wsfurlan

Other than energy, fertilizer is the most important story

Anyone more than casually following the Russia-Ukraine war knows that supply chains in several key markets have been disrupted on its account. A good summary of the fallout can be seen here from a University of Illinois white paper:

The Russian invasion of Ukraine substantially elevates the risk of disruptions in the global fertilizer trade. Russia is the world’s largest exporter of fertilizers, accounting for 23% of ammonia exports, 14% of urea exports, 10% of processed phosphate exports, and 21% of potash exports, according to data from The Fertilizer Institute. The primary destinations of fertilizers from Russia are Brazil (21%), China (10%), the US (9%), and India (4%)

With natural gas being a primary feedstock in the production of ammonia and urea-based fertilizers, the cost of producing these fertilizers has also shot through the roof as natural gas prices soar. The fertilizer companies have been able to pass this cost on to the end user. Food, after all, is the most essential of all defensive/consumer staple categories. Whatever the cost, the consumer will need to pay.

CF Industries Holdings, Inc. (NYSE: CF) has screened in the top 30 stocks all year for Magic Formula stocks in the above-$15 Billion market cap category. This is the market cap category I prefer to use for a portion of my portfolio where the goal is to track BETA with a slight edge. $15 Billion puts the crosshairs squarely on S&P 500 (SP500) companies with institutional support.

The Magic Formula was designed by Joel Greenblatt, and the screener can be found here for free. The metric creates a score based on “good” and “cheap.” Good is represented by return on invested capital or ROIC, while cheap is based on the earnings yield, either EPS/SP or EBIT/EV. Scores of more than 20 are solid and normally make the screener depending on where you set the minimum market cap.

CF Industries has been on a roll since the pandemic outbreak and all the other negative macroeconomic headwinds ensued, breaking down supply chains. If we look at CF’s history, the story is one of the up-and-down years without consistent growth and certainly not anything resembling the past few years. With the stock trading at single-digit P/E ratios and momentum at its back, the stock still looks cheap. The P/E ratio indicates a market waiting for a pullback in commodities prices that will bring the fertilizer industry’s earnings yields back to normalcy. From my analysis below, CF Industries is a buy, but a cautious one.

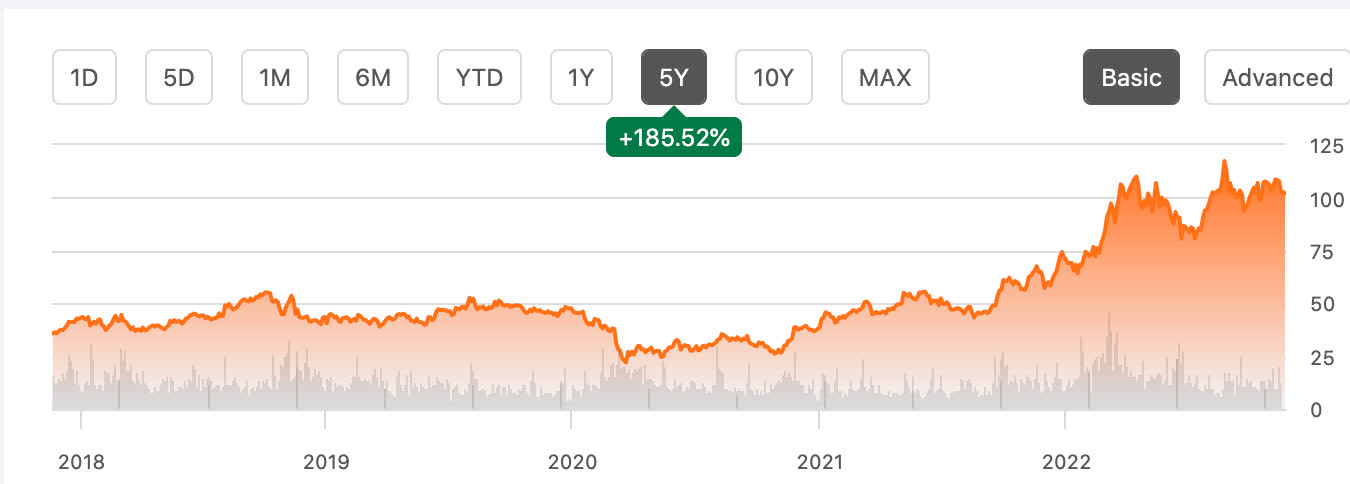

Up 56% year to date, the ship might have more steam left in it until macro issues settle. However, once they do and a reversion to the mean in commodities prices happens, this may be a swing trade to get out of once we see the cost of goods sold begin to tail off. This may be counterintuitive to think a reduction in the cost of goods sold is a negative, but it could also be a leading indicator as to what the trends in feedstock prices look like which will mean the supply chain bottleneck is about to uncork. That could be a good point to offload shares should you have gains.

Magic Formula numbers

The most recent fiscal year data for return on invested capital I have for CF Industries is 13.44%, data supplied by my brokerage. The big bump in the formula number for CF Industries is not in their return on capital, but in their enormous earnings yield compared to the price. If ROIC represents “good” and earnings yield represents “cheap”, we can see that CF is more cheap than good with an earnings yield of 25% calculated using Enterprise Value divided by EBIT. The total magic formula score would be 13.44 + 25 = 38.44, a very nice number for companies in this market cap size. Additionally, since the ROIC percentage is for the most recent fiscal year of 2021 but the EV/EBITDA score tracks TTM, I would expect ROIC to be much higher after 2022 is in the books. It’s fairly evident by these scores, why the run-up in price has seen an almost 200% price appreciation since the pandemic.

CF share appreciation (seeking alpha)

The big picture

What CF Industries does:

Our principal customers are cooperatives, independent fertilizer distributors, traders, wholesalers and industrial users. Our core product is anhydrous ammonia (ammonia), which contains 82% nitrogen and 18% hydrogen. Our nitrogen products that are upgraded from ammonia are granular urea, urea ammonium nitrate solution ((UAN)) and ammonium nitrate ((AN)). Our other nitrogen products include diesel exhaust fluid ((DEF)), urea liquor, nitric acid and aqua ammonia, which are sold primarily to our industrial customers, and compound fertilizer products (NPKs), which are solid granular fertilizer products for which the nutrient content is a combination of nitrogen, phosphorus and potassium.

Our principal assets as of December 31, 2021 include:

•five U.S. nitrogen manufacturing facilities, located in Donaldsonville, Louisiana (the largest nitrogen complex in the world); Port Neal, Iowa; Yazoo City, Mississippi; Verdigris, Oklahoma; and Woodward, Oklahoma. These facilities are wholly owned directly or indirectly by CF Industries Nitrogen, LLC ((CFN)), of which we own approximately 89% and CHS Inc. ((CHS)) owns the remainder. See Note 18—Noncontrolling Interest for additional information on our strategic venture with CHS;

•two Canadian nitrogen manufacturing facilities, located in Medicine Hat, Alberta (the largest nitrogen complex in Canada) and Courtright, Ontario;

•two United Kingdom nitrogen manufacturing facilities, located in Billingham and Ince;

•an extensive system of terminals and associated transportation equipment located primarily in the Midwestern United States; and

•a 50% interest in Point Lisas Nitrogen Limited (PLNL), an ammonia production joint venture located in the Republic of Trinidad and Tobago that we account for under the equity method.

-CF Industries 2021 10K.

Why they are important

According to the United Nations, 2023 is on a fast track to global famine:

The world is on its way to “a raging food catastrophe,” Secretary-General António Guterres warned leaders gathered in Bali, alerting them that “people in five separate places are facing famine.” Simultaneously, we are witnessing a crunch in the global fertilizer market,” he continued, highlighting once again the Black Sea Grain Initiative to export vital food supplies from Ukraine, and fertilizers from Russia.

In the face of this, Uralkem, a large Russian fertilizer conglomerate, is donating fertilizers to the world food program, or WFP. Food and fertilizers are not subject to sanctions, the UN article points out. The main issue of getting fertilizers out of Russia seems to be a matter of difficulty in making any payments to Russia period.

The above is a serious matter. We in the United States are experiencing inflation, but nothing like countries whose currency has depreciated against the U.S. dollar. With natural gas and petroleum products as the main feedstock for fertilizers and all petroleum products principally purchased in U.S. dollars, you can see where other countries could experience famine far easier than the country with the global reserve currency. This also puts CF Industries at an advantage, as their business operates on dollars being based out of the United States. They should be able to derive a cost advantage on their feedstock over foreign operators.

As the beginning of my article points out, Russia accounts for nearly a quarter of the world’s fertilizers. Also, keep in mind that these products are not to be sanctioned. If a payment plan to fertilizer producers gets worked out, this bottleneck that has propelled CF Industries’ earnings to grow 250% in a year may be short-lived.

Valuation

In addition to the Magic Formula, let’s take a look at CF Industries’ valuations based on both a trailing PEG ratio and the Graham number.

yahoo finance

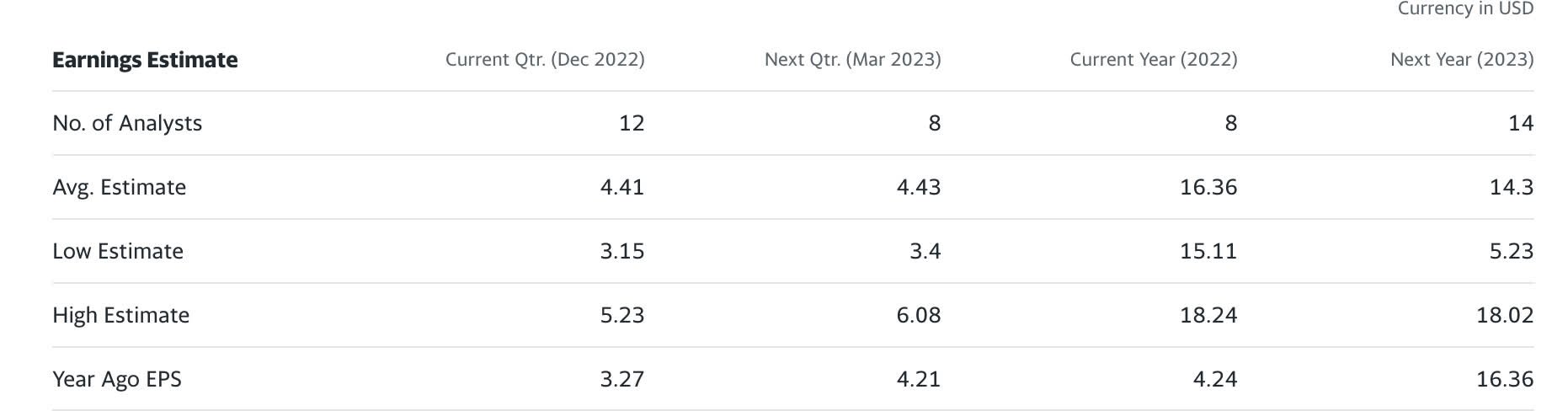

Since we are close to the end of the year, I want to find the analyst estimates for the full 2022 EPS. The difference between 2021 and 2022 is shocking. A year ago the EPS was 4.24 and the conservative low estimate to finish out 2022 is $15.11 a share. For context, CF Industries beat their entire 2021 EPS in the Q2 June 30 print of $5.59 a share. Using these numbers to calculate a PEG ratio value is certainly going to create a skewed perspective, but let’s take a look anyways.

I typically use the method taught by Peter Lynch to calculate the PEG ratio, trailing 5 years EPS CAGR or non-GAAP earnings CAGR as the multiplier without the percent sign, plus the dividend added as a kicker to the multiplier. In this case, CF had an EPS of $1.25 a share in 2018 and our terminal value will be the low-end estimate of $15.11 for 2022. That’s a CAGR of 64.62% + 1.5 kicker for the dividend yield for a total multiplier of 66.12. TTM EPS is $15.3 a share as our multiplicand. 66.12 X $15.3 gives us a ridiculous value of $1,011. That certainly needs to be thrown out as Peter Lynch points out, growing earnings at more than 25% per year, in the long run, is unrealistic.

The last year certainly skews the growth rate with a 253% growth in earnings between the 2021-2022 period. However, if we even take the most conservative low-end 2023 EPS estimate of $5.23 and multiply that by the trailing 6 years CAGR if we were starting at 2023 looking backward, we would still have a multiplier of 26.94+1.5 (static dividend assumption) X $5.23= $148.74. This $148.74 price is far more realistic. This would still leave about 40+% more upside on the table through 2023 if the supply chain remains as is and earnings work out the way the assumptions appear. Just watch those costs of revenue or the cost of goods sold.

Graham number

Looking at the value based on the Graham Number taught in the Intelligent Investor tells a bit of a different story. This number for fair value teaches that a company’s price-to-book value X price-to-earnings should not exceed 22.5. To find at what price those values hit the 22.5 thresholds, the price target formula is as follows: SQRT 22.5 × (Earnings Per Share) × (Book Value Per Share). Our inputs for CF Industries are TTM EPS of $15.3 and a book value per share of $22.47, thus SQRT 22.5 X ($15.3) X ($22.47)= $87.95.

The Graham number incorporates both book value and earnings to get a fair price. The fertilizer industry is certainly one that relies on hard assets and commodities, the main drag on the price target here is not the earnings but the overvalued assets. If we based our estimate on this pricing strategy and incorporated 2023 estimates, there could be quite a bit of downside based on this assumption. CF is maximizing its assets in this macro environment and I would put the bottom to the downside somewhere around this number of $87.95 if and when fertilizer prices begin to revert to the mean. Possibly lower if earnings get halved.

The dividend

yahoo finance

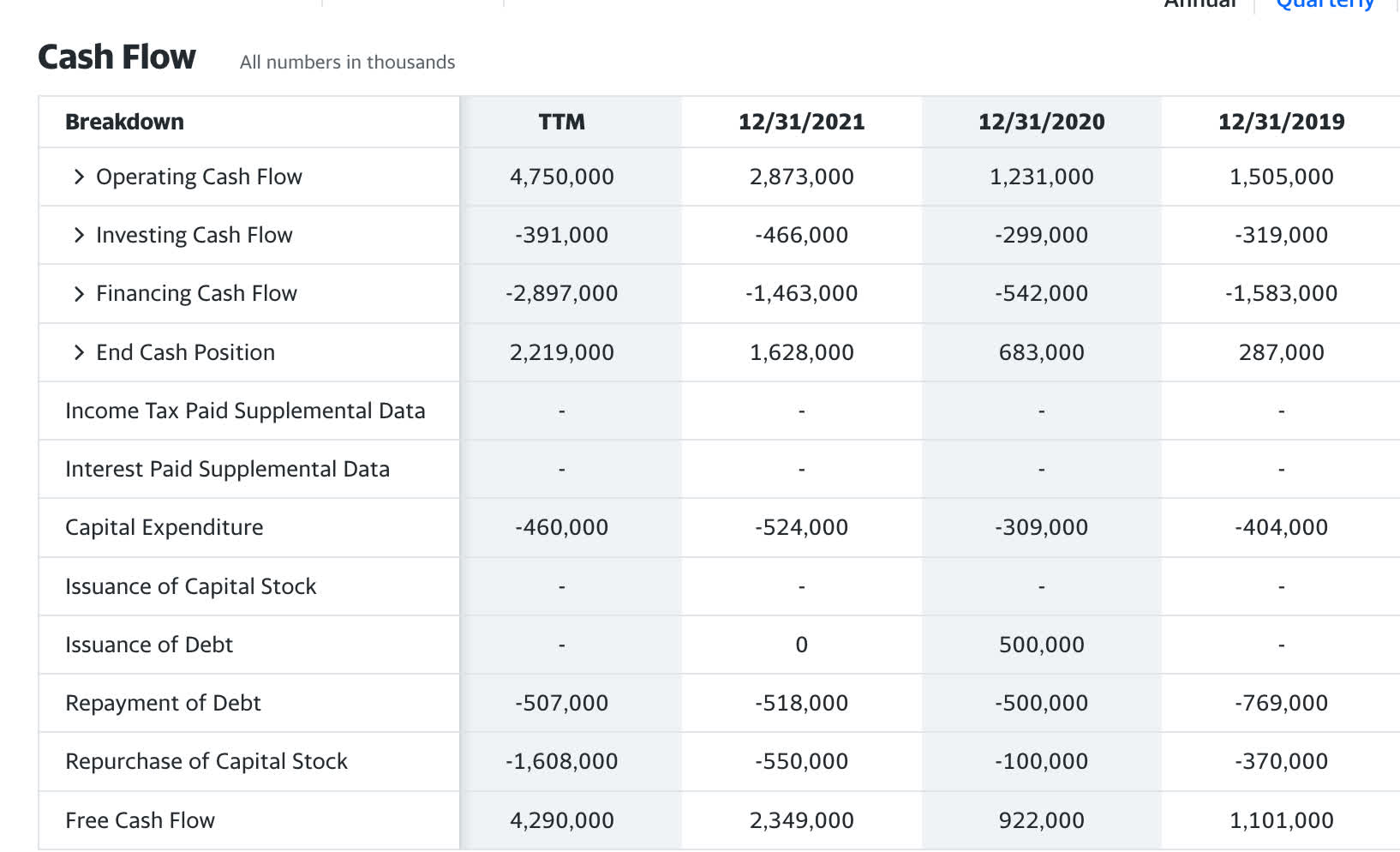

The forward dividend for CF industries is $1.6 a share with 207 million shares outstanding, a dividend liability of $331.2 million. The free cash flow for TTM sits at $4.29 Billion. This is a dividend coverage of 12.9 X. That is enormous and begs the question, will we see any special dividends or large increases in dividends per share in the upcoming year? Even with EPS in the $4 range for 2021 the company was able to generate $2.3 Billion in free cash flow. The shareholders are due for a nice increase as the current dividend is nothing to write home about. Fingers crossed.

Taking a look at the balance sheet

yahoo finance

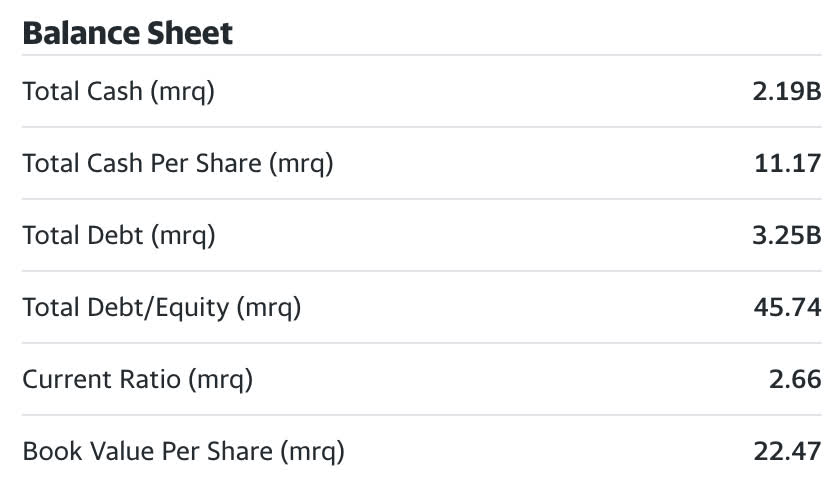

With a total debt load of only $3.25 Billion and a debt-to-equity ratio of 45.7 %, this is a strong balance sheet. $2.19 Billion in the bank plus $4 Billion in free cash flow could allow the company to wipe out all its debt within a year or so should it choose to. The current ratio is well over 2 X at 2.66. Hopefully, they keep up the good work with balance sheet management. If the macro environment continues to present high inflation and or stagflation for years to come, levering up and expanding operations shouldn’t be too difficult from here.

Catalysts

Continued, prolonged supply change issues that get worse, unfortunately, might be a catalyst for earnings growth. A commodities super cycle will see global reserve currency operators having a competitive advantage. The difficulty of expanding operations in countries that are trying to curb petroleum bi-product pollution in all ways could be an issue. ESG initiatives that may help expansion are also laid out in the 2021 10K:

we are on a path to decarbonize our ammonia production network – the world’s largest – to enable green and blue hydrogen and nitrogen products for energy, fertilizer, emissions abatement, and other industrial activities. Our nine manufacturing complexes in the United States, Canada and the United Kingdom, an extensive storage, transportation and distribution network in North America, and logistics capabilities enabling a global reach underpin our strategy to leverage our unique capabilities to accelerate the world’s transition to clean energy.

Additionally, as the largest producer of Ammonia, which is an efficient means of storage of hydrogen, green energy initiatives by CF could lead to a whole other line of revenue:

We are taking significant steps to support a global hydrogen and clean fuel economy, through the production of green and blue ammonia. Since ammonia is one of the most efficient ways to transport and store hydrogen and is also a fuel in its own right, we believe that the Company, as the world’s largest producer of ammonia, with an unparalleled manufacturing and distribution network and deep technical expertise, is uniquely positioned to fulfill anticipated demand for hydrogen and ammonia from green and blue sources

With ample free cash flow, now would be a great time to expand operations for future revenue growth. The stability that a producer of a product could provide to an end user when that end user knows the supply will not be cut off could garner premiums. If I had a farming operation, paying a bit more for CF Industry’s products versus one at risk of being in a sanctioned country one day might be worth it. Even though we don’t sanction food products and fertilizers, sanctions can hit payment methods. Executing on the right items to ensure capacity expansion is the biggest catalyst for me.

Risks

The biggest risk would be everything getting back to normal in the macro environment and inflation normalizing to 2-4%. The price of fertilizers will not be very sticky if a huge portion of the supply chain comes back online. Drops in prices of feedstock will be a leading indicator of fertilizer price drops in my opinion. Even if extra supply doesn’t come online, competitors will begin to undercut each other as the cost of goods sold begins to drop.

The primary competitors are Nutrien (NTR) and Koch fertilizers. Nutrien, the Canadian fertilizer juggernaut, has a higher mix of potash fertilizers and a similar price appreciation but has cooled off in momentum quite a bit versus CF Industries. CF further points out that the barriers to entry are low, therefore the price of the product is very competitive. Watch the prices of both feedstock and fertilizers closely.

Summary

CF Industries has been the benefactor of a macro environment that’s rough to all but a select few. They are one of the select few. The stock price would imply a $148 pt based on a PEG ratio incorporating 2023 numbers. It is severely undervalued based on almost any metric at 6.6 X earnings and 4.6 X free cash flow. Very little debt. Big Magic Formula score. Great balance sheet. The question an investor has to ask themselves is, how long will the party last? Xi Jin Ping just attended the G20. Some adversarial relationships seem to be trending towards normalization with inflation showing its first cooling pattern in a long time.

I would watch CF Industries Holdings and be cautious from here. The 45% upside is my trigger for a swing trade, if I hit that from here, I would be happy and most likely exit. Buy CF Industries Holdings, Inc., but be cautious.

Be the first to comment