imaginima

(Note: This article was in the newsletter on January 2, 2023.)

There has been a whole lot of prognosticating about the chart of Occidental Petroleum (NYSE:OXY) and more importantly, its prospects this fiscal year. But traders often miss out on the best runs of a stock like this. So, it is usually best to hang on. Warren Buffett (through Berkshire Hathaway (BRK.A)(BRK.B)) did not buy this stock for a one-year result. The same should go for the average investor who gets busy with work and family. So sometimes that same investor will not review a stock for a while. When he comes back the company still needs to be there focused upon improvement. Occidental still has to maximize the benefits from that acquisition. That still has not changed.

Similarly, Warren Buffett thinks the next few years are going to be decent or he would not have purchased the shares in the first place. Warren Buffett may not always be right. But he is right far more than he is wrong.

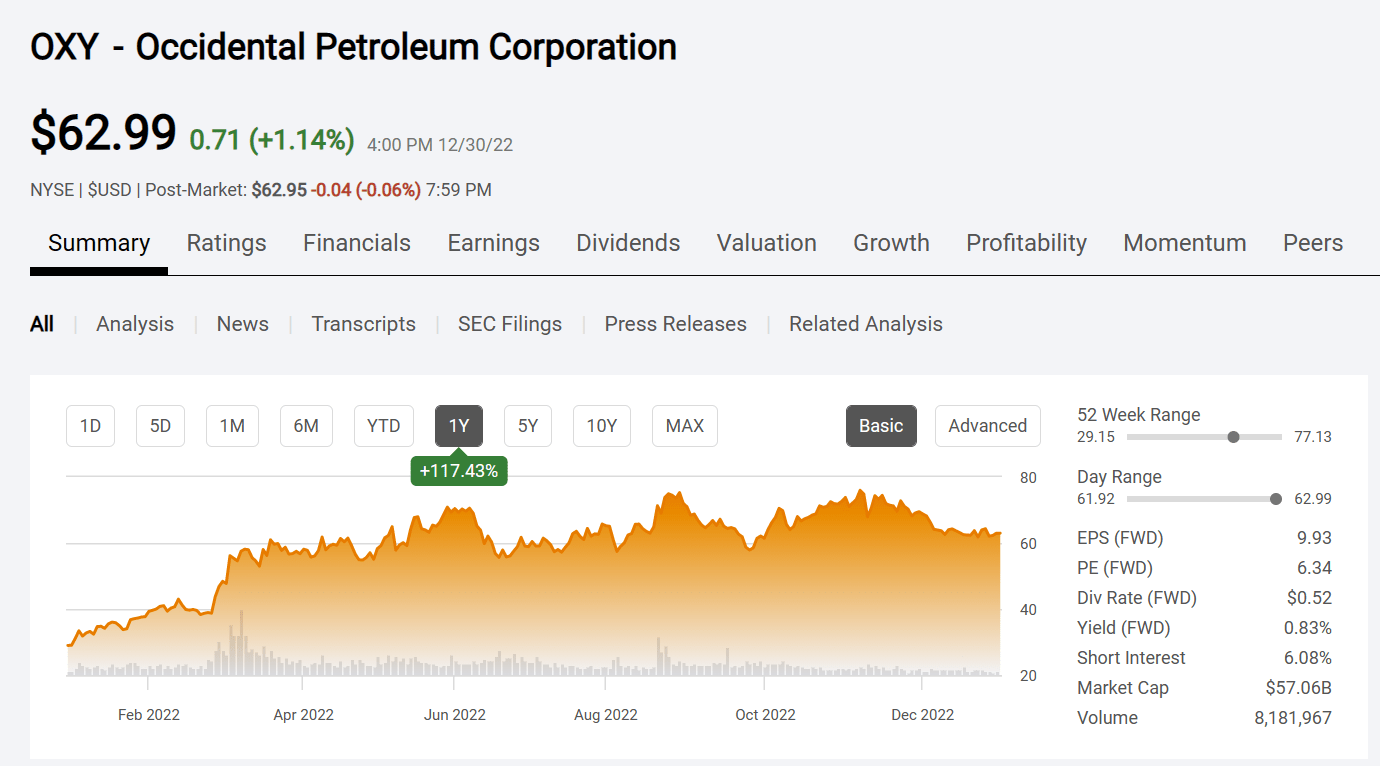

Occidental Petroleum Common Stock Price History And Key Valuation Metrics (Seeking Alpha Website January 2, 2023)

Shown above is what has “everyone” (“and their brother”) stating it is time to hold or sell. The stock has not gone anywhere since roughly June. So, all of a sudden you have “investors” and long-term “investors” stating it’s now time to sell and get out. It seems that long-term is still the time between breakfast and lunch.

But no one should sell on a chart unless they are a darn good technician. Typically, buy-and-hold investing means that the due diligence resulted in a strategy based upon that research. So, the investor should not be selling unless the original research-based assumptions have changed the investing strategy. A stock price action can indicate trouble. So, by all means, keep up on all the news. But selling because the stock has “gone nowhere” or even down is a good way to separate a long-term investor from his profits.

Whatever happened to a five-year horizon? Occidental just made a large acquisition a few years ago. Acquisitions like that take years to assimilate and optimize. Maybe right now with oil prices retreating it seems like it is time to get out. The problem with that is when you try to get back in, the stock will likely be 50% to 200% higher and you will have missed out on that money. That story has been repeated so many times I lost count.

Comstock Resources – An Example From The Past

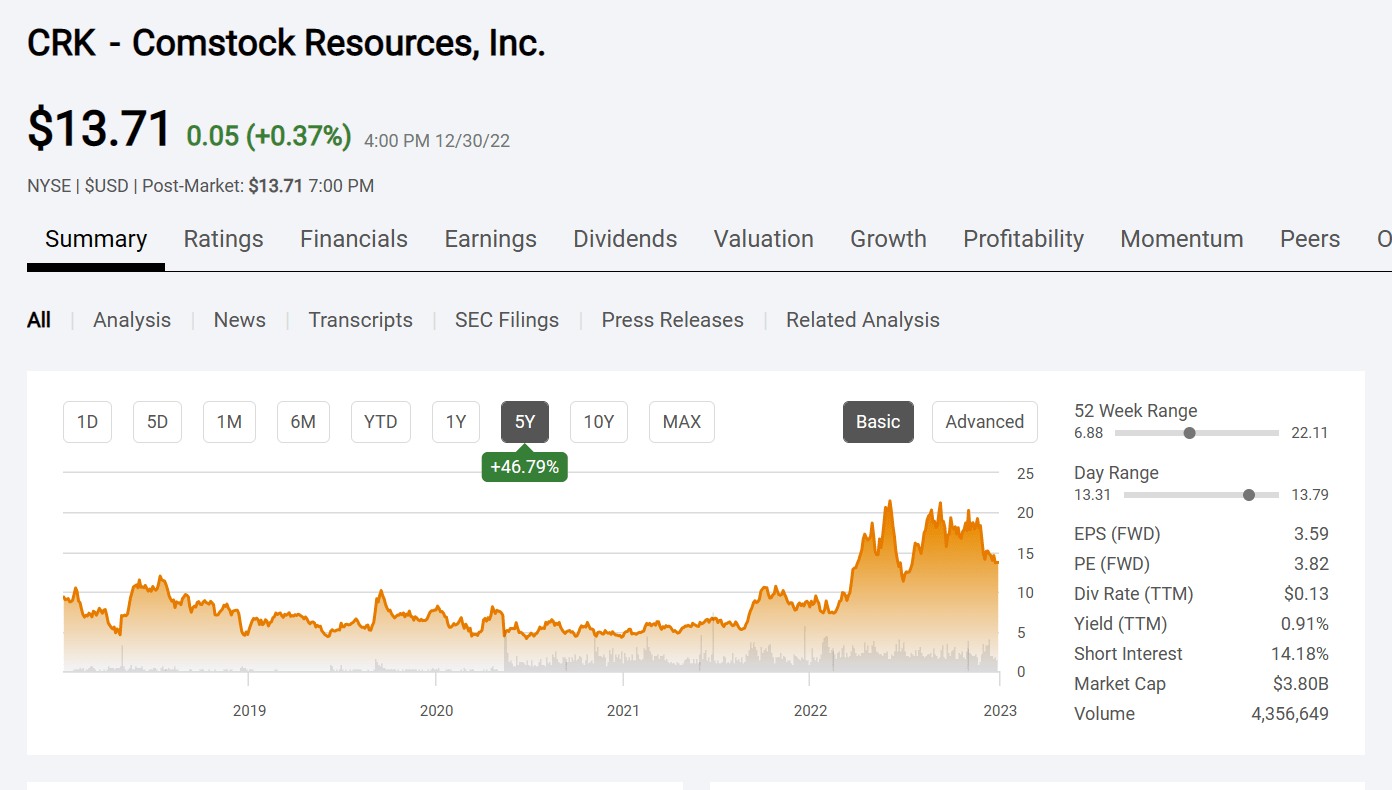

Comstock Resources (CRK) appeared to have seen its better days when Jerry Jones came along. Jerry Jones invested about 1 billion of his own money beginning in 2018 to turn things around. Had anyone decided to jump in then they would have been met by a price decline as shown below:

Comstock Resources Common Stock Price History and Key Valuat (Seeking Alpha Website January 2, 2023)

Even though Jerry Jones paid roughly $7 a share or maybe a little more on average, the stock price declined. Then 2020 hit to make things look even worse. But people like Jerry Jones wait for the strategy to play out. They don’t bail because the stock price “hit resistance” or because a pandemic hit. Now its fiscal year 2023. Jerry has had his positions a little more than 4 years and that position has roughly doubled from his initial investment.

I had more comments about this “dog” stock. Mostly the comments were that this was going nowhere. It actually went nowhere for quite a while. So, an investor would need to be as patient as Jerry Jones. I actually had some spare money and picked up 100 shares in the $4 range. I still have those shares.

But when did I get inquiries on this stock? Really, they picked up around $10. A lot of investors made money from roughly $10 to $13 and are patting themselves on the back. Meanwhile, Jerry Jones made money from the $7’s roughly to the current price. He is probably going for more gains as well. The problem with trying to time stocks is so many times it does not feel right to get in until a fair amount of gains are gone. That is usually the “easy money” too.

Far more importantly, Comstock has a pretty good future ahead. So even though the latest part of the chart “hit resistance” you can bet (forget the probably noted before) he is holding on for more gains. That is the big thing about investing. It is not catching every last price move. It is about waiting for the strategy you picked to play out. Once that value is achieved, then you sell. Given the outlook long term for natural gas, I suspect it will be years before Jerry Jones sells his stake (if indeed he ever sells it).

So What About Occidental

I am still waiting for the full exploitation of all the unexplored acreage that came with the acquisition. Originally that was about 10 million acres at really no value that came with the acquisition. Those acres do not need to average much value to make the acquisition a “steal”. Then there is the optimization of operations as the Occidental way gradually replaces older Anadarko production.

I am well aware that Occidental has talked about very slow, if any, growth in the immediate term. All one has to do is go back to the 1990’s when the newspapers screamed that oil prices were sky-high and production was not increasing. Does that sound familiar?

Back in the 1980s Saudi Arabia had re-entered the market and pushed the price of oil down to $10 or so for 4 years. Anyone with pencil and paper could figure out that would take a few years for the industry to recover from those years, and that is exactly what happened. The unconventional boom followed those newspaper headlines next along with industry growth that only recently stalled. The market is not quite as orderly as the public and investors would like. But it is the best system we have.

This time around the industry needs to recover from a pandemic. That should surprise no one. The credit markets became much more conservative after the aborted recovery in fiscal year 2020. Meanwhile, Mr. Market demanded return of capital rather than more growth. All of this is really just a replay of history. So, there is likely going to be some industry growth in the future. All an investor has to do is wait for it.

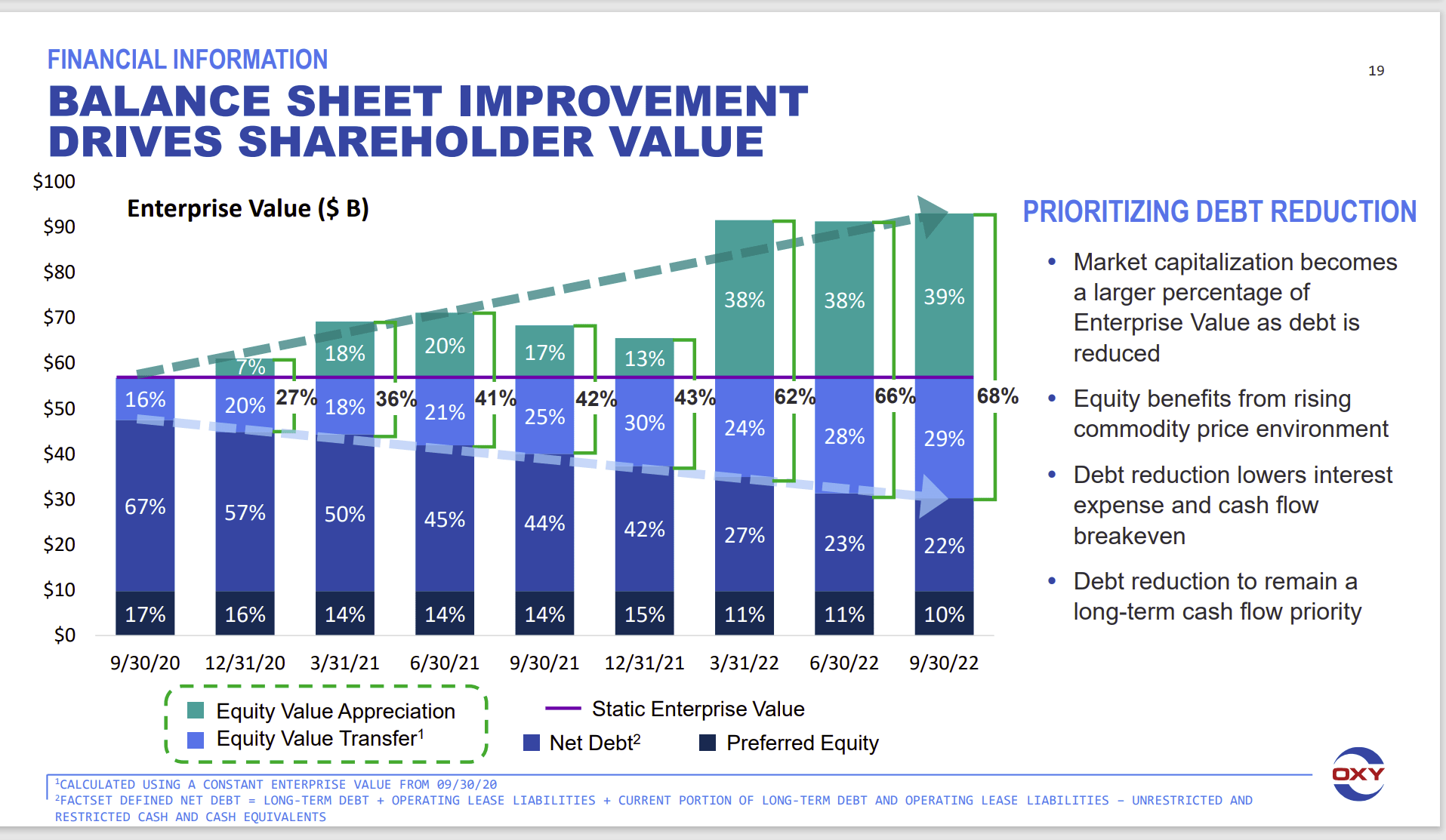

Occidental Petroleum Financial Strategy (Occidental Petroleum Third Quarter 2022, Earnings Conference Call Slides)

Sure enough, Occidental has spent much of the cash flow reducing the debt load. But the absence of a lot of interest expense alone is going to aid the earnings comparison in the current fiscal year. The next task is to retire the preferred shares. That is likely to begin in the current fiscal year.

There is going to be a venture into carbon capture and storage. But at some point, the growth that Occidental is known for will return. That unexplored acreage is not going to sit there forever.

Management has been busy cutting costs and optimizing operations. But that is going to continue for some time. Frankly, Anadarko was a mess and messes take time to turn around.

Permian

When it comes to Permian operations, Occidental is as big as they come. Furthermore, the CEO stated that there is a lot more potential to the Permian.

Vicki Hollub

“And I would add that, my view is that the world cannot afford a climate transition without — by cutting out completely oil and gas production. Oil production is going to be needed from decades — for decades to come and using CO2 in enhanced oil recovery is a way to produce a net 0 emission oil. And to have that as the fuel source, it’s low cost, lower cost than other options, it would help with the transition, it would help to fund the transition. So, I think that oil is needed for us, for our company, in particular, we have 2 billion barrels of resources available for further development in our enhanced oil recovery assets.

And we’d like to use either antibigenic or atmospheric CO2 for the — to develop those resources. In addition, we do know that we can technically use CO2 in the shale reservoir, so we can increase the 10% recovery that we have today to something much higher than that. So, it’s — there is a use for CO2 in enhanced oil recovery. It’s not as well recognized yet. But when the world realizes how much the transition will cost, I do believe that this will become the preferred option to ensure that we can continue the production of low-carbon fuel for those that need it.”

Source: Occidental Petroleum Third Quarter 2022, Earnings Conference Call Transcript

Occidental may have the largest EOR business in North America. So, when you get an opinion that secondary recovery for the unconventional business is the next way to increase recovery, that opinion probably has a lot of validity. Occidental potentially could not only sell some credits generated by carbon dioxide recovery, but they could also use that carbon dioxide to make still more money in the future. To me, the whole situation looks loaded with future potential for a lot of money.

Far from the unconventional business peaking, it is about to embark on still another stage of operations (secondary recovery) that the conventional business tackled a long time ago. Besides we still do not know how to get oil from shale. Nor do we know how to get oil from limestone formations (for example). So, there is a lot of oil out there that we need to develop the technology to get. I personally think that Occidental and others will be in the lead to develop that technology.

You have to remember that Tier one acreage was roughly a 3,000 foot well that flowed 200 barrels and did not suddenly dry up when I was a teenager. Then along came horizontal drilling and after that unconventional. I am an optimist that we will get better at extracting more oil from the ground. The country has plenty, we just have to keep technology moving as it has in the past.

The Future

Occidental is just getting started. The benefits from the Anadarko acquisition will become apparent in the future. Warren Buffett is not discouraged by a flat or even down year compared to fiscal year 2022. Neither should you be. He also does not pay a whole lot of attention to charts alone. Neither should most investors unless they have the time for it and the expertise.

This industry has such low volatility that we really do not know how 2023 will turn out. Last year it turned out that prices peaked early. I still remember when no one expected oil prices to be anything close to what happened last year. Expect that low visibility to continue.

What you can depend upon is that management saw value in Anadarko and that management will continue to get that value into shareholder’s pockets one way or another. Timing as always is uncertain. But to leave the stock now invites a purchase when the stock is 50% or more higher and you missed out on the easy money.

Warren Buffett saw something in this stock. He does not get involved for a 10% or so return. Neither should you. He at least sees the potential to double his money and probably more. But it is over time. So let us give management that time because I think management will make good use of that time.

Be the first to comment