Morsa Images/E+ via Getty Images

Dear Readers/Followers,

Owens & Minor (NYSE:OMI) plays in the medical supply & healthcare sector. This is a highly competitive, low-margin field of business with expertise from many companies across several parts of the world. Nonetheless, legacy OMI managed to eke out a living for itself in an attractive field in the space – until it didn’t and things went south. The company used to be a high-yielder with a well-covered yield of above 4%, but then earnings fell through the floor.

The dividend is still a “zero”, and the visibility for reinstatement is so-so, as is reflected by the way the share price has developed since my last piece.

OMI Article (Seeking Alpha)

Let’s revisit the company and see if we can buy it half as cheap as when I wrote about it last.

Revisiting Owens & Minor

Now, remember. This company used to actually trade in single digits not all that long ago. In 2020, at one point, you could have picked up shares for below $3/share.

Obviously, such an investment would have been a superb RoR, especially if you managed to recognize the peak overvaluation as we went into -21. Equally obviously, this was a massively risky play – which is why I stay out of it, and similar plays such as Tupperware (TUP).

The company isn’t easy to look at. Early 2022 was actually still quite decent, with pandemic-infused growth, which has abated and caused share price declines in the latter half of the year, corresponding with earnings declines.

That being said, the company’s fundamentals are, from a high level, not uninteresting or “bad”. Despite the way the share price has gone, the company remains a business that serves over 4,000 healthcare providers across the world, with its 20,000 employees working with 1,200 branded manufacturers in 400+ facilities.

OMI has a tradition going back 140 years. It’s obvious to me that any company with this tradition would claw and fight against its own demise, as OMI certainly has, and try to hold onto whatever it could. Its relationships and what it has built over its history are neither unattractive nor worthless – the question just is how much it actually is worth.

Typically when faced with such a question, we look at what sort of earnings the company can get from its business and those relationships – and that is unfortunately where things have gone south.

The company still has plenty of revenue – almost $10B on an annual basis to be exact – and gross margins of around 15%, which isn’t bad for the sector, but it also isn’t class-leading or anything close to “amazing”. OMI has been able to grow its company revenues from $8.5B in 2020 to close to double-digits in 2022.

However, the uncertainty and volatility in the earnings flow and how things have gone for the past years have completely thrown investors off the cliff when it comes to forecastability and faith in the business. The company’s management and their opacity haven’t exactly made things easier. The company remains incredibly volatile – as evidenced by the 34.97% drop in a single day after the company dropped forecasts. Need evidence that investors in the company are easily spooked? There you go.

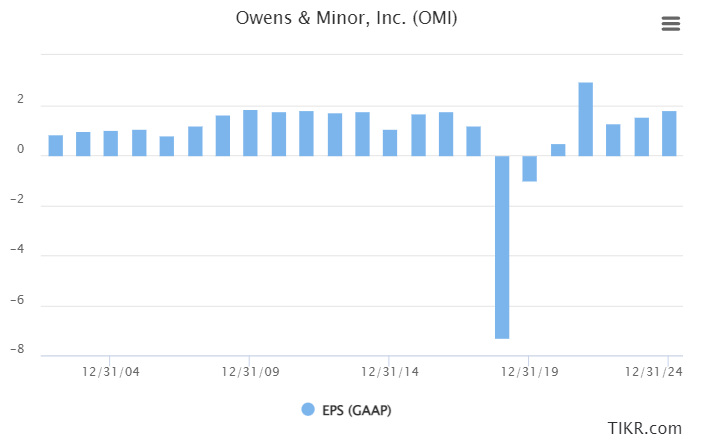

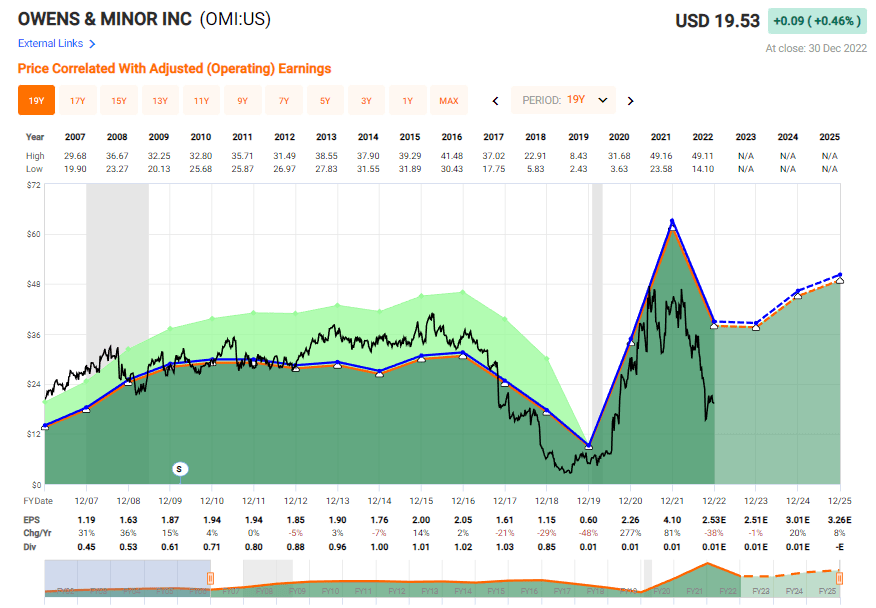

There’s a reason for investors’ fears here. The way OMI crashed was nothing short of spectacular. Take a look at GAAP EPS trends over the past 20 years and the next 2-3 forecasts.

OMI GAAP EPS (TIKR.com)

OMI completely failed to safeguard its fundamental business stability, and no amount of reassurance based on historicals and looking back 140 years can bring that faith back quickly.

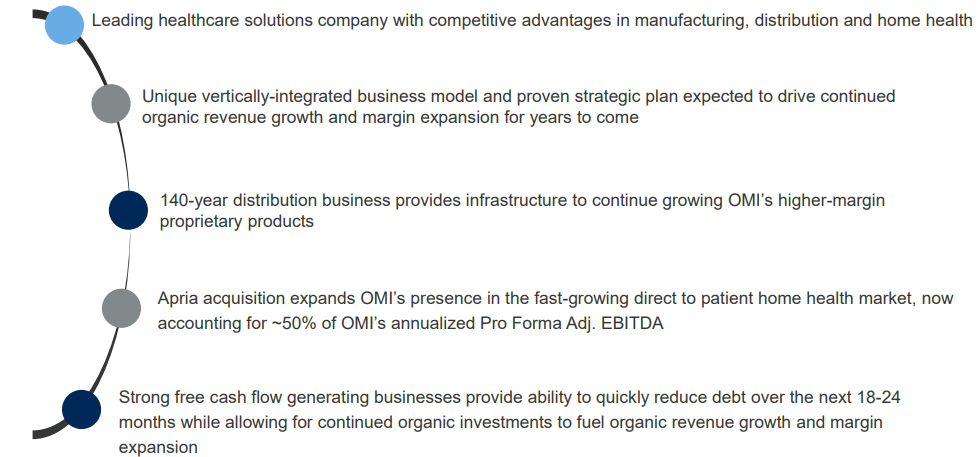

OMI IR (OMI IR)

OMI’s fundamental issues are two-fold. First off, significant debt going into, and already being in a rising interest cycle, coupled with a low-margin business that traditionally has generated FCF/EBITDA margins of below 3%, completed by market and sector volatility as we move in and out of pandemic trends. This neither makes for a stable nor an assuring trend.

OMI is still BB- rated – it’s junk, and fairly low-grade Junk, being closer than farther away from being cut to B+. There is no forecast, despite adjusted earnings coming in decently when the company might start paying a dividend again. Don’t get me wrong, a dividend would be irresponsible here. The company has a close-to 73% LT debt/cap ratio and desperately needs to cut down on debt.

Its Apria M&A puts OMI into a fight for its life, Rambo: Last Blood-style. The new acquisition alone accounts for more than half the company’s Pro-forma annualized EBITDA, and if it can capitalize on this, there’s a very real potential that this company could rise from the ashes.

Because as I said, calling the company “bad” isn’t really valid.

OMI IR (OMI IR)

It’s “distressed” – unfortunately, the degree in which it is distressed is fairly major here, especially going into a rising interest cycle out of a cheap debt cycle, with the pandemic in the US more or less “finished” here. If this had been done 5 years ago and prior to the pandemic, I have no doubt that OMI could have become a blockbuster business and used the excessive flows of cash to quickly pay down debt and prepare for this trend.

However, that is not the case here – and it’s unlikely the company could have M&A’ed Apria under those circumstances anyway.

The company’s fundamental upsides, as they say, remain.

OMI IR (OMI IR)

However, none of these trend upsides are unique to OMI – and there are supply companies much better positioned that don’t share any of this company’s negatives. While Apria might be or might become a strong selling point going forward, there’s a distinct lack of clarity here as to how things might be going.

Some analysts have made what I would call insane PT changes.

Citi today downgraded OMI to Neutral/High Risk and reduced its price target to $18 from $52, to reflect increased risks and lack of management clarity.

(Source: Seeking Alpha news)

To change from that to that, your modeling assumptions have to include a lot of faith and excessiveness that, as I see it, should never have been baked into a financial model given how clear it’s been for literally years that this company is facing fundamental trouble. And if you don’t properly model but rather reach targets by reading a share price graph combined with throwing darts at a wall, then perhaps you shouldn’t be analyzing securities in the first place. I don’t know the specifics of that model, obviously, but looking at my own work, I have a very hard time conceiving how they reached $52 without essentially copy-pasting the most exuberant reports for the pharma industry based on pandemic trends and other things.

That is neither conservative nor, as I view it, realistic.

The cut OMI gave us in October was a harsh one. The non-GAAP forecast is down to $2.60 on the high-end versus around 55 cents higher – and there are issues with the reporting structure which include problems with how distribution/manufacturing flow is quantified, as well as how much exactly the pandemic sales are impacting. The thing is, none of that was unknown before that share price crash. That had already been the case for several quarters running – me, I had it baked into my assumptions already.

Let me show you the valuation and why I view this company the way that I do.

Owens & Minor Valuation

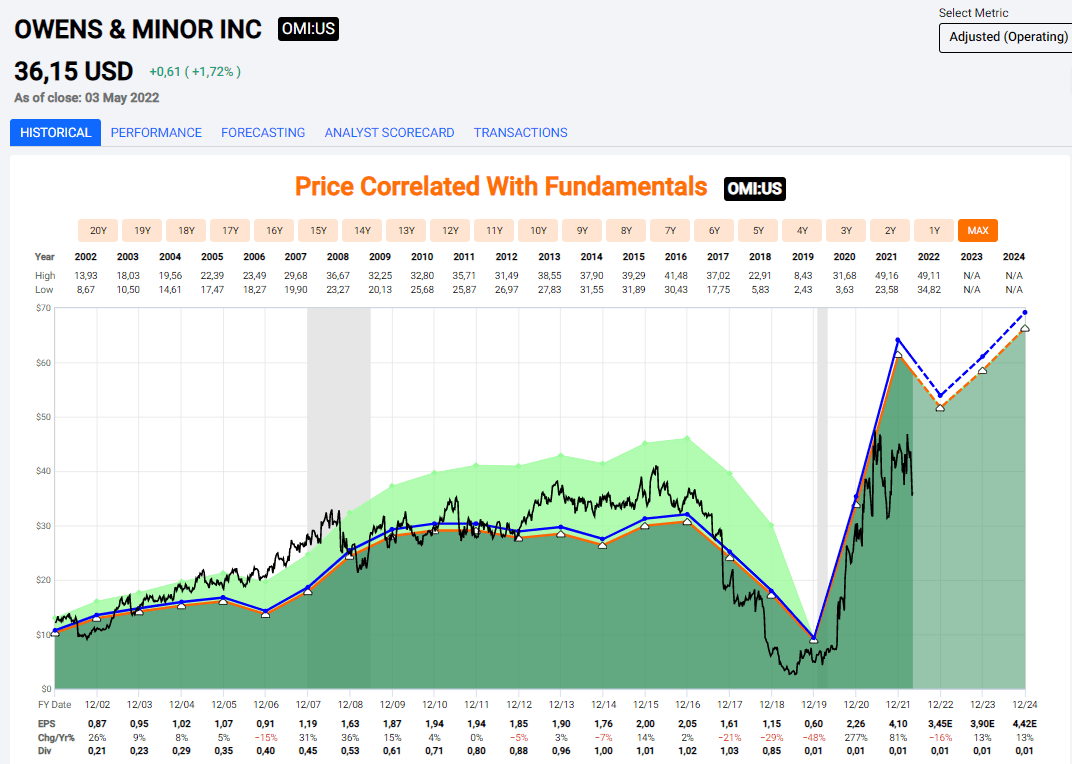

Owen’s & Minor’s valuation chart gives us insight into exactly what happened that caused the company to decline as it did. I want to show you the previous valuation chart from my article 7 months back, to give you an insight in what exuberant and non-conservative expectations can do to you.

OMI valuation May 2022 (F.A.S.T graphs)

So that’s mid-May.

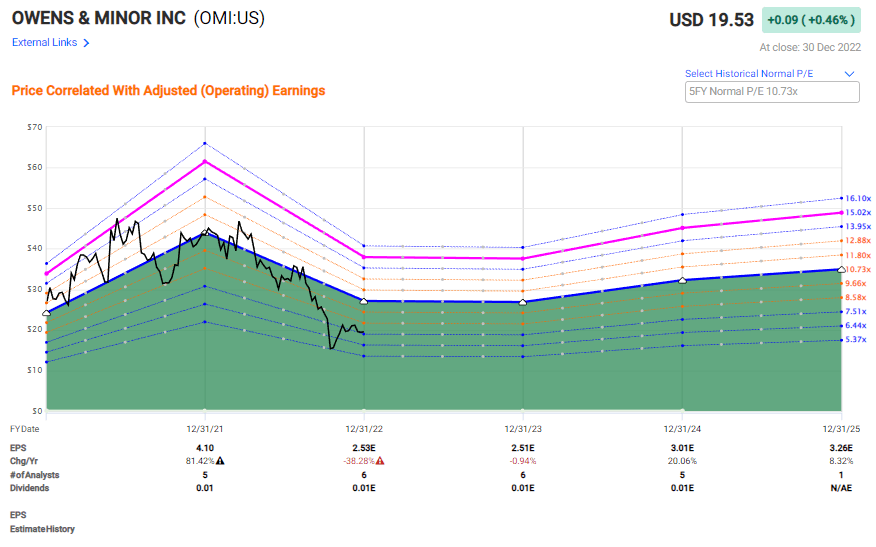

OMI December Forecasts (F.A.S.T graphs)

And that is now. You may notice the slight difference, which obviously has punted the share price down quite a bit. Back 7 months ago, all analyst averages for this company came in between $43-$68/share with averages of $58.8/share.

Boy, that doesn’t really look good 7 months after the fact, does it?

If you recall, my own company PT at the time was $24 – less than half of analysts.

I allowed for the potential of normalization to 15x, but I didn’t really believe in it, because I always err on the side of caution. A 10-15% annual upside is great, but the fact is that we have such upsides in a company with much better overall fundamentals.

When the crash came, I only slightly had to adjust my share price down. Most of what happened were potentials I had already accounted for – but they came in somewhat worse than even I expected.

There is still no implication that the dividend is going to be restored any time soon, which means that the sole upside we’re having here is capital appreciation.

Forecasting this company remains very uncertain – and that is why I heavily discount the company. Fortunately, though, I don’t need to cut my targets by 50-70%, as some of the analysts have done. The current low-end range of the S&P Global PT has gone from $43 to $17, and the high-end has moved from $70 to $23 – again illustrating how these analysts do their job in the short-term.

I have gone from $24 to $19.5, which allows for a potential long-term normalization while still discounting the company at a very healthy level. I do not need to adjust much because I had already accounted for this potential over 8 months ago. 6 analysts follow this business, and out of those, none rate it at an “outperform” or similar rate, with 3 at “HOLD” and several at “underperform”.

OMI valuation (F.A.S.T graphs)

The potential for OMI is still here – that hasn’t changed. But we’re no longer at the market excessively overvaluing the stock. Normalized upside to 10x P/E is around 20% annually here, based on current EPS forecasts, but there’s too much uncertainty baked in for this to be investable in the light of what else is available on the market today.

Thesis

My thesis for OMI is as follows:

- Owens & Minor remains a mostly “broken” company, in the sense that it has no investment-grade credit, no dividend, and troubled history. However, the turnaround is still possible – and I’m curious about a dividend resuming here, and improving fundamentals.

- I consider OMI a “BUY” at $19/share, which makes the company a “HOLD” Today. Even if they drop below $19.5, I would check with the rest of the market before going in.

- While the price target is definitely demanding and conservative, consider for a moment what you’re investing in, and I believe it will make sense to you.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

This company is overall qualitative. This company is fundamentally safe/conservative & well-run. This company pays a well-covered dividend. This company is currently cheap. This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This illustrates the value of my criteria – because when a company does not fulfill at least 3, it cannot be interesting to me. In this case, I want a dividend restoration or some sort of fundamental restoration before I allow for this to convince me into a “BUY”.

Be the first to comment