Maria Symchych-Navrotska/iStock via Getty Images

A Quick Take On Outset Medical

Outset Medical (NASDAQ:OM) reported its Q3 2022 financial results on November 8, 2022, beating revenue and EPS estimates.

The firm is commercializing a new hemodialysis machine for acute care and home settings.

While revenue growth promises to improve in the coming quarters, the company is still producing large operating losses, a distinct negative in the current increasing cost-of-capital environment.

I’m on Hold for OM until management can make significant progress toward operating breakeven.

Outset Medical Overview

San Jose, California-based Outset was founded to design improved hemodialysis technologies to reduce the infrastructure required to operate traditional dialysis machines.

Management is headed by president and Chief Executive Officer Ms. Leslie Trigg, who has been with the firm since November 2014 and was previously in several senior roles at Lutonix, a medical device company acquired by CR Bard.

The company sells its integrated system, called Tablo, which is composed of a console with integrated water purification, a single-use cartridge and Tablo connectivity and data sharing.

The benefit of the system to clinics and other healthcare facilities is that they no longer need a dedicated water cleaning system just for hemodialysis machine purposes.

The firm sells the Tablo system for use in either clinical settings or in the home.

In addition, the firm generates revenue from selling per-treatment consumable products related to its operation as well as services via annual service contracts.

Market and Competition

According to a 2017 market research report by Grand View Research, the U.S. market for hemodialysis and peritoneal dialysis reached $60 billion in value in 2015.

The report forecasts a CAGR of 6.0% from 2015 to 2025.

The main drivers for this expected growth are a rise in the incidence of renal system failure among an aging population and increased availability of services and new devices.

Also, North America accounted for 35% of total revenue in 2015, while the Asia Pacific region is expected to grow at the fastest rate by region through 2025.

U.S. Hemodialysis Market (Grand View Research)

Major competitive or other industry participants include:

Outset’s Recent Financial Performance

-

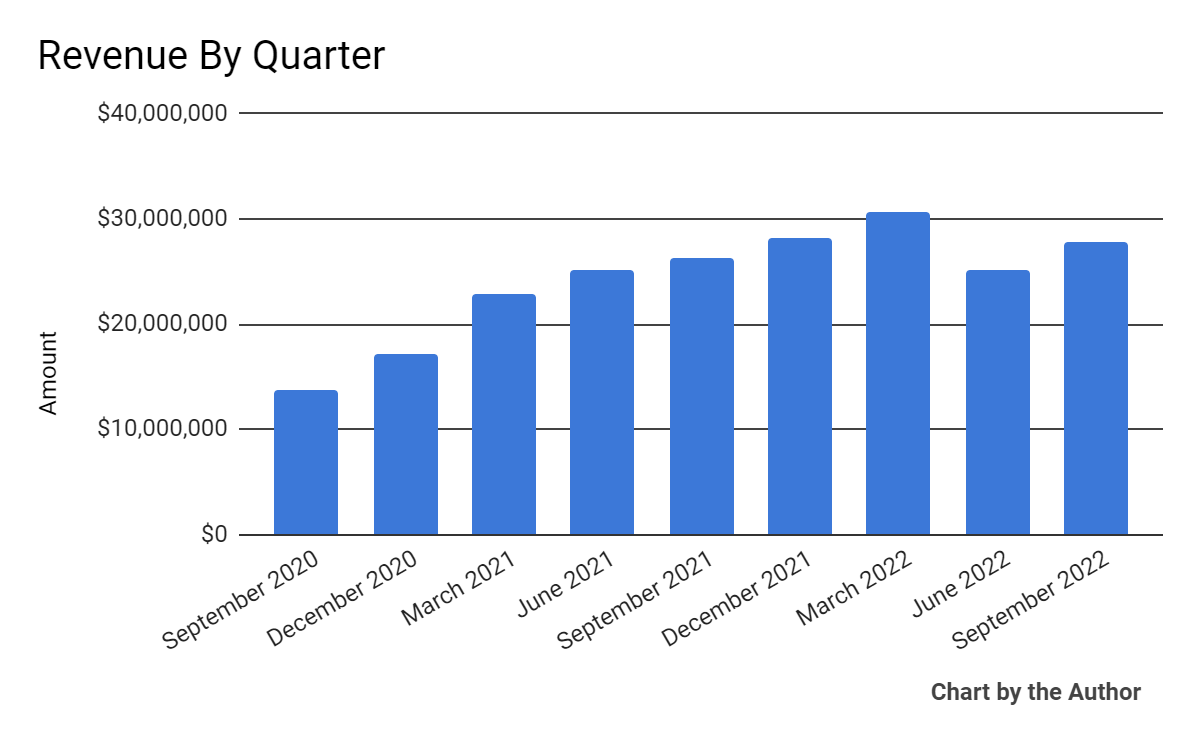

Total revenue by quarter has grown revenue per the following chart:

9 Quarter Total Revenue (Seeking Alpha)

-

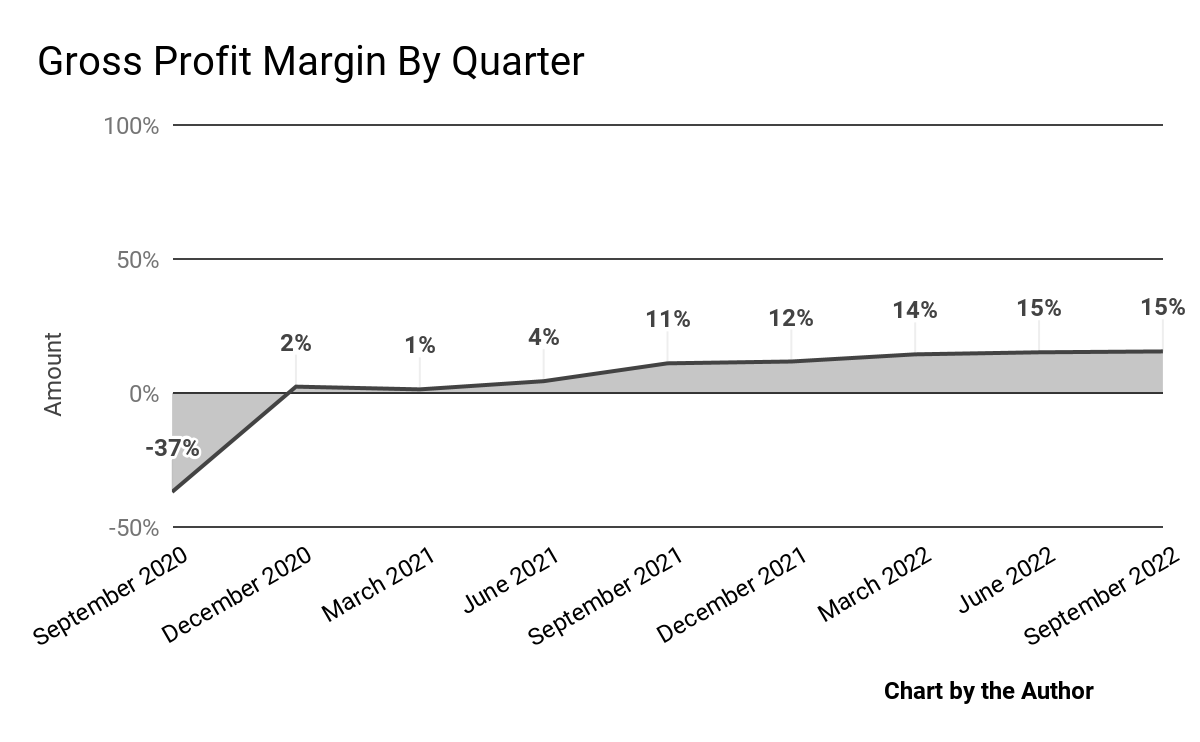

Gross profit margin by quarter has trended higher in recent quarters:

9 Quarter Gross Profit Margin (Seeking Alpha)

-

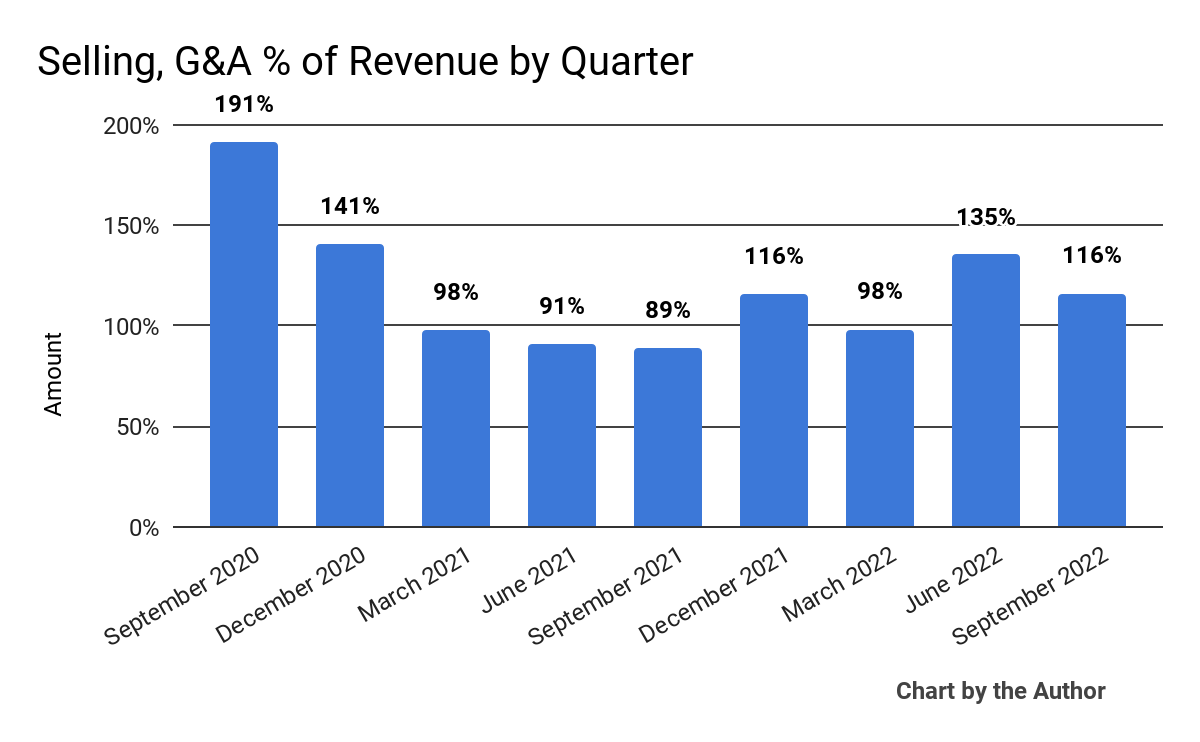

Selling, G&A expenses as a percentage of total revenue by quarter have risen substantially more recently:

9 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

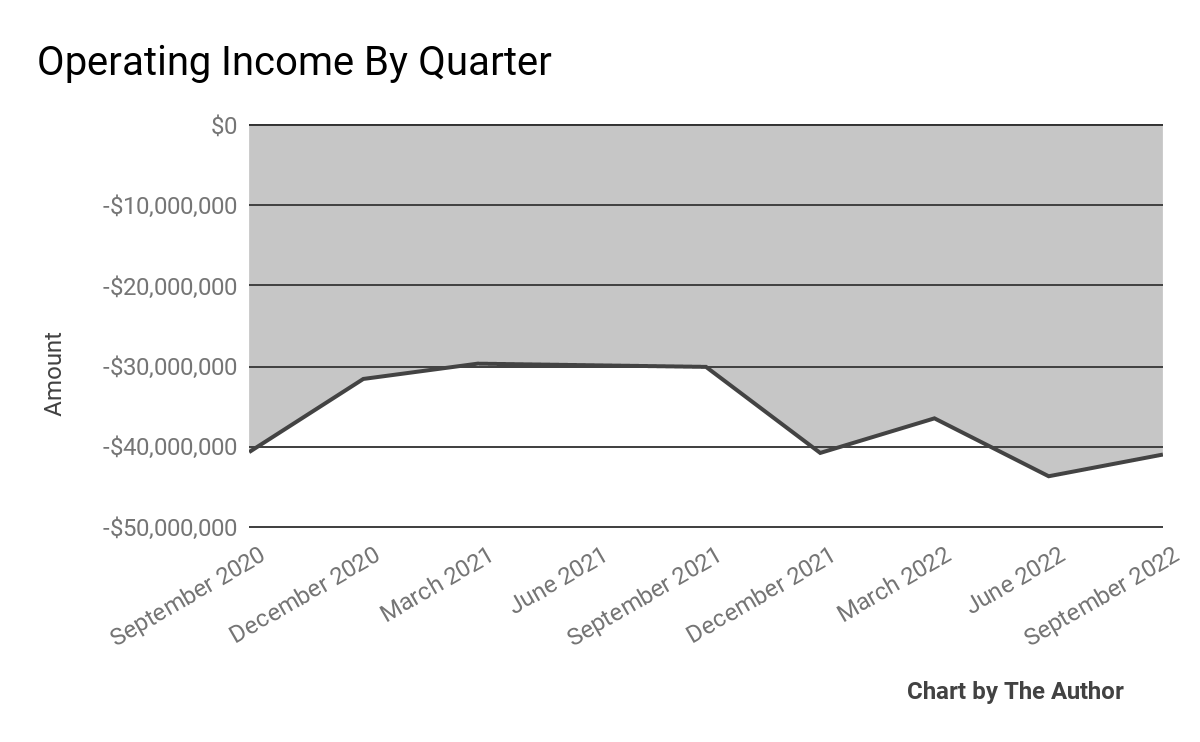

Operating losses by quarter have worsened materially in recent quarters, as shown here:

9 Quarter Operating Income (Seeking Alpha)

-

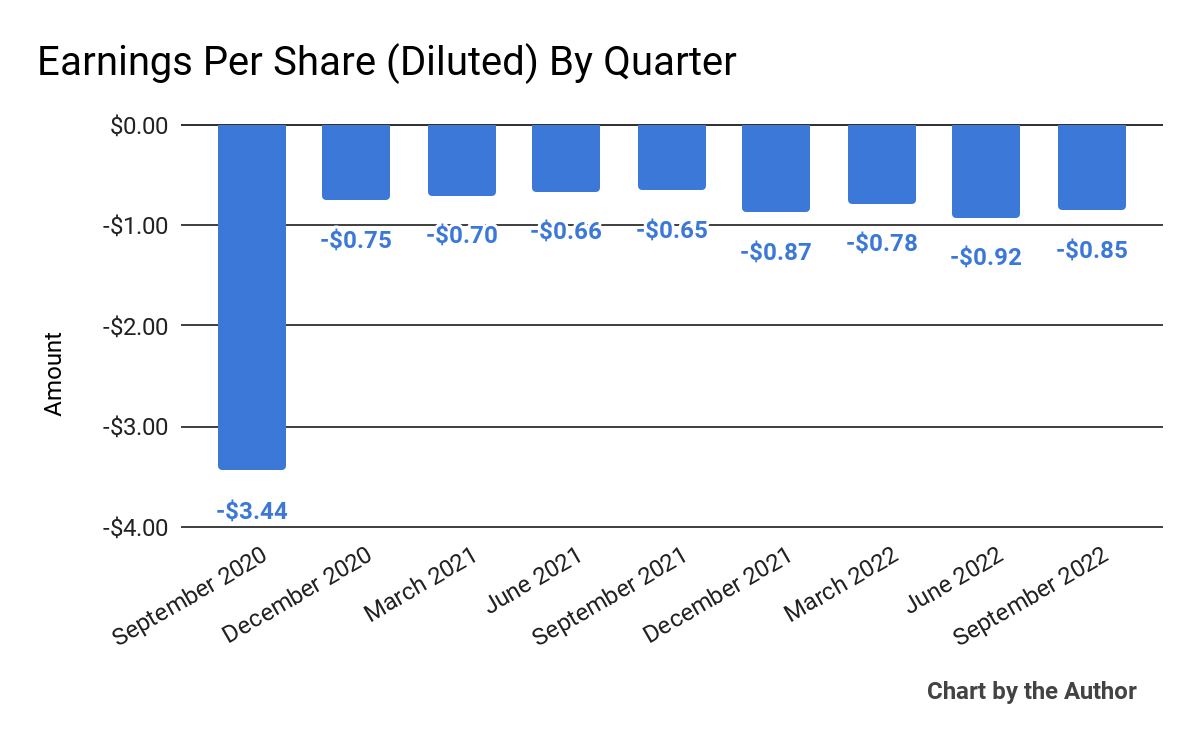

Earnings per share (Diluted) have also deteriorated further into negative territory recently:

9 Quarter Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

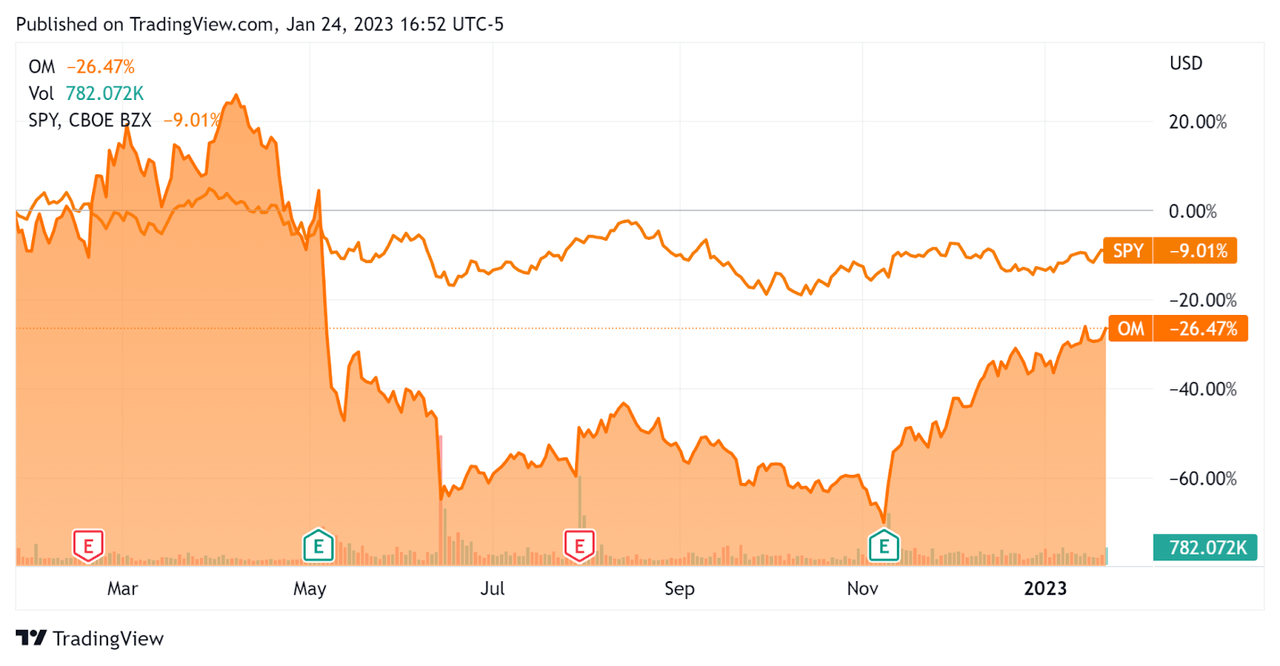

In the past 12 months, OM’s stock price has fallen 26.5% vs. the U.S. S&P 500 index’s drop of around 9%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Outset Medical

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

10.6 |

|

Revenue Growth Rate |

21.6% |

|

Net Income Margin |

-145.9% |

|

GAAP EBITDA % |

-140.6% |

|

Market Capitalization |

$1,366,629,890 |

|

Enterprise Value |

$1,176,140,930 |

|

Operating Cash Flow |

-$143,898,000 |

|

Earnings Per Share (Fully Diluted) |

-$3.42 |

(Source – Seeking Alpha)

Commentary On Outset Medical

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted the doubling of orders for Tablo in the home versus Q3 2021.

The firm entered Q4 2022 with a large backlog of home consultations and expects significant revenue growth from home placements.

A notable win in the acute care space was with a large regional healthcare system of 50 hospitals in nine states.

Another was a Veterans Administration contract awarded during the quarter that now enables the Tablo to be sold into the 106 VA hospitals in the United States.

As to its financial results, total revenue rose only 5.7% year-over-year after the company had previously placed home shipments on hold.

Management characterized Tablo’s retention rate ‘to sit far above the historical retention rates on the home incumbent hemo system.’

Gross profit margin continues to improve, but operating losses have worsened sharply due to growth in headcount, as has negative earnings per share.

For the balance sheet, the company finished the quarter with $227.5 million in cash, equivalents and short-term investments and $29.8 million in long-term debt.

Over the trailing twelve months, free cash used was $151.0 million, of which capital expenditures accounted for $7.1 million. The company paid $24.6 million in stock-based compensation.

Looking ahead, management guided full-year 2022 revenue upward to $112 million at the midpoint of the range, or 9% over the prior year, and subsequently increased that guidance to $115 million, a 12% increase over 2021, if achieved.

However, the industry continues to face nursing shortages which serve as a dampening effect on the firm’s ability to bring new patients online.

Regarding valuation, the market is valuing OM at an EV/Revenue multiple of 10.6x on TTM revenue growth of 21.6%.

The primary risk to the company’s outlook is the industry facing ongoing nursing shortages which serve as a dampening effect on the firm’s ability to bring new patients online.

Notably, OM’s EV/Sales multiple [TTM] has dropped by 29.5% in the past twelve months, although that is much higher than its previous lows, as the chart shows here:

Enterprise Value / Sales Multiple (Seeking Alpha)

A potential upside catalyst to the stock could include a short and shallow macroeconomic downturn in 2023 and faster-than-expected uptake in new hospital and VA center locations.

While the firm’s revenue ramp looks to improve and management believes the company has sufficient capital available for the period ahead, the high and increasing operating losses continue to serve as a caution for me.

Accordingly, I’m on Hold for Outset until the company can make meaningful progress toward operating breakeven.

Be the first to comment