Justin Sullivan/Getty Images News

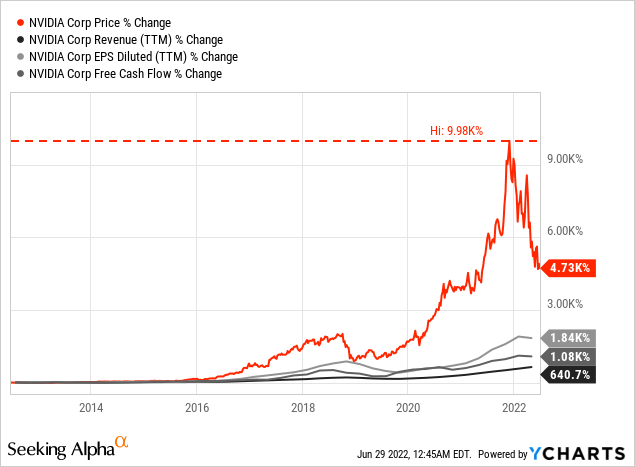

NVIDIA Corporation (NASDAQ:NVDA) was one of the great growth stories of the last ten years. While revenue increased 641%, free cash flow increased 1,080% and earnings per share increased even 1,840%.

These are without doubt impressive fundamental numbers, but the stock price increased even 5,330% in the last ten years (and at the peak in late 2021, the stock increased even 9,980%). While it might seem that the stock price simply outran the fundamental performance in the last ten years, we also must keep in mind the extremely low multiples the stock was trading for ten years ago (we will get to that).

Nevertheless, we not only have to ask if the valuation multiples of the last few quarters were justified (probably not), but also if current valuation multiples are justified. Especially when considering the low valuation multiple Intel Corporation (INTC) is trading for right now, we must ask if NVIDIA is deserving a much higher valuation multiple. And not every impressive growth story is also a great long-term investment with a wide economic moat that will protect the business in the years to come.

Stock Price Justified?

I already mentioned above that NVIDIA is much more expensive than its competitor Intel, and you might instantly have found several reasons why the comparison is completely off. NVIDIA was growing at a high pace and was an investors’ darling, while Intel was the opposite in the last few years.

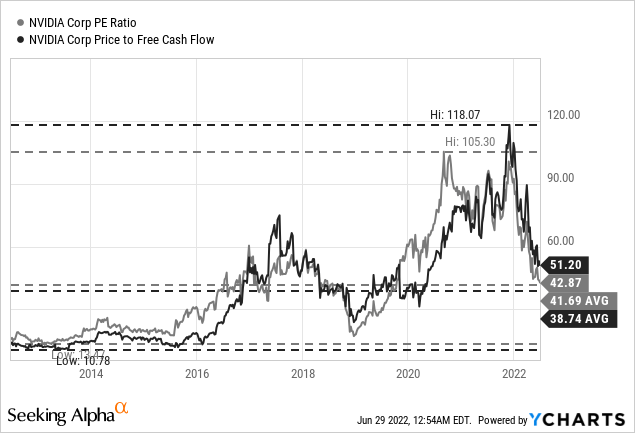

Nevertheless, NVIDIA seems to be expensive when looking at simple valuation metrics, as NVIDIA is still trading for a P/E ratio of 43. While this is in line with the average of the last ten years (41.69) and clearly below the peak P/E ratio of 105.30 (reached in 2020), we still can’t make the argument that NVIDIA is cheap. When looking at the price-free-cash-flow ratio, NVIDIA is still trading for 51 times free cash flow, which is below the peak of 118 set a few months earlier but well above the average of the last ten years (38.74).

I know many might disagree with me, but when stocks are trading for valuation multiples of 50 or higher, I usually get very cautious if the stock price is justified and if we are actually talking about a great investment or not just a hyped stock. In the following sections, I will present different reasons why I think the valuation is not justified. We will talk about the last quarterly results, the potential recession and its consequences, as well as the economic moat of NVIDIA and the question how long the business can grow with such a high pace.

Quarterly Results

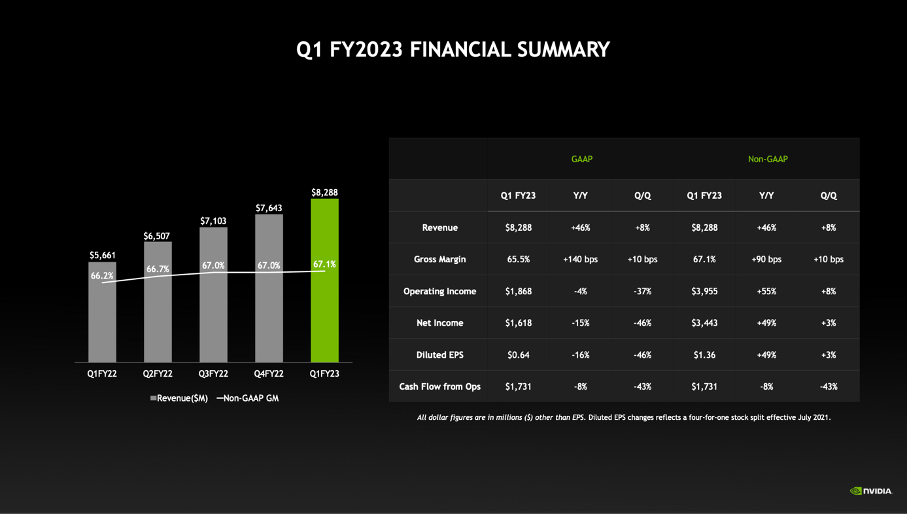

The last quarterly results NVIDIA reported (for the first quarter of fiscal 2023) might have been a first small warning sign. While the company could still beat earnings per share as well as revenue estimates and increased revenue from $5,661 million in the same quarter last year to $8,288 million this quarter (resulting in 46.4% year-over-year growth), the results were still rather mixed. Operating income declined from $1,956 million in the same quarter last year to $1,868 million this quarter (resulting in 4.5% YoY decline) and diluted earnings per share declined from $0.76 in the same quarter last year to $0.64 this quarter – a decline of 15.8% YoY.

NVIDIA Q1/21 Presentation

And during the earnings call, management was still optimistic about the long-term trends being intact, but expected slowdowns for the next quarter:

However, we started seeing softness in parts of Europe related to the war in the Ukraine and parts of China due to the COVID lockdowns. As we expect some ongoing impact as we prepare for a new architectural transition later in the year, we are projecting Gaming revenue to decline sequentially in Q2.

Management also mentioned cryptocurrencies as a potential issue in the last earnings call:

The extent in which cryptocurrency mining contributed to Gaming demand is difficult for us to quantify with any reasonable degree of precision. The reduced pace of increase in Ethereum network hash rate likely reflects lower mining activity on GPUs. We expect a diminishing contribution going forward.

Recession

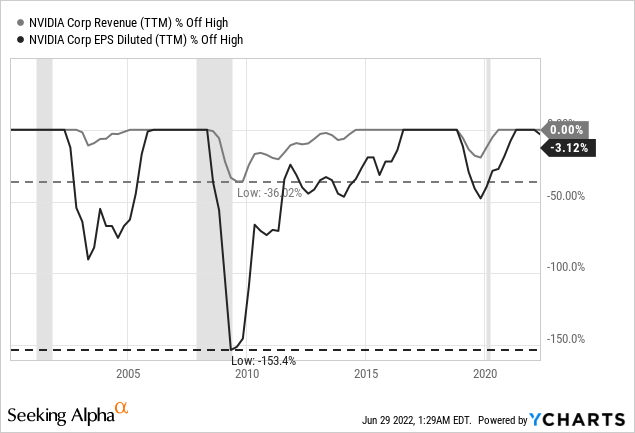

Although NVIDIA could grow with an extremely high pace in the last two decades, we can clearly see that the business was impacted by recessions. And while we can argue if the declines right before the COVID-19 recession and after the recession in the early 2000s might only be a coincidence, the decline following the Great Financial Crisis is hard to ignore. While revenue declined 36% in the following quarters, earnings per share declined 150% and turned negative. It also took several years before NVIDIA could reach pre-crisis levels again.

And in my opinion, we should not be too optimistic about the next (and probably upcoming) recession, as I would assume NVIDIA will be hit hard again. Among other things, NVIDIA is relying on gamers as well as the creator economy. And while the creator economy is estimated to be at $100 billion already and growing, as well as about 100 million new gamers coming into the PC industry in the last two years (according to NVIDIA earnings call), I expect NVIDIA to be hit hard in case of a recession.

I also see the long-term trend towards a creator economy and people working more from home, which are tailwinds for NVIDIA. However, I also see the possibility of a recession having a huge negative impact on the creator economy, on cryptocurrencies and crypto mining, as well as gaming. I might be wrong, but in case of a severe recession in the United States (and many other countries around the world), people suddenly might not have the time and money anymore to spend huge amounts on gaming.

I also see it as a likely scenario that cryptocurrencies – including Bitcoin (BTC-USD) – will implode during the next recession. And the creator economy might also be among those getting hit hard by a recession. As a result, I would not be surprised if demand is slowing down in the next two or three years due to an economic contraction.

Growth Rates Sustainable

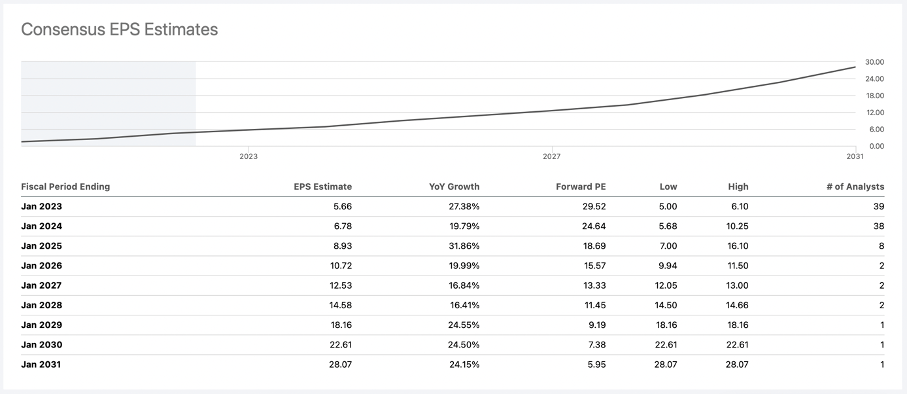

Aside from a potential recession that might lead to growth rates slowing down we also have to ask how sustainable these extremely high growth rates are. NVIDIA could grow with a high pace in the last decade – revenue increasing with a CAGR of 22.67% and earnings per share increasing with a CAGR of 36.76%. But the decisive question is rather if NVIDIA can continue to grow with a high pace in the years to come. And at least analysts seem to be extremely confident that NVIDIA can continue its outperformance – until fiscal 2031 analysts are expecting earnings per share to grow with a CAGR of 22.74%.

Seeking Alpha

And it is easy to imagine that NVIDIA will continue to grow, as the company will probably profit from several megatrends in the coming years and decades. We usually tend to extrapolate existing trends into the future – which can make a lot of sense, but sometimes be also extremely dangerous. The list of companies that underlined the dangers of just extrapolating high growth rates into the future is long: PayPal (PYPL), Meta Platforms (META), and Target (TGT) might be some recent examples. And while I am a shareholder of all three and confident about the long-term potential, these companies and stocks showed us that growth can slow down, and stock prices will tumble heavily.

And when asking the question how sustainable such high growth rates could be, we also must address the question if a business has a wide economic moat. For starters, we can look at some metrics to determine if NVIDIA might have a wide economic moat around the business.

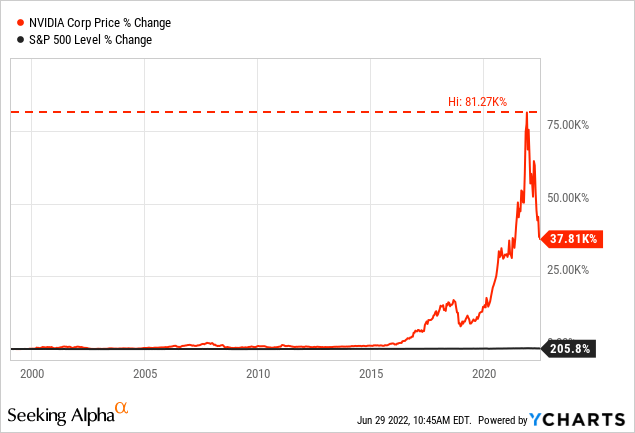

First, an outperformance of the stock over a long timeframe is a good sign for a high-quality business. NVIDIA had its IPO in 1999 and it would be great if we had the data for one or two more decades (especially as the last bull market is now already running for 13 years), but the outperformance of NVIDIA over the S&P 500 (SPY) is impressive. While the S&P 500 gained 205% in value, NVIDIA gained about 38,000% in the same timeframe.

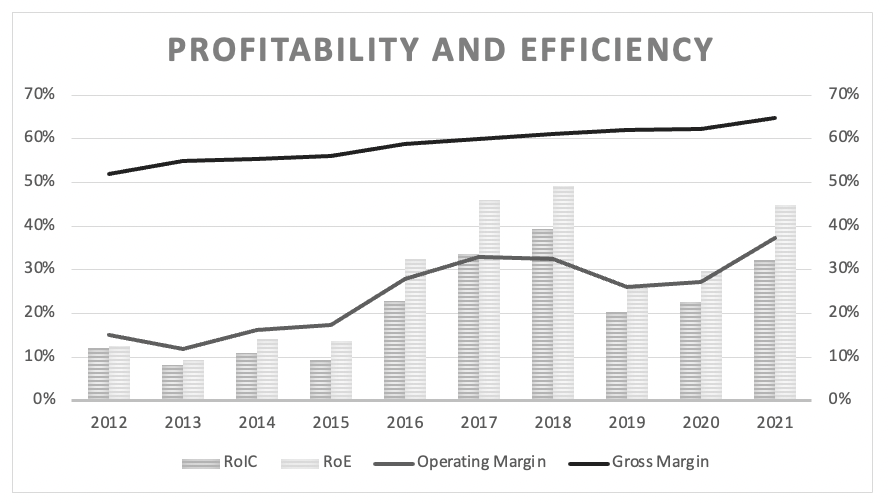

Additionally, we can look at the company’s gross and operating margin. While the operating margin is fluctuating, we can see a clear upward trend, which is a good sign. And especially the gross margin is improving with a stable pace – which is a hint for pricing power.

Author’s work

We can also look at return on invested capital, which was especially high in the last few years and 21.19% on average during the last ten years – another strong hint for a wide economic moat.

When looking at these metrics, it seems like NVIDIA has an economic moat around its business. However, we are basically dealing with a commodity (a product where the price is usually determining if a customer is buying from company A or company B) and it is difficult for such businesses to build a moat around the business. However, there are at least two ways to overcome these obstacles: cost advantages and a strong brand name. And in case of NVIDIA, I would argue that the NVIDIA brand name is a valuable asset (although it is not on the list of the 100 best global brands) and has a great reputation (making customers willing to pay a higher price or choose NVIDIA products).

Nevertheless, we should be prepared for growth slowing down. PayPal and Meta Platforms are also two companies with a strong moat around the business (in my opinion) but growth rates slowed down. And I can imagine a similar scenario for NVIDIA in the coming quarters.

Valuation (Part II)

At this point, we can return to asking the question if NVIDIA is fairly valued right now and if a valuation multiple of 50 can be justified for the business. However, let’s not just use simple valuation metrics like the price-earnings ratio or the price-free cash flow ratio. Instead, we will use a discount cash flow (“DCF”) calculation to determine an intrinsic value for NVIDIA.

When taking the free cash flow of the last four quarters (which was $7,926 million) and assuming a 10% discount rate, NVIDIA must grow 16% annually for the next ten years followed by 6% growth till perpetuity to be fairly valued (of course, these are idealized assumptions). And when looking at the growth rates in the recent past, these growth rates certainly seem achievable. In the last ten years, NVIDIA could grow earnings per share with a CAGR of 32.26%. Nevertheless, 16% growth for 10 years without growth slowing down would probably be the highest assumption I ever used in a discount cash flow calculation for any business (and is also ignoring the potential recession).

Even for high-growth companies I usually assume growth slowing down over the next ten years. And we seriously must ask the question why we should be so optimistic about NVIDIA and assume such high growth rates. And we must consider that other companies could also grow with an extremely high pace in the last ten years – Tencent (OTCPK:TCEHY, OTCPK:TCTZF) grew earnings per share with a CAGR of 35.65%, Amazon (AMZN) grew with a CAGR of 47.06%, Meta Platforms was growing with a CAGR of 41.43% and Alibaba (BABA) was growing even with a CAGR of 73.27%.

Most of these stocks are trading for much lower valuation multiples right now, and for Tencent, we would get an intrinsic value of more than HKD 700 when calculating with the same growth rates as above (16% for the next 10 years, followed by 6% growth till perpetuity). For Meta Platforms, we would get an intrinsic value of more than $700. And while nobody would justify that intrinsic value for Meta Platforms right now as growth rates have declined, what is making us so optimistic that growth for NVIDIA won’t slow down as well?

Stock Price Declining Further

I would be cautious about every stock that is trading for extremely high multiples, as the risk of these multiples suddenly contracting is rather high. And at least for the next few years, I see a rather high risk of the stock price declining further.

I mentioned above that NVIDIA is facing the risk of lower revenue and lower earnings per share due to a potential recession. Additionally, NVIDIA is facing the very high risk of multiples contracting as investors are suddenly not so optimistic about NVIDIA and the growth potential anymore. And when combining these two aspects – EPS declining and multiples contracting – the stock price could decline much steeper. A few months ago, we had to refer to the Dotcom bubble to warn about the risks many pandemic high-flyers are facing. But now we have already countless examples of stocks declining 70%, 80%, or sometimes even 90%, and it should be clear for everybody that stocks with extremely high valuation multiples face a high risk of steep declines.

Conclusion

Of course, there is one major difference between many of the companies mentioned above and NVIDIA – at least until now the company has continued to grow revenue at a high pace (and results of a single quarter are not enough to challenge that narrative). But I see a high risk of NVIDIA’s stock declining further. I will rate NVIDIA with a “Hold” as I don’t see the stock so extremely overvalued that the price can’t be justified in any way. But the valuation is still high, and I certainly see downside risks going forward.

Be the first to comment