MicroStockHub

Investment Thesis

Nucor (NYSE:NUE) is well-placed to reward investors. Here are three reasons why I think Nucor is going to be a strong investment in the coming 12 months.

- There’s China’s real estate market finding a floor.

- In the medium term, there’s the great energy transition underway.

- Nucor’s valuation is particularly attractive.

This stock is very exciting, so let’s get to it.

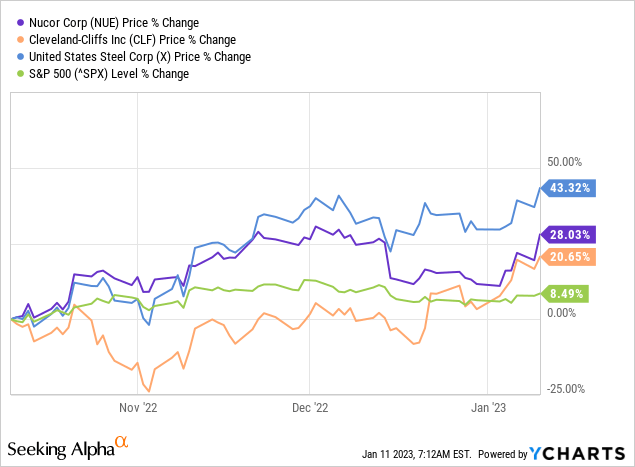

The SP500 Can’t Stand Steel

Before going further, let’s lay out some context.

Steel is trouncing the S&P500. Why?

Three reasons. China, the great energy transition, and valuations. I’ll take these topics in order and provide further details as required.

But before that, allow me to digress. Several investors told me that they don’t want to get involved with capital-heavy industries because they are cyclical. And while I respect their opinion, I believe that they miss the point.

Cyclical companies can make terrific investments. Steel companies have operated with an eye toward profitability. After all, steel companies have been categorically out of favor for a while, and this has been reflected in their valuations. More on this in a moment.

Now the reason why this is a good time to get involved is that there are two strong catalysts for steel companies.

China’s Real Estate Market, the Biggest Steel Consumer

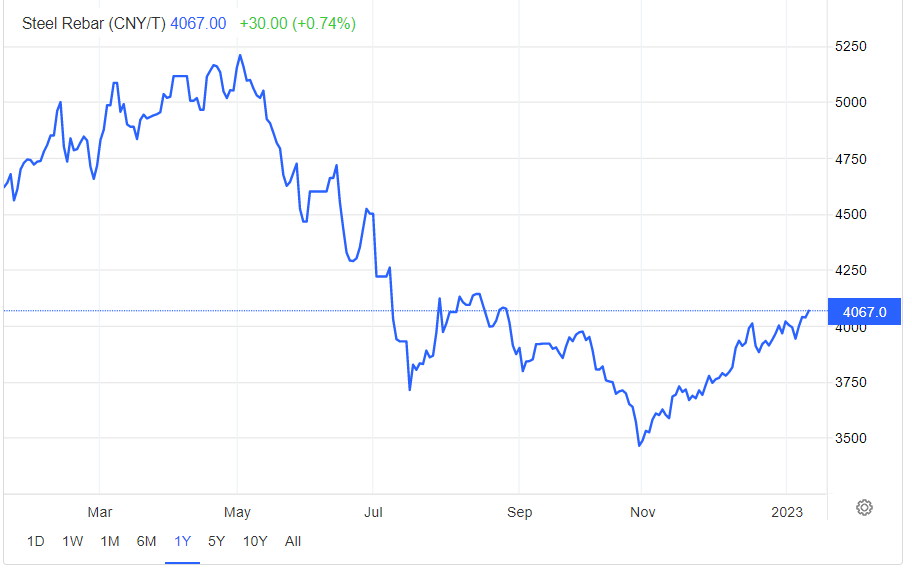

China’s real estate market has found support from the government in the form of ”indirect liquidity”. Put simply, the government has signaled to banks to extend further credit lines to overleveraged real estate developers.

Accordingly, this signals two things. China is creating a real estate bubble that will implode, in time, and cause mayhem.

And yet, for now, this also means that China’s real estate market has found a floor. Which in turn means that the world’s biggest consumer of steel will continue to consume steel. Thus, leading steel prices to rise.

Trading Economics, steel prices

Steel For the Great Energy Transition

Next, we’ll discuss the other catalyst facing Nucor. The great energy transition, particularly, in the US.

NUE investor day

Steel will see a strong increase in demand over the next three to five years. As countries double down on their energy transition, steel demand is going to go up.

Whether that’s from steel used in offshore wind turbines or solar panels, steel will play an important role in all renewables, especially solar and wind.

While every country will have its own preference for its own energy security requirements, countries require steel.

Next, we’ll get down to NUE’s valuation.

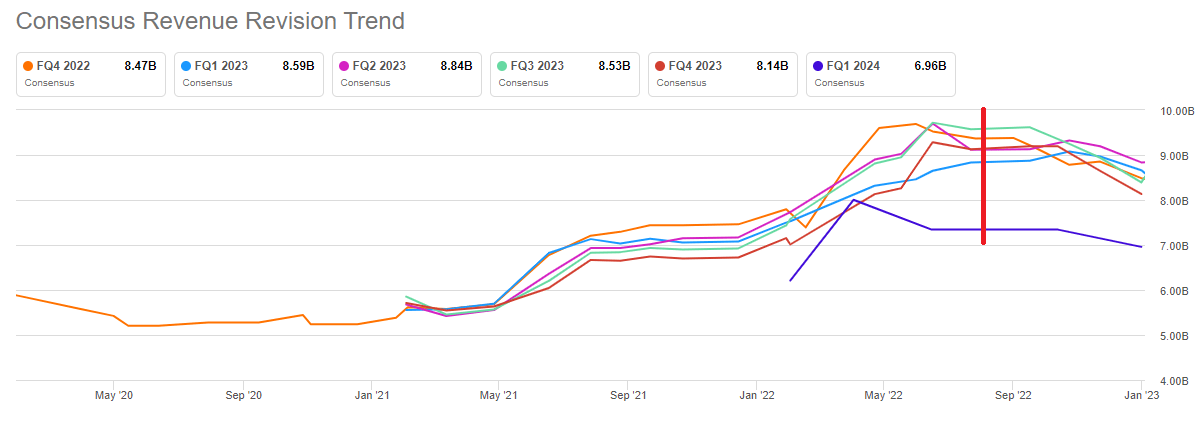

NUE Stock Valuation – 6x Normalized EBITDA

What you see in the graphic that follows is that analysts have been busy downwardly revising their estimates for NUE’s revenue targets for several months.

NUE revenue estimates

But as you know from what I’ve shown you above, is that steel prices in the spot market have bounced off a hard floor.

Consequently, in the coming weeks, analysts will revisit and upwardly revise their financial models and raise NUE’s revenue targets.

And that’s exactly where you want to be invested. You want to be invested in a stock, that’s on the cusp of receiving upgrades.

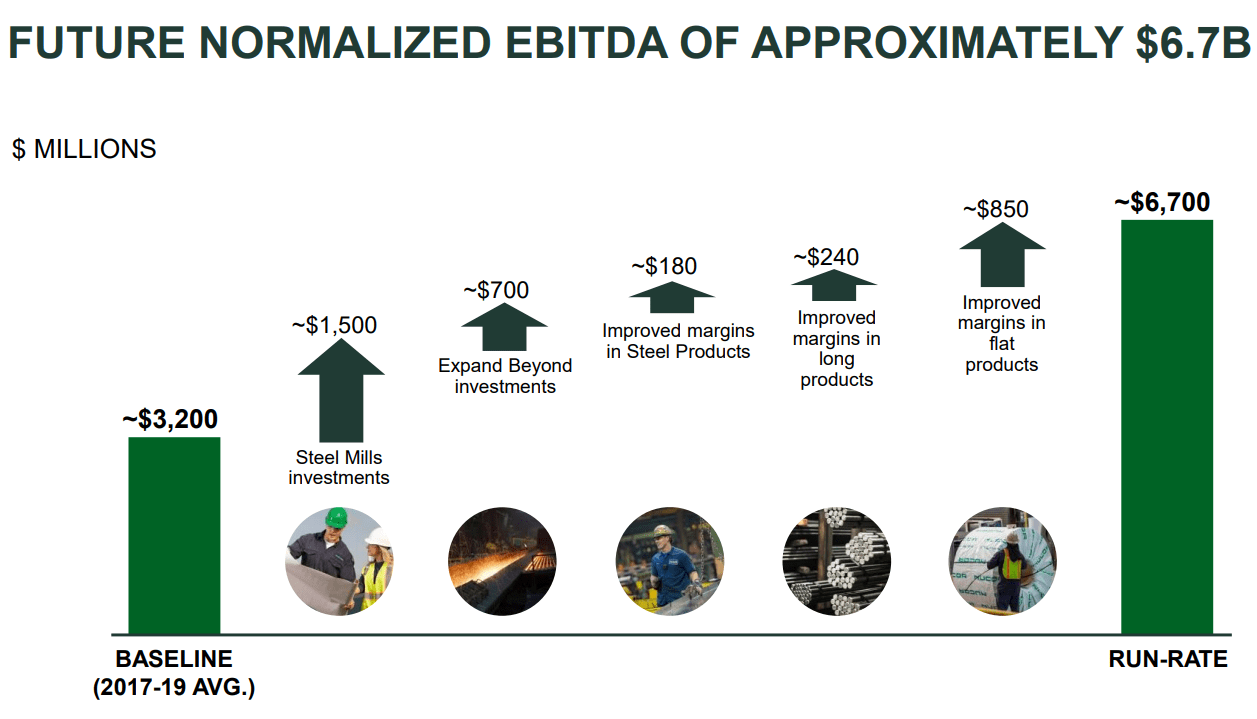

What’s more, as you can see in the graphic that follows, NUE’s 2017-2019 average baseline EBITDA was approximately $3.2 billion.

NUE Investor Day

However, NUE’s December Investor Day points to Nucor having the means to get closer to $6 billion of EBITDA in the not too distant future. That means that compared with its baseline from a few years ago, NUE’s EBITDA will have doubled.

That leaves NUE priced at approximately 6x future EBITDA. That being said, as I stated last month, I believe that for this year, NUE could report around $3 billion of free cash flow. This translates to approximately 11x this year’s free cash flow.

For a company with strong tailwinds to its back, paying 11x depressed free cash flows, in this market, is a very attractive valuation, in my opinion.

The Bottom Line

The are several risks worth noting.

- One overhanging risk is that steel is a commodity. And that production overcapacity can be a serious risk to NUE.

- The other noteworthy risk is that energy prices have been notably strong. That means that steel, which is particularly energy-intensive, could see its margins compress.

- Lastly, but not least important, with energy prices in Europe taking a breather, there are going to be a lot of idled factories eager to resume production. That may cause this tight market to become oversupplied.

All that being said, my message for the past several months has been consistent. Every renewable energy structure requires steel. The demand for steel is going to go up in the coming three years, and Nucor is cheaply valued.

That means that investors considering Nucor right now haven’t missed anything yet. Nucor’s prospects are strong, while its stock is particularly attractive.

Be the first to comment