Antonio Bordunovi

FYQ2 outlook and thesis

Things have changed rapidly for Nvidia (NASDAQ:NVDA) during the past few months. Let’s start with a recap of its Q1 FY2023 earnings reported on May 31, 2022, only less than 3 months ago. In that report, its gaming segment was a bright spot. The segment raked in total revenue of $3.6 billion, a healthy 6% growth from the previous quarter and a whopping 31% growth YoY. The RTX 30 Series has reported the best Gaming product cycle ever.

However, the business already felt weakness lurking. It provided an $8.1 billion sales guidance for Q2, representing a 2% contraction compared to Q1, largely driven by a sequential decline in its Gamin segment. Although the guidance still represents a 25% YoY growth.

NVDA Q2 FY2023 ER

Now, its Q2 preliminary results turned out to be much worse than the above guidance. According to the following Reuters report, the key takeaways are (slightly edited and emphases added by me):

Nvidia Corp on Monday warned its second-quarter revenue would drop by 19% from the prior quarter on weakness in its gaming business… Nvidia said its gaming unit’s preliminary revenue, which includes sales of high-end graphic cards for desktops and laptops, declined 44% from the previous quarter to $2.04 billion.

So, its Q2 revenue would contract by 19% from the previous quarter instead of the anticipated 2%. And the game unit’s 44% contraction reminds me of the cryptocurrency winter it suffered in 2018, as discussed immediately below. This leads me to the main thesis here too. I am seeing similar effects from the crypto crash on both its stock prices (through market psychologies) and fundamentals (through its exposure to crypto mining).

Anatomy of the 2018 crypto winter

The following charts show the anatomy of the 2018 crypto winter, with the top panel showing the Bitcoin USD (BTC-USD) prices and the bottom panel showing NVDA quarterly operating revenue YoY growth. As you can see from the top panel, Bitcoin prices collapsed from over $19k at the peak in 2018 to about $3.6k in a year (a decline of 81%, which would take a 427% rally to breakeven). And NVDA’s quarterly operating revenue turned from a 40%+ expansion to a ~40% contraction in tandem.

NVDA used to provide an estimate of its exposure to crypto mining in the past. For example, in 2018, NVDA estimated that its crypto-related sales were about $0.6B (about 5.7% of its $10.6B total sales). While another independent analyst (Mitch Steves at Business Insider) provided a much higher estimate of $1.95 billion of revenue related to crypto/blockchain (about 18.4% of its then overall revenues). I am guessing the true answer is somewhere in between the above two estimates.

Currently, we are experiencing a similar collapse in bitcoin prices. Bitcoin prices plunged from over $65k in Nov 2021 to the current $23.8k (a 64% decline, which will take a 173% rally to break even). And now, we will need to estimate how much impact this collapse will create for NVDA this round.

Seeking Alpha

Will the 2018 crypto winter repeat?

NVDA does not provide estimates of crypto-related sales anymore, and the range of estimates has become even wider in my view. On the one hand, its CFO Colette Kress commented (abridged and emphases added by me) during its FY Q1 earnings that it’s difficult to get such an estimate, but NVDA expects a diminishing going forward.

…the extent in which cryptocurrency mining contributed to Gaming demand is difficult for us to quantify with any reasonable degree of precision. The reduced pace of increase in Ethereum network hash rate likely reflects lower mining activity on GPUs. We expect a diminishing contribution going forward.

On the other hand, its latest 10-Q acknowledged the risks associated with crypto mining in quite specific languages (emphases added by me):

Changes to cryptocurrency standards and processes including, but not limited to, the pending Ethereum 2.0 standard may decrease the usage of GPUs for Ethereum mining as well as create increased aftermarket resales of our GPUs, impact retail prices for our GPUs, increase returns of our products in the distribution channel, and may reduce demand for our new GPUs.

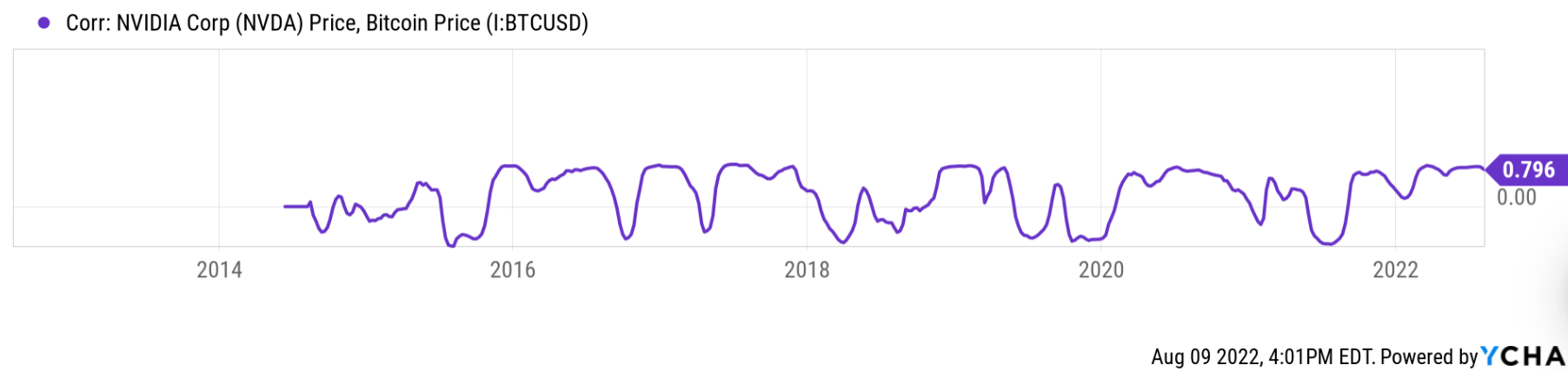

Although from all these following data points that I’ve gathered, I am suspecting that NVDA still has a large exposure to crypto mining. First, this Reuters report estimated that NVDA has actually increased the supply of cryptocurrency mining processors in recent quarterly and that crypto-related sales contributed $266 million in Q2 last year. Second, the large crypto mining exposure would help to explain (not prove though) the 44% quarter-over-quarter decline in revenue from its gaming segment. Finally, as you can see from the following two charts, NVDA is quite strongly correlated to bitcoin prices both in terms of stock prices and EPS. The first chart shows a fluctuating correlation between bitcoin prices and NVDA stock prices, reflecting largely market psychology. Although the long-term average is a positive 0.26, currently, the correlation is near a peak level of around 0.8. The second chart shows the correlation between bitcoin prices and NVDA EPS, which is more reflective of business fundamentals. And as can be seen, the correlation here is more stable and also positive most of the time. The long-term average is also stronger at 0.49. And the current correlation of 0.72 is also near a historical peak.

Seeking Alpha Seeking Alpha

Difference between 2018 episode and this one

Finally, my view is that the 2018 crypto crash was largely caused by market psychology. This ongoing 2022 episode, in contrast, does have a fundamental aspect due to Ethereum’s pending network transition from proof-of-work to proof-of-stake (the so-called Merge). The Merge is expected to take place in late September 2022. This Merge is expected to force the mining industry to find other ways to make money (thusly impacting the fundamentals of the crypto business) and also to slow processor usage as well (thusly impacting chip businesses like NVDA).

Final thoughts and other risks

In summary, I see the current developments surrounding crypto mining and NVDA as a replay of the cryptocurrency winter in 2018. During the 2018 episode, Bitcoin prices crashed by more than 80% in one year, and NVDA’s quarterly operating revenue growth turned from 40%+ to negative ~40%. In this 2022 episode, we are seeing a 64% decline in bitcoin prices since Nov 2021 and a 44% QoQ contraction in NVDA’s gaming revenues. Going forward, I am still seeing signs indicating NVDA’s substantial exposure to crypto mining, either directly or indirectly. And as a result, I am anticipating the pressure from the crypto crash to persist on NVDA both due to market psychology and also business fundamentals.

Besides the above exposure to crypto mining, NVDA also poses relatively high valuation risks as you can see from the following chart. Compared to other chip stocks, NVDA is priced at a substantial premium, both in terms of topline and bottom line metrics. Take its FW PE as an example. Its FY1 PE currently stands at 38x even after the recent large corrections. That is more than 65% higher than AMD and more than 2x or even 3x higher than other players such as AMD, INTC, QCOM, and AVGO.

Seeking Alpha

Be the first to comment