Tom Werner

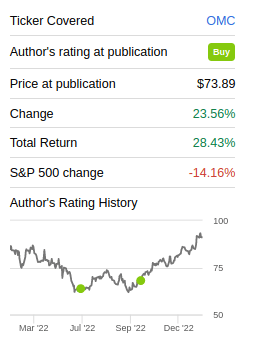

We had been arguing that Omnicom Group (NYSE:OMC) was cheap in the low $70s, despite the slow growth the business was proving resilient and the valuation was just too attractive. Shares were yielding more than 4% with a well-covered dividend and significant share repurchases by the company. Looking at the most recent results the performance of the business has been very decent, but with shares having appreciated a significant amount we believe it is time to adjust our rating to a ‘Hold’ from a previous ‘Buy’. In this article, we’ll go over the most recent results and we’ll also touch on why we believe the valuation is no longer that attractive.

Seeking Alpha

Q4 and 2022 Results

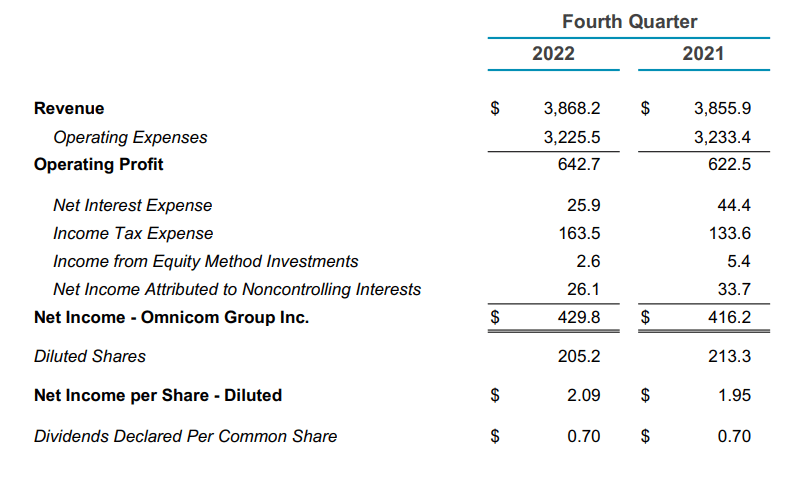

While Omnicom delivered very decent organic revenue growth of ~7.2% in Q4, actual revenue grew only about 0.3%. The difference is that most of the organic revenue growth was offset by foreign exchange impacts and business dispositions. Still, the company posted a very solid 16.6% operating profit margin with a 7.2% year over year growth in diluted EPS. It also announced some important customer wins, including L’Oréal (OTCPK:LRLCF) and Burberry (OTCPK:BURBY).

Omnicom Investor Presentation

For the full year 2022, GAAP diluted EPS came in at $6.36, a reduction compared to the $6.53 delivered in 2021.The company produced some earnings growth, however, when using Non-GAAP earnings, which were $6.93 in 2022 and $6.39 in 2021. Omnicom is targeting 2023 organic revenue growth of 3% to 5% and expects its operating margin to be between 15% and 15.4%.

Growth

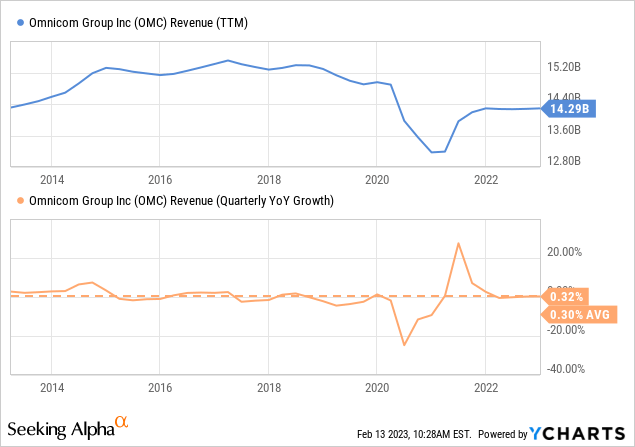

One thing investors have to realize with Omnicom is that this is a company that will struggle to generate significant growth. While organic revenue growth of 9.4% for the full year 2022 doesn’t sound too bad, about half of that gain was erased by foreign exchange impacts, and the other half from business dispositions. In the end the company delivered almost the same revenue as in the previous year. While foreign exchange impacts can go both ways, and could become a tailwind in the future, the problem we see is that if one looks at revenue over the past ten years, it has barely changed. This is one of the main reasons we believe the company does not deserve a high P/E multiple.

There is some reasons for optimism in that the company has done some work offloading some lower growth and less attractive businesses in recent years. It has also made investments in areas where it believed that growth would be consistent in good times and in bad, such as in precision marketing, and the expansion of services in the health area. This could mean somewhat better growth than what the company delivered the past ten years, but we still believe investors should probably be cautious with their growth assumptions.

Free Cash Flow

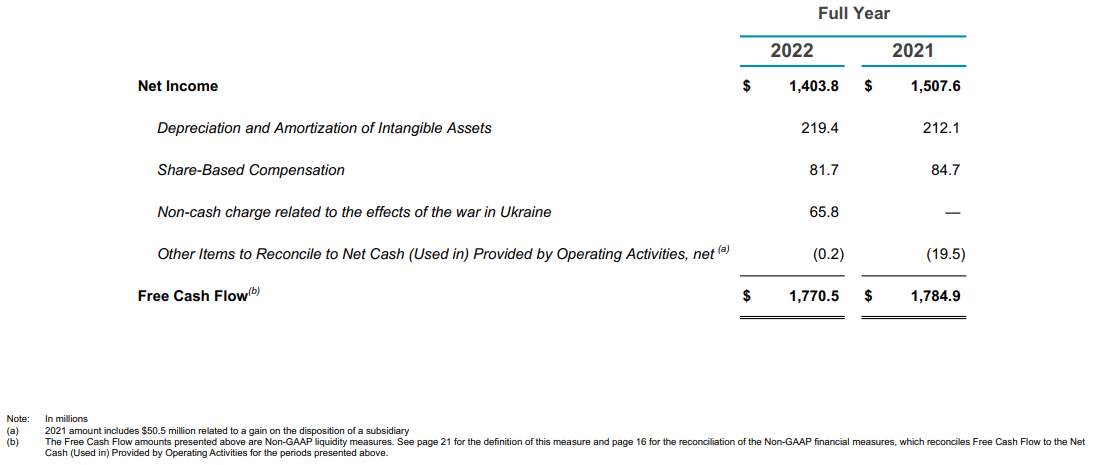

Similarly, if we look at free cash flow generated by the company in 2022 compared to 2021, it actually decrease by a small amount. To a certain extent it is to be expected that growth would be minimal, as most of its earnings are being distributed to shareholders in the form of dividends and share repurchases. The company does reinvest some of its cash flows into capex and M&A, but so far the resulting growth has not been that significant.

Omnicom Investor Presentation

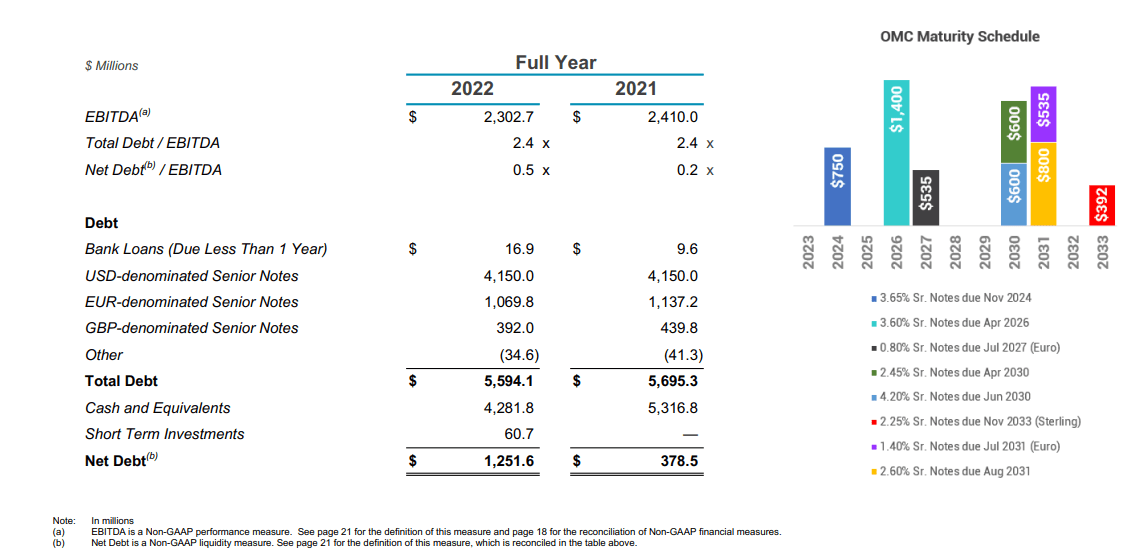

Balance Sheet

The balance sheet remains quite solid with low leverage and a well-laddered maturity schedule. That said, net debt did increase significantly from ~$378 million to ~$1.2 billion. The reason behind the increase in net debt was mostly a negative $844 million change in operating capital, and a negative $218 million effect of foreign exchange rate changes on cash and cash equivalents.

Omnicom Investor Presentation

Valuation

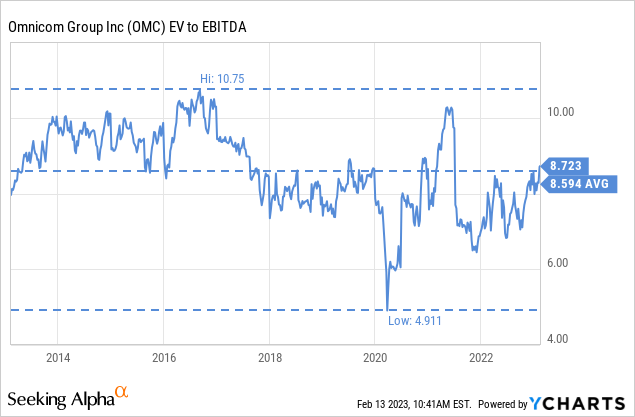

Shares are now trading very close to their ten year average valuation multiples. The EV/EBITDA is now ~8.7x, a little above the ten year average. We believe this is a reasonable multiple for the type of growth and quality of Omnicom’s business, but no longer reflects the previous undervaluation.

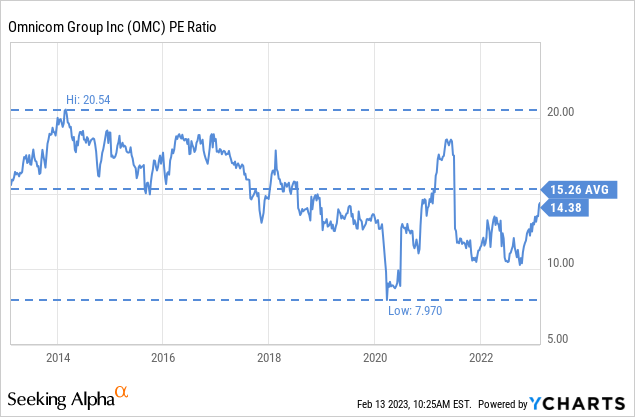

Similarly, the P/E ratio is very close to its ten year average. A close to 15x price/earnings multiple seems pretty fair for a company that recently delivered 7% EPS growth. With organic growth guided for 2023 at only 3% to 5% we don’t think the business justifies a much higher multiple than that.

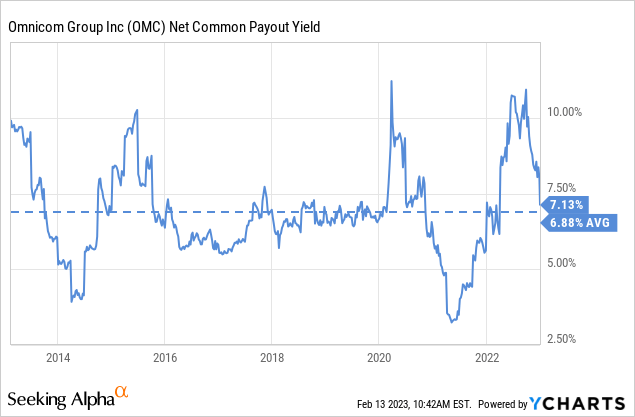

One thing Omnicom investors have going for them is how generous the company is sharing the earnings. Between the ~3% dividend yield and share buybacks the net common payout yield is close to 7%.

Risks

Advertising and media agencies are particularly vulnerable to recessions, as this is an expense that businesses sometimes cut during tough times. This is another reason to be extra cautious with the shares right now. The risk is partially mitigated by the company’s strong balance sheet, but it could still mean significantly lower earnings should a severe recession arrive.

Conclusion

We believe Omnicom Group delivered solid Q4 and full year 2022 results, despite being significantly impacted by foreign exchange impacts. Shares have performed very well since our last article, and mostly based on valuation we are downgrading our rating to ‘Hold’ from ‘Buy’ previously. Given the 2023 guidance, and the company’s historical growth, we do not believe it deserves much higher multiples than where it is currently trading. We believe this remains a decent business, but shares now appear fully valued.

Be the first to comment