JackF

Investment Thesis

Nutrien (NYSE:NTR) is priced at approximately 6x this year’s free cash flow. That’s the headline figure. That being said, going forward, I will not overly emphasize Nutrien’s valuation.

Instead, I’ll lay out the backdrop facing Nutrien’s potash opportunity, which makes up about 50% of Nutrien’s profitability.

Here I’ll describe the bull and bear case that investors should think about when it comes to the fertilizer market.

This is why I’m bullish on Nutrien.

Alas, the Weak Hands

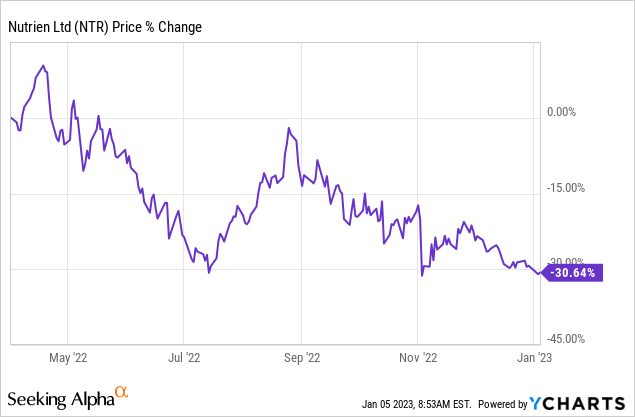

As has been widely reported, 2022 didn’t exactly pan out as many fertilizer investors had expected. There were all the reasons to expect to be rewarded. And yet.

Furthermore, 2023 is up against very tough comparables, particularly when it comes to potash prices in the first half of 2023.

But rather than being despondent about Nutrien’s prospects, this is how I’m thinking about it. There’s really nobody invested in Nutrien today expecting fireworks. Investors that came to the stock on the expectation of fireworks will have left at some point in the fall of 2022.

The investors that remain in the stock are not loose hands, looking to sell. The time to exit the stock has come and gone.

The shareholders that are in the stock, will stick around for a while. The remaining group of shareholders is buying into the potash story.

So, that leads me to discuss the potash story.

2023 and the Most Expensive Commodity in the World

Approximately 50% of Nutrien’s EBITDA is derived from its potash business. What’s more, potash prices have been falling as farmers, in mass, have done everything in their power to stretch out their inventories. This includes diluting their fertilizer or even avoiding laying down fertilizer all together.

But the problem here is that this is not a sustainable way to farm. Consequently, farmers will be forced to replenish their inventories in 2023.

So, this leads me to discuss the world’s most expensive commodity. Investor patience. Investors were highly eager to get rewarded in 2022. Everyone understood the dynamics that were supposed to happen. And therein was the problem.

There was a ubiquitous, singular hypothesis, that potash prices were high. Management knew it. Investors knew it. And farmers knew it.

Nutrien’s management raised their guidance in early 2022. Farmers saw the issue at hand, namely expensive fertilizer, and turned their backs. And this left shareholders disgruntled and in disbelief.

But everything that I described for 2022, is highly likely to take place in 2023. What will be different, in my opinion, is that it won’t be a ubiquitous singular hypothesis, but a slow and steady acceptance that was supposed to take place in 2022 is now taking place in 2023.

Namely, that farmers, on mass, will return to the market to replenish their depleted fertilizer inventories.

Consequently, this leads me to discuss what investors are looking out for in 2023.

Investors Demand One Thing for 2023, Cash Flow

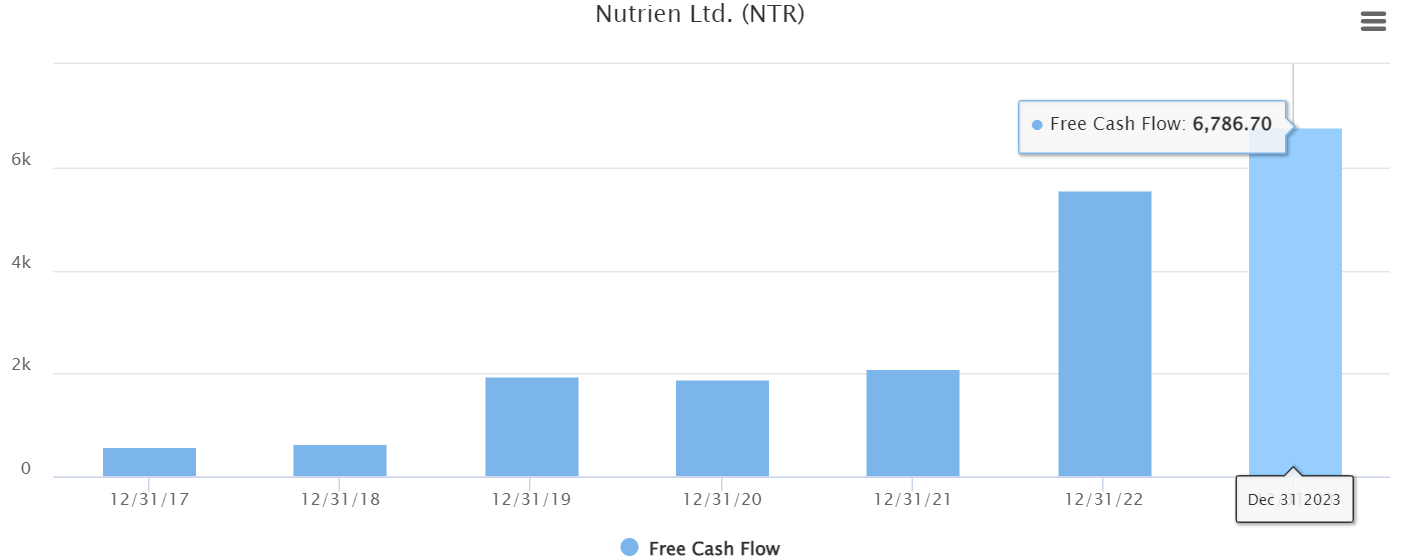

The focus for investors will be on Nutrien’s cash flows and profitability. Nutrien’s 2022 free cash flows are expected to reach approximately CAD$8 billion. For this figure, I assumed that Nutrien’s capex would be approximately CAD$4 billion. And that its EBITDA would end the year at approximately CAD$12 billion.

These figures are a rough estimate, but they work for our purposes.

TIKR.com

Meanwhile, analysts following the company assume that Nutrien’s free cash flow in 2023 will be higher. Note, the table above used USD rather than CAD.

While the ultimate free cash flow figures are not likely to be accurate, what’s important here is the directionality of the free cash flow. Analysts presently assume that in 2023, Nutrien’s free cash flow will be higher than in 2022.

Accordingly, one way or another, Nutrien is priced at approximately 6x this year’s free cash flow.

The Bottom Line

This is the one-line takeaway, Nutrien is a highly profitable fertilizer company that is well-positioned for 2023.

The slightly expanded summary would put forward a question to readers. Do you think that Nutrien has more than 6x years’ worth of strong free cash flows left in this business? Because that’s what the market is saying.

The market is valuing this business at 6x this year’s free cash flow. Essentially saying that forget the dividend payout. Forget any share repurchases. There are about 6x this year’s strong free cash flow left in this business. What do you think?

Be the first to comment