Vladimir Zakharov

I’m sure you’ve heard the saying before, “good things come in small packages”.

The simplicity of that idiom is that bigger is not always better and sometimes it pays to own the smaller things in life.

I’m 6′ 3” inches so it’s kind of hard for me to drive small cars, so that doesn’t apply.

Also, whenever I travel, I always insist on a King size bed and an exit row seat on the plane.

I’ve been going to the gym a lot lately, which means I have a big appetite, so it’s difficult for me to live off yogurt and oatmeal.

When it comes to stocks, I also gravitate to the big fish in the sea, companies with large liquidity and broad portfolio diversification.

Names like Realty Income (O), American Tower (AMT), and Camden Property Trust (CPT) come to mind.

However, there are always exceptions to the rule…

Today, I’m proud to say that iREIT™ is re-introducing small cap REIT coverage.

For years on Seeking Alpha we provided our readers with research on many small cap REITs but we opted to focus on the higher quality names during Covid-19.

However, as our service has grown (and we added new analysts) we decided that it was time to crank it back up again, especially given the wide discounts we’re seeing in the market these days.

Prior to Covid-19, our small cap portfolio delivered annual returns in excess of 40% (2014-2019) and we believe that we can mirror that success record, given our bandwidth in the REIT sector.

So without further ado, let’s dive into some small cap REITs…

Whitestone REIT (WSR) – Market Cap: $474.98 million

Whitestone is an internally managed REIT that specializes in open-air retail shopping centers with a focus on service-oriented tenants including grocery stores, restaurants, health and fitness centers, educational, and financial services.

As of year-end 2022, WSR’s portfolio consists of 57 properties that cover approximately 5.1 million gross leasable square feet and have an occupancy rate of 94%. The majority of their properties are located in 5 markets within 3 states with their largest concentration being in Houston and Phoenix.

In total they have twenty five shopping centers in Scottsdale and Phoenix, fourteen shopping centers in Houston, nine shopping centers in Dallas, five shopping centers in Austin, three shopping centers in San Antonia, and one shopping center in Buffalo Grove, Illinois. 93% of their properties are structured under a triple-net lease agreement with a weighted average lease term of approximately four years.

Additionally, WSR has no more than 2.5% exposure to any one tenant.

WSR – IR

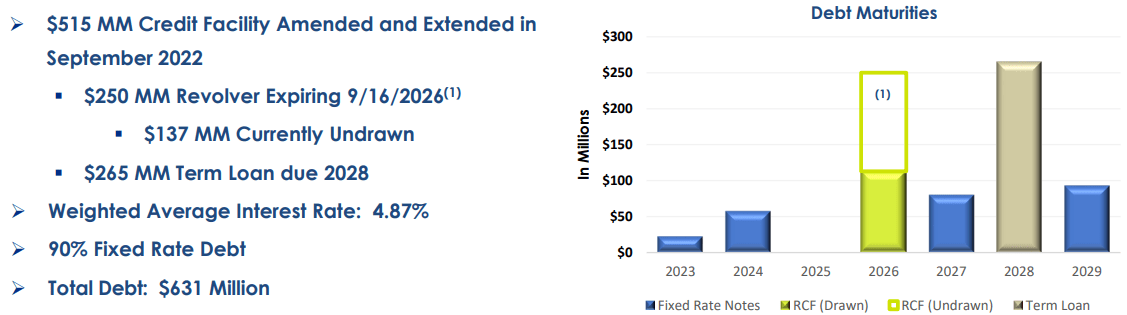

Whitestone REIT has a relatively high amount of debt with a net debt to EBITDA of 7.85x, an interest coverage ratio of 2.91x, and a long-term debt to capital of 58.21%. In their latest earnings release WSR provided 2023 guidance for net debt to EBITDAre to range between 6.9x and 7.3x.

They have $631 million in total debt that is 90% fixed rate and has a weighted average interest rate of 4.87%. They have minimal debt maturing in 2023 and $137 million available to them under their revolving credit facility.

WSR – IR

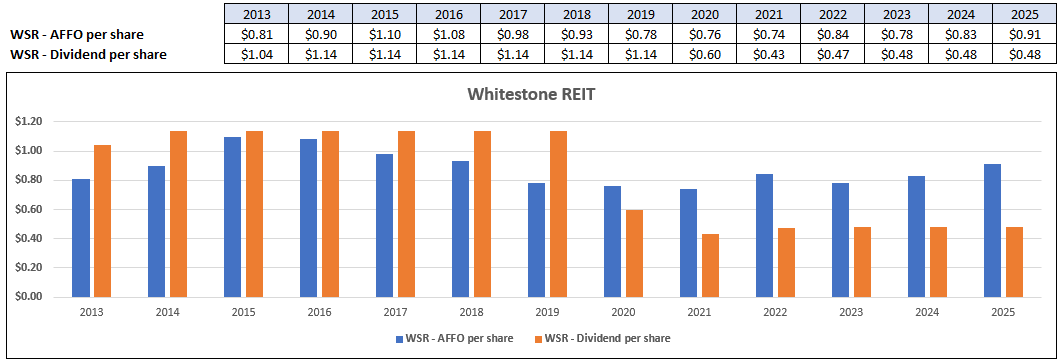

Whitestone REIT increased its AFFO per share from 2013 to 2015, but AFFO per share declined from 2017 to 2021. AFFO increased by 13% in 2022 but analysts expect AFFO to fall by -7% in 2023 before rebounding with expected increases of 7% and 10% in the years 2024 and 2025 respectively.

WSR increased its dividend in 2014 from $1.04 to $1.14 but maintained the same rate up until 2019. In 2020 WSR cut their dividend by -47.37% and then by -28.75% the following year. The dividend was increased in 2022 to $0.47 per share and analysts expect a dividend rate of $0.48 per share for the next several years. I recently spoke with the company’s CEO at REIT week, watch the video here as he discusses the dividend.

You can watch the entire interview at iREIT™ on Alpha.

FAST Graphs (compiled by iREIT)

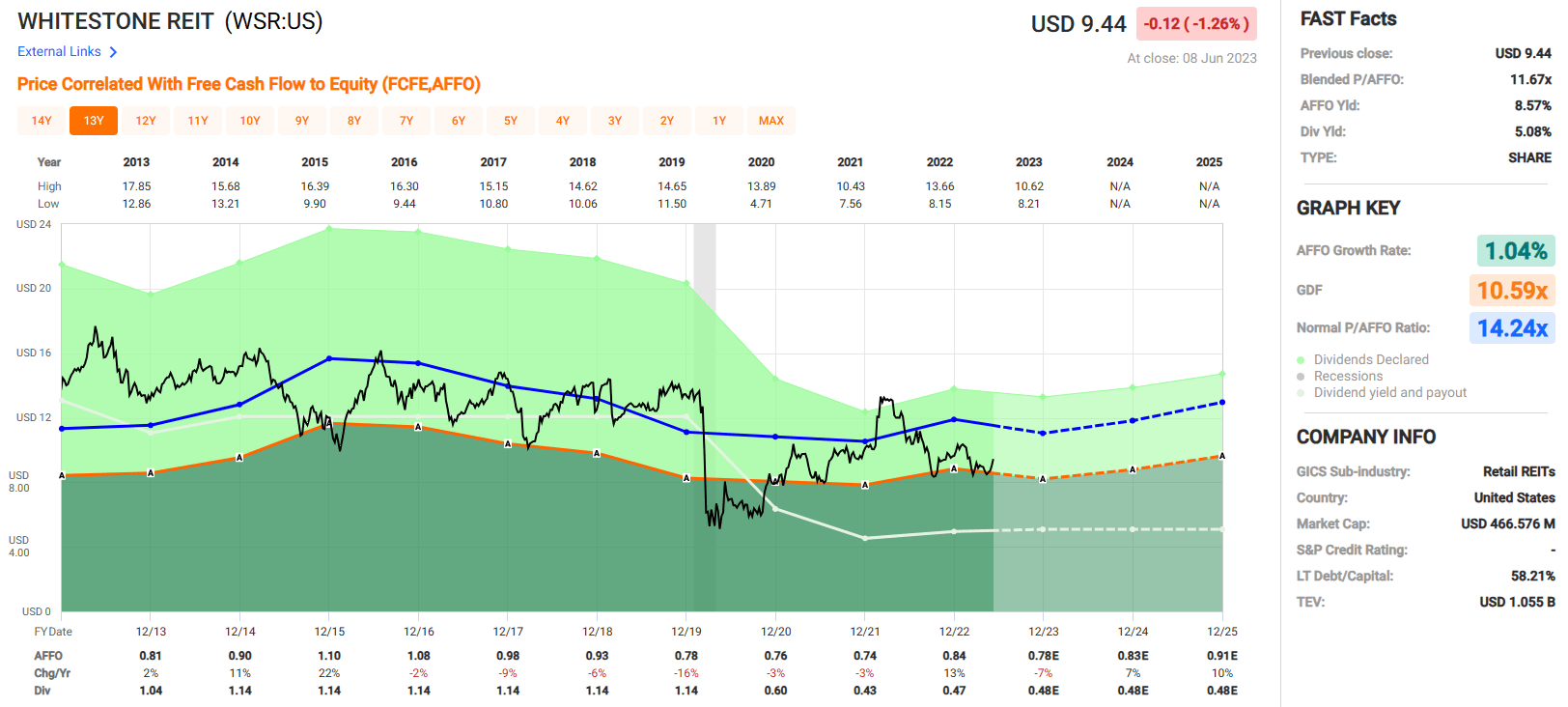

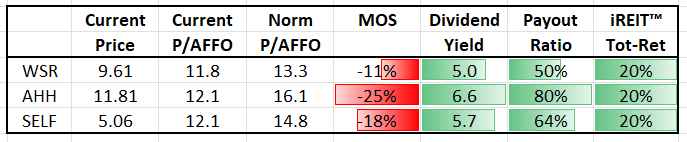

Whitestone REIT pays a 5.08% dividend yield that is well covered with an AFFO payout ratio of 55.99% and trades at a P/AFFO of 11.67x which compares favorably to their normal AFFO multiple of 14.24x. Given its current valuation we rate Whitestone REIT a Spec BUY.

FAST Graphs

BSR Real Estate (OTCPK:BSRTF) – Market Cap: $745.39 million

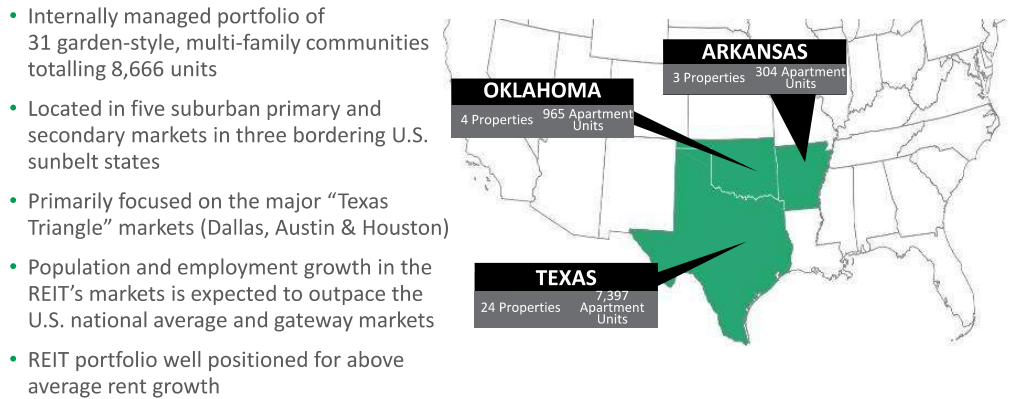

BSR Real Estate is an internally managed REIT that specializes in multifamily properties in the Sunbelt region of the U.S. Their portfolio consists of 31 multifamily properties that contains a total of 8,666 apartment homes. BSRTF properties are primarily located in Texas with 24 multifamily communities that contains 7,397 apartments units.

Additionally, they have 4 properties in Oklahoma that contains 965 apartment units, and 3 properties in Arkansas that contains 304 apartments units. Within Texas, their largest concentration of properties are located in Dallas, Austin, and Houston.

BSR – IR

In total, their portfolio of multifamily properties has an average monthly rent of $1,489, an occupancy rate of 95.9%, a new lease growth rate of 0.2%, and a renewal lease growth rate of 7.7% as of the first quarter in 2023.

BSR – IR

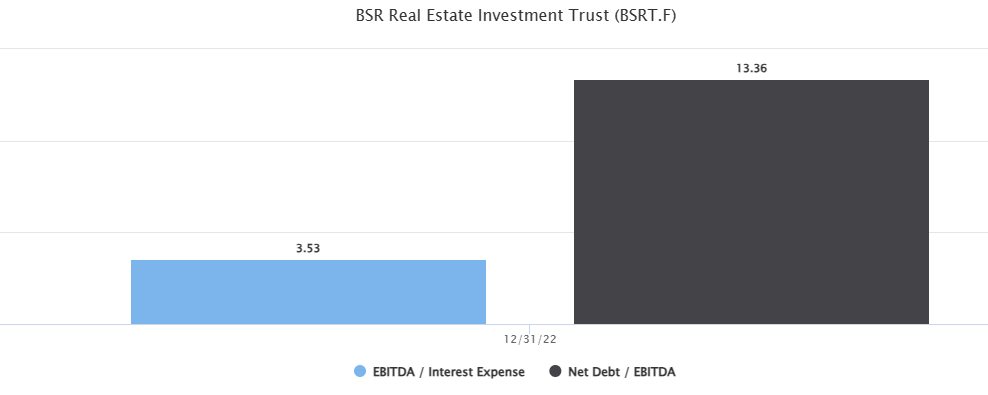

BSR Real Estate has a net debt to EBITDA of 13.36x, which is higher than I’d like to see and an interest coverage ratio of 3.53x.

Source: TIKR.com

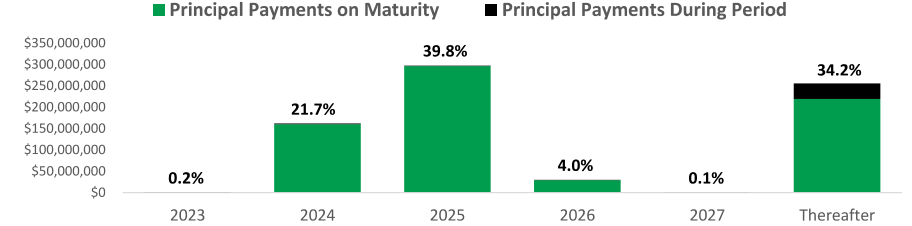

97% of their debt is either fixed rate or hedged and has a weighted average mortgage term to maturity of 4.9 years and a weighted average interest rate of 3.3%. They have minimal maturities due in 2023, but 21.7% of their debt matures in 2024 and approximately 40% of their debt matures the following year.

BSR – IR

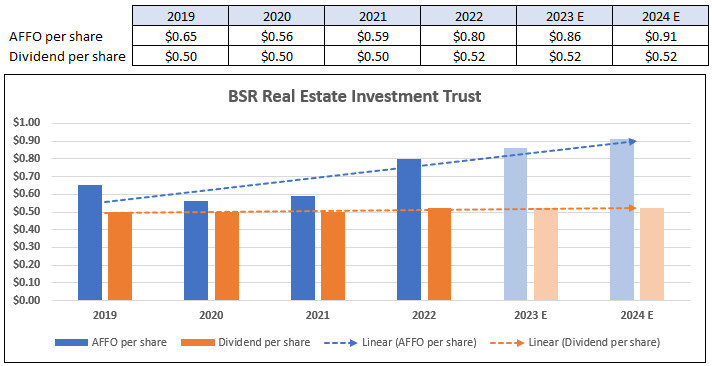

BSRTF’s AFFO per share fell from $0.65 in 2019 to $0.56 in 2020 for a -14% decline. Since that time they have delivered positive AFFO growth and in 2022 AFFO increased by 36%. Analysts expect AFFO per share to increase 7% in 2023 and 6% in 2024. The dividend remained at $0.50 from 2019 to 2021 but was increased by 3.52% in 2022 to $0.52 per share.

FAST Graphs (compiled by iREIT)

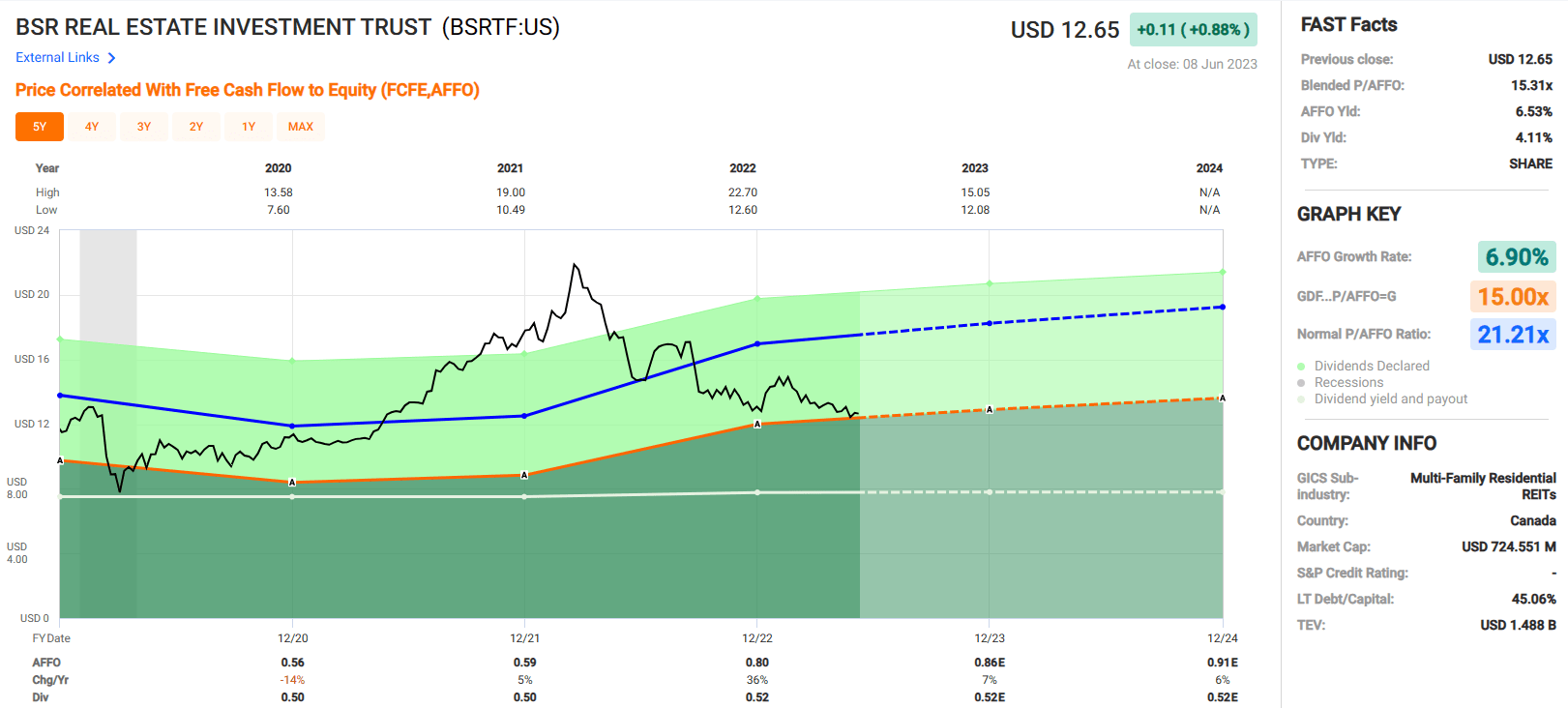

Since 2020, BSRTF has an average AFFO growth rate of 6.90% and an average dividend growth rate of 1.17%. They pay a 4.11% dividend yield that is well covered with an AFFO payout ratio of 64.75%. Currently the stock is trading at a P/AFFO of 15.31x which is well below their normal AFFO multiple of 21.21x.

BSRTF is not currently within our coverage universe, but I would be hesitant to initiate a position due to their levels of debt and the anemic dividend growth over the past several years.

FAST Graphs

Global Self Storage (SELF) – Market Cap: $56.39 million

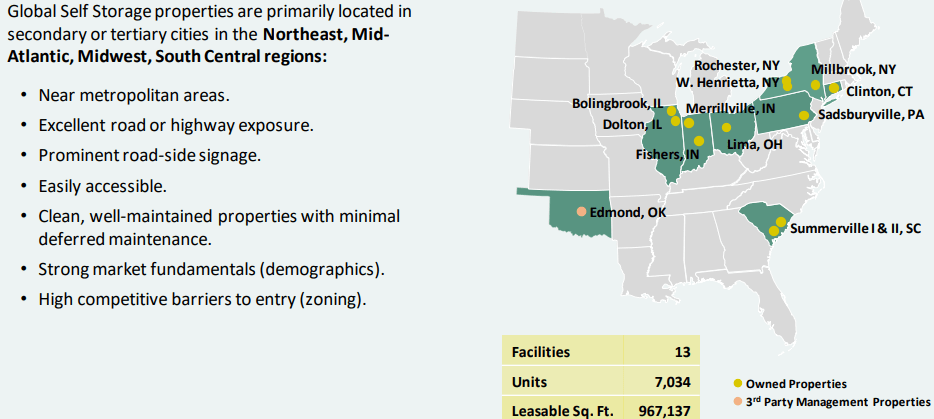

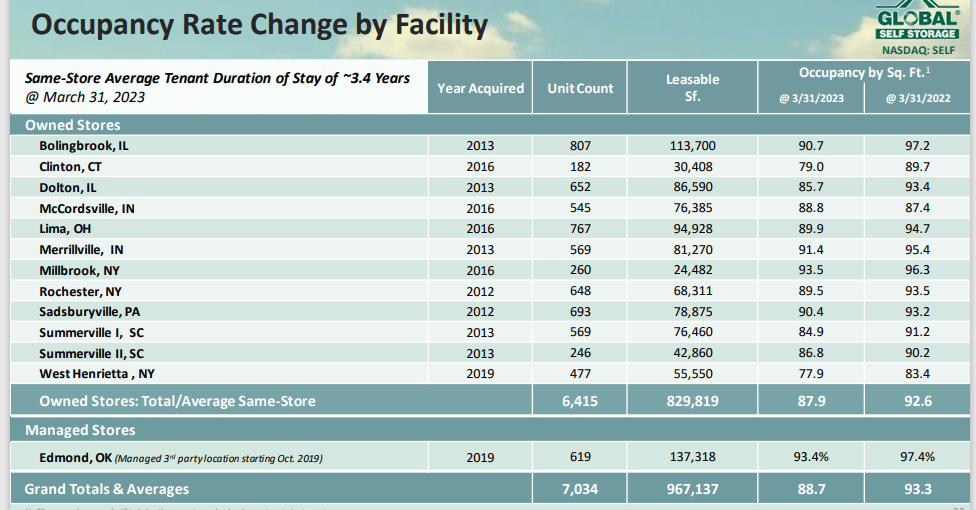

Global Self Storage is an internally managed REIT that specializes in self-storage properties within the U.S. As of year-end 2022, SELF owned or managed 13 properties located in 8 states that contain 7,034 self-storage units and covers 967,137 square feet of leasable space.

59% of SELF’s properties are traditional drive-up storage units, 33% of their properties are climate-controlled units, and 8% of their properties contain both covered and outside RV and boat storage.

SELF – IR

SELF’s properties are primarily located in secondary and tertiary markets in the Mid-Atlantic, Northeast, Midwest, and South Central regions of the U.S. Their same-store average tenant duration is approximately 3.4 years, and their average occupancy rate is 88.7%, down from an occupancy rate of 97.4% for the same period in the prior year.

SELF – IR

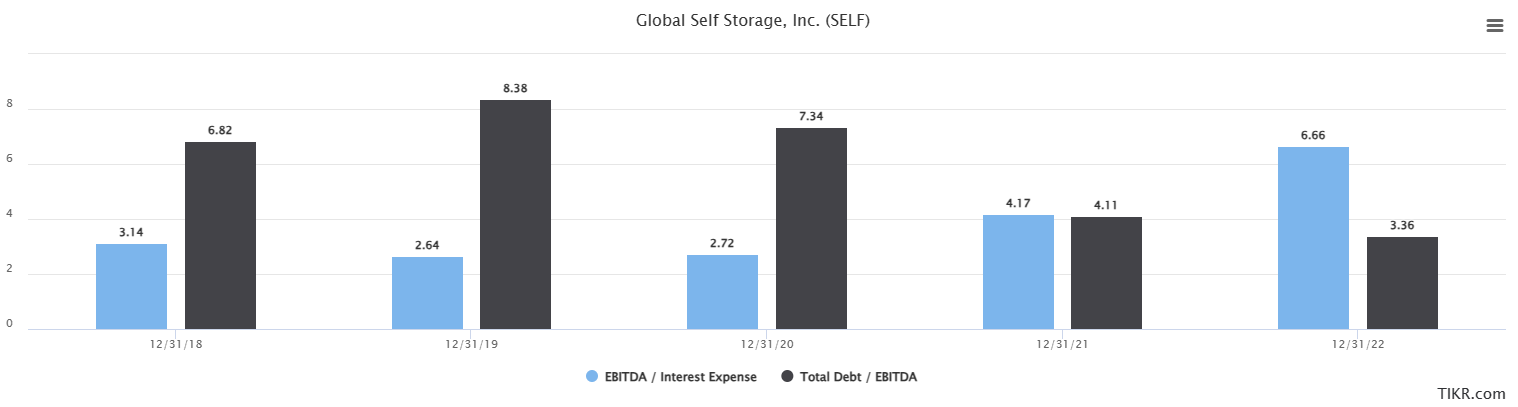

SELF has excellent debt metrics with a long-term debt to capital ratio of 25.68%, a total debt to EBITDA of 3.36x and an interest coverage ratio of 6.66x. They have significantly improved these metrics since 2018 when their debt to EBITDA was 6.82x and their interest coverage ratio was 3.14x.

Source: TIKR.com

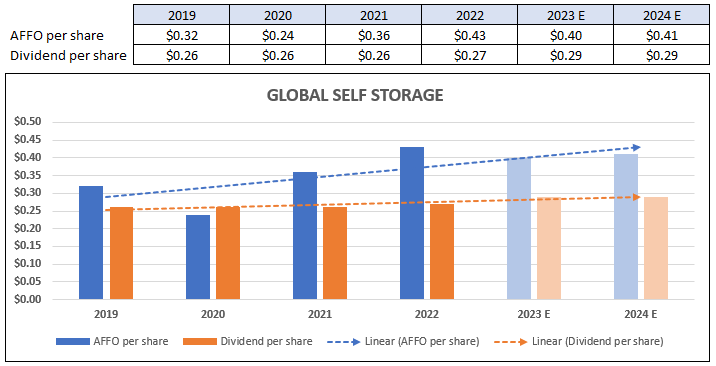

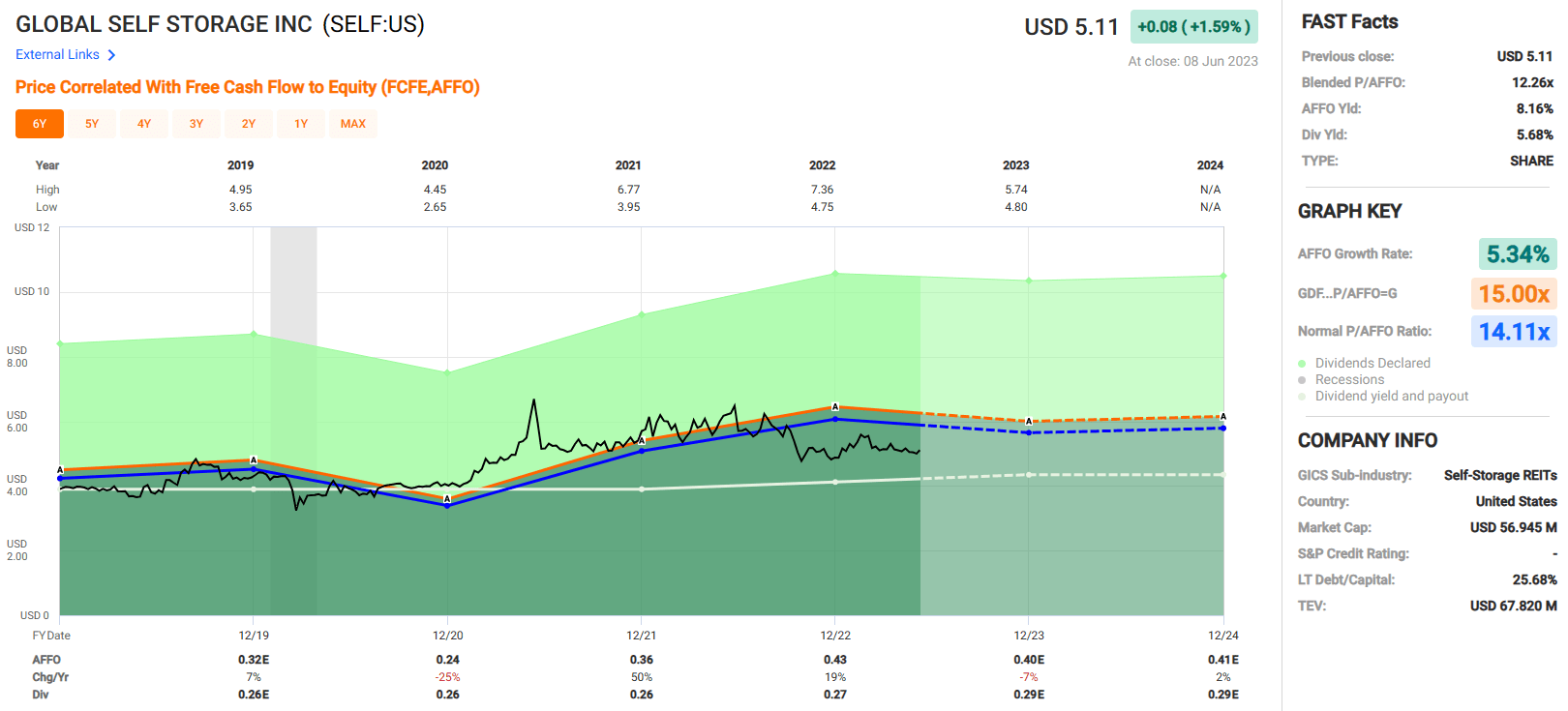

From 2020 to the end of 2022 SELF has delivered positive AFFO per share growth. Over this time period they have averaged an AFFO growth rate of 5.34%. Analysts expect AFFO to fall by -7% in 2023 and increase by 2% in 2024. SELF maintained the divided of $0.26 per share from 2019 to 2021, before raising it to $0.27 in 2022. Over the past 4 years SELF’s average dividend growth rate has been 1.44%.

FAST Graphs (compiled by iREIT)

SELF pays a 5.68% dividend yield that is secure with an AFFO payout ratio of 63.95%. The stock is currently trading at a P/AFFO of 12.26x which compares favorably to their normal AFFO multiple of 14.11x. Additionally, the stock is currently trading at 62% of its net asset value (“NAV”).

There is an increased level of risk given that this is a micro-cap stock with a market cap of approximately $56 million and only 13 properties within their portfolio, but they have excellent debt metrics, offer a high yield, and are trading at discount to their normal valuation.

We do not currently have coverage on SELF, but this might be a rewarding pick for the more risk tolerant investor.

FAST Graphs

Armada Hoffler (AHH)- Market Cap: $1.05 Billion

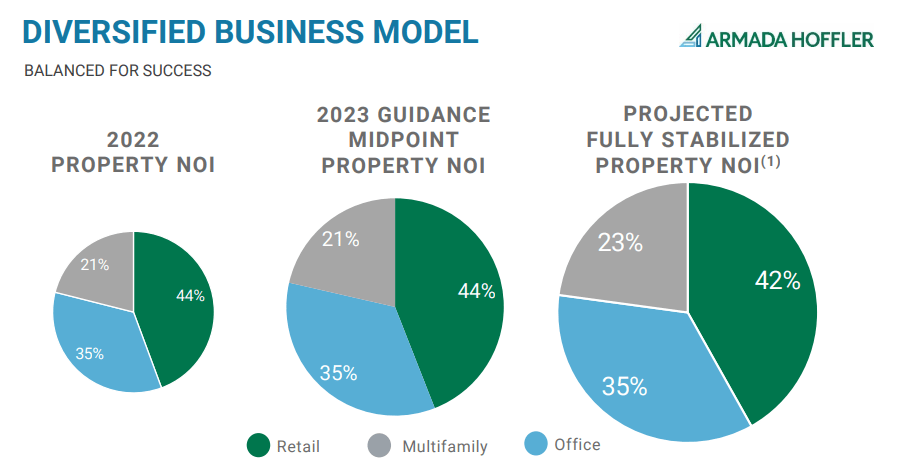

Armada Hoffler is a diversified REIT with portfolio that consists of mixed-use retail (42%), multifamily (23%) and office (35%) properties and the focus is mixed-use (office + retail + apartments) and grocery-anchored shopping centers in mid-Atlantic and Southeast markets with core/core-plus returns.

The multifamily portfolio consists of 2,947 units (10 properties) which represents 25% growth from Q4-21. The portfolio is currently 95.7% occupied and delivered 5.4% cash same store sales in the latest quarter.

The retail portfolio consists of 38 properties (3.9 mm SF) which represents 7.3% cash same store sales in the latest quarter/ The portfolio was 98.4% occupied in Q1-23 with 10.1% GAAP releasing spreads. The portfolio contains well recognized tenants such as Harris Teeter, Lowe’s Food, Whole Foods, Ross, Costco, and Home Depot.

The office portfolio consists of 9 properties totaling 2.1 million square feet that is currently 96.8% occupied (that is no typo). The portfolio generated 2.1% GAAP Same Store Sales and 10.9% GAAP Releasing Spreads in the latest quarter. Top tenants in the portfolio include Constellation Energy (8.0% of ABR), Morgan Stanley (3.9% of ABR), Clark Nexsen (1.5% of ABR), and Franklin Templeton (1.0%).

AHH – IR

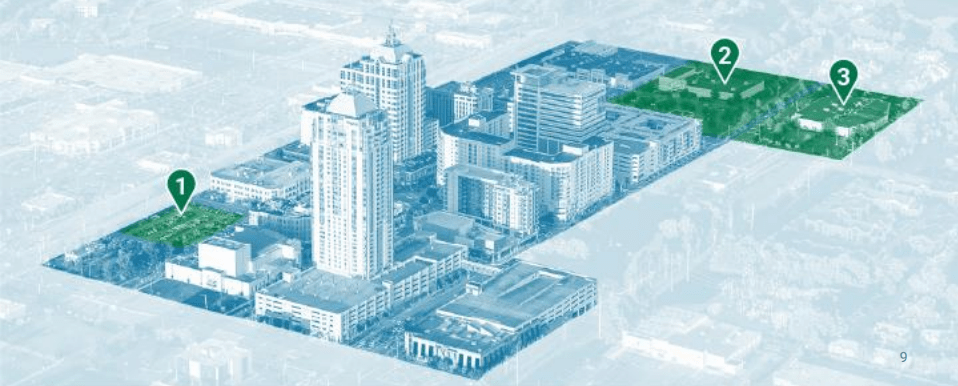

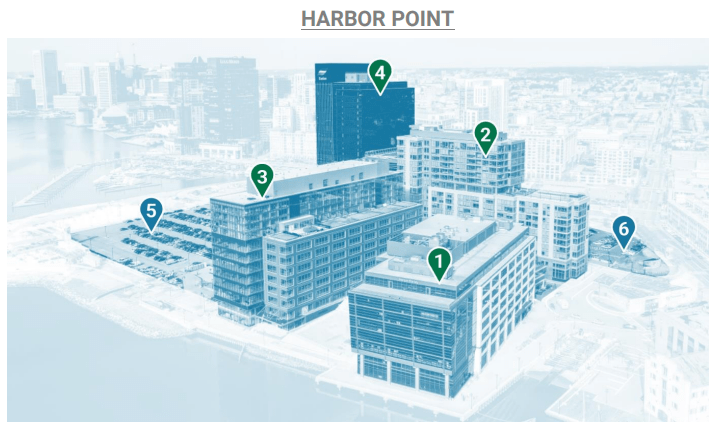

The portfolio is concentrated in mid-Atlantic and Southeast markets and many of properties are located in the Town Center of Virginia Beach and Harbor Point at Baltimore where NOI from each represented 23% and 19%, respectively, of total NOI for the year ended December 31, 2022. This is a snapshot of the Virginia Beach mixed use project:

AHH – IR

At Town Center in Virginia Beach Armada Hoffler was able to execute a long-term lease with KPMG here in its headquarters building. This new lease brings the 800,000 square feet of Town Center office space to 99% leased.

Harbor Point (see below) is another missed use project developed by Armada Hoffler which consists of office, multi family, and retail. At Harbor Point the T. Rowe Price global headquarters (550,000 sf) continues to progress and the company is underway with another 312-unit apartment building.

AHH – IR

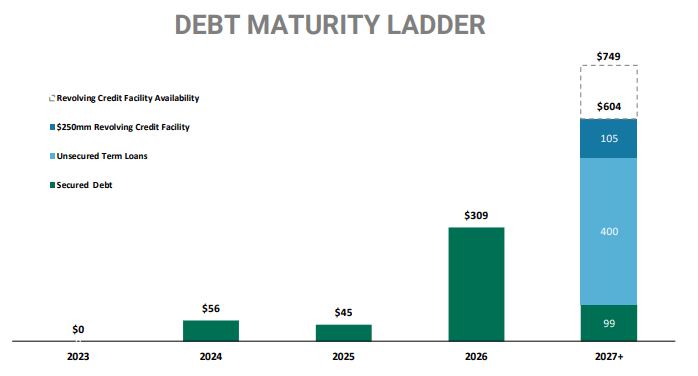

Armada Hoffler continues to transition the balance sheet towards long-term fixed rate unsecured debt while maintaining good liquidity and respectable financial metrics. In Q1-23 the stabilized portfolio debt to stabilized portfolio EBITDA was 5.4x and the debt service coverage ratio and fixed charge coverage ratio reported 2.8x and 2.3x.

The liquidity position continues to be strong at roughly $180 million, more than able to cover the 2023 cash requirements for the development pipeline and any potential preferred equity deals. This combined with a well-structured debt maturity ladder means the company can continue to grow earnings without the need to enter the equity markets.

AHH – IR

For reference, Armada Hoffler has no debt maturities in 2023 and the small amount of debt maturing in 2024 and 2025 will be paid off at maturity adding these assets to its unencumbered borrowing base.

One of Armada’s key themes over the last 12 months has been the rebalancing of the portfolio with the reduction of mezzanine book. The announcement of acquiring the mixed-use Interlock asset in West Midtown, Atlanta replaces the mezzanine interest income with stable property NOI, increasing the value of these earnings.

In Q1-23 Armada reported FFO of $0.23 per diluted share and normalized FFO of $0.30 per diluted share. It also maintained the guidance range accordingly at $1.23 to $1.27 per diluted share of normalized FFO and the Board increased the dividend to $0.195 per quarter (just under 3%).

Unique to the REIT sector, Armada Hoffler also owns a construction business and the CEO told me last week that it provides the company with a competitive advantage. Watch the video HERE.

You can watch the entire interview at iREIT™ on Alpha.

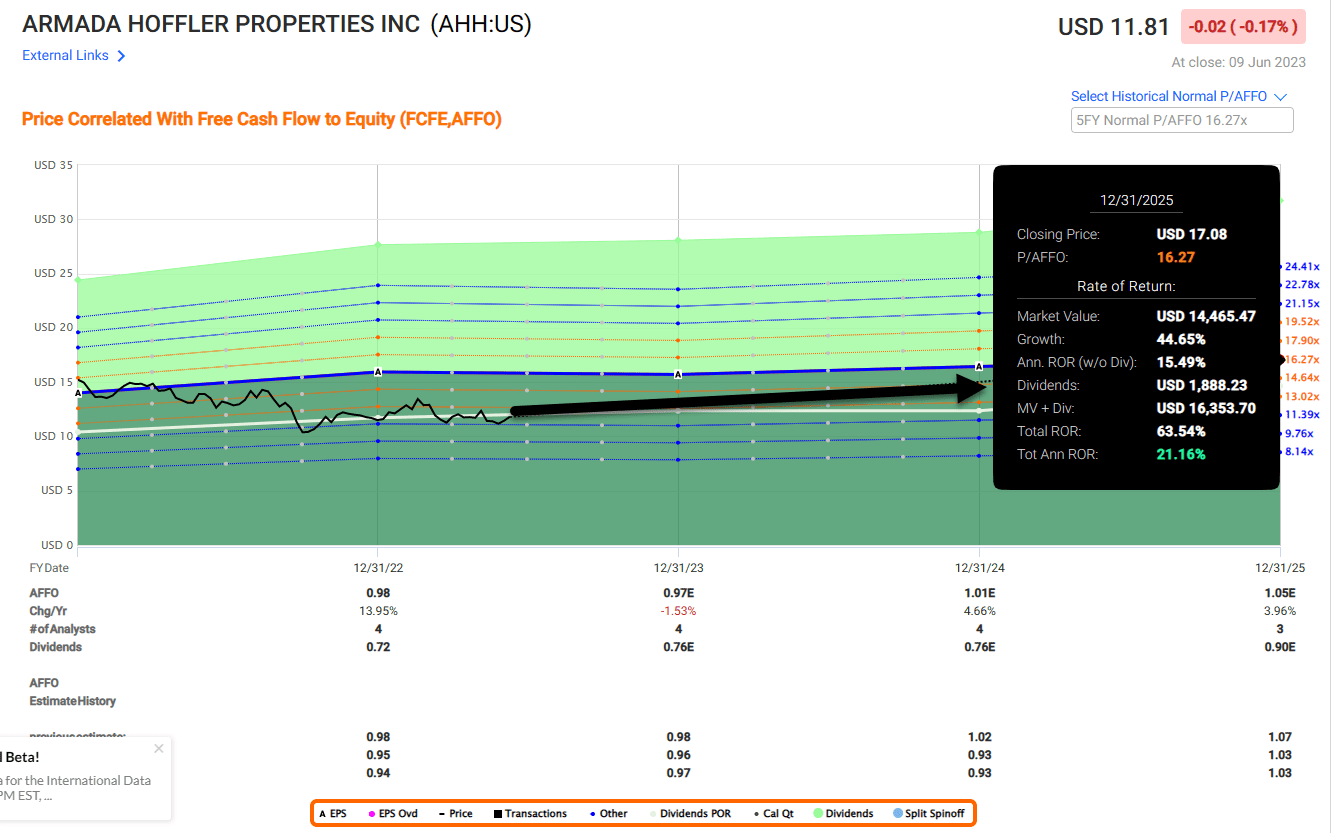

In terms of valuation, we find Armada shares attractive based on a P/AFFO of 12.1x (normal is 15x) and dividend yield of 6.6%. What’s most interesting is that Armada has no direct peers, as the portfolio is diversified, and the office portfolio is 96.8%.

Compare that to REITs like Federal Realty (FRT) – trading at 20.1x – or Kimco Realty (KIM) – trading at 15.5x. While these two REITs do have a much better balance sheet, I don’t believe the discount (300 to 500 bps) is justified.

We’re initiating a Spec BUY with a target annual total return forecast of 20%.

FAST Graphs

In Closing…

We plan to add Whitestone Realty, Global Storage, and Armada Hoffler to the new Small Cap REIT portfolio.

iREIT™

Note: There are risks to owning small cap stocks (defined as companies that have a market capitalized between $300 million and $2 billion) due to higher leverage, enhanced volatility, and modest research coverage; however, they may be able to rise much more quickly.

For retirees, we advise focusing on the proven blue-chip REITs.

Thanks for reading and I look forward to your comments below.

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment