zlikovec

Investment summary

After paring back the rating on IRadimed Corporation (NASDAQ:IRMD) late last year the company came in with a strong set of Q4 and full-year numbers. We emphasized the impact of potential downside after the firm withdrew 510(k) for the 3870 MR IV pump. As an upcoming tailwind, we can confirm management intends to re-file the submission later this year. The post-earnings drift in IRMD’s stock price is positively welcomed and we observed IRMD’s capacity to grow by investing in high-growth opportunities this year, whilst still distributing high amounts of free cash to equity holders. This is key to our revision to buy, and we affirm IRMD deserved to trade at a premium, and that we are paying fair price at 36x earnings.

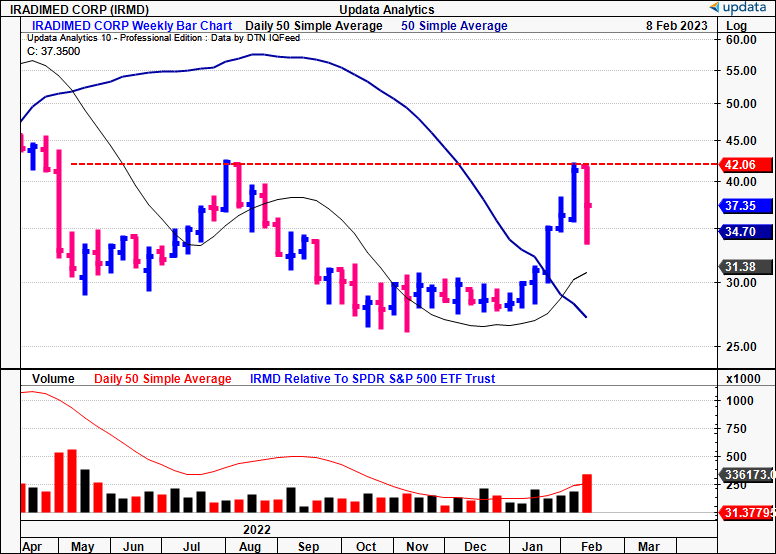

Exhibit 1. IRMD post-earnings drift, testing previous highs

Data: Updata

Q4 results analysis

IRMD maintained its growth route for the full-year with a solid YoY growth in revenue of 28% to $53.3 million. Switching to the quarter, there were several key investor takeaways:

- Q4 revenue stood at $14.9 million, representing a YoY increase of 25% and sequential growth of 11% compared to Q3. Within the domestic market, sales rose by 28% YoY to $12.2 million. Conversely, international sales saw a more modest increase of 8% to $2.6 million in the quarter.

- Looking at the segment highlights, device turnover saw a 23% increase to $9.8 million, particularly due to a 51% increase in monitor sales – a big tick for the salesforce in our estimation. Disposables and services revenue also increased by 32% to $4.5 million, and maintenance contracts by 17% to $595,000.

- The gross margin for the quarter was 75.5%, with a full-year gross margin of 77.4%. This is a decompression of ~100bps YoY. OpEx pulled in to $7 million or 47% of turnover due to a higher spread the SG&A line. As a result, pre-tax operating income lifted 37% YoY to $4.3 million for the quarter. IRMD also booked a tax expense of ~$1mm compared to a tax benefit of ~$779,000 in Q4 2021, leading to an effective tax rate of 20.7%.

-

Moving down the P&L, the company reported net income of $0.29 per diluted share, compared to $0.31 in the prior year quarter. This was attributed to the lower tax benefit. It also realized CFFO to $3 million, declining from $3.4 million in the same quarter of the prior year, whereas FCFF was an inflow of $2.6 million in Q4, down from $3.2 million last year.

-

In terms of business segments, the MR monitor business has been demonstrating remarkable growth and is projected of growth of ~20% in FY23′. We’d note management has forecasted FY23′ revenue in the range of $61 million-$63 million, with GAAP diluted EPS of $1.10-$1.20 on this amount.

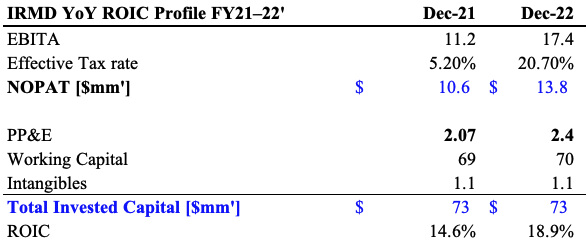

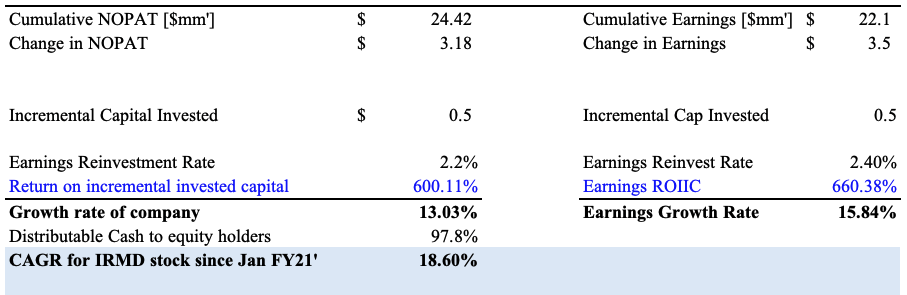

Meanwhile, turning to back to the full-year results, we noted tremendous momentum on IRMD’s profitability front. It generated $24mm in cumulative post-tax earnings and grew earnings by $3.5mm YoY [Exhibit 2]. As a standout, it only increased capital investment by $0.5mm to achieve this. Hence, the incremental ROIC was ~600% from year-to-year [Exhibit 3]. This is ahead of the periodic ROIC, illustrating to us that IRMD’s new investments are generating strong momentum on the profitability front. It only had to reinvest 2.2% of post-tax earnings to achieve this growth, meaning, that, after factoring in this reinvestment, earnings grew 15.8% YoY. A c.2-3% reinvestment to achieve such high return is an attractive value proposition. Hence, ~98% of post-tax earnings are distributable to equity holders. This undoubtedly factored into the company’s $1.05 per share special dividend.

Exhibit 2.

Data: Author, using data from IRMD SEC Filings

Exhibit 3.

Data: Author, using data from IRMD SEC Filings

Valuation and conclusion

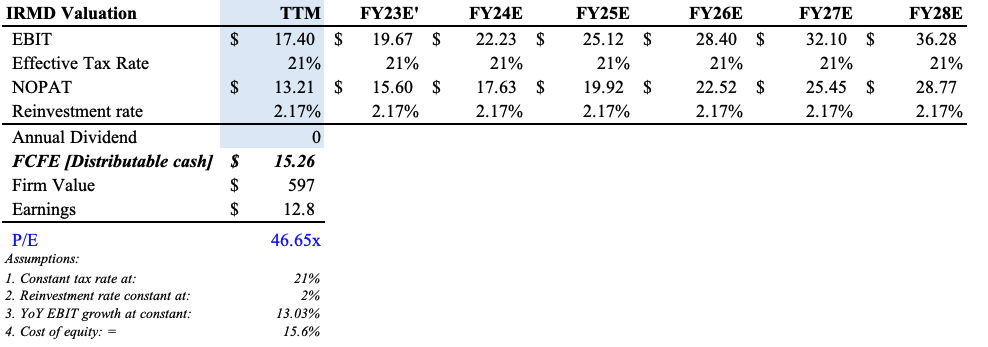

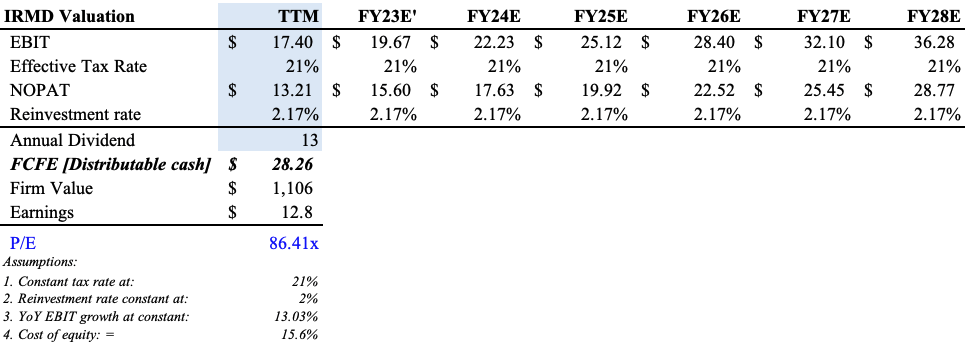

The stock trades at ~31x forward earnings, a 54% premium to the sector. Yet, we advocate IRMD is fairly valued at ~46x earnings, lifting to 86x with the special dividend [Exhibit 4, Exhibit 5, respectively]. Key supportive data points supporting this include:

1. Profitability momentum outlined above, where IRMD invested just 2-3% of post-tax earnings for future growth.

2. The incremental ROIC>historical ROIC, illustrating new launches more profitable than previous ones – serves as robust data for growth in the MR monitor business.

3. High residual FCFs distributable to equity holders as a function of these parameters.

Exhibit 4. IRMD Valuation ex-special dividend

Data: Author’s Estimates

Exhibit 5. Including special dividend

Data: Author’s Estimates

Net-net, we revise our IRMD rating to a buy following the growth percentages exhibited in FY22, pushing our valuation to 86x earnings when factoring in the announced special dividend.

Be the first to comment