naphtalina/iStock via Getty Images

Investment summary

Numerous selective opportunities exist within the broad healthcare spectrum as we near the final days of 2022. As we do so, the markets continue ticking over, offering investors the opportunity to position strategically for the year to come. We’d note that buying activity is still rampant in these final periods, and that certain names within our coverage have produced a year-end rally. One name that’s shot onto our radar is TELA Bio, Inc (NASDAQ:TELA), with the stock breaking out from an 18-week long sideways channel in the past 2 weeks.

There’s been no major news attributable to the upside action, other than management’s approval of inducement grants of stock options for 8 of its newly hired employees. The grant allows the company to purchase an aggregate of 15,450 shares, effective of December 7, 2022. However, we’d suggest this is only one part of the picture. Naturally we wanted to see if the recent upside warranted, and what prospects it has on extending into the new year. Here we’ll cover a series of charts to lay the backdrop of our findings. Net-net, after careful examination of all the technical data, we rate TELA a hold.

Note, there is upside risk to our investment thesis that TELA will in fact continue to surge higher on the chart. If this were to occur, it would nullify our hold thesis on the stock, and this must be considered into the investment debate. The same is said for the downside. It’s also important to mention that, should the broad market take another sharp downturn, there is risk TELA could take a larger-than-expected hit to the downside. There are also standard market risks around volatility and large-sigma economic events that could take the broad market by surprise.

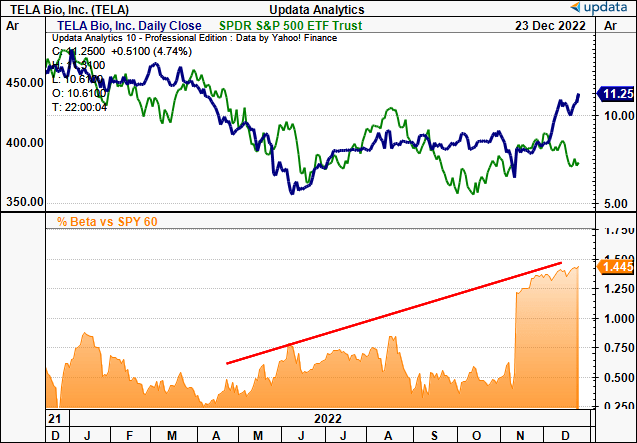

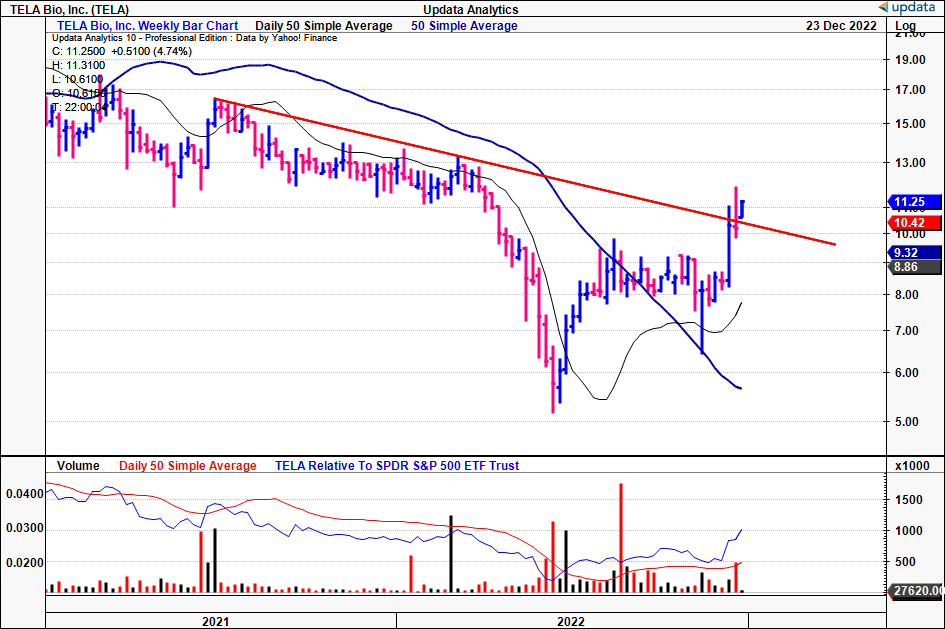

Exhibit 1. TELA 12-month price action, and recent divergence from the S&P 500.

Note, the high-beta nature of the price returns, raising questions as to whether the rally can continue with a pullback in the broad indices.

Data: Updata

Macro-thematic remains challenging for growth-based med-tech companies

In order to understand the market’s positioning in the small-cap domain of the med-tech universe, it’s prudent to be fully aware of the current macro-thematic.

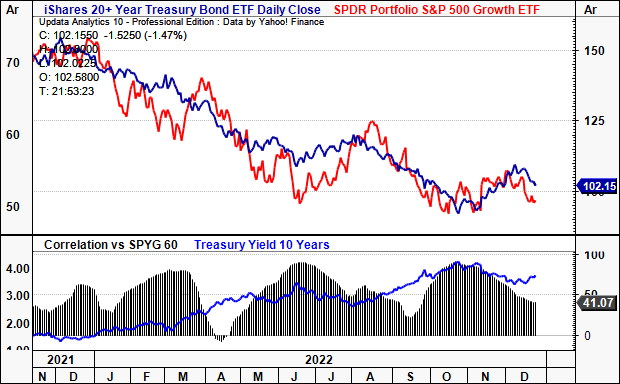

Whilst inflation has been one dominant feature in the market’s performance in 2022, the path of short and long-duration Treasuries has been equally as sensitive. Yields at the long end of the curve continue to roll higher, despite a cooling of inflation data in H2 FY22′. From their low point in 2021, central banks around the world have embarked on a tightening regime the likes of which we haven’t seen in ~40 years.

The yield on the 10-year Treasury note, a good starting point as a benchmark yield, has held its 3.7-4% handle for the bulk of 2022, whilst short-dated T-bills are yielding c.400bps YTM at the time on writing. Both equities and Treasuries continue to be sold off, despite the stock/bond correlation rolling back to FY21 levels. Hence, for risk assets, more so long-duration equities such as TELA, this presents as a downside risk to re-rating further downstream.

Exhibit 2. Yields on long-dated Treasuries continue to compress long-duration equities in H2 FY22.

Data: Updata

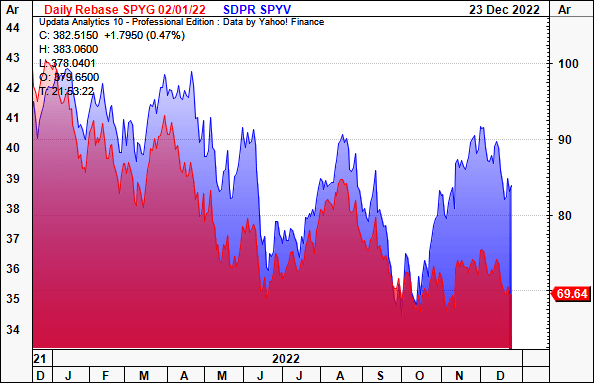

As for factor positioning, the above market turbulence has been unkind to growth-type propositions this year. The predictability of future cash flows is now far less certain, given the higher discount rate, and the cost of capital has shot to multi-year highs. Moreover, the availability of capital has begun to dry up.

The result has led to factors of value maintaining a positive spread over growth for the entirety of 2022, with the divergence increasing over the final quarter of the year. Again, this pressurizes TELA to overcome the fairly sour sentiment geared towards growth-type equities.

Exhibit 3. Value retains positive spread over growth for the entire FY22′.

Data: Updata

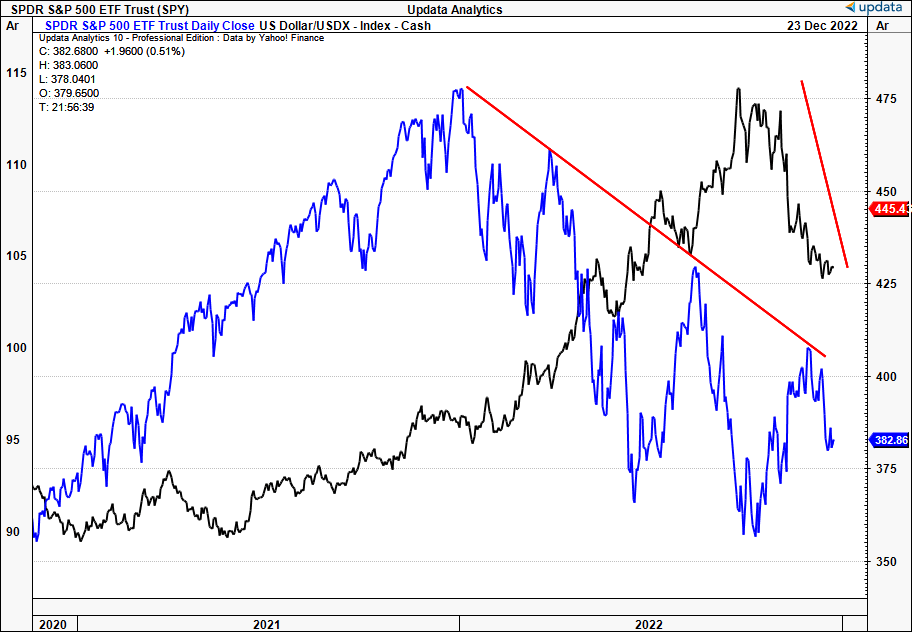

Whereas investors had sought resiliency in the USD in a large flight to quality in early 2022, that trade looks to have exhausted, and the DXY has lost a good portion of its momentum. At the same time, the SPX has just cycled out of its 3rd and final bear market rally for 2022, failing to break above the longer-term resistance level shown below. Again, this isn’t conducive to the performance of risk-assets in general, let alone those equities without the resiliency factors needed to withstand an economic downturn.

Exhibit 3. Correlation in DXY and S&P 500 as divergence between the pair begins to close

Data: Updata

Each of these factors discussed above suggest a difficult time for risk assets in 2023, with long-duration equities [those unprofitable names with cash flows priced well out into the future] looking to have an asymmetrical downside skew.

TELA technical studies – breakout lacks buying support

We turned to our chart studies in order to gauge the validity of TELA’s latest upside moves. You’ll see below the stock broke out from an 18-week sideways consolidation two weeks ago.

In doing so, it poked its head above the longer term resistance level, but the move hasn’t extended, and support’s been weak in terms of buying volume [seen in the bottom frame in Exhibit 4].

At the same time, the stock is trading well aloft its 50DMA and 250DMA, and has been for the bulk of 2022. We’ve yet to see the 250DMA curl upwards, meaning TELA requires more time in this latest rally to see this happen.

Moreover, the lack of volume support is telling that buyers may be absent, with the order book fairly shallow on both sides of the price ladder [in terms of buyers and sellers].

Exhibit 4. TELA 24 month weekly price evolution [log scale].

Data: Updata

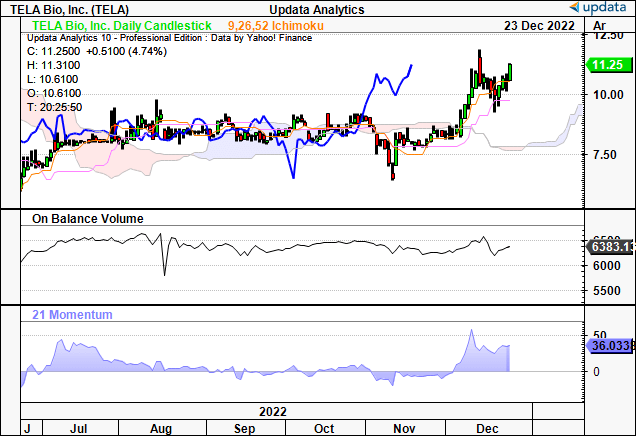

In addition, it’s also worth advising that shares are currently trading well above cloud support after the breakout. Prior to this, it was trading in a narrow range, with consistently tight daily closes. We’re not so confident that the move will sustain itself, because on balance volume is very flat, whilst momentum has also rolled back to the downside. In our opinion, this suggests a lack of accumulation, and certainly doesn’t demonstrate the presence of institutional buying power required to sustain the move.

We checked the options chain for TELA for contracts expiring anywhere from January-April 2023 to see if there was market positioning in TELA without owning the underlying stock. However, it’s noted that there’s currently no calls or puts currently in the money, nor is there positioning to suggest investors are betting on the move to continue. Hence, this aids in our belief shares may continue sideways, as they have done for the past 9 days.

Exhibit 5. Trading above cloud support, yet on balance volume, momentum unsupportive of the move to extend.

Data: Updata

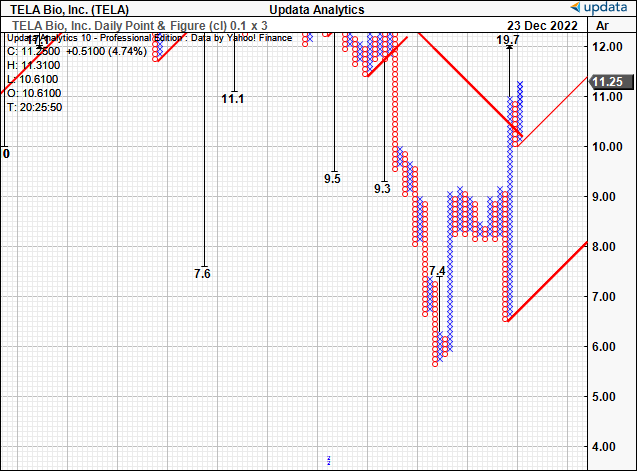

Despite the above analysis, we’d also note that we have upside targets present to $19.70 from our point and figure studies. With the latest price action, shares have thrust off a low point, providing additional support to this level, after it originally took out the $7.40 mark shown.

A jump to $19.70 is certainly attractive at this point, and would imply a further 75% upside potential from the current market price. This should be heavily factored into the investment debate for TELA, and adds a bullish tilt to an otherwise firmly neutral investment debate.

Exhibit 6. Upside targets as high as $19.70, supportive of the rally to continue

Data: Updata

In short

When pulling it all together, we have both factors of division and confluence providing a balanced investment debate for TELA. These technical studies indicate a potentially difficult period for risk-assets leading into the new year, whereas when checking TELA’s price action, volume indicators and directional trend, it may be that an extension of its latest rally could exhaust soon. Immediately offsetting this point is the fact we have technically derived upside targets to $19.70, representing considerable upside potential to that objective. However, in our opinion, the mitigating factors outweigh the attractive ones at present. There doesn’t appear to be the overwhelming presence of buyers needed to drive the stock higher, back above its previous highs. Therefore, without the abundance of required evidence present on analysis, we rate TELA a hold.

Be the first to comment