wellesenterprises/iStock Editorial via Getty Images

Investment Thesis

Oracle Corporation (NYSE:ORCL) beat on the top and bottom line for fiscal Q4 and investors positively cheered the stock that had already increased 80% in the past twelve months.

Clearly, Oracle’s cloud applications and infrastructure businesses which grew by 50% y/y at constant currency stole the show. But beyond the headlines, as we look through its financial results with considerable attention to detail, I’m not convinced that paying around 17x forward earnings for a highly leveraged business, which relies substantially on its balance sheet for future growth, is all that enticing.

So I’m going to remain neutral on this name for now.

Why Oracle? Why Now?

Oracle provides enterprise IT solutions, infrastructure, and hardware. Through its cloud services and hardware, Oracle offers rapid deployment and connectivity.

Oracle seeks to deliver flexible deployment models, such as on-premise and cloud-based, to cater to customer needs. In a nutshell, Oracle offers software and hardware solutions so companies can manage their computer systems.

Moving on, Oracle used the opportunity of its earnings report to remind the investment community that Nvidia Corporation (NVDA) is using Oracla’s GPU clusters. See below,

Oracle’s Gen2 Cloud […] has the highest performance, lowest cost GPU cluster technology in the world. NVIDIA themselves are using our clusters […]

Recall, Oracle had already rallied more than 20% in the past 30 days as investors positively welcomed any opportunity to pick up ”yet another business” that will benefit from AI.

And true to form, Oracle didn’t waste any time and rapidly made its mandatory salutations to the ”AI-like” gods and the stock pressed forward at a rapid clip and jumped a further 5% after hours.

Next, let’s get further into the financials details, noting both the good and the bad considerations.

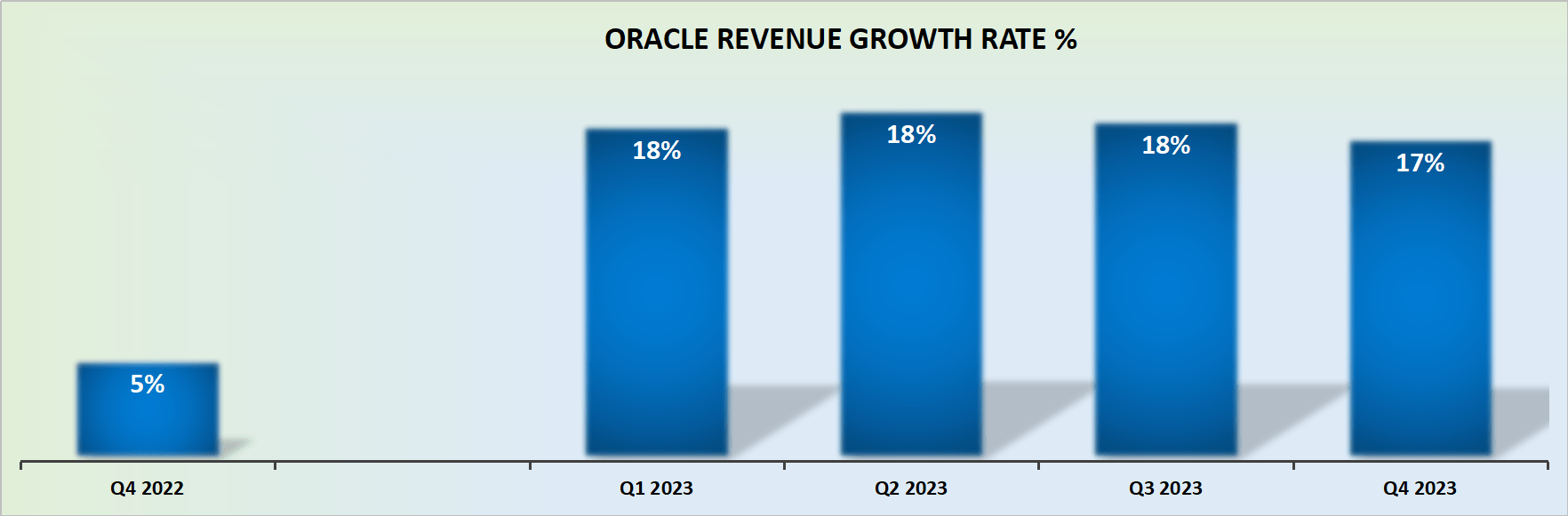

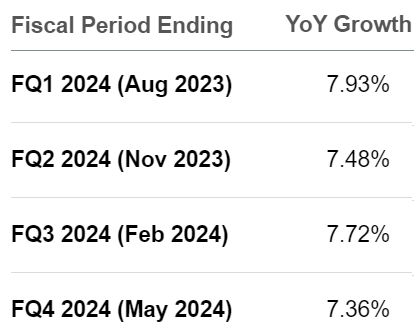

Revenue Growth Rates Could Decelerate to 10% CAGR

ORCL revenue growth rates

Oracle managed to beat analysts’ fiscal Q4 2023 consensus revenue estimates. Given that it’s been a long while since Oracle could be counted on as a reliable and consistent ”top-line beater,” this revenue beat was nicely welcome by investors.

On the other hand, one could make the case that for fiscal Q4 2023, Oracle was up against relatively easy comparables. The big question now is what will fiscal 2024 shape up to be.

SA Premium

As it stands right now, analysts are expecting Oracle’s revenue to grow in the high single digits.

Even if Oracle manages to somehow positively impress investors and grow at 10% CAGR in fiscal 2024, I’m not sure that this is in actuality rapid enough revenue growth rate to keep investors positively enthused over its near-term prospects. Irrespective of how many times Oracle mentions AI.

Looking Beyond its Revenues

The bull case here no doubt points to Oracle’s cash flows, which jumped by 80% y/y in fiscal 2024.

The bad news is that Oracle was extremely acquisitive throughout fiscal 2023. Consequently, this left its balance sheet with approximately $80 billion of net debt.

In other words, Oracle will have its work cut out over the next twelve months if Oracle wishes to grow its AI operations, pay down its debt, and payout more than $3.5 billion towards its growing dividend.

I’m not saying that Oracle will struggle on any of those matters. But at the same time, it’s difficult to believe it will be particularly easy.

For instance, as a point of reference, it’s worthwhile noting that Oracle spent about $950 million in interest payments in fiscal Q4 2023. Meaning that on an annualized basis, Oracle is likely to spend more in interest payments on its debt over the next twelve months, than it will be able to payout on its dividend.

The Bottom Line

Oracle Corporation reported strong financial results, with its cloud applications and infrastructure businesses experiencing significant growth.

However, considering the company’s high leverage and reliance on its balance sheet for future growth, paying a relatively high forward earnings multiple may not be attractive.

While investors have been optimistic about Oracle’s prospects in AI and its cash flow growth, the company’s substantial net debt and the challenge of simultaneously growing its AI operations, paying down debt, and maintaining dividends pose potential difficulties. Overall, I remain neutral on Oracle Corporation stock for now.

Be the first to comment