Justin Sullivan

Investment Thesis

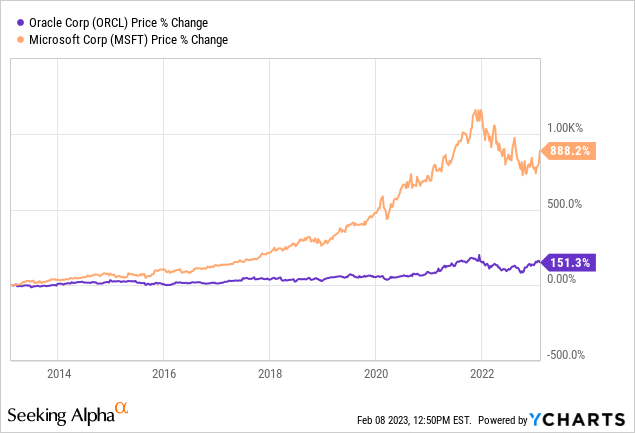

Oracle Corporation (NYSE:ORCL) is one of the world’s most iconic software companies, founded in 1977 by Larry Ellison. However, the company seems to get very little attention nowadays while Microsoft Corporation (MSFT) gets all the spotlight. This is understandable, as it struggled to grow revenue in the past decade and its share price also underperformed the Nasdaq Index and most large-cap tech companies.

I think this may change soon as Oracle is starting to look exciting again. When we think of the cloud, we usually think of Amazon Web Services (“AWS”) (AMZN), Azure, or Google Cloud (GOOG). But Oracle also has a meaningful presence in the space and is benefiting from the strong tailwinds. Its cloud segment is now demonstrating strong traction, and revenue is starting to reaccelerate. Oracle is up over 40% from its 52-week low, yet I still believe it is undervalued. The market is overlooking the potential of its cloud business, which currently accounts for nearly 30% of total revenue. Valuation is also below peers, which provides some margin of safety. I think a successful transition to cloud will unlock meaningful upside potential. Therefore, I rate the company as a buy.

Emerging Cloud Giant

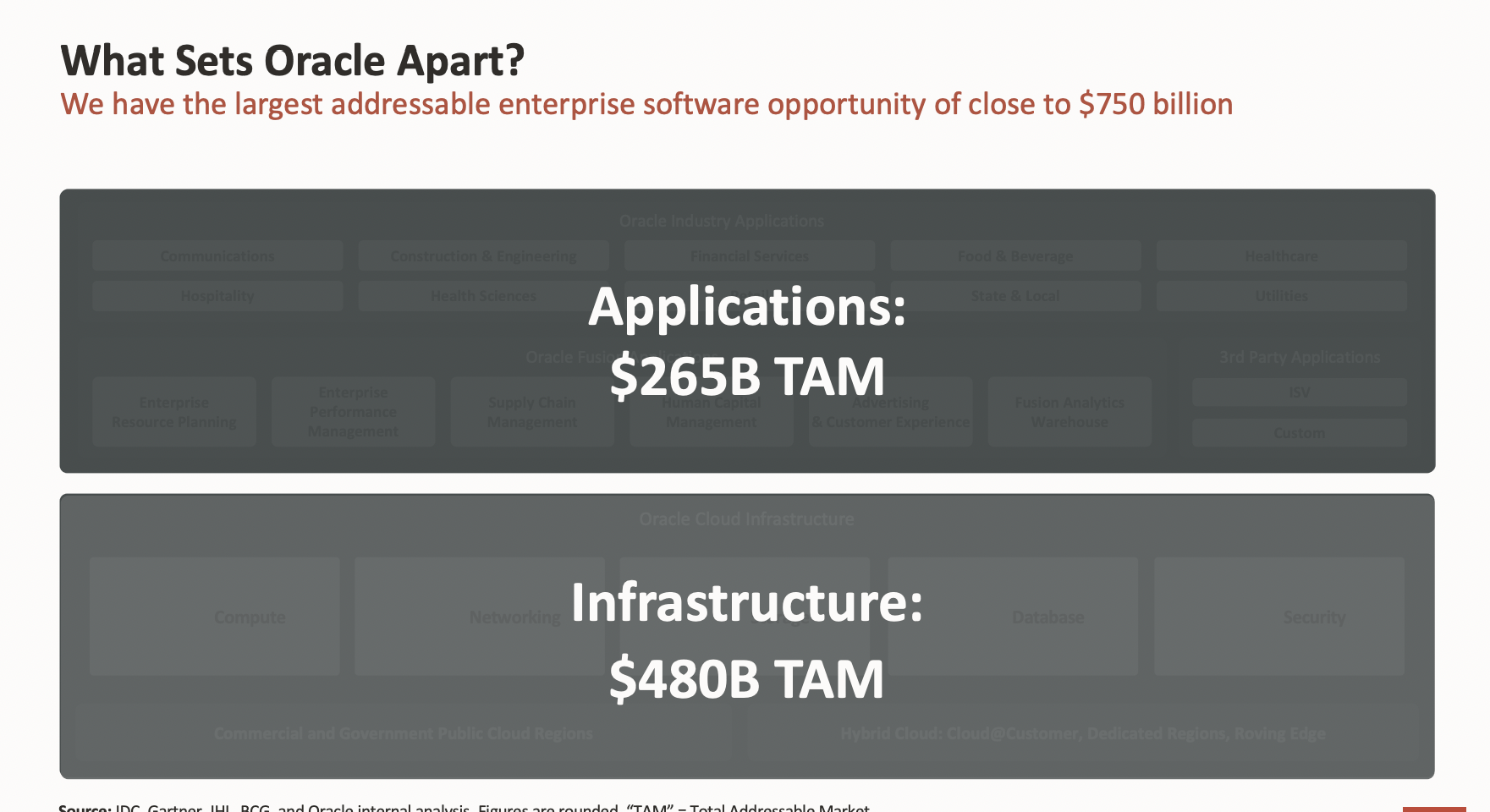

Cloud computing is one of the largest and fastest-growing industries in the world. It is essentially the backbone of the digital world. According to MarketsandMarkets, the global TAM (total addressable market) of cloud computing is forecasted to grow from $545.8 billion to $1.24 trillion by 2027, representing a CAGR (compounded annual growth rate) of 17.9%. Oracle themselves are slightly more conservative and estimates the TAM to be around $750 billion, with application accounting for $265 billion while infrastructure accounts for $480 billion.

Oracle

Digital transformation and IoT (Internet of Things) are driving the expansion of the cloud. We are seeing increased adoption of newer technologies such as AI (artificial intelligence) and a lot more products such as vehicles are now digitally connected. This is only made possible thanks to cloud computing, as it vastly improved productivity and flexibility. For instance, chip designer NVIDIA Corporation (NVDA) has moved a lot of its AI and ML (machine learning) workload to Oracle Cloud.

Larry Ellison, Chairman, on NVIDIA:

NVIDIA has moved and a bunch of others have moved, lots of AI, artificial intelligence and machine learning workloads to the Oracle Cloud because it turns out we’re really good at that. We’re better than that than any of the other clouds, which may surprise some people.

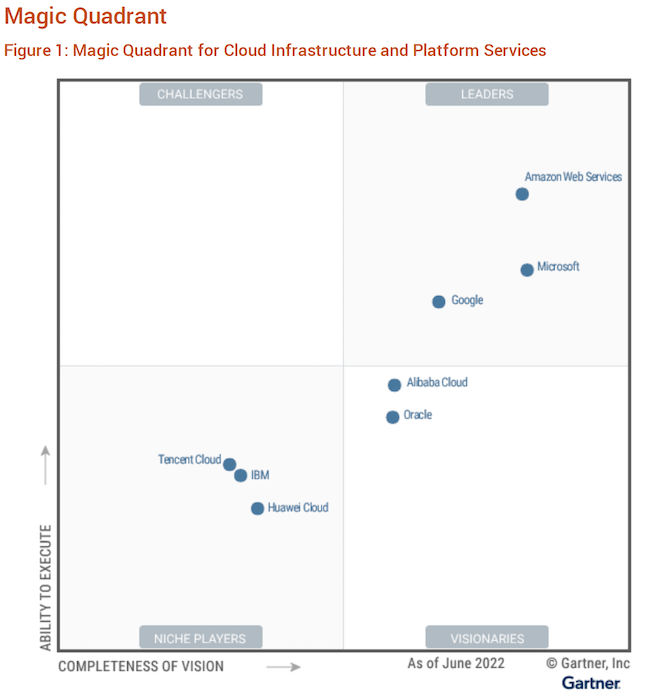

Oracle cloud has been seeing strong traction, and it now accounts for 30% of total revenue compared to just 20% in FY20. Cloud revenue growth has also accelerated from 13% in FY20 to 43% in the latest quarter. We are only in the early innings as the company has over 430,000 customers, yet only 45,000 are using its cloud application and 18,000 are using its cloud infrastructure. The opportunity to cross-sell cloud offerings to existing customers alone is already massive. In order to manage higher usage rates, the company has also been expanding its infrastructure footprint and now has the most global locations among hyperscalers. Oracle Cloud is currently the fifth-largest cloud, behind the big three and Alibaba Cloud (BABA). There are still some ways to go, but I believe Oracle will eventually move up to the leader category as well.

Gartner

Financials

Oracle’s latest earnings results are very impressive as cloud successfully re-ignited growth. The company reported revenue of $12.3 billion, up 18% YoY (year over year) from $10.36 billion. On a constant currency basis, revenue was up 25%. The growth was largely driven by the strong momentum in the cloud segment. Total cloud revenue (infrastructure+application) was $3.8 billion, up a whopping 43% YoY compared to $2.8 billion. The segment now accounts for 30.9% of total revenue. Infrastructure (IaaS) revenue was up 53% YoY to $1 billion while application (SaaS) revenue was up 40% YoY to $2.8 billion. Oracle Cloud revenue growth has outpaced Azure, AWS, and Google Cloud this quarter and continues to accelerate, while others are starting to see a slowdown.

The company’s existing reach is already massive, so it does not need to spend much on S&M (sales and marketing) expenses. It only has to convert existing customers into cloud users. S&M expenses this quarter only increased by 13.4% despite revenue being up 20%. This benefited the bottom line substantially, and the company reported an operating income of $3.07 billion, compared to a loss of $824 million in the prior year. Non-GAAP EPS was $1.22 compared to $0.44, or a 177% increase. The operating margin was 25%. The company expects its operating margin to grow over time as it continues to benefit from strong operating leverage.

Cheaply Valued

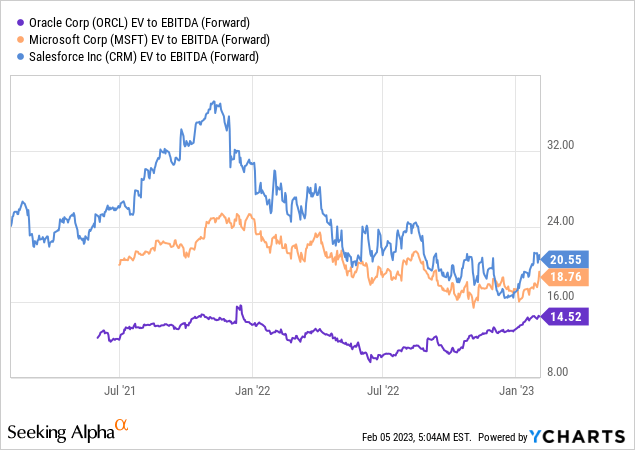

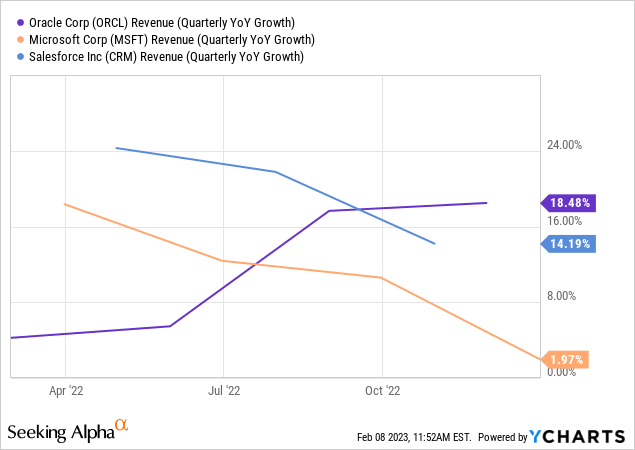

Despite the 40% run-up in share price since October, Oracle’s valuation is still attractive in my opinion. It is currently trading at an fwd EV/EBITDA ratio of 14.5x, which is very cheap considering its growth(I am using the EV/EBITDA ratio because it can also take the debt into account). From the first chart below, you can see that this is way below large-cap software companies such as Microsoft and Salesforce (CRM), which has an average fwd EV/EBITDA ratio of 19.2x. Oracle is trading at a 32.4% discount, yet its revenue growth is actually the highest, as shown in the second chart below. I think the valuation gap is too big and the market is still valuing Oracle as a legacy software company. I believe we will see an upward revision in multiples as the market realize Oracle’s turnaround, which should offer meaningful upside potential.

Investor Takeaway

I believe Oracle is an underrated cloud play. The company is not known for its cloud offerings, but cloud revenue now represents over 30% of total revenue and continues to grow rapidly. The TAM for cloud computing is massive and there are still tons of opportunities out there to be captured. This, alongside ongoing tailwinds, should help Oracle maintain strong and durable growth rates in the long run. The company is also showing solid operating leverage, and margins should go higher over time, which will boost the EPS figure.

The current Oracle Corporation valuation is very cheap when you consider the market opportunities and growth rates it is reporting. Oracle is significantly discounted compared to peers, and an upward revision in multiples to peers’ average will offer decent upsides. I like the risk-to-reward ratio here, therefore I rate Oracle Corporation as a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment