Dzmitry Skazau

(This article was co-produced with Hoya Capital Real Estate)

Introduction

As of day, we know that the Democrats hold the Senate with the Georgia race deciding the degree (it effects committee and some rules), and the Republicans will control the House by an unknown amount, but less than 10. Congress being split should mean income tax rates should not change but extending today’s rates beyond 2025 is not likely either. While federal taxes might be frozen for now, investors still need to keep an eye on what the politicians back home are doing.

For investors in California, New Jersey, and New York, I provide links at the end to recent articles covering single-state CEFs for each. I also include links to funds that are AMT friendly for investors with that concern. Here I will review the only two Nuveen National Municipal Bond CEFs that show a positive return over the last five years, though not by much.

- Nuveen Select Tax-Free Income Portfolio (NYSE:NXP)

- Nuveen Intermediate Duration Municipal Term Fund (NYSE:NID)

Nuveen Select Tax-Free Income Portfolio review

Seeking Alpha describes this CEF as:

The Fund’s investment objective is current income exempt from regular federal income tax, consistent with preservation of capital. The fund invests in the investment-grade municipal securities rated Baa and BBB or better. It benchmarks the performance of its portfolio against the Standard & Poor’s (S&P) National Municipal Bond Index and Lipper General and Insured Unleveraged Municipal Debt Funds Average. The original NXP fund started in 1992. Its two related funds became part of NXP in late 2021.

Source: seekingalpha.com NXP

NXP has $639m in Total Managed Assets and provides investors with a 4% yield. Fees are only 24bps!

NXP holdings review

Nuveen provides a great set of data points from the end of the prior month.

nuveen.com NXP

Unlike some Nuveen Municipal Bond funds, both NXP and NID hold many fewer assets and have durations half the length of most. Those shorter durations help explain their superior performance as rates started climbing over the past year. Offsetting some of that is the 33% allocation to Zero-coupon bonds, where the price of a zero-coupon bond will decrease more than the price of a regular coupon bond when interest rates rise; all other things being equal.

Like corporate bonds, there are sectors within the municipal bond market.

nuveen.com NXP sectors

NXP has over 47% of its exposure to bonds dependent on tax receipts, the top two sectors. The next two sectors, Transportation and Health Care, comprising over 28% of the portfolio, could find their income sources hurt if another wave of lockdowns occurs. That said, the credit quality of the portfolio is very strong. Morningstar gives NXP’s portfolio an average rating of “A+”.

nuveen.com NXP ratings

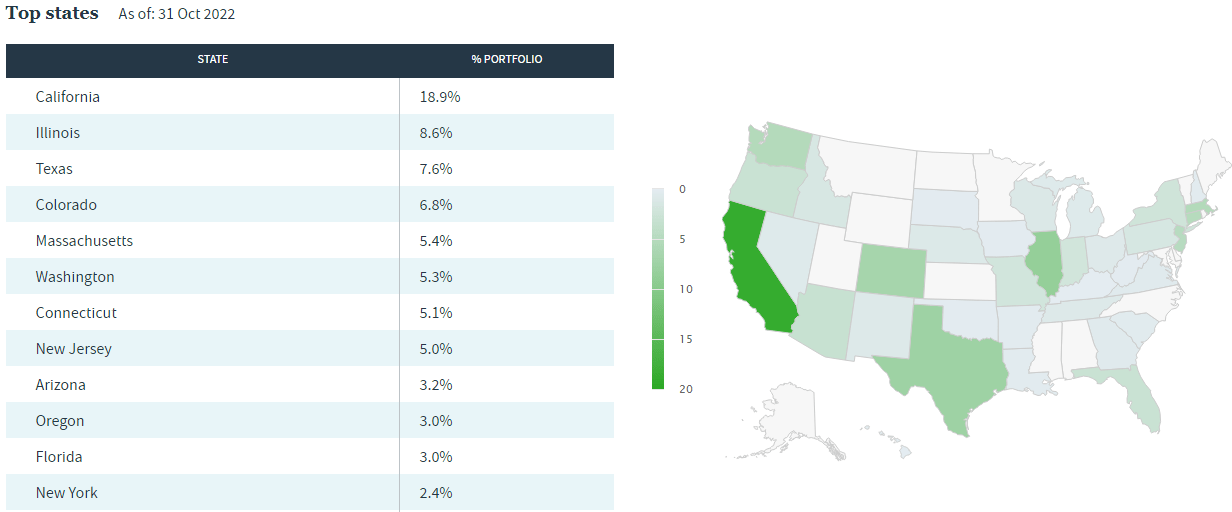

I showed the rating before the next table as a reminder they are more important, in my view, than allocations to states with poor ratings, such as Illinois, as all issues are not state-related. There are about 40 states represented, which helps diversify the economic exposure risk.

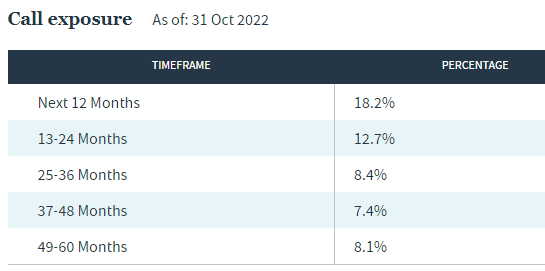

nuveen.com NXP states nuveen.com NXP Call schedule

Call exposure before 2026 is over 20%, though that risk diminishes as rates climb.

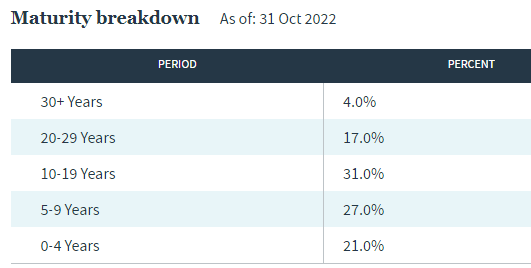

nuveen.com NXP Maturity schedule

As a reflection of its short, relatively speaking, average maturity of 13.3 years, NXP has 11% maturing in the next four years; hopefully an opportunity to redeploy funds into higher coupon bonds. Another risk measure, Issuer concentration, is minimal in my eyes too.

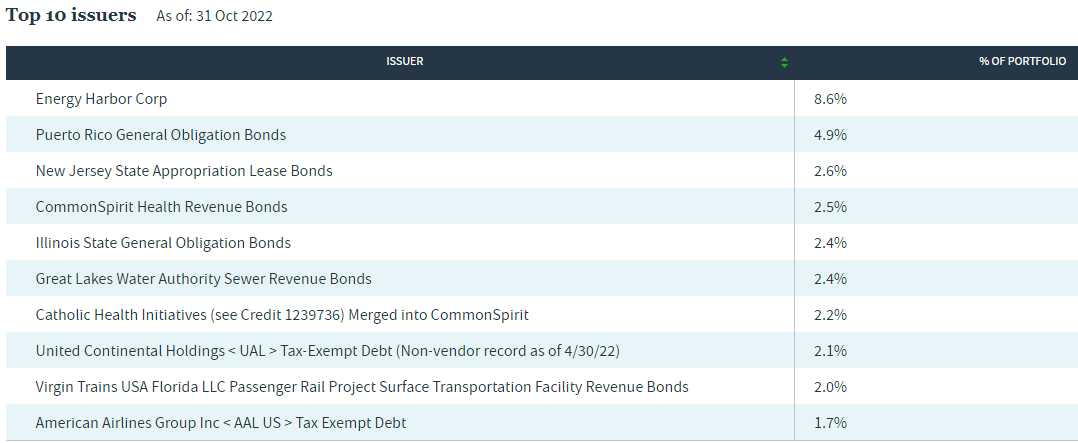

nuveen.com NXP Issuers

The top 10 Issuers are just over 25% of the portfolio and could represent multiple holdings for each one.

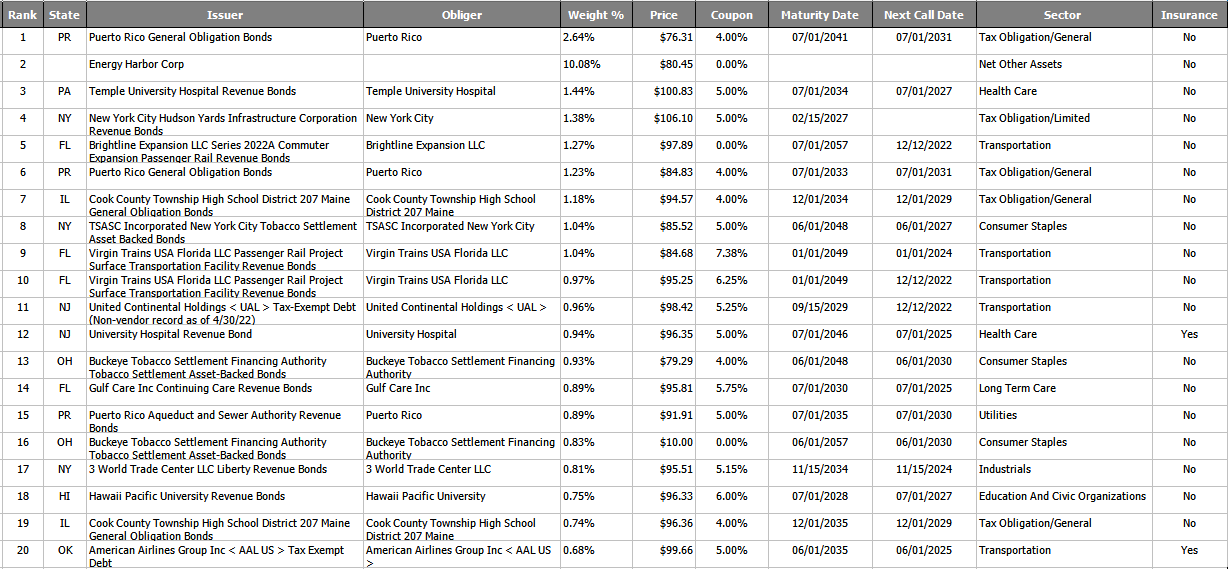

Top holdings

nuveen.com NXP holdings

Even with over 250 assets, the Top 20 still account for 25% of the portfolio. Providing protection against defaults, which are rare with municipal bonds, is the fact that 33% are covered against that event, plus another 8% are being pre-funded.

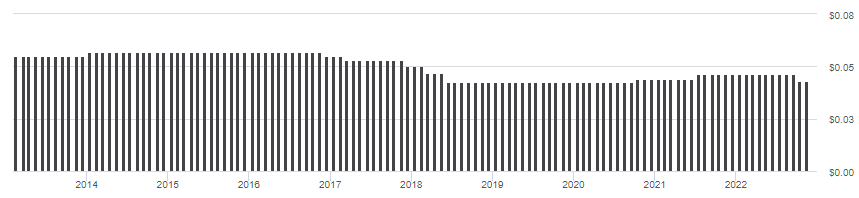

NXP distribution review

Nuveen also provides important data related to the fund’s distributions.

nuveen.com NXP payouts seekingalpha.com NXP DVDs

NXP has paid the same monthly amount since 2016, which means, unlike other Nuveen Municipal funds, it has not made cuts in 2022. With the latest earnings/distribution ratio just below 100%, the current payout seems safe.

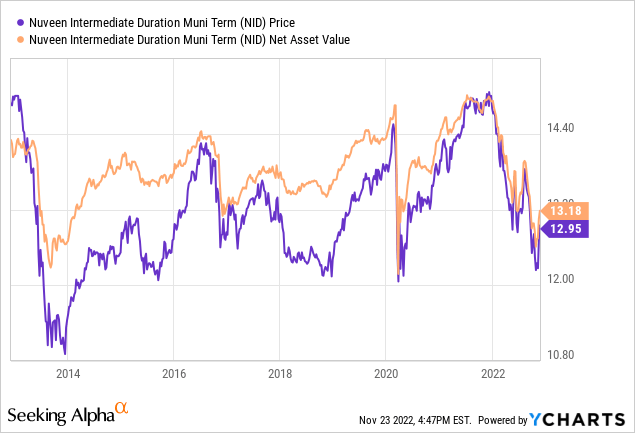

NXP Price and NAV review

CEFConnect.com NXP

NXP current sells at a -3.24% discount, within what seems its normal range, but unlike some CEFs, it has managed to sell where the price exceeded the NAV by over 5% several times, opening up the possibility of investors earning a better return.

Nuveen Intermediate Duration Municipal Term Fund review

Seeking Alpha describes this CEF as:

The Fund’s primary investment objective is to provide a high level of current income exempt from regular federal income tax. The Fund’s secondary investment objective is to seek additional total return. The Fund will invest at least 80% of its Assets in municipal securities and other related investments. The Fund invests in municipal securities that are exempt from federal income taxes, and seeks to maintain a portfolio with a levered effective duration of between 3 and 10 years, which takes into account the effects of leverage and optional call provisions of the municipal securities in the Fund’s portfolio. Benchmark: S&P Municipal Intermediate. NID started in 2012.

Source: seekingalpha.com NID

NID has $771m in Total Managed Assets, with $175m coming from their 34% effective leverage ratio. This results in a higher fee of 88bps; 46bps from the leveraging costs. NID also yields 4%.

Termination cancelled

Earlier this year Nuveen called for a shareholders meeting, requesting that the termination date for both the Nuveen Intermediate Duration Municipal Term Fund and the Nuveen Intermediate Duration Quality Municipal Term Fund (NIQ). At the October meeting, that request was approved, subject to these actions to be completed:

- Each fund must conduct a tender offer allowing shareholders to offer up to 100% of their common shares for repurchase at net asset value.

- If a fund’s aggregate assets attributable to common shares, taking into account common shares properly tendered in the tender offer, would be $70 million or greater, the tender offer will be completed and the fund’s term structure will be eliminated.

- If a fund’s aggregate assets attributable to common shares after the tender offer would be less than $70 million, the tender offer will not be completed and no common shares will be repurchased, the restructuring proposal will not be implemented and instead, the fund will proceed to terminate as scheduled pursuant to its original term, unless the fund’s Board of Trustees extends the term for up to twelve months in accordance with the fund’s charter documents.

It was noted that during the interim period, each fund may not be fully invested in accordance with its investment policies and may reduce its leverage in order to raise liquid assets in anticipation of payments to shareholders.

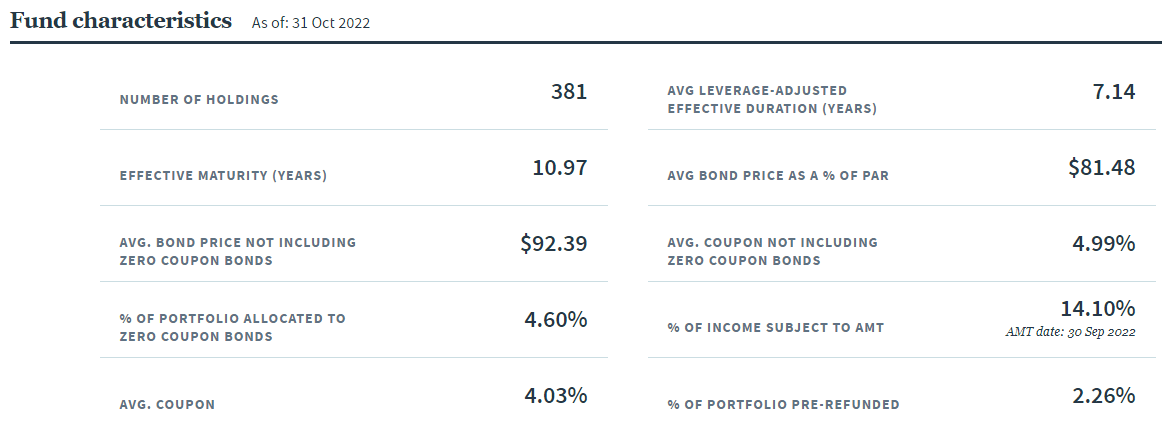

NID holdings review

Nuveen provided data for the CEF are:

nuveen.com NID

I will compare these against NXP later.

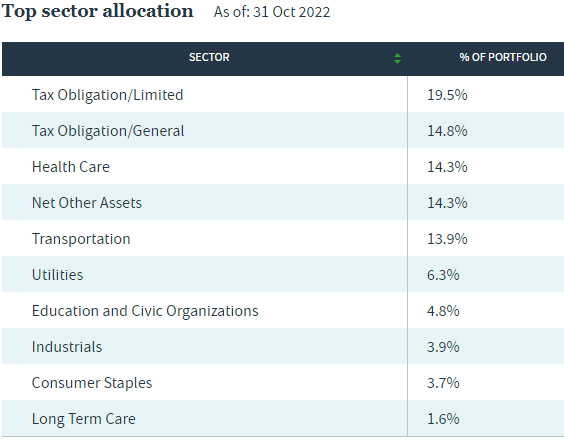

nuveen.com NID sectors

NID is less dependent on tax-backed bonds (34% vs 47%). Health Care and Transportation still play a major role (28% combined), but between those sectors is one labeled “Net Other Assets”.

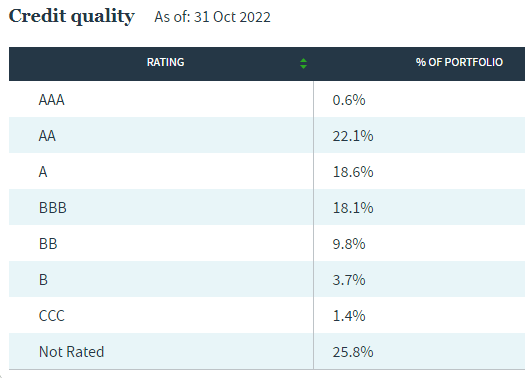

Making it harder to judge the credit risk is the fact that almost 26% of the portfolio is not rated. Morningstar did not rate this portfolio; my calculation gives it a “A-“.

nuveen.com NID ratings

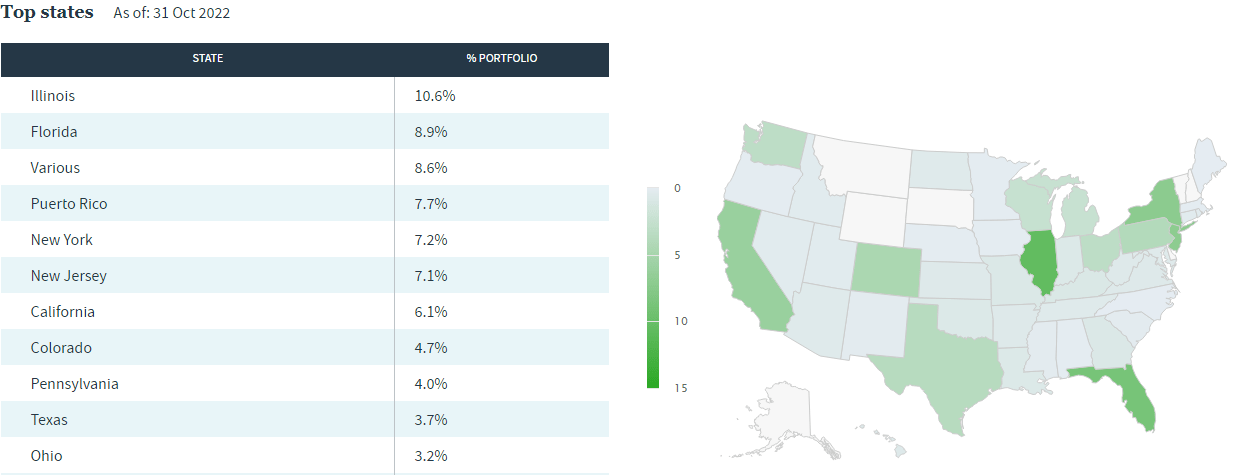

NID has close to 45 states included, slightly more than what NXP has.

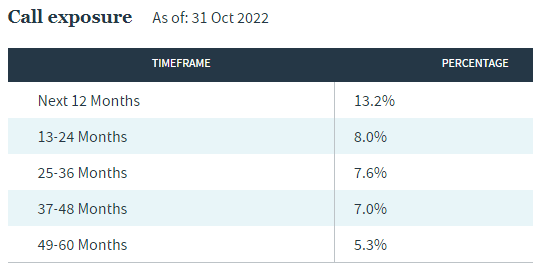

nuveen.com NID states nuveen.com NID Call schedule

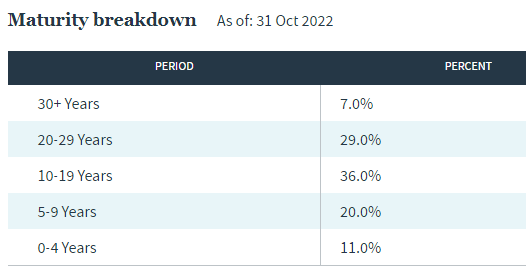

While the odds are decreasing, 31% of the portfolio is callable over the next 24 months. Maturity wise, 21% will mature before the end of 2026; hopefully some over the next year when rates are likely to peak.

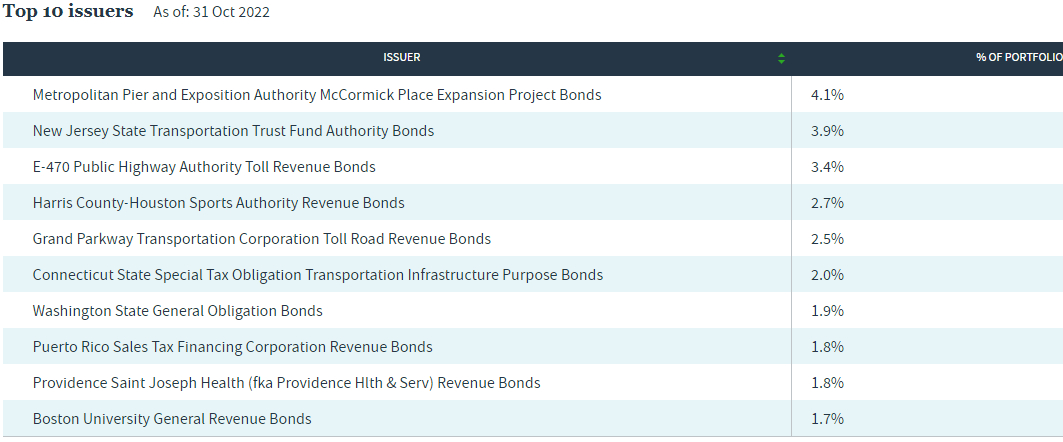

nuveen.com NID Maturity schedule nuveen.com NID Issuers

The top holdings, also owned by NXP, is most of the assets listed under the “Net Other Assets” sector, though the weight here is 6X what NXP’s exposure is. Energy Harbor resulted from the exit from bankruptcy of the old First Energy Corporation. The holdings are common stock. The rest of that sector is USD and futures.

Top holdings

nuveen.com NID holdings

NID is even more concentrated than NXP as the Top 20 are 30% of the portfolio. NID carries more risk in its portfolio by having only 13% insured. Most of the pre-funded bonds are also covered by that insurance.

NID distribution review

Nuveen provided distribution data points include:

nuveen.com NID payouts

Unlike NXP, this CEF is below 90% on covering its payout with earnings. That probably caused the payout cut earlier this year, with the current rate just above what it was two years ago.

seekingalpha.com NID DVDs

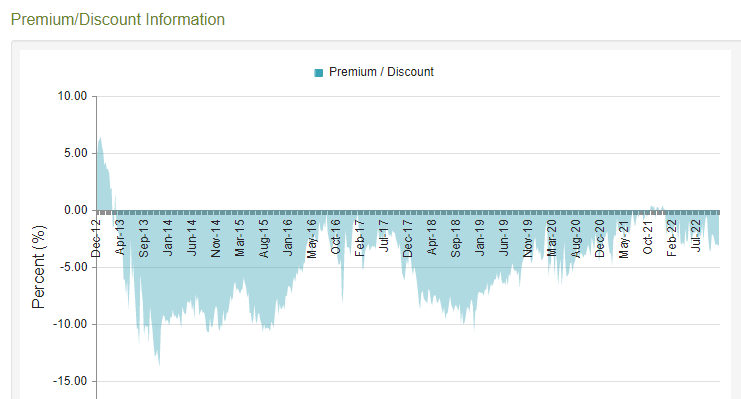

NID price and NAV review

CEFConnect.com NID

NID is currently at a 1.75% discount. While normal over the past two years, it has spent much of its life below a 5% level, over 7% being common. The big difference compared to NXP is how little time NID has sold at a premium.

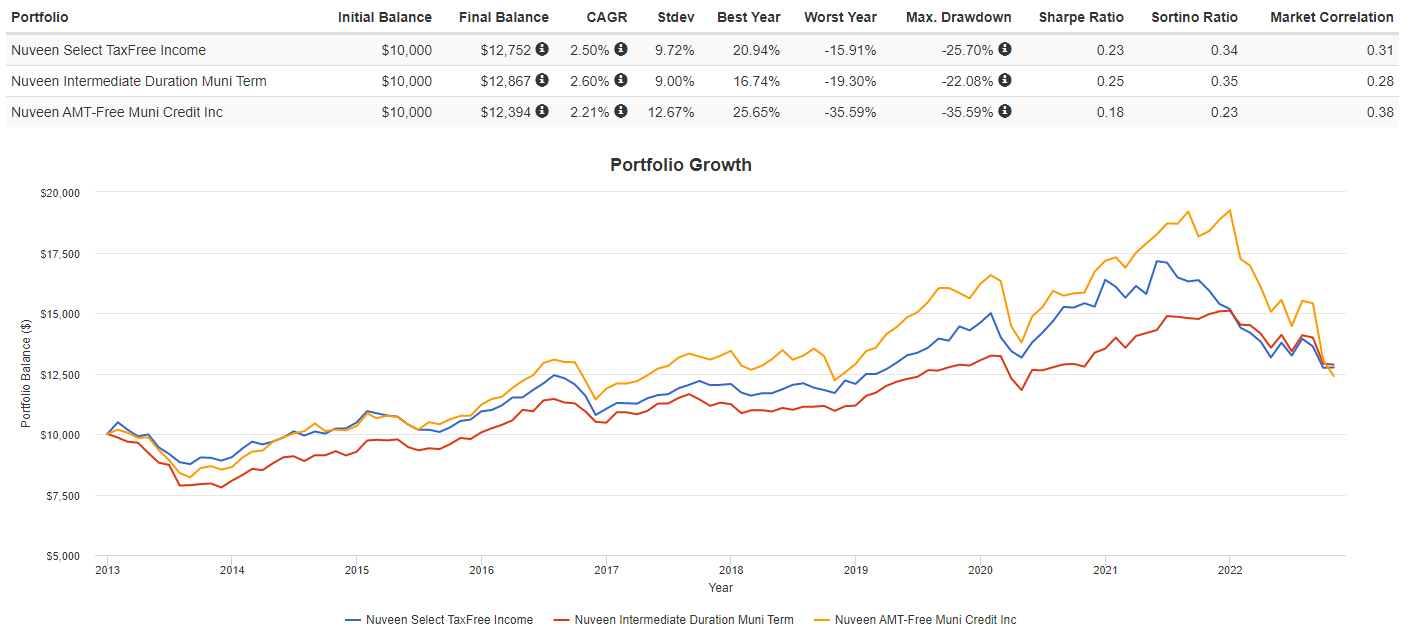

Comparing funds

Since my article on Nuveen AMT-Free Municipal Credit Income Fund (NVG) said investor should compare it against non AMT-free funds, I included it here for that reason, in reverse.

| Factor | NXP | NID | NVG |

| AUM | $639m | $771m | $4.45b |

| Fees | 24bps | 88bps | 207bps |

| Leverage | 0.0% | 34.1% | 44.1% |

| Premium/Discount | -3.24% | -1.75% | -7.91% |

| WA duration (yrs) | 7.74 | 7.14 | 17.04 |

| WA maturity (yrs) | 13.35 | 10.97 | 18.21 |

| Yield | 4.00% | 4.00% | 5.40% |

| 5-Year CAGR | 1.19% | 2.88% | -1.06% |

| Average Bond Price (non-zero) | $96.45 | $92.39 | $89.99 |

| Average coupon (non-zero) | 4.70% | 4.99% | 4.99% |

| Percent in Zero-coupon bonds | 33.0% | 4.6% | 12.7% |

PortfolioVisualizer.com

Both NXP and NID produced roughly the same results since NID started just under ten years ago. NVG was ahead until recently but has a history of being much more volatile. While the both have shorter durations and maturities than NVG, NXP and NID are close there. The two big differences is NXP’s lack of leverage and their high allocation to Zero-Coupon bonds.

Income wise, investors were rewarded for that extra risk, with again, NXP and NID being close.

PortfolioVisualizer.com

Portfolio strategy

For investors wanting to avoid AMT taxes, it appears using NVG is the best choice of these three and prior articles place it ahead of Nuveen’s other two AMT-free funds. With NXP achieving the same results without leverage, risk-adverse investors should prefer it over NID. One uncertainty right now with NID is the recent vote to not terminate. That might change how it allocates its portfolio by credit risk and maturities.

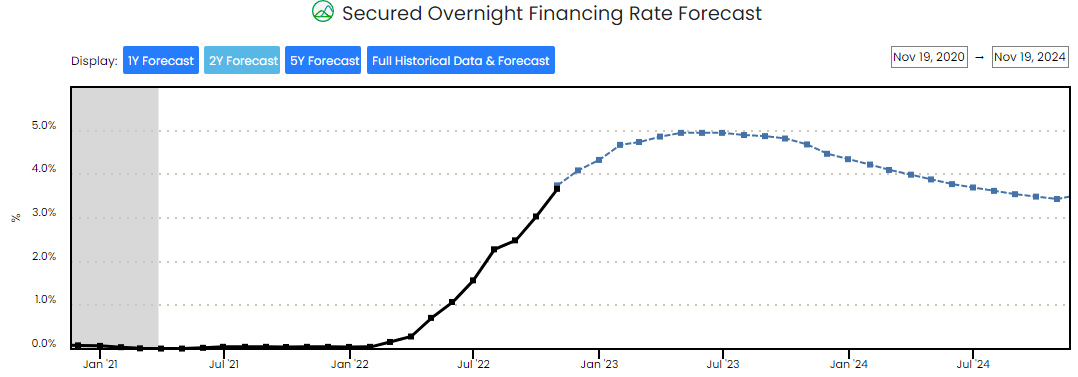

econforecasting.com/forecast-sofr

With rates forecasted to be climbing another 125bps by summer, sitting in cash or CDs until then might be the wisest play for bond funds. Investors sitting on losses might want to capture some, especially if they have gains that need offsetting for avoid a IRMAA income breakpoint.

Promised links

All these reviews were recent. Nuveen also offers single-state CEFs for Arizona, Georgia, Massachusetts, Minnesota, Missouri, Ohio, Pennsylvania, and Virginia. While the last two links are 100% ANT-free, most of the others have limited exposure to AMT income.

- NKX Vs. PCQ: Comparing CA-Only Muni CEFs

- MUJ Vs. NXJ: There Is A Clear Winner, NJ Residents

- NRK Vs. NAN: Comparing Nuveen NY State Municipal Bond CEFs

- NVG: Nuveen’s Best AMT-Free Muni Bond CEF

- NEA Vs. NUW: Clear Winner Between These Nuveen AMT-Free CEFs

Be the first to comment