock now trading at 6x sales.

Seeking Alpha

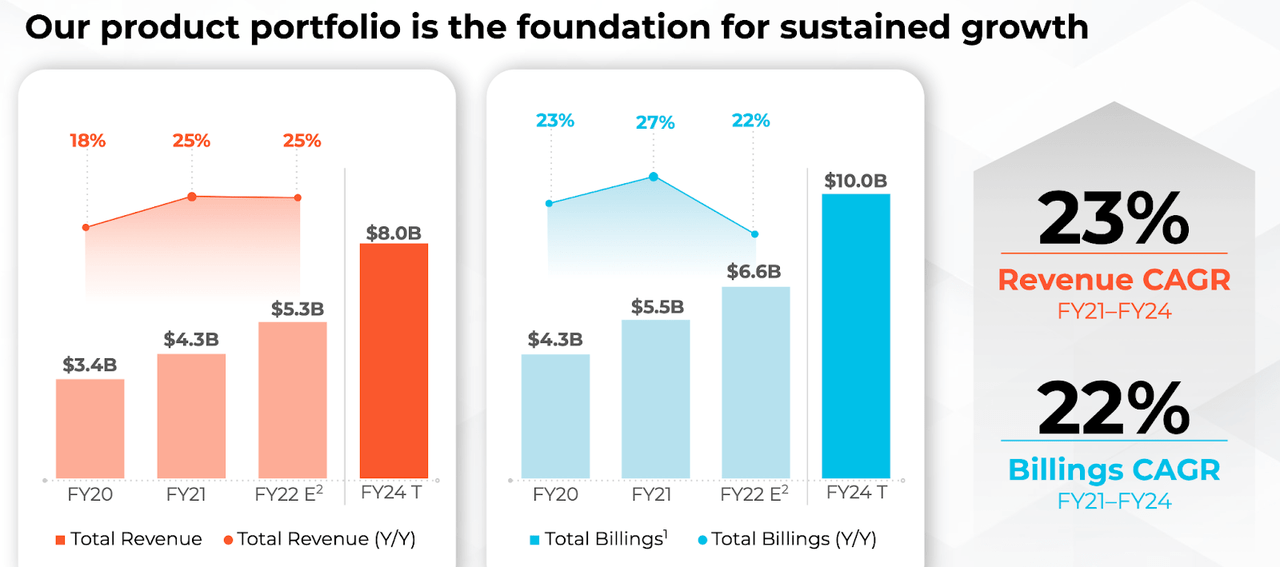

PANW had previously guided for 23% annual topline growth to $8 billion in revenue in 2024.

2021 Investor Day

Consensus estimates see PANW crushing that guidance with $8.4 billion in projected 2024 revenues.

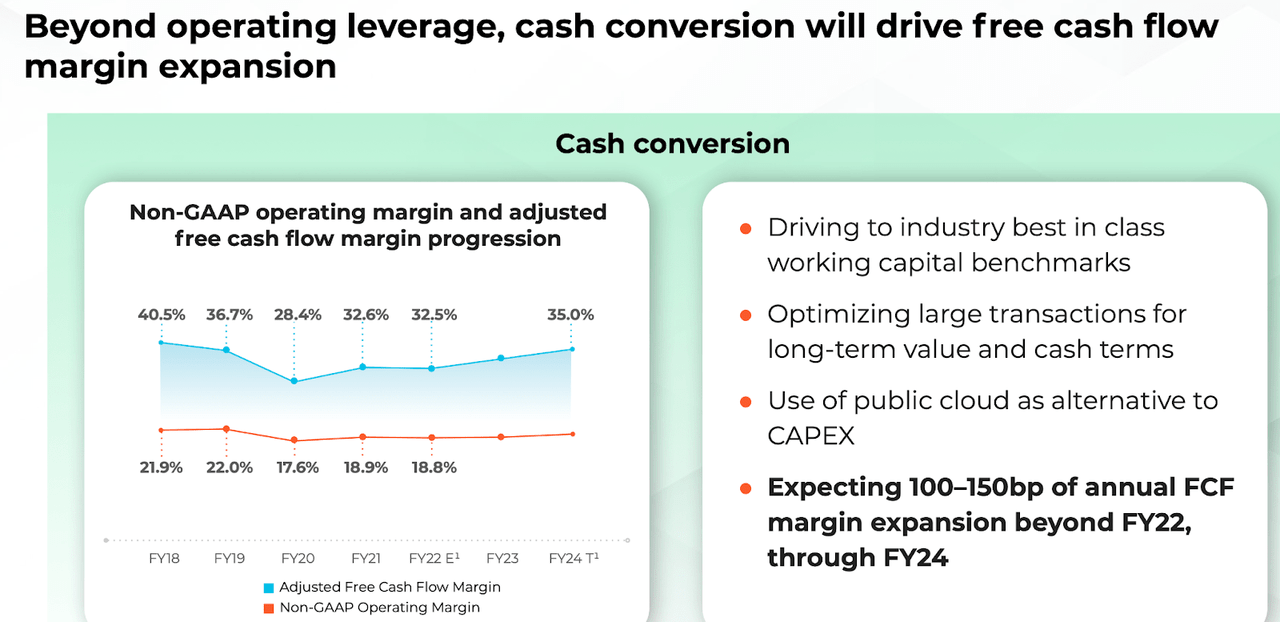

PANW had also guided for free cash flow margins to reach 35%. Based on management’s guidance for this year, the company is expected to hit that target one year in advance.

2021 Investor Day

Based on 20% projected growth, 25% long term net margins and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see PANW trading at 7.5x sales, representing a stock price of $209 per share and 50% potential upside over the next 1.5 years.

What are the key risks? PANW and much of the cybersecurity platform still retain some relative premium to other tech peers. If growth slows down due to macro concerns, I would not be surprised to see PANW re-rate substantially lower. I could see PANW trading down 25% just to trade similarly with peers. Another risk is that of competition. There are many formidable competitors in cybersecurity and at some point this may lead to market saturation. PANW is in an enviable financial position due to its net cash balance sheet and robust cash flow generation, but its stock has not yet priced in such a bearish scenario. Another risk is that PANW appears to be a Wall Street darling, which may subject it to more violent negative reactions in the case of downside surprises. Consider that if the company merely meets their previous guidance for 2024 revenues, then they would be underperforming the consensus estimates by around 5%. As discussed with subscribers to Best of Breed Growth Stocks, this is the time to be investing wide across undervalued tech stocks amidst the tech stock crash. PANW fits right into such a basket, with the stock offering profitable secular growth at reasonable valuations.

Be the first to comment