Michael Vi

Thesis

Palantir Technologies Inc. (NYSE:PLTR) stock surges as much as 23% in after hours trading, after the company released Q4 2022 results. Not only did Palantir beat analyst consensus estimates with regards to both sales and earnings, but also surprise analysts with guiding for the first ever profitable financial year–in 2023. As Palantir’s long-term opportunity in cloud data analytics remains intact, I reiterate a ‘Buy’ rating for Palantir. Moreover, with profitability on the horizon, I feel PLTR stock can now be anchored less speculatively, and I personally estimate a fair implied share price equal to $9.45/share.

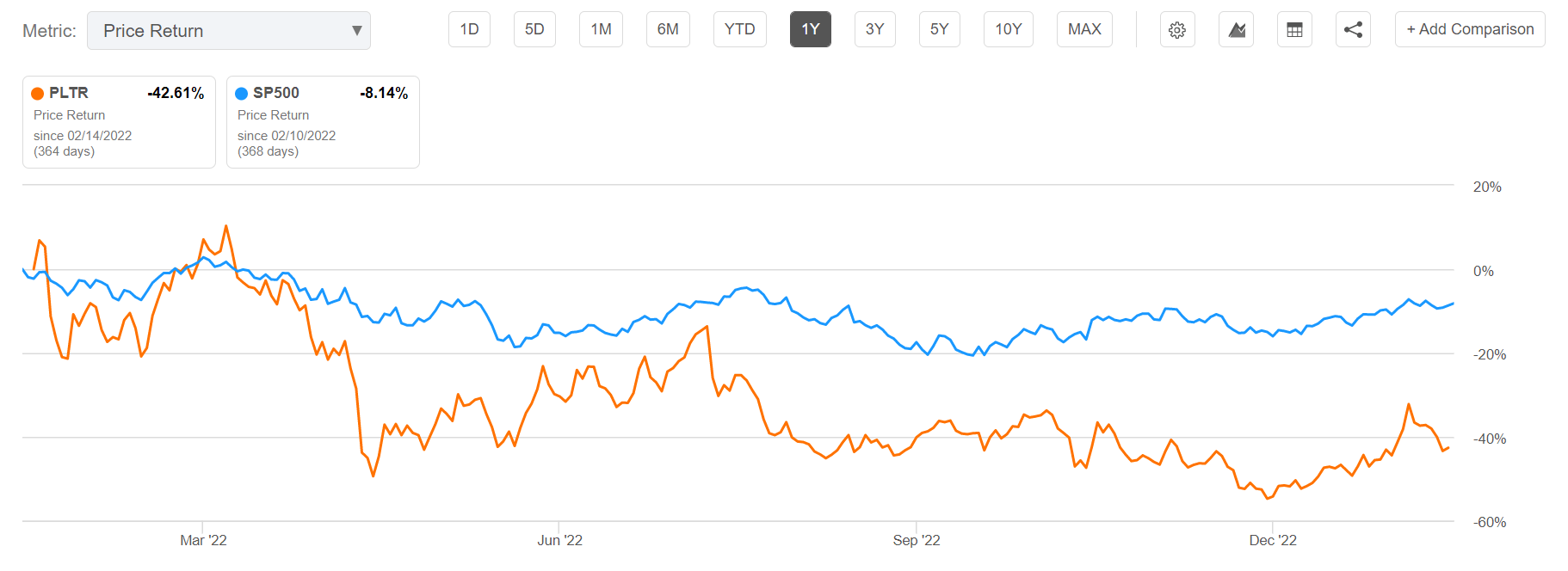

For reference, PLTR stock is down approximately 43% for the past twelve months, as compared to a loss of close to 8% for the S&P 500 (SPY).

Seeking Alpha

Palantir’s Q4 Performance

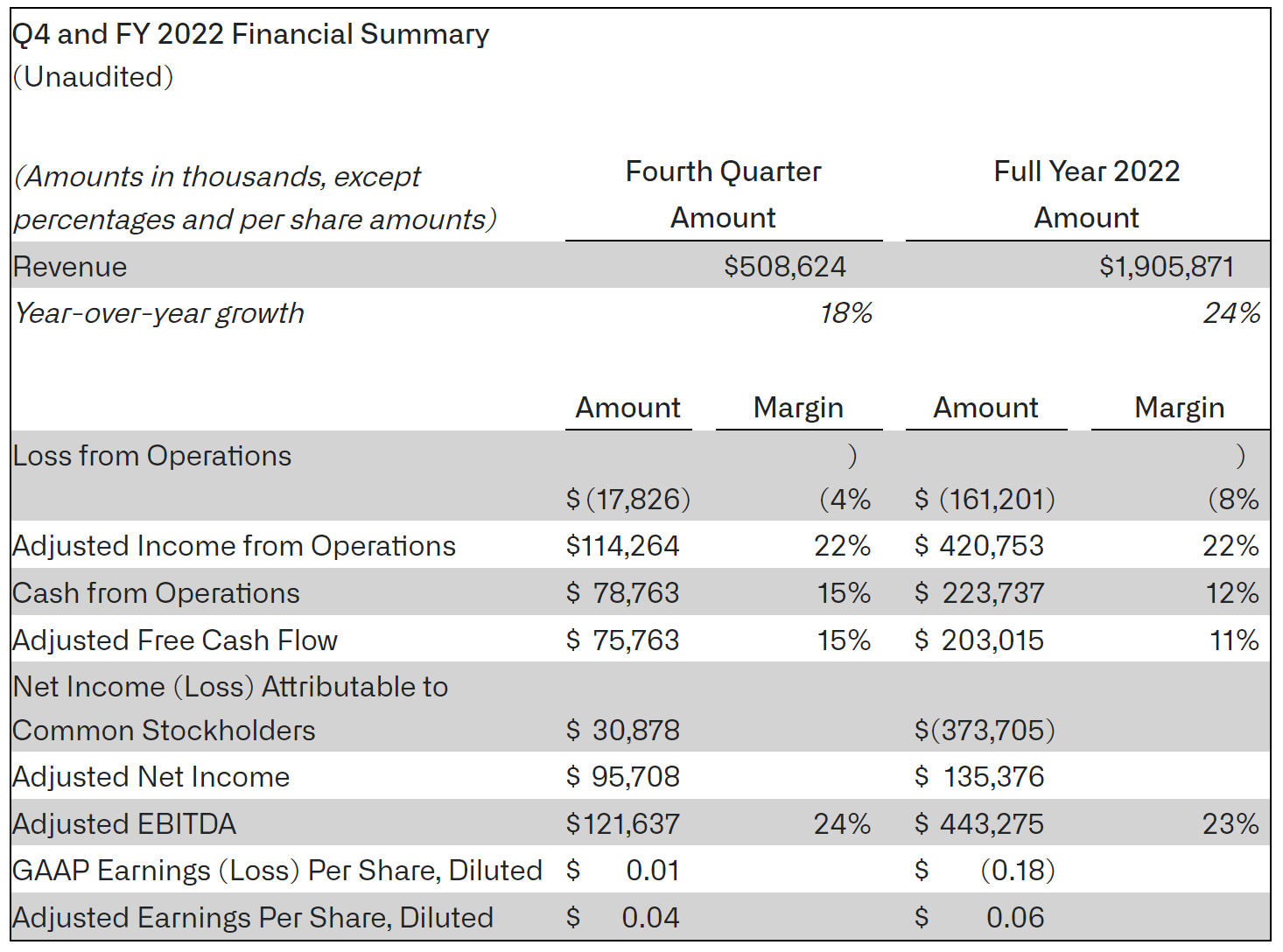

Palantir delivered a s strong December 2022 quarter, beating analyst consensus estimates with regards to both sales and earnings. During the period from September to end of December, the company generated total revenues of about $509 million, as compared to $433 million for the same period one year earlier (18% year over year growth) and compared to $478 million as estimated by analyst consensus. Adjusted income from operations came in at $144 million (22% year over year growth), and adjusted net income was $95.7 million, or $0.04/share (beating analyst expectations for a $0.03/share loss). Notably, Q4 2022 marked Palantir’s first ever profitable quarter, with Alex Karp commenting:

With this result, Palantir is profitable. This is a significant moment for us and our supporters

Palantir Q4 2022 reporting – results

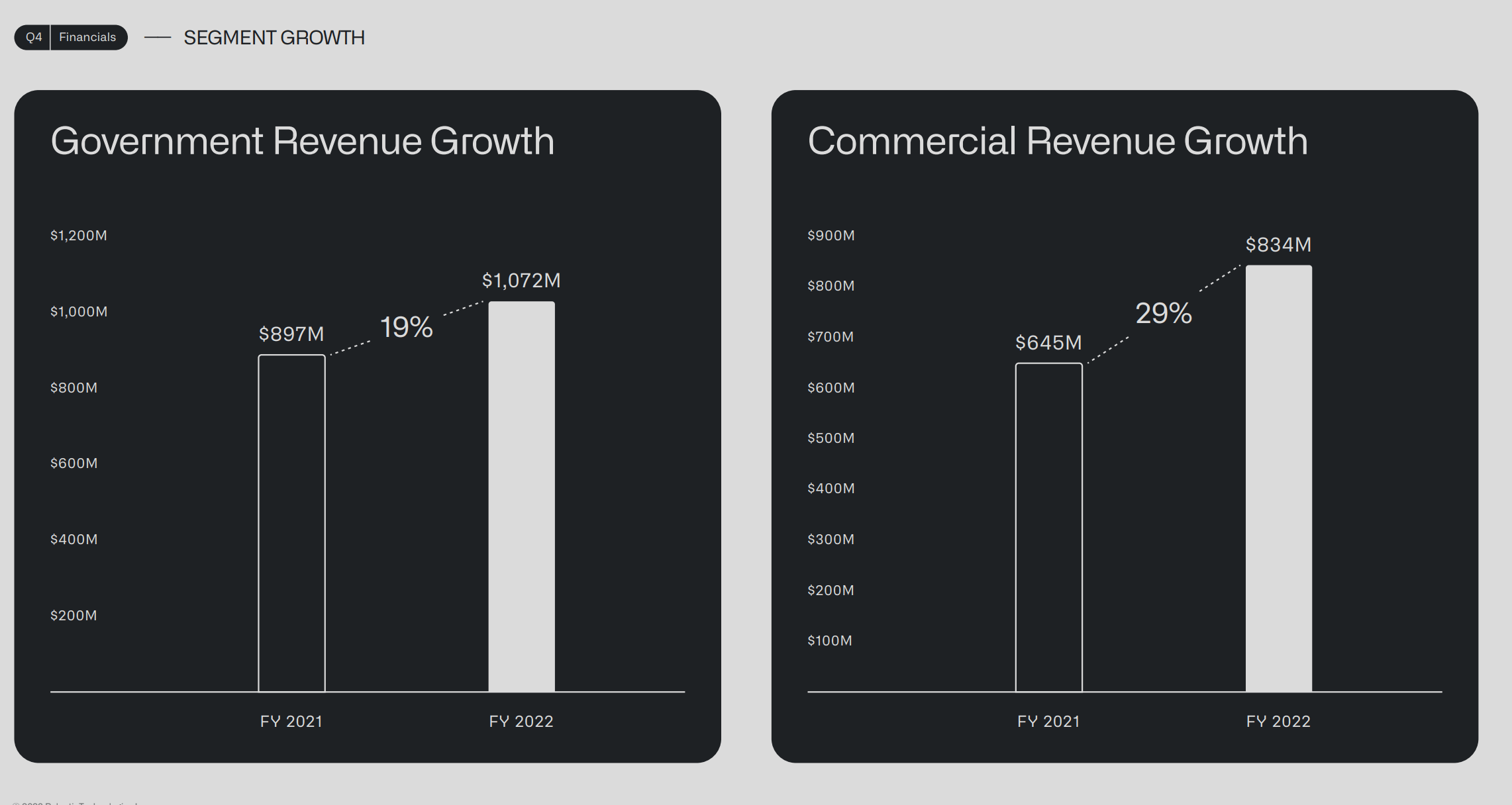

Palantir’s strong Q4 2022 was supported by both strength in government (19% YoY expansion) as well as commercial revenue growth (29% YoY expansion), with commercial at $834 million of revenue slowly catching a similar business size as government at $1.07 billion.

Palantir Q4 2022 reporting – results

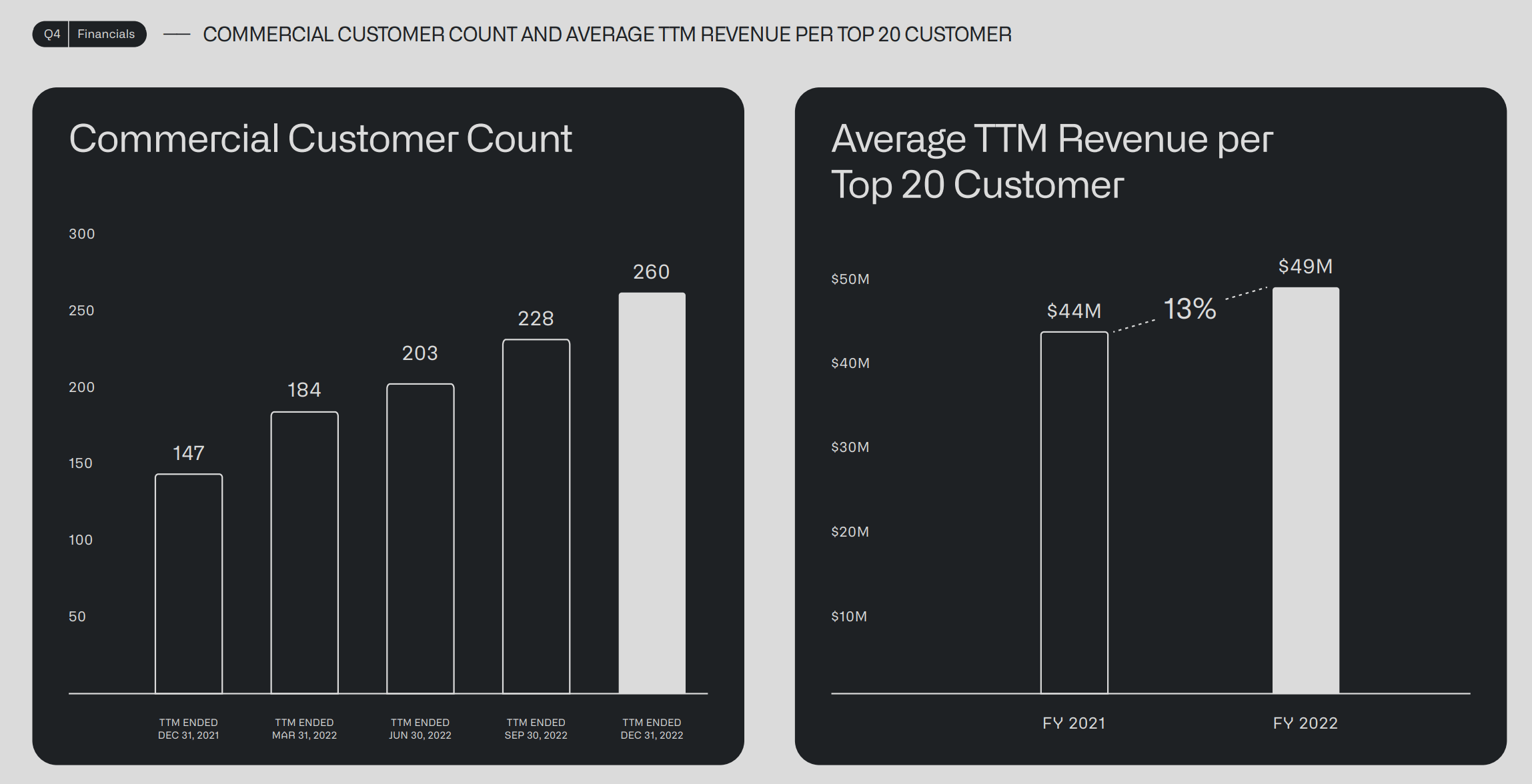

In addition, Palantir managed to attractively grow commercial customer count, while also increasing monetization. As of Q4 2022, Palantir recorded 260 commercial customers (77% YoY jump), with the average TTM revenue per top 20 customer being $49 million (13% YoY growth)

Palantir Q4 2022 reporting – results

Strong Momentum Going Into 2023

Anchored, amongst others, on the prediction that an “increasingly widespread adoption of artificial intelligence in civilian applications will come soon”, as Palantir CEO Alex Karp wrote in a letter to shareholders, Palantir guided for a strong 2023:

A threshold has been crossed, and this is the start of our next chapter … We expect to generate a profit for the current fiscal year, our first profitable year in the history of our company.

Going into Q1 2023, the company guided for revenue of $503 to $507 million and adjusted income from operations of $91 to $95 million. For the full year 2023, Palantir management expects revenues in the range of $2,180 to $2,230 million and adjusted income from operations somewhere between $481-$531 million. However, no guidance was given regarding GAAP net income.

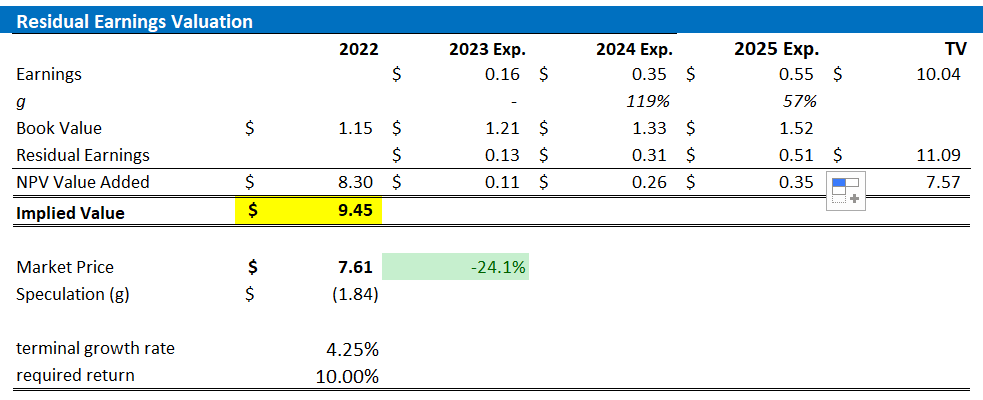

Residual Earnings Model

With profitability on the horizon, I feel it is fair to start valuing Palantir with a residual earnings model, which anchors on the idea that a valuation should equal a business’ discounted future earnings after a capital charge. As per the CFA Institute:

Conceptually, residual income is net income less a charge (deduction) for common shareholders’ opportunity cost in generating net income. It is the residual or remaining income after considering the costs of all of a company’s capital.

With regard to my Palantir stock valuation model, I make the following assumptions:

- To forecast EPS, I anchor on the consensus analyst forecast as available on the Bloomberg Terminal ’till 2025. In my opinion, any estimate beyond 2025 is too speculative to include in a valuation framework. But for 2-3 years, analyst consensus is usually quite precise.

- To estimate the capital charge, I anchor Palantir’s cost of equity at 10%.

- For the terminal growth rate after 2025, I apply a proud 4.25%, which is approximately double the estimated long-term nominal GDP growth (to reflect a strong growth tailwind until at least 2030).

Given these assumptions, I calculate a base-case target price for Palantir of about $9.45/share, which implies that Palantir could be overvalued by as much as 24.1%.

Author’s EPS estimates and valuation

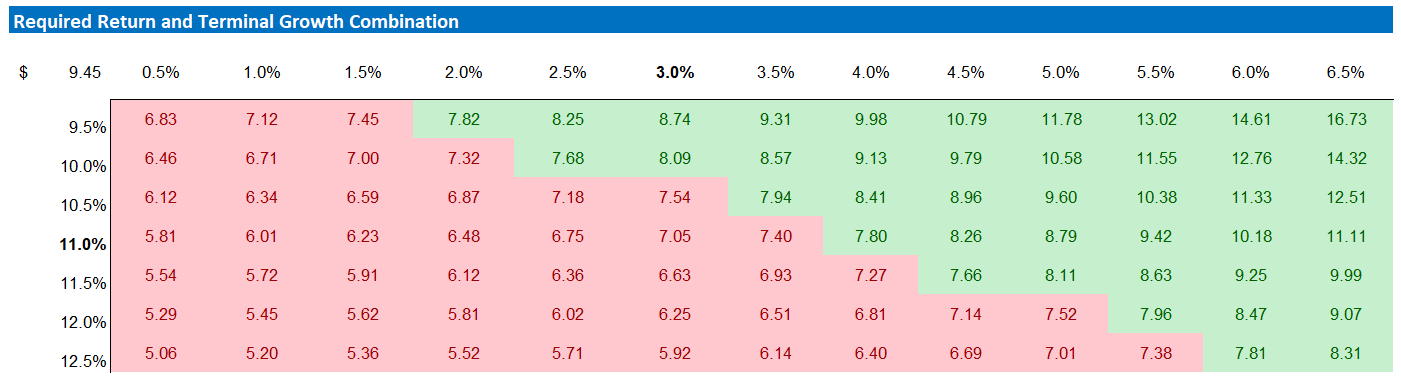

My base case target price does not calculate a lot of upside. But investors should also consider the risk-reward profile. To test various assumptions of Palantir’s cost of equity and terminal growth rate, I have constructed a sensitivity table.

Author’s EPS estimates and valuation

Risks

As I see it, there has been no major risk updated since I have last covered PLTR stock. Thus, I would like to highlight what I have written before:

Investing in Palantir is a speculation, as there is considerable uncertainty related to projecting a company’s fundamentals for multiple years into the future. Moreover, the uncertainty surrounding Palantir’s value proposition adds to the complexity. That said, there is no guarantee that the company will reach my estimated 2030 sales and profitability targets.

Investors should also consider that much of Palantir’s current share price volatility is driven by investor sentiment towards stocks. Accordingly, investors should expect price volatility even though Palantir’s business outlook remains unchanged.

Conclusion

Following Palantir’s stronger than expected Q4 2022 reporting, paired with a strong and profitable outlook for 2023, I continue to like PLTR stock. Investors should consider that the market for data analytics remains in a structural growth trend – with Palantir being well positioned to capture a major share of the $1 trillion market for data management/analytics and business intelligence (2030 estimate).

On the backdrop of arguably reasonable EPS estimates through 2025, a 4.25% terminal YoY growth rate and a 10% cost of equity, I calculate a fair implied share price for PLTR equal to $9.45. Buy.

Be the first to comment