Sam Tarling/Getty Images News

The only time to eat diet food is while you’re waiting for the steak to cook.” ― Julia Child

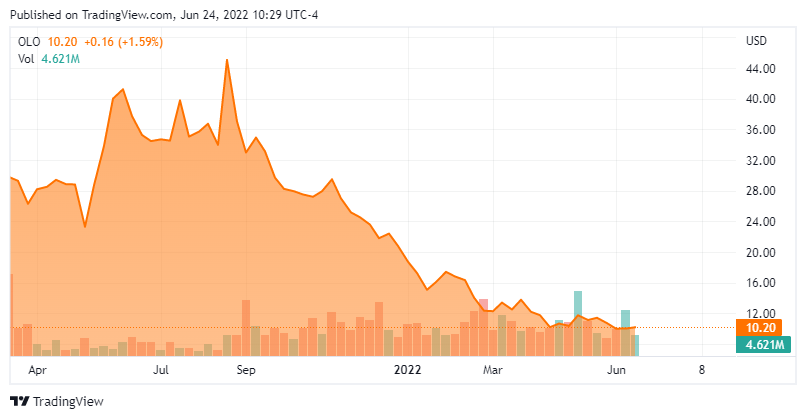

Today, we take our first look at Olo Inc. (NYSE:OLO), a small cap company helping to digitize and automate the restaurant industry. This cloud concern provides an ordering system that restaurants can integrate into their website, so customers can order off their menu digitally. The company came public late in the first quarter of 2021 as elevated valuations, the stock was priced at over 40 times sales on its debut. Like most of that IPO ‘vintage‘, the stock finds itself deep in ‘Busted IPO‘ territory. Are the shares oversold now, or is there still more pain ahead for shareholders? An analysis follows below.

Seeking Alpha

Company Overview

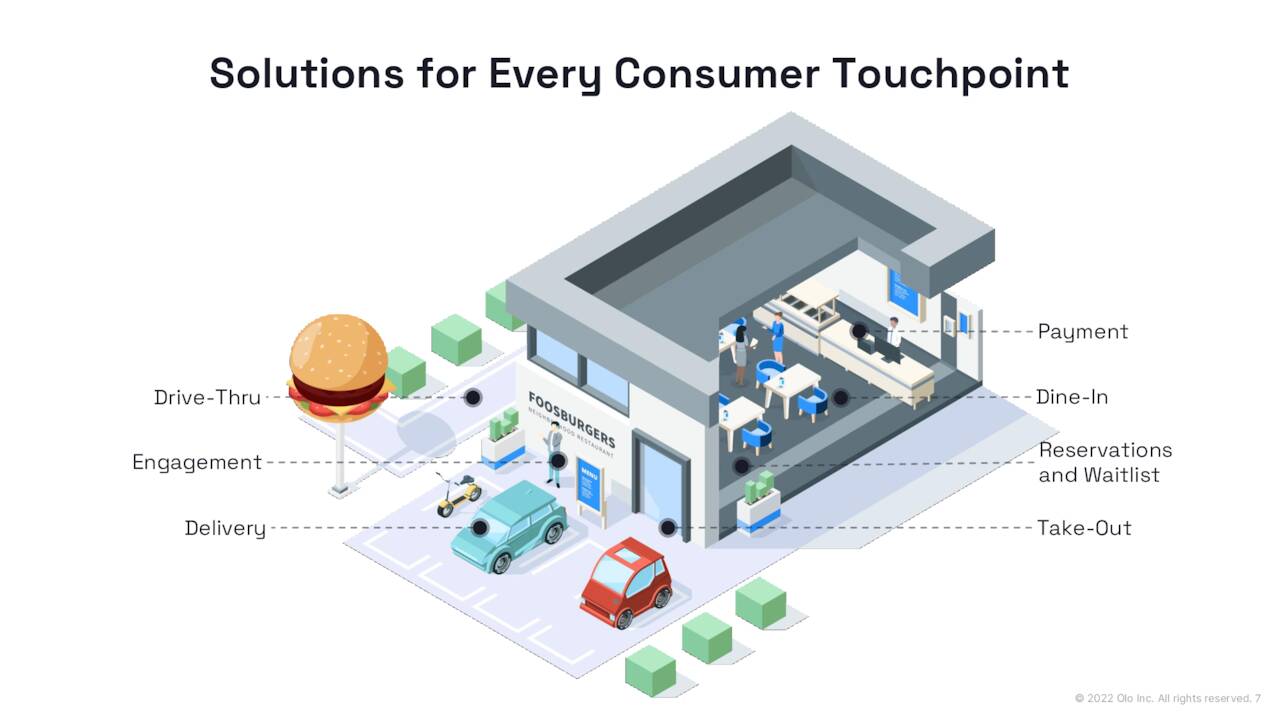

Olo Inc. is headquartered in New York City. The company provides a software-as-a-service [SaaS] platform for multi-location restaurants in the United States. Olo offers a variety of modules that provide unique solutions for tasks such as ordering, delivery, payment and customer management. The stock currently trades just above ten bucks a share and sports an approximate $1.6 billion market cap.

May Company Platform

First Quarter Results

On May 10th, the company posted its first quarter numbers. Olo had a non-GAAP profit of one penny a share as revenues rose nearly 19% on a year-over-year basis to nearly $43 million. Both top and bottom line numbers slightly beat the analyst consensus.

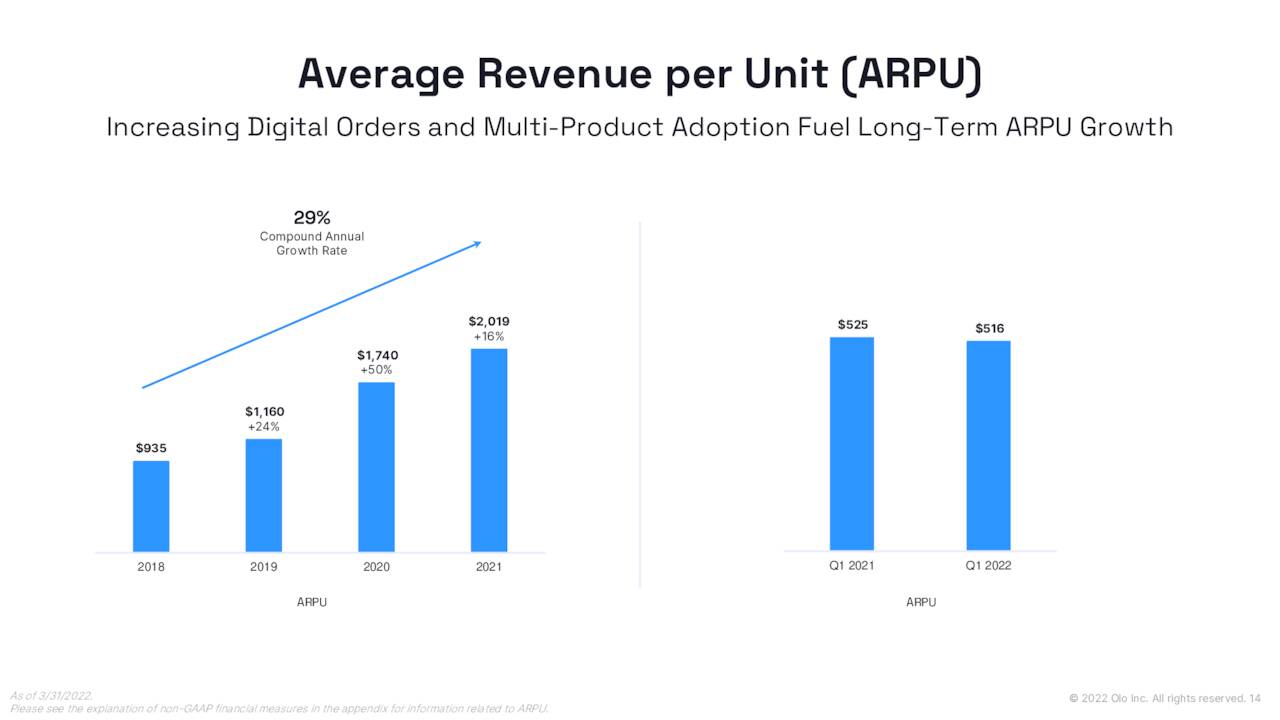

It is important to note that on a GAAP basis, the company posted a net loss of $11.5 million, or seven cents a share. Free cash flow for the quarter was a negative $3.4 million. In addition, average revenue per unit or ARPU decreased 2% year-over-year, even as it rose 2% sequentially to approximately $516.

May Company Presentation

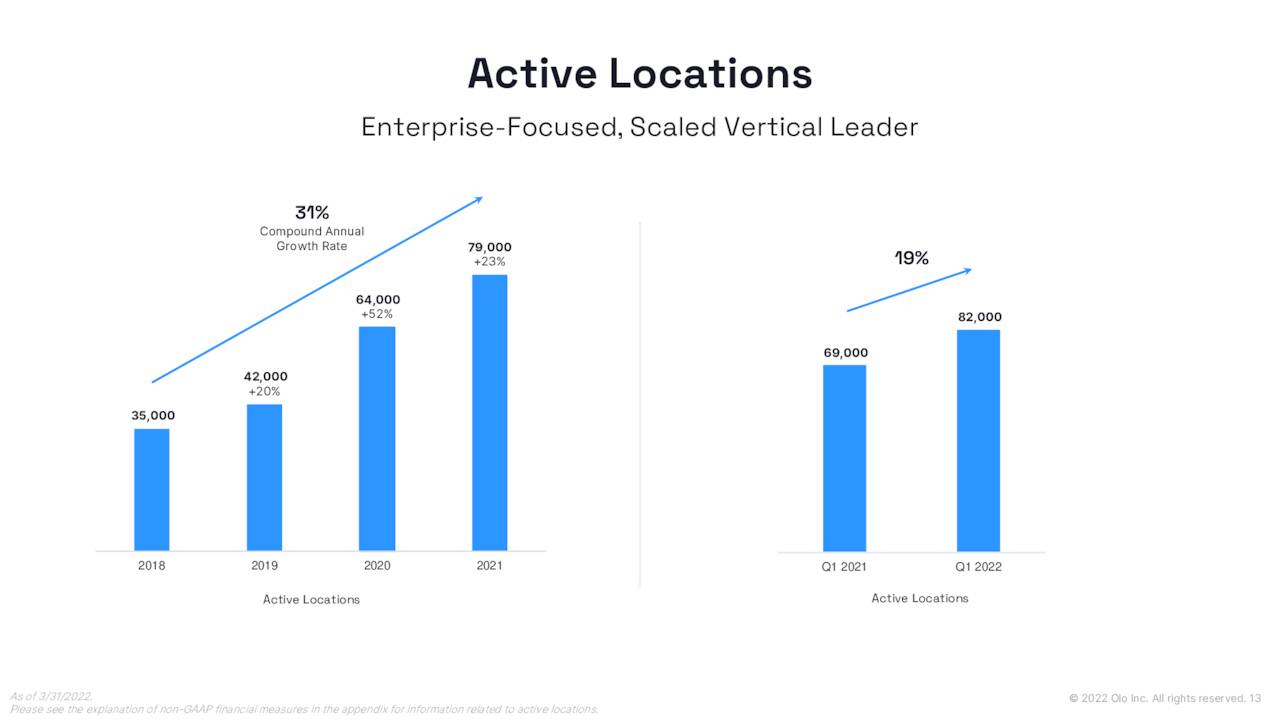

The company has a large network of partners, brands, and customers which continues to expand. Locations grew some 13,000 to 82,000 in the first quarter.

May Company Presentation

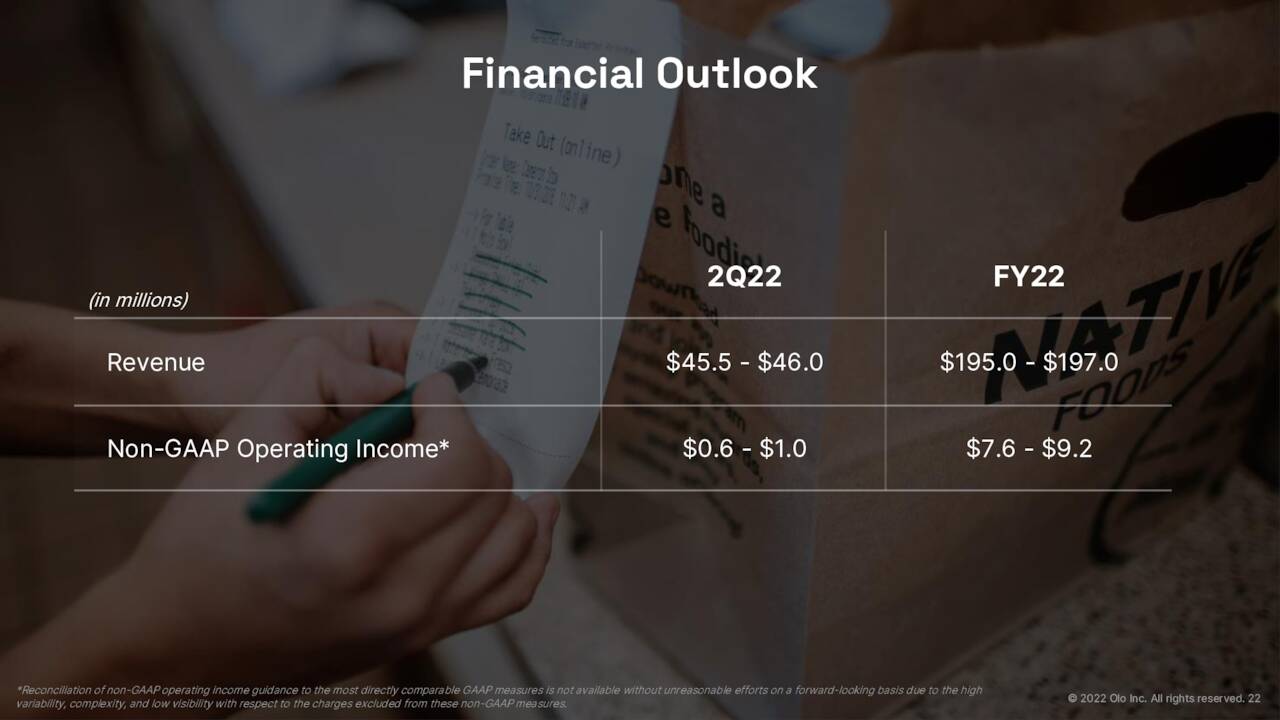

Leadership now sees revenue between $195 million to $197 million for FY2022, where it expects to turn a small profit on a non-GAAP basis.

May Company Presentation

Analyst Commentary And Balance Sheet

The analyst community remains sanguine on the company’s prospects. Since first quarter earnings posted, four analyst firms including RBC Capital and Piper Sandler have reissued Buy ratings on the stock. Albeit, all four also contained downward price target revisions. Price targets proffered ranged from $12 to $21 a share.

Just over 20% of the outstanding float of the shares are held short. The company ended the first quarter with just over $460 million of cash and marketable securities on its balance sheet after posting a GAAP net loss of $11.5 million. Olo has no long-term debt. Despite the large drop in the shares, insiders continue to be consistent and frequent sellers of the stock here in 2022 and have disposed of more than $500,000 worth of shares so far in June.

Verdict

The current analyst consensus has the company making four cents a share of profit in FY2022 and revenues rise just over 30% to $195 million. Similar growth is seen in FY2023 as sales hit $250 million and the company posts a 14 cent a share profit.

The company’s valuation is now just over eight times forward sales, approximately 20% of the valuation based on this metric as when it came public. Accounting for cash, that shrinks to around six times forward revenues. There is no doubt the company is aiming at a large market. Only 15% of restaurant orders are currently digitized, a percentage that will continue to grow over time.

This large market has attracted myriad competitors. My personal preference and the only name I hold in this space is Toast, Inc. (TOST) which I profiled in March and have a small covered call position within. The stock has a slightly lower valuation based on price to sales and has gotten rave reviews from the restaurant owners I know. Sales growth rates also much larger. The stock has held up well since then despite a beneficial owner cashing out a huge chunk of shares, and the equity has approximately one fourth the short interest of Olo, Inc.

To eat is a necessity, but to eat intelligently is an art.”― François de la Rochefoucauld

Be the first to comment