chinaface

Occidental Petroleum Corporation (NYSE:OXY) is expected to release its 4Q 2022 financial results on 28 February. As a result of lower oil, natural gas, and LNG prices, I expect OXY’s 4Q 2022 financial result to be weaker than in 3Q 2022. Also, energy prices are expected to continue decreasing in 2023.

On the other hand, the U.S. is expected to remain the world’s leading source of supply growth, and crude oil and natural gas production in the Permian Basin is still increasing. Thus, despite lower commodity price realizations, OXY’s production volumes will remain high. The company is financially healthy and can remain profitable with the current energy prices as oil prices are still relatively high. Occidental Petroleum Corporation stock is a hold.

The market outlook

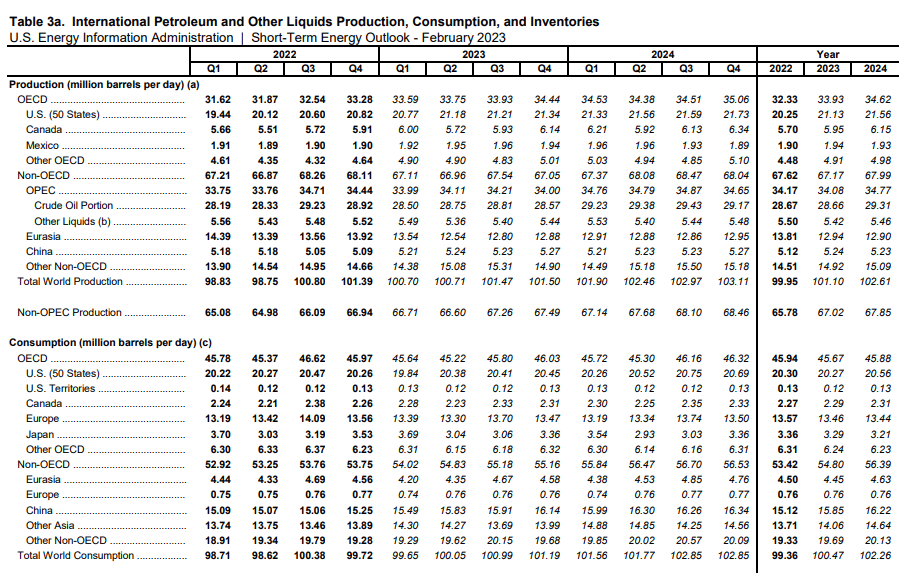

According to IEA’s January 2023 oil market report, as a result of the sudden reopening of China, the global oil demand is expected to rise by 1.9 mb/d to a record 101.7 mb/d. According to EIA’s short-term energy outlook, China’s oil consumption is projected to increase continuously in the following quarters.

IEA projects that due to oil production cuts in Russia (to retaliate against the European ban on seaborne imports and price caps for Russian oil products) and OPEC+ production cut to support oil prices, the world oil supply growth in 2023 will be lower than in 2022. Based on this market condition, the United States is expected to remain the leading source of crude oil supply growth. U.S. oil production in 2023 is expected to be 101.10 mb/d, compared with 99.95 mb/d in 2022. U.S. oil production in 4Q 2022 is estimated to be 20.82 mb/d, higher than in 3Q 2022. EIA projects U.S. oil production in 1Q 2023 to decrease to 20.77 mb/d, and then increase to more than 21.00 mb/d in the following quarters.

Based on EIA’s drilling productivity report, oil production in the Permian Basin in February 2023 is expected to be 5635 thousand barrels per day, compared with 5605 thousand barrels in January 2023. Also, gas production in the Permian Basin is expected to increase from 21615 million cubic feet per day in January 2023 to 21724 million cubic feet per day in February 2023. OXY’s income is significantly linked to its operations in the Permian Basin. Thus, I expect OXY’s oil and natural gas production volumes to continue increasing. On the other hand, I expect the company’s oil and natural gas realized prices to continue decreasing.

Figure 1 – International petroleum and other liquids production and consumption

eia

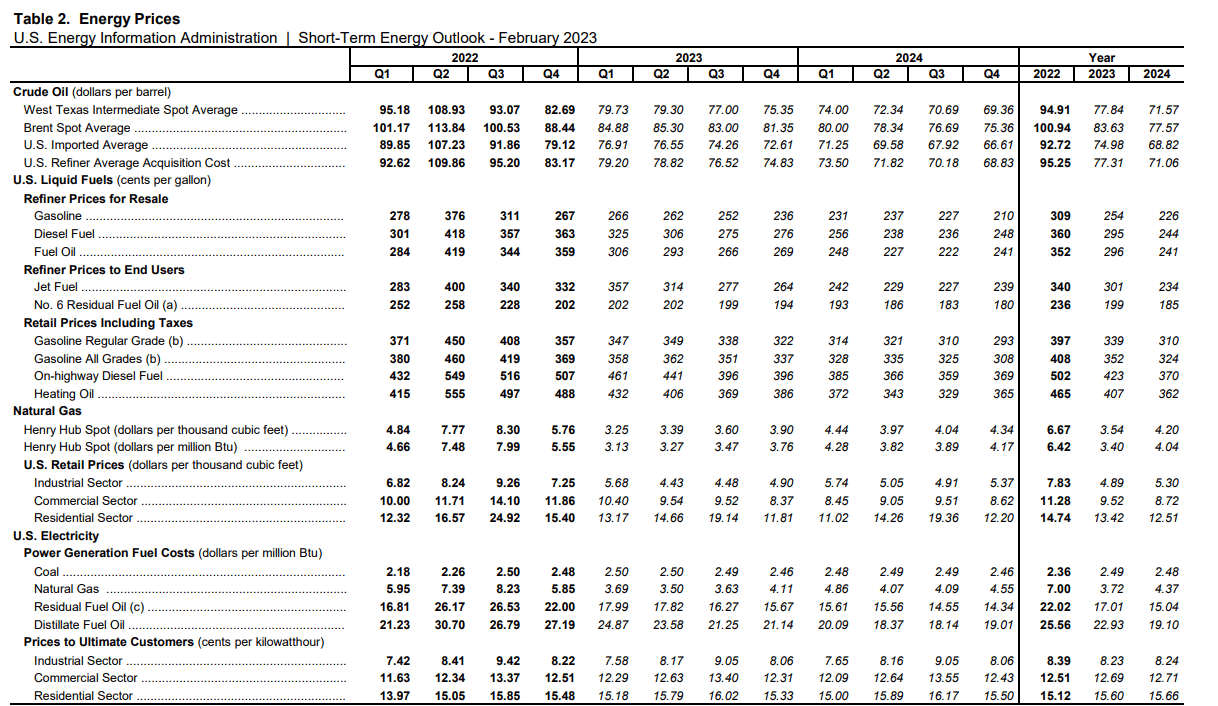

Figure 2 shows that WTI crude oil prices and Henry Hub natural gas prices in 4Q 2022 were significantly lower than in 3Q 2022. Also, WTI crude oil prices are expected to continue decreasing in the following quarters. Furthermore, as a result of warmer-than-normal weather that decreased natural gas domestic consumption in the United States, Henry Hub’s natural gas prices in the first quarter of 2023 are expected to fall by 44% QoQ to 3.25 per thousand cubic feet. It is worth mentioning that due to the Freeport’s restart in March, which can process up to 2.1 billion cubic feet of natural gas per day, natural gas prices may increase again. However, I don’t expect natural gas prices to increase to their 2022 levels.

Figure 2 – Energy prices

eia

OXY performance outlook

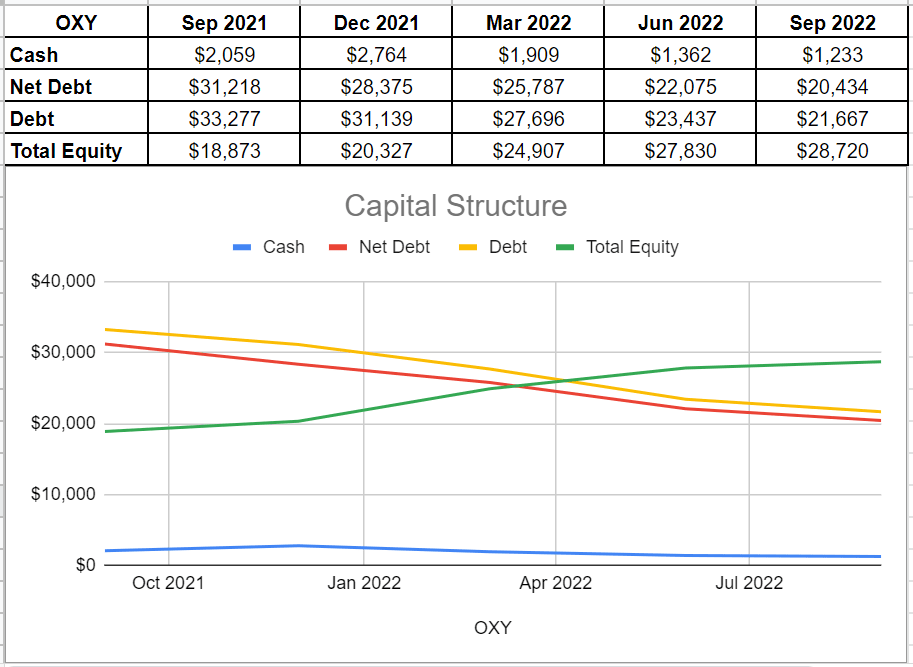

Since the first quarter of 2022, the company’s cash and equivalents decreased by 35% to $1233 million in 3Q 2022 versus its amount of $1909 million at the end of 1Q 2022. Also, the company’s drop in its debt amount of $23437 million in 2Q 2022 to $21667 million in the third quarter of 2023, combined with cash generation led to a 7% decline in its net debt. In minutiae, OXY’s net debt plunged from $22075 million at the end of the second quarter of 2022 to $20434 million at the end of 3Q 2022. Furthermore, OXY’s total equity improved slightly to $28720 million in 3Q 2022 compared with its previous amount of $27830 million at the end of 2Q 2022. Also, the company’s net debt is over 50% higher year-over-year versus its level of $18873 million in 3Q 2021. Thankfully, OXY’s net debt and total equity are well enough to tailor a scope of capacity to bring benefits for its shareholders and assimilate upcoming risks. Thus, Occidental Petroleum’s capital structure prospects a healthy position and enables the company to increase its distributions (see Figure 3).

Figure 3 – OXY’s capital structure (in millions)

Author (based on SA data)

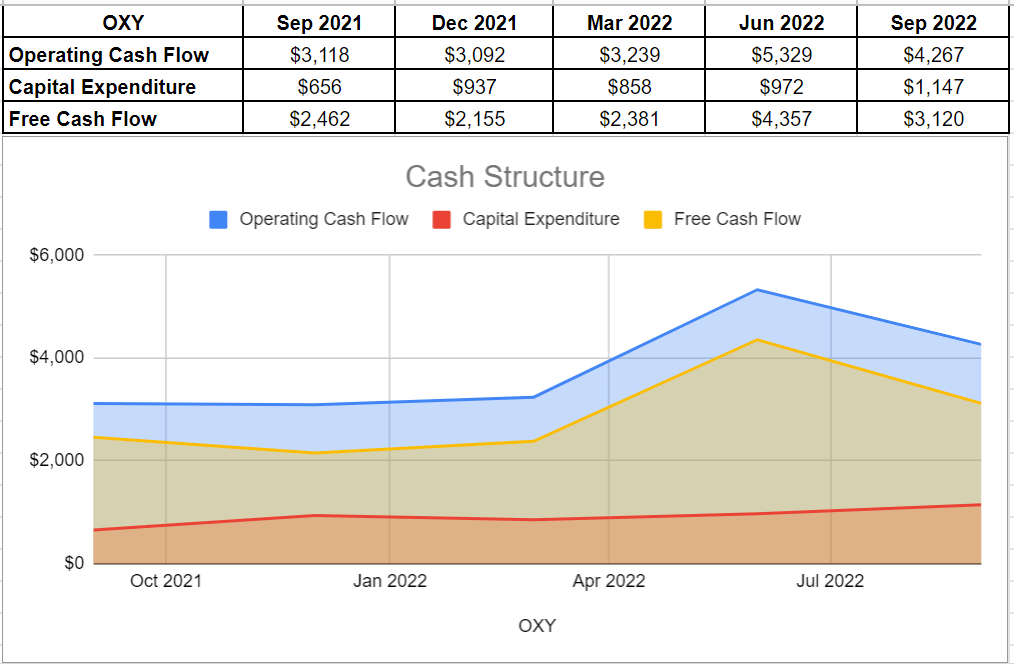

After the downturn of 2021 due to the COVID-19 pandemic, the company started the recovery process successfully. Albeit OXY’s cash operation boosted to $5329 million in 2Q 2022 compared with its amount of $3092 million at the end of 2021, its amount dropped back to $4267 million in 3Q2022. However, the cash operation in 3Q 2022 is still far higher year-over-year compared with its level of $3118 at the same time in 2021. Also, Occidental Petroleum’s capital expenditure increased slightly by around 18% to $1147 million in 3Q 2022 versus its previous amount of $972 million at the end of the second quarter of 2022. When all was said and done, the company ultimately generated $3120 million of free cash flow at the end of the third quarter, which indicates a 28% decline versus the amount of $4357 million in 2Q 2022. Notwithstanding a decrease, OXY’s free cash flow amount is still 26% higher year-over-year compared with its amount of $2462 million in 3Q 2021, which may cater to a scope of capability for more reliable distributions in case of stringer market outlook (see Figure 4).

Figure 4 – OXY’s cash structure (in millions)

Author (based on SA data)

Furthermore, I looked at Occidental Petroleum’s profitability ratios in this section to assess how well the company can turn a profit and use its assets to make money for its investors. I have examined the profitability ratios for margin, and return ratios to provide useful insights into the financial health of the company. I calculated the ratios in comparison to earlier quarters to be more helpful.

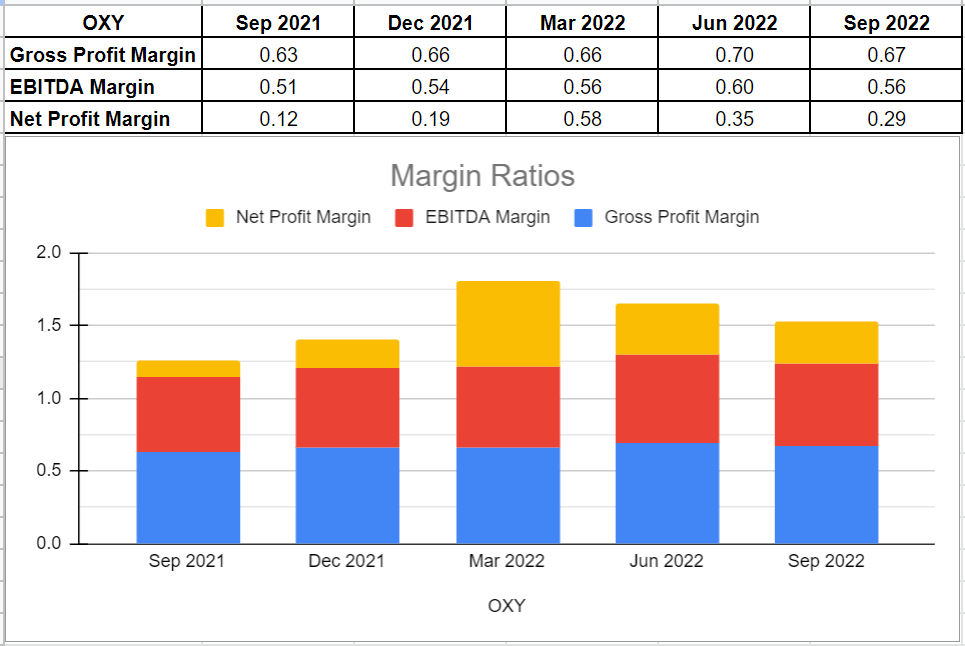

In general, margin ratios evaluate the ability of the company to turn revenues into profits in a number of ways. Due to the lower oil and gas prices in 2022, this energy company had weaker gross profit, EBITDA, and net profit margins in the third quarter compared with the second quarter of 2022. In minutiae, the total revenue of Occidental Petroleum declined by 12% from $10676 million in 2Q 2022 to $9390 million in 3Q 2022. A decline in revenue combined with the lower level of profits and EBITDA led to lower margin ratios in the third quarter of 2022.

OXY’s gross profit margin was 0.67 in the third quarter of 2022, which is slightly lower than its amount of 0.70 at the end of 2Q 2022. Also, the company’s EBITDA margin was 0.56 in 3Q 2022, which is 6% lower than the previous quarter and 9% higher year-over-year compared with its amount of 0.51 in 3Q 2021. Moreover, Occidental Petroleum’s net profit margin, which is a final picture of how profitable the company is after all expenses, dropped by 17% to 0.29 in 3Q 2022 versus its previous amount of 0.35 at the end of the second quarter of 2022. As a result, the weakening energy market conditions in the preceding year affected Occidental Petroleum’s revenue and declined its margin ratios. Also, because of lower crude oil and natural gas prices in 4Q 2022, I expect lower margin ratios for the fourth quarter of 2022 (see Figure 5).

Figure 5 – OXY’s margin ratios

Author (based on SA data)

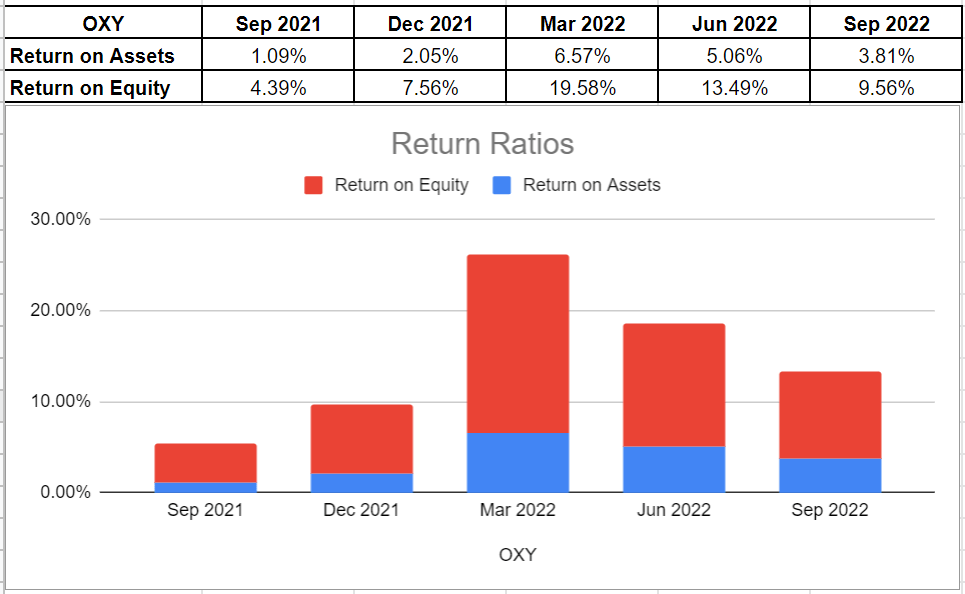

To wrap up the company’s performance outlook, I looked into OXY’s return on equity and return on assets ratios to show how well the company can tailor returns to its shareholders. The ROA ratio illustrates the amount of profit a company may produce for each dollar of its assets. The ROA ratio of 3.81% for Occidental Petroleum in 3Q 2022 decreased by 125 bps compared with its level of 5.06% in 2Q 2022 but is still far higher year-over-year versus its level of 1.09% in 3Q 2021. Additionally, its return on equity of 9.56% in the third quarter of 2022 is considerably lower than 13.49% in 2Q 2022. ROE ratio shows the company’s net income concerning shareholders’ equity and is important since it calculates the rate of return on the capital invested in the business. In other words, a decline of 17% in net income in the third quarter affected its return ratios. It means that the return ratios of Occidental Petroleum could indicate that the return circumstances of the corporation weakened due to the deficiency of the energy market, and to be honest, I anticipate similar results for the fourth quarter of 2022 (see Figure 5).

Figure 5 – OXY’s return ratios

Author (based on SA data)

Summary

As a result of high commodity price realizations and relatively high production volumes in 2022, Occidental Petroleum Corporation was able to improve its debt ratios significantly. Also, OXY increased its capital expenditures in the previous quarter to increase its share in the energy market of the United States. However, oil and natural gas prices decreased in Q4 2022 and are expected to decrease further in the following quarters. Thus, I don’t expect Occidental Petroleum Corporation’s financial results in 2023 to be as strong as in 2022. Occidental Petroleum Corporation stock is a hold.

Be the first to comment