Michael Vi

After the market closes on February 13th, the management team at Palantir Technologies (NYSE:PLTR) is expected to announce financial results covering the final quarter of the company’s 2022 fiscal year. Last year was an undeniably volatile year for investors in the software and data-centric enterprise, as the prospect of continued rapid growth gave way to a new outlook that growth moving forward might be more tepid. Already, shares of the company were rather pricey. But add in the broader economic concerns that most other companies are dealing with also, and it should be no surprise to investors how much shares of this business have moved around. Whether you like it or not, it is highly probable that we will see continued fluctuations in the business, with those most often occurring in response to earnings results. But to prepare themselves, investors would be wise to understand what to expect when the company does report. Only by understanding what the market expects and reacting to what the company ultimately reports (all in a timely manner), can investors maximize their returns or minimize their losses while still participating in the potential the company provides.

Overall guidance is key

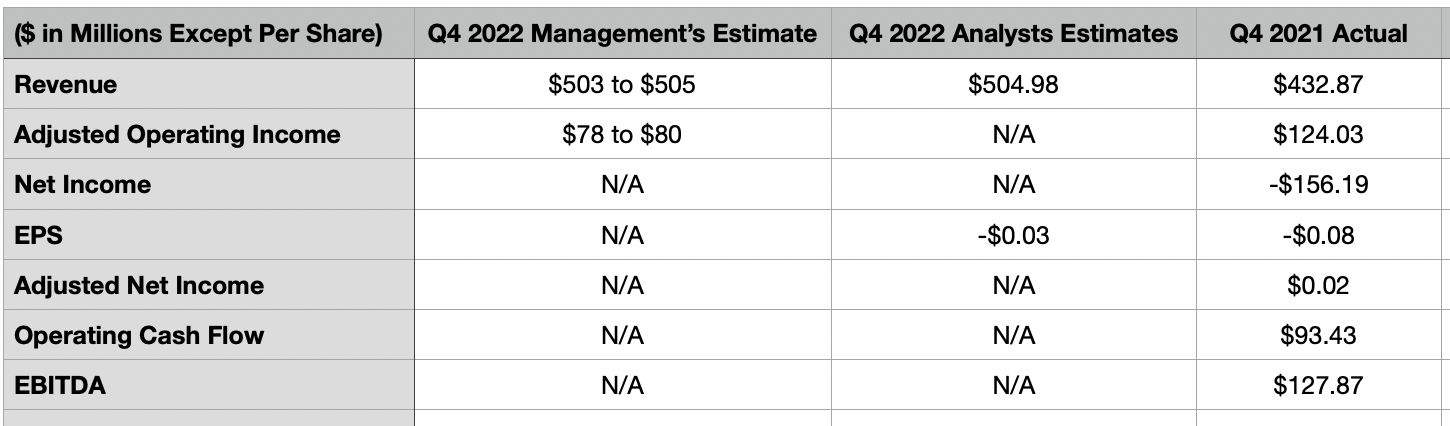

The two initial items that investors will be paying attention to will be revenue and profits per share. For the quarter, management most recently forecasted sales of between $503 million and $505 million. If we ignore foreign currency fluctuations, this would be slightly higher at between $508 million and $510 million. To put this in perspective, the overall sales the company reported during the final quarter of its 2021 fiscal year came in at $432.87 million. Hitting the midpoint on expectations would translate to a year-over-year increase of 16.4%. Analysts seem slightly more optimistic, with a current forecast for sales of $504.98 million.

Author – SEC EDGAR Data

Particularly interesting would be the commercial revenue the company generates. Historically speaking, Palantir Technologies has very much been focused on government contracts. But in order to capture rapid growth moving forward, management has been pushing more toward locking down commercial contracts. The company prided itself in the fact that, during the third quarter of 2022, it experienced a 53% surge in commercial revenue from the U.S. market. However, overall commercial revenue was a much more modest 17%. The growth the company has seen has come largely from a rise in the number of commercial customers on its roster. As of the end of the latest quarter for which data was available, this came out to 228. That was up from 203 reported one quarter earlier and stacked up nicely against the 115 that the company had as of the end of the third quarter of 2021. For context, the number of commercial customers that the business had as of the final quarter of 2021 came in at 147.

Clearly, investors should pay attention to the commercial side of things. In recent months, management has reported some positive movements on this front. The most recent came on February 1st of this year when the company announced a $50 million expansion with SOMPO Holdings that will allow its customer to roll out critical workflows across over 10,000 of its salespeople within Japan. On January 19th, Palantir Technologies announced a partnership with the Cleveland Clinic to deliver an operations ‘Virtual Command Center’ for the Clinic. That particular initiative will be focused on driving operational excellence and improving patient access by means of enabling data-driven decision-making and resource allocation for the hospital. On January 10th, Palantir Technologies announced a strategic partnership with Cloudflare (NET) in order to help the organization cut cloud costs, increase control, and improve predictability over multi-cloud workloads. These are just a few of the developments that could ultimately add to the firm’s commercial efforts, even though these particular ones will not show up on the final quarter income statement.

Investors will also be paying attention to bottom line results. Analysts currently anticipate earnings per share of negative $0.03, with adjusted earnings of $0.03. This compares to the $0.08 per share loss (translating to a loss of $156.19 million) the company experienced at the same time one year earlier, with an adjusted profit during that time of $0.02 per share (or $45.40 million as a whole). Management does not provide any real guidance on this front. But they did say that adjusted income from operations should be between $78 million and $80 million for the quarter, down from the $128.03 million reported one year earlier. Management did not offer any guidance for EBITDA but, for context, this metric the same time one year earlier came in at $127.87 million. Investors would also be wise to pay attention to other profitability metrics as well. For instance, in the final quarter of 2021, operating cash flow for the company came in at $93.43 million. Given the current expectations compared to what was seen in the 2021 fiscal year, it is looking as though the company’s bottom line will suffer to some degree.

Author – SEC EDGAR Data

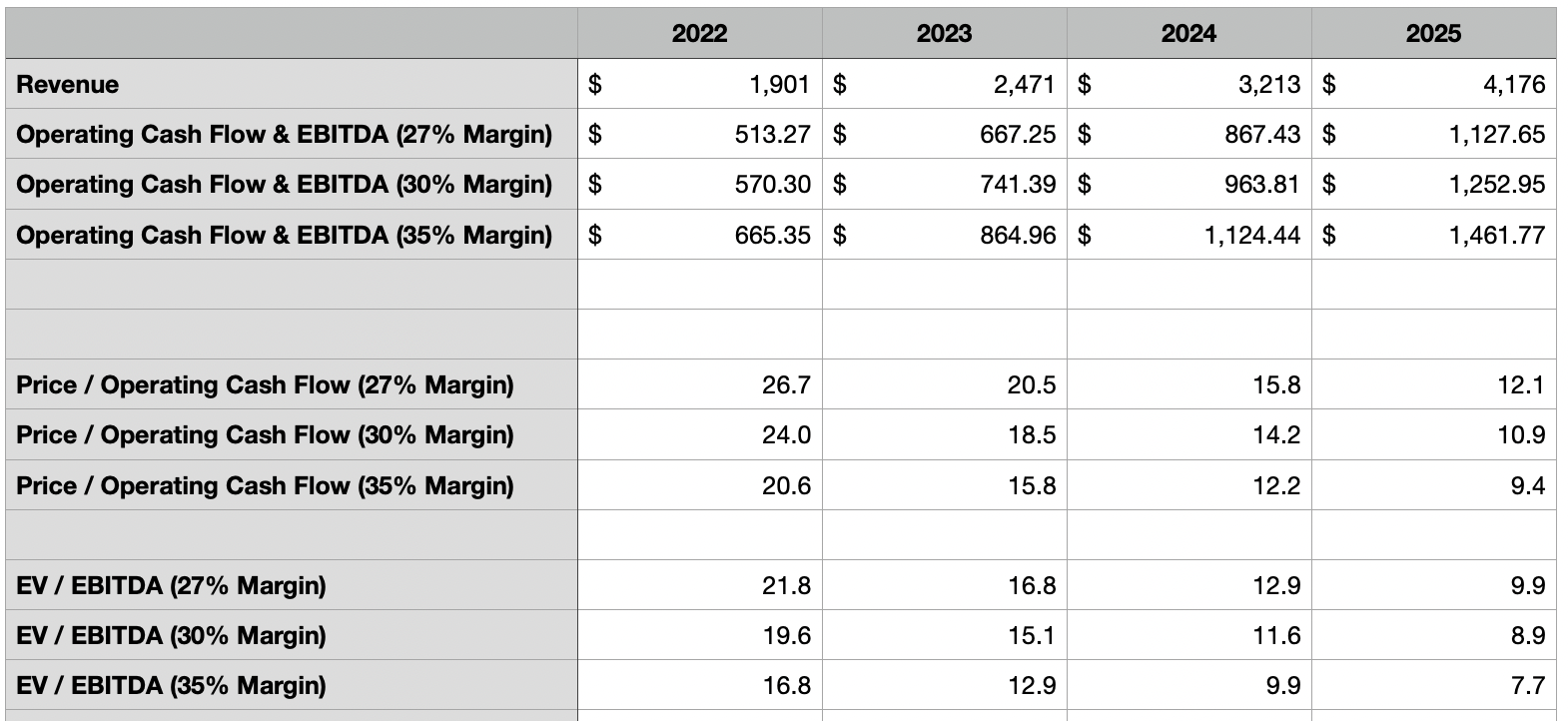

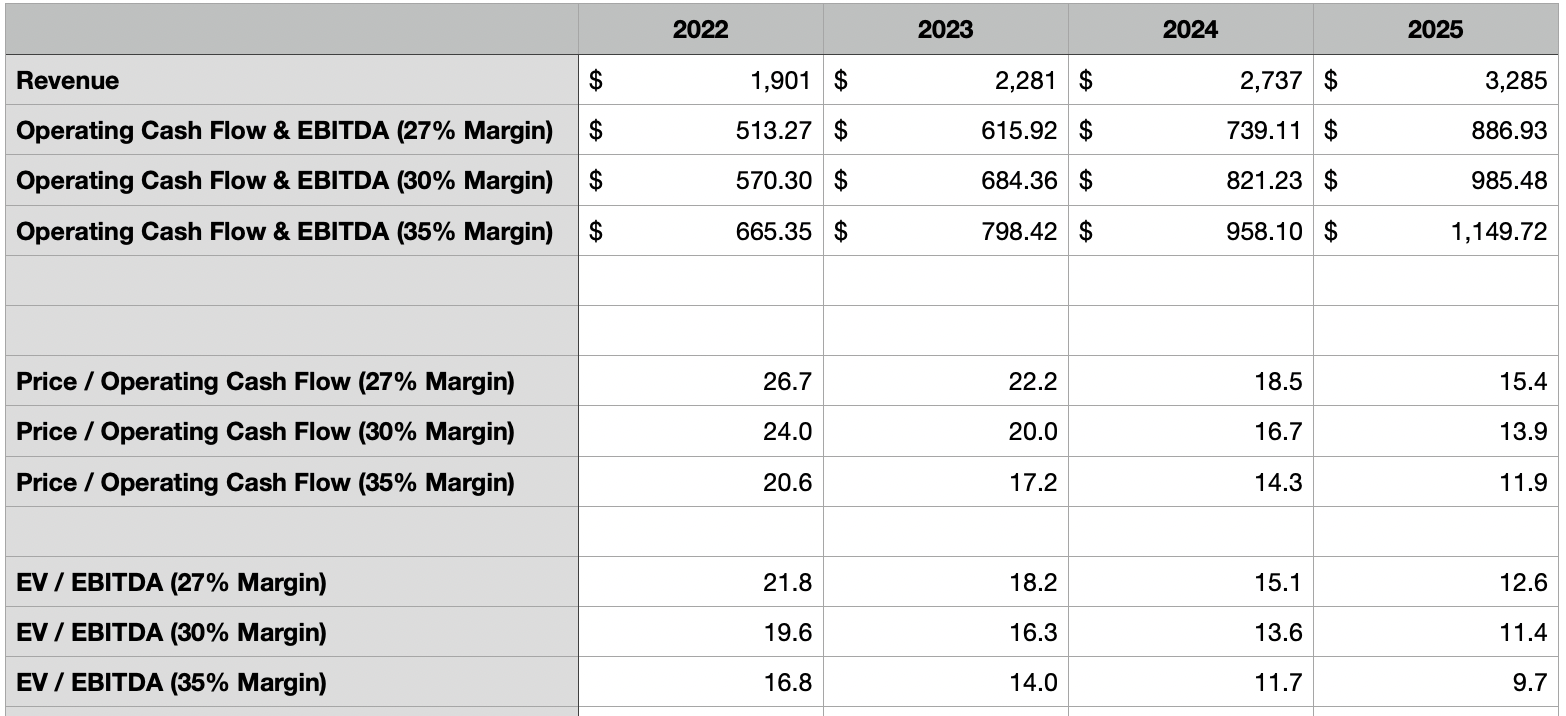

Financial results matter for every company. They serve as a barometer for the health of the business and the kind of upside potential that investors should expect. But fundamental performance is especially important for a company that already looks expensive. As part of my analysis, I decided to value the company based on some expectations about what the future holds. We will know what to expect from a growth perspective once management reports financial results for the final quarter. I have no expectation that the company will continue to grow at the 30% rate that management once said that it would. But if it does, shares of the company don’t start to look appealing to me until closer to 2024. In the table above, you can see the implied revenue as well as both the implied operating cash flow and EBITDA margins for the company, as well as the amount of both metrics that should be generated based on those margins. You can also see the multiples at which shares are trading for under those different scenarios. In the subsequent table below, you can see what happens if you assume a growth rate that’s closer to 20%. In this case, shares don’t look attractive to me until closer to 2025.

Author – SEC EDGAR Data

Takeaway

Based on the data provided, Palantir Technologies doesn’t seem to offer that much opportunity for investors at this time. No doubt, the company will continue to grow year-over-year. Having said that, shares are still pricey at this time. Leading up to earnings, we should keep an open mind though, because that picture could ultimately change. If the company reports results and guidance that are significantly better than anticipated, my stance on the matter could change. But until we see some evidence of that, I still believe that a more prudent assessment of the company involves a ‘hold’ rating.

Be the first to comment