klenger/iStock via Getty Images

Introduction

In a June update, I argued the attractive dividend yield offered by Northwest Bancshares (NASDAQ:NWBI) did not necessarily make the stock attractive. As interest rates (and margins) are on the rise these days, NWBI should benefit as well so I wanted to have another look at this small regional bank focusing on Pennsylvania and some counties in New York, Indianapolis and Ohio. NWBI currently has just under 127 million shares outstanding, resulting in a market capitalization of approximately $1.78B.

The net interest income should continue to increase

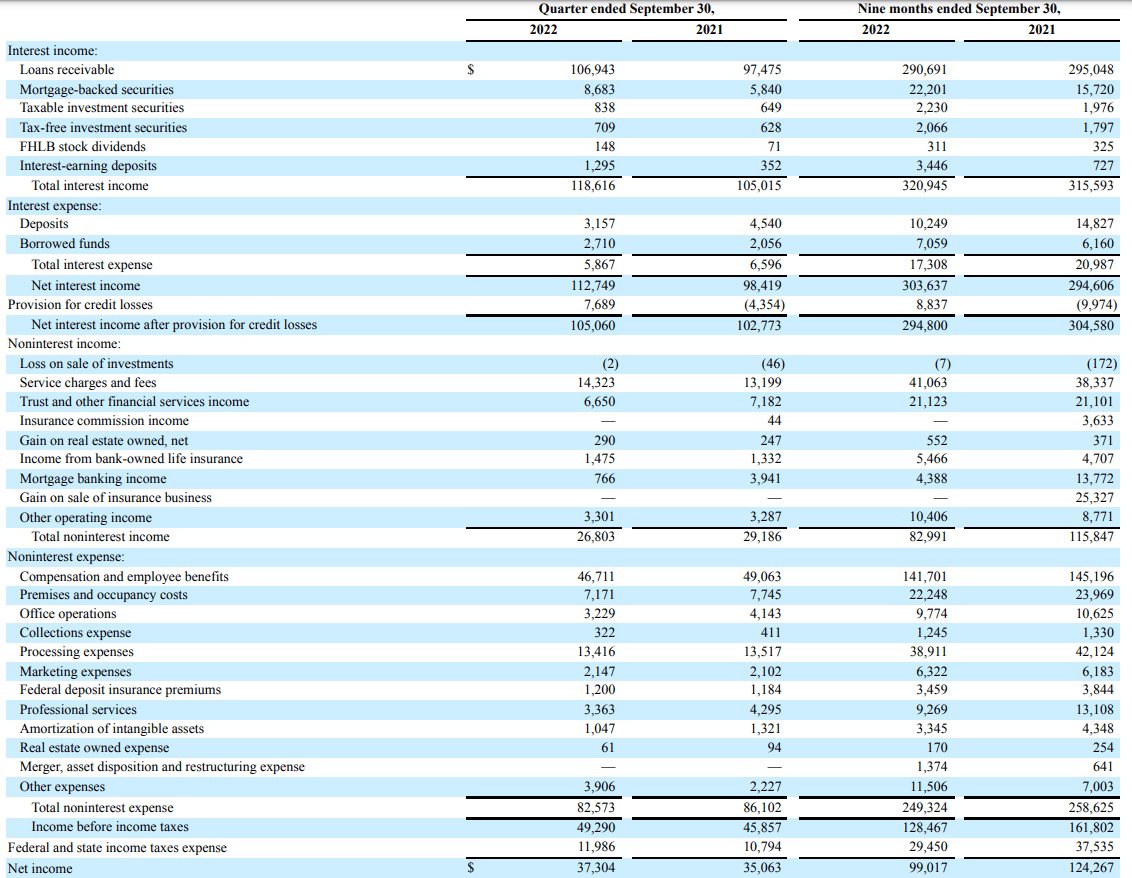

During the third quarter, Northwest saw its interest income increase again while the interest expenses remained pretty stable (and even decreased compared to the third quarter of last year). This caused the net interest income to increase by approximately 15% on a YoY basis.

NWBI Investor Relations

The total non-interest income was $27M while the total non-interest expenses came in at $82.6M for the quarter, resulting in a net non-interest expense of $56M. The pre-tax and pre loan loss provision income was approximately $57M and after recording a $7.7M loan loss provision and making the almost $12M tax payment, the net income was $37.3M for an EPS of $0.29.

This pushed the 9M 2022 EPS to $0.78 and this does highlight the Q3 performance as the EPS in the entire first half of the year was just $0.49 while 85% of the 9M 2022 loan loss provisions were recorded in the third quarter.

Northwest Bancshares currently pays a quarterly dividend of 20 cents per share, and while the rather high payout ratio of approximately 90% was a reason for concern in my previous article, the increased net interest income has strongly improved the dividend coverage ratio as the bank only paid out about 70% of its Q3 EPS. I will be looking for confirmation in the next few quarters but so far, so good.

The book value further deteriorated – but I expect stabilization soon

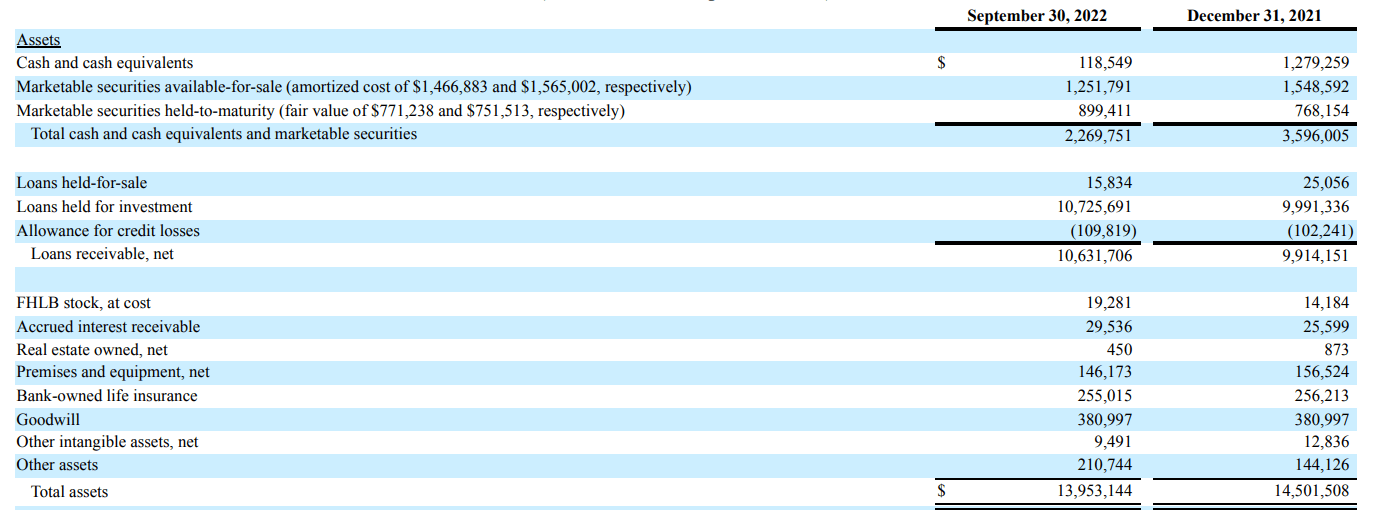

I initially liked Northwest’s relatively conservative balance sheet. The focus clearly was on liquid assets but that also meant the bank had a substantial position in securities available for sale. Those securities have to be marked to market and due to the increasing interest rates on the financial markets, the value of those securities went down.

NWBI Investor Relations

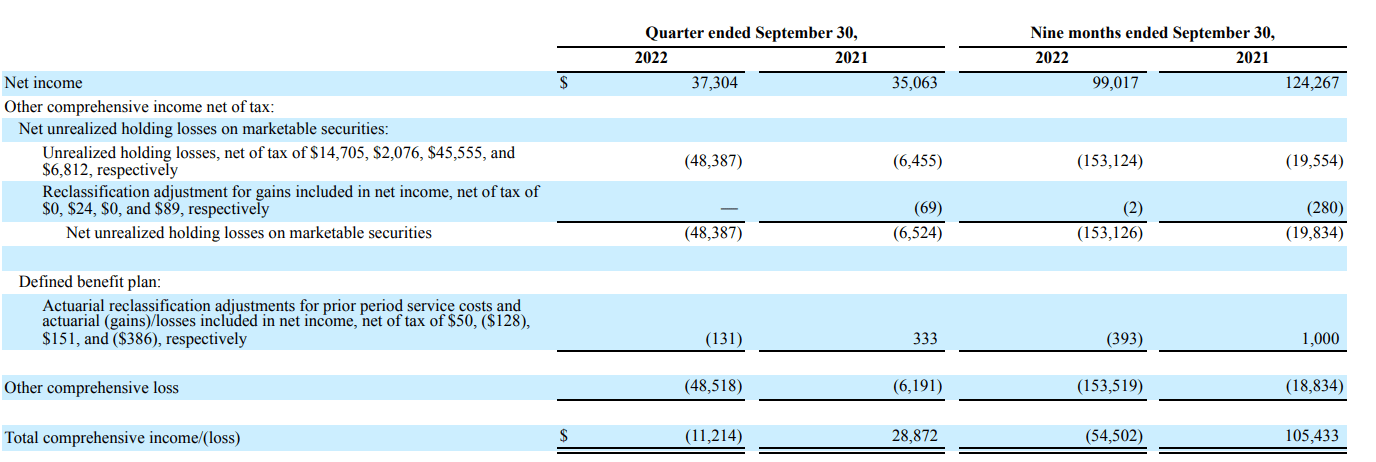

The losses are marked in the comprehensive income statement, and the overview below shows the unrealized losses on the securities AFS portfolio came in at just under $50M for the quarter.

NWBI Investor Relations

Looking at the liabilities and equity side of the balance sheet, we see the total amount of equity has indeed decreased to $1.46B. That’s about $142M lower than the situation as of the end of last year, despite generating a net income of $99M in the first nine months of this year. This is obviously related to the securities available for sale (with a negative $154M revaluation) partially offset by retained earnings (reported net income minus the dividends that were paid out in the first nine months of this year).

As it looks like bond yield are stabilizing, I expect the majority of the bad news to have been incurred by now and I don’t anticipate the book value decreases to be more moderate in the near term future where after the retained earnings will allow NWBI to slowly increase the book value again.

As of the end of September, NWBI’s book value was approximately $11.49/share. The tangible book value (the equity value minus the goodwill and other intangible assets) was approximately $8.42.

Investment thesis

Investors could consider buying Northwest Bancshares for its dividend yield of approximately 5.7% and perhaps we can expect a small dividend increase in the near future considering the dividend hasn’t been hiked yet since Q2 2021.

The stock is currently trading at approximately 1.65 times its tangible book value and at about 11 times the forward earnings for 2023. I will keep an eye on the evolution of the bank’s tangible book value over the next few quarters, but at this moment, I’m not willing to pay a 70% premium to TBV. The attractive dividend yield appears to be the main reason to consider Northwest Bancshares at this point, but I remain on the sidelines.

Be the first to comment