anatoliy_gleb

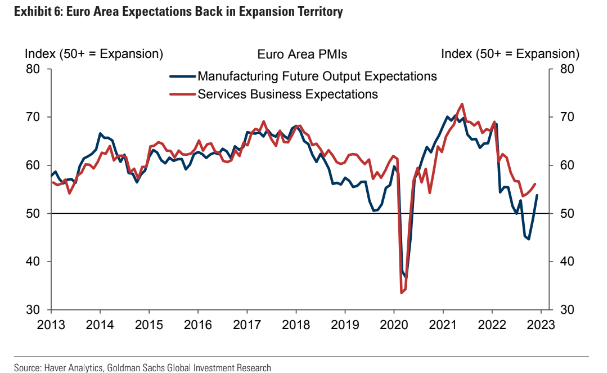

Goldman Sachs (GS) rocked the macro landscape this week by forecasting no recession in Europe. With PMIs back on the mend and a rising Euro currency – indicative of some optimism across the pond – shares of European-based firms have been in rally mode since October.

Global companies, particularly those sensitive to commodity prices, have attracted some bids to their stock prices. But is there more upside to come? Let’s take a look at one Chemicals firm.

European Recession? Not Seeing It, Says Goldman

Goldman Sachs

According to Bank of America Global Research, Huntsman Corporation’s (NYSE:HUN) portfolio of businesses represents a diversified set of chemical products touching an even broader set of end markets. The company reports across four business segments: Polyurethanes, Advanced Materials, Performance Products, and Textile Effects, representing the revenues and profits from the company’s exposure to five primary chemical chains. Across many of these platforms HUN operates a vertically integrated footprint from upstream commodities to downstream derivatives.

The Texas-based $5.9 billion market cap Chemicals industry company within the Materials sector trades at a low 5.8 trailing 12-month GAAP price-to-earnings ratio and pays a 2.8% dividend yield, according to The Wall Street Journal.

With exposure to Europe, the firm was cut to sector perform at Scotiabank in November, but that call might have been right at the wrong time as it appears Europe may indeed sidestep a recession. Moreover, high inflation and soaring energy costs were once a problem for Huntsman, but those could reverse to tailwinds this year. In all, the firm matched analysts’ earnings estimates in early November, and the company is scheduled to report Q4 results in February.

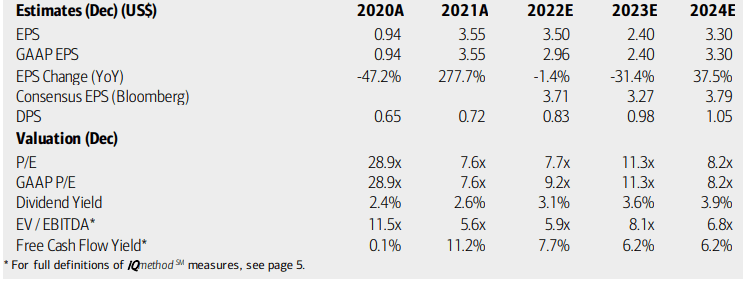

On valuation, analysts at BofA see earnings having fallen modestly in 2022, but per-share profits are seen as dropping hard in 2023 before recovering in 2024. Interestingly, the Bloomberg consensus forecast is much more sanguine compared to BofA’s take. Even with the assumed pessimism from BofA, HUN’s earnings multiples appear low now and in the coming quarters.

Dividends, meanwhile, are expected to rise significantly through 2024. With a current EV/EBITDA ratio about half that of the S&P 500 and considering Huntsman’s solid free cash flow, the stock looks like a decent value. So, I generally concur with Seeking Alpha’s B rating.

Huntsman: Earnings, Valuation, Dividend Forecasts

BofA Global Research

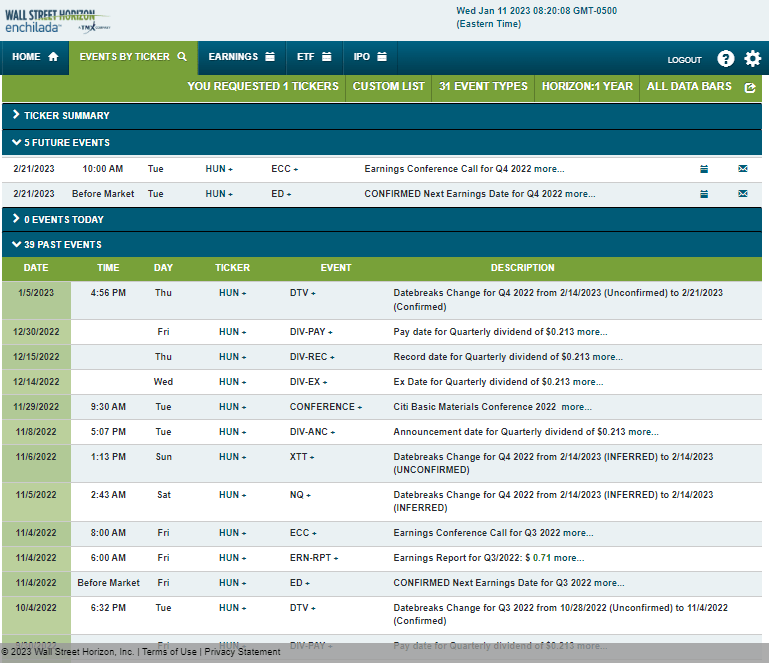

Looking ahead, corporate event data from Wall Street Horizon show a confirmed Q4 2022 earnings date of Tuesday, February 21 before market open with a conference call later that morning. You can listen live here. The calendar is light on volatility catalysts aside from next month’s reporting date.

Corporate Event Calendar

Wall Street Horizon

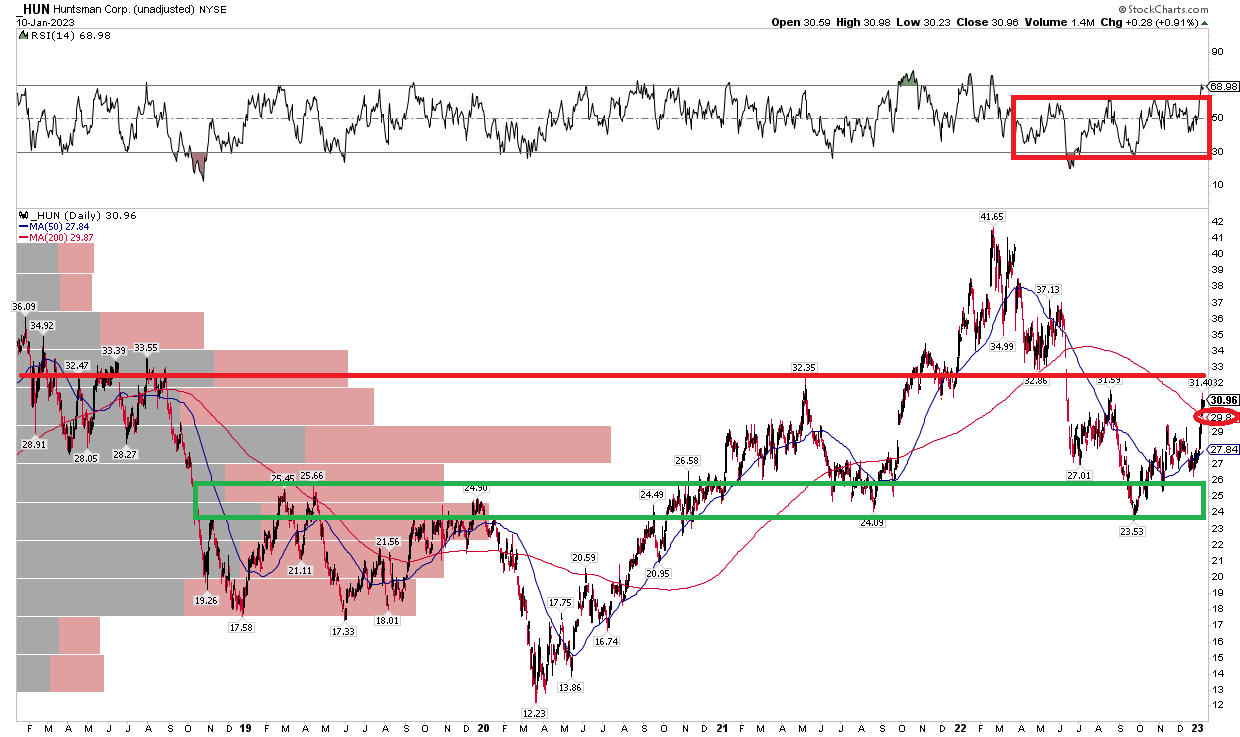

The Technical Take

If we took a very long-term view of HUN, we would see a generally uptrending chart with higher lows and higher highs. The recent all-time peak above $41 did not last long, though, as shares plunged to $23 and change in October around the market lows. That barely undercut the Q3 2021 low of $24.09 – which is common in trading action – thus stops should often have some cushion below a key support point to avoid false breakdowns.

Notice in the chart below that the stock could see some selling at the first-half 2021 high near $32 here. But the bulls managed to take HUN above the falling 200-day moving average which was confirmed by a new high in RSI momentum. The chart arguably completed a bearish head and shoulder top this year with the decline to $23, so I would bias to the long side from the chart, but it’s not a screaming technical buy.

HUN: Shares Hold Support, Momentum Favors the Bulls

Stockcharts.com

The Bottom Line

With a good valuation and decent chart, I’d be long shares here but would like to see HUN rise above $33 on volume to help confirm a possible move to the 2022 highs.

Be the first to comment