Brandon Bell

Thesis

One thing was clear to us from Occidental Petroleum Corporation’s (NYSE:OXY) Q3 earnings release: its record revenue and earnings spurt has slowed dramatically.

We cautioned OXY bulls in our previous article that Occidental could find it increasingly challenging to outshine its spectacular performances in FY21/22 as underlying energy markets weaken further.

Accordingly, WTI crude oil futures (CL1:COM) have fallen nearly 40% from their June 2022 highs to their recent November lows. Likewise, NYMEX natural gas futures (NG1:COM) fell more than 50% from their August highs to their October lows before recovering from their oversold bottom.

However, OXY remains entrenched close to its August highs, as OXY bulls cheer the company’s increasing focus on stock repurchase and dividend distribution moving forward.

We applaud CEO Vicki Hollub & team’s capability to drive outperformance for OXY from its COVID pandemic lows. Furthermore, the “Warren Buffett effect” (BRK.A, BRK.B) has also lifted investors’ sentiments on management’s credibility, encouraging investors to pile onto OXY. However, we believe it’s a timely reminder for investors looking to join the bandwagon now that Berkshire’s average cost of its stake in OXY is likely in the “low 50s,” relative to OXY’s last closing price of $72.8.

Therefore, we urge investors to consider very carefully whether growth normalization headwinds could impact the market’s assessment of OXY’s valuation moving ahead.

We postulate that another momentum surge seen in WTI crude oil futures and natural gas futures previously is unlikely, even as the market parses Russia’s reaction to Europe’s proposed oil price caps that the continent is trying to finalize.

Maintain Sell, as we urge investors sitting on massive gains to leverage the recent rally to cut more exposure.

Don’t Ignore Occidental’s Growth Deceleration Risks Anymore

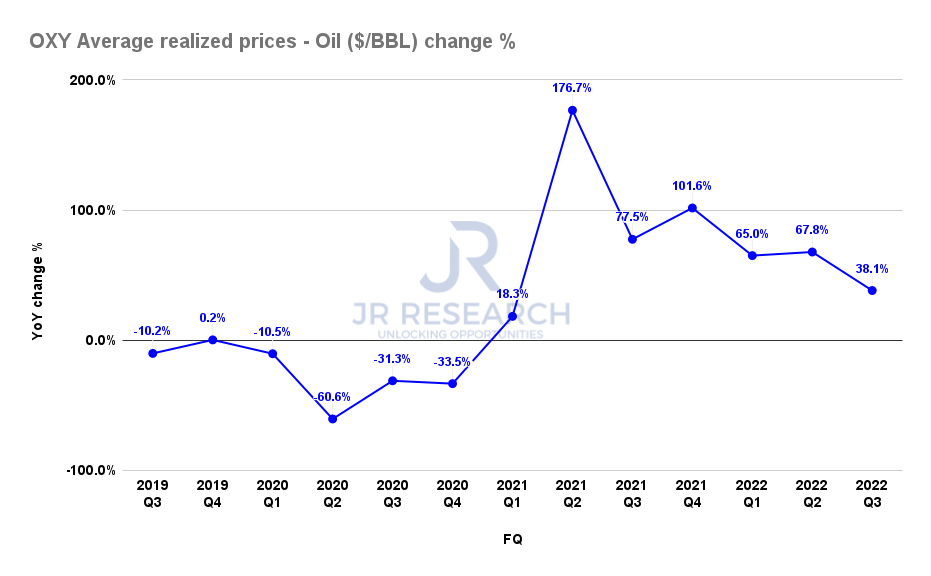

OXY Average worldwide realized prices for oil change % (Company filings)

As seen above, Occidental reported a 38.1% uptick in worldwide realized oil prices for FQ3, down from Q2’s 67.8% increase. Therefore, it continued a decelerating trend for Occidental, suggesting that highly challenging comps could hamper outperformance moving ahead.

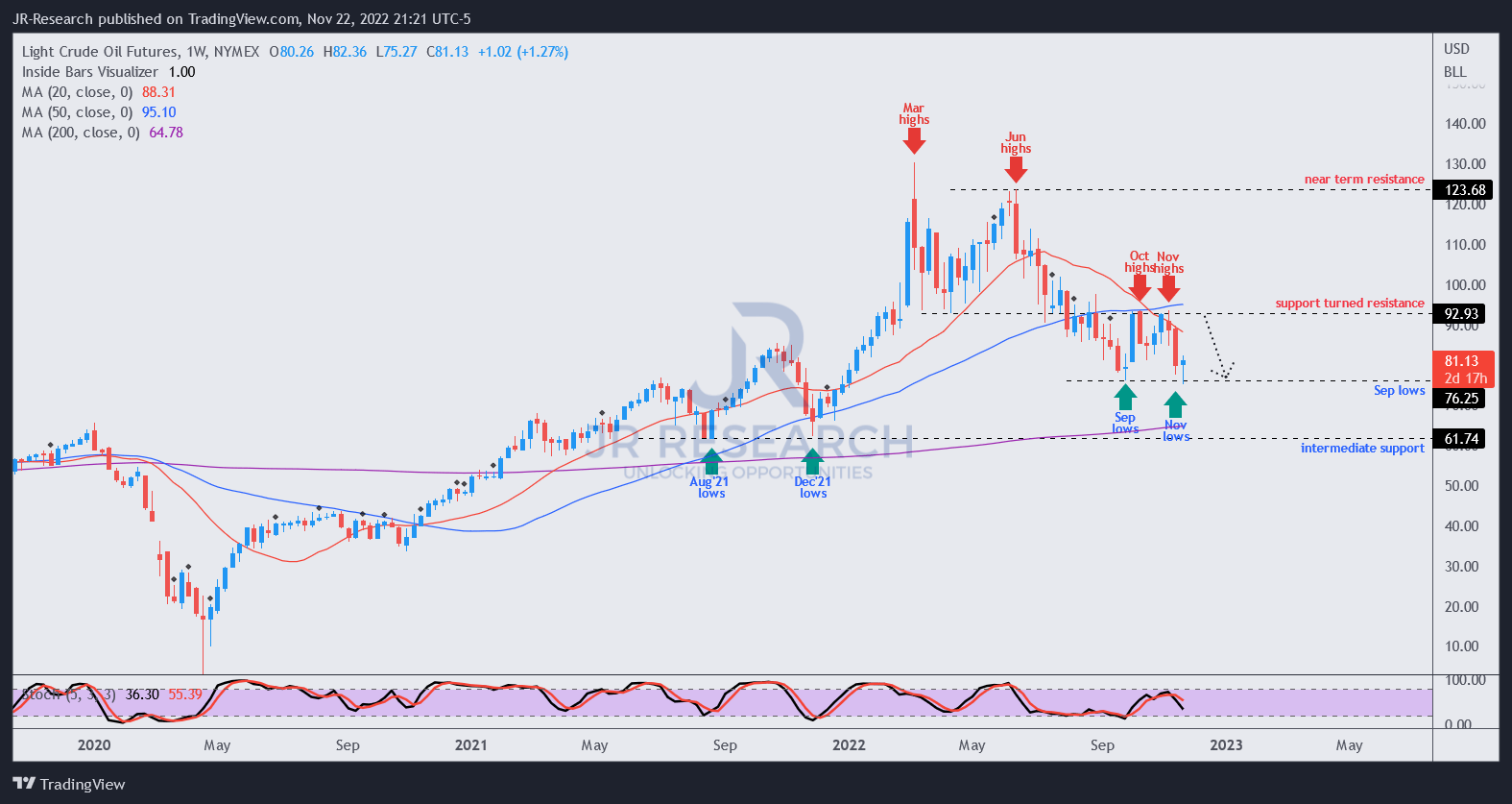

CL1 price chart (weekly) (TradingView)

Notably, Q3’s performance was indexed against WTI crude oil futures at $91.55. However, CL1 has continued to slide with its medium-term downtrend, re-testing its September lows recently.

We postulate that the strength of the re-test at the current levels should provide clues on oil buyers’ conviction to defend its critical support, which could portend further downside toward the $60+ region if buyers fail to hold the line firmly.

Hence, with potentially lower indexed prices into Q4 and H1’23, we believe investors need to be prepared that the days of remarkable outperformance could likely be over.

Analysts Estimates Have Been Cut Further

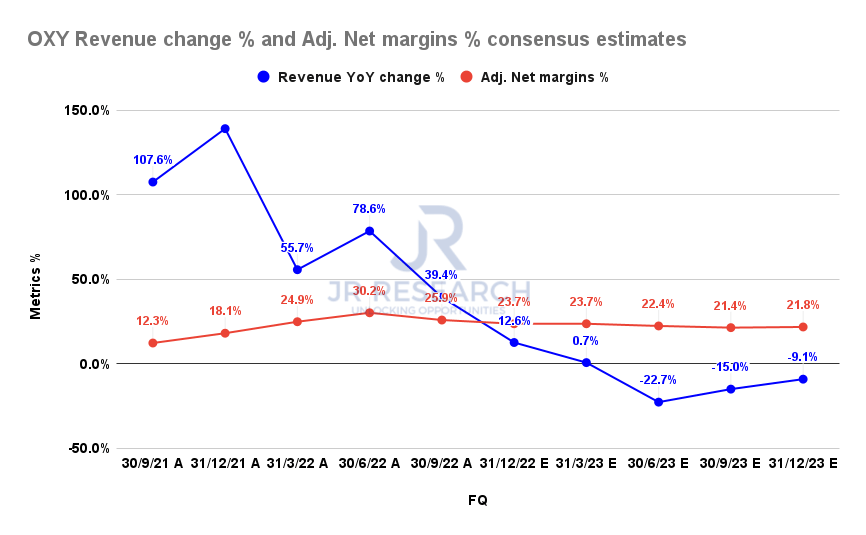

OXY Revenue change % and Adjusted Net margins % consensus estimates (S&P Cap IQ)

However, we noted that the market has yet to reflect Wall Street analysts’ revised consensus estimates (neutral) after the recent Q3 card.

While OXY had a momentary post-earning selloff, the bulls have recovered those losses, keeping OXY perched close to its August highs.

However, we urge investors to consider that Occidental’s revenue growth could continue to moderate through FY23, as seen above. Moreover, it’s also expected to impact its net margins, even though we don’t expect a near-term impact on its capital allocation policies for now. Occidental’s low-cost base of below $40 WTI gives investors tremendous confidence in the company’s capital allocation priorities.

Furthermore, Hollub stated that management’s focus remains not on increasing production unsustainably, as she accentuated:

If [production] growth is an outcome, it would probably be somewhere in the neighborhood of 1% or less. So it’s not our intention to grow it. But if we have more wells like Richard [OXY’s President, Operations] just talked about, there will be growth from our assets, but it’s not our desire to grow it in 3% to 5%. The growth is not the target. It’s to develop the best wells in the best possible ways. (Occidental FQ3’22 earnings call.)

We deduce that OXY bulls have continued to use rapid selloffs as opportunities to “buy the dips,” demonstrating confidence in Hollub & team. However, we urge investors to consider how much further they expect OXY to continue rising from here without a significant pullback, given the underlying energy markets’ headwinds.

Is OXY Stock A Buy, Sell, Or Hold?

OXY last traded at an NTM normalized P/E of 9x, well above its oil & gas peers’ median of 6.8x (according to S&P Cap IQ data).

We also gleaned that the market has not re-rated OXY, broadly similar to its peers, likely in anticipation of potential earnings compression.

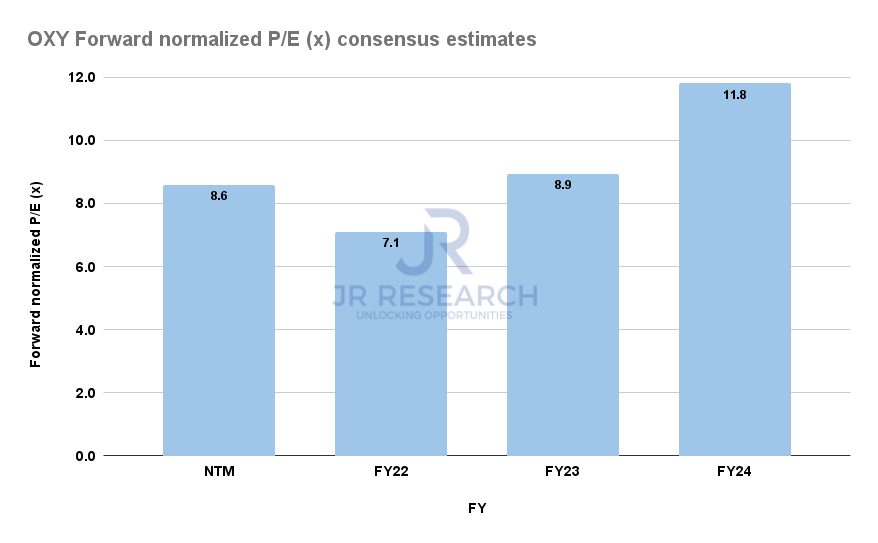

OXY Forward normalized P/E consensus estimates (S&P Cap IQ)

With earnings estimates cut further through FY24, we believe the market is likely drawing in the late buyers to OXY before digesting the over-optimism.

OXY last traded at an FY24 normalized P/E of nearly 12x. Furthermore, energy analysts have remained generally optimistic about the industry’s forward prospects.

Therefore, the earnings revisions have been relatively subdued than other industries. As such, we believe there are risks to the consensus estimates (behooving more cuts) for Occidental Petroleum Corporation if the market anticipates worse-than-expected demand destruction or recessionary risks moving ahead.

Maintain Sell.

Be the first to comment