risamay

Earnings of LCNB Corp. (NASDAQ:LCNB) will most probably continue to increase next year, partly on the back of subdued loan growth. Further, the ongoing up-rate cycle will slightly lift the net interest margin, which will further support earnings. Overall, I’m expecting LCNB Corp. to report earnings of $1.85 per share for 2022, up 11%, and $1.97 per share for 2023, up 7% year-over-year. Compared to my last report on the company, I have favorably tweaked almost all income statement line items. Next year’s target price suggests a high upside from the current market price. Therefore, I’m maintaining a buy rating on LCNB Corp.

Loan Growth to Remain Near the Current Level

LCNB Corp.’s loan growth remained lackluster in the third quarter after a disappointing first half of the year. The portfolio grew by only 0.5% in the first nine months of the year, or 0.7% annualized. Fortunately, the growth in loan commitments has been better, which bodes well for loan growth in the near term. According to details given in the 10-Q filing, unused lines of credit were 51% higher at the end of September 2022 compared to the end of December 2021.

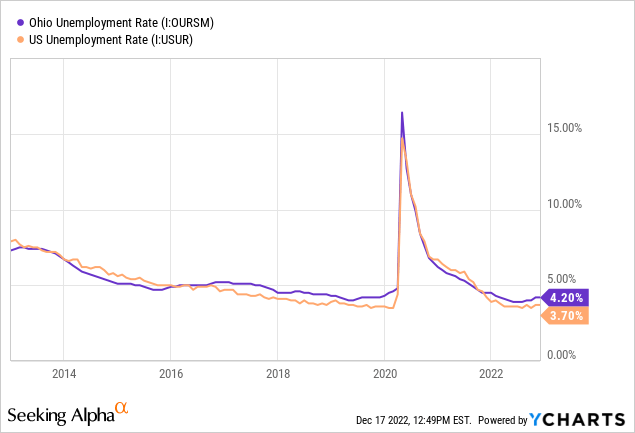

I’m expecting loan growth to remain near the third quarter’s level in future quarters because of a mixed economic outlook. Firstly, the job market is likely to act as a tailwind for loan growth. LCNB serves communities in Southwest and South-Central Ohio; therefore, the local economy is key for loan growth. Ohio’s unemployment rate is currently higher than the national average, but it’s doing quite well in a historical context, as shown below.

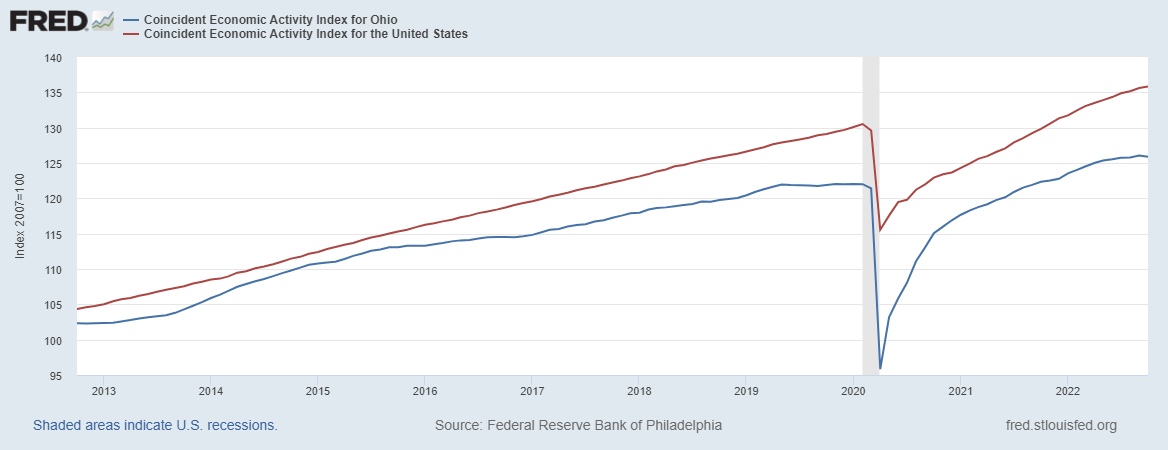

On the other hand, high-interest rates are the biggest headwind for loan growth. Further, the economic activity in the state of Ohio has started to flatten, which looks worse when compared to the national average.

The Federal Reserve Bank of Philadelphia

Considering these conflicting factors, I’m expecting the loan portfolio to grow by 0.75% in the last quarter of 2022, taking full-year loan growth to 1.3%. For 2023, I’m expecting the portfolio to grow by 3.0%. Meanwhile, I’m expecting other balance sheet items to grow somewhat in line with loans. The following table shows my balance sheet estimates.

| Financial Position | FY18 | FY19 | FY20 | FY21 | FY22E | FY23E |

| Net Loans | 1,195 | 1,239 | 1,294 | 1,364 | 1,381 | 1,423 |

| Growth of Net Loans | 41.3% | 3.8% | 4.4% | 5.4% | 1.3% | 3.0% |

| Other Earning Assets | 274 | 214 | 253 | 337 | 331 | 341 |

| Deposits | 1,301 | 1,348 | 1,455 | 1,629 | 1,670 | 1,720 |

| Borrowings and Sub-Debt | 103 | 46 | 28 | 16 | 35 | 36 |

| Common equity | 219 | 228 | 241 | 239 | 198 | 211 |

| Book Value Per Share ($) | 18.3 | 17.4 | 18.6 | 19.3 | 17.6 | 18.7 |

| Tangible BVPS ($) | 13.0 | 12.6 | 13.8 | 14.3 | 12.2 | 13.3 |

| Source: SEC Filings, Author’s Estimates(In USD million unless otherwise specified) | ||||||

Slight Margin Expansion to Also Help the Earnings

LCNB Corp.’s net interest margin was almost unchanged in the third quarter following the 19 basis points rise in the second quarter of this year. We can expect similarly low changes in future quarters because the loan and deposit mixes have not changed much over the last two quarters.

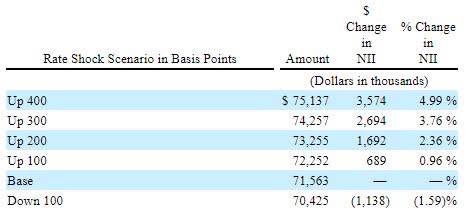

LCNB’s deposit beta (rate sensitivity) is quite high because of the large balance of NOW, money market, and savings accounts, which altogether made up 59% of total deposits at the end of September 2022. These deposits will reprice soon after every rate hike. As a result, the net interest margin is only slightly positively correlated to interest rate changes. The results of the management’s interest rate sensitivity analysis given in the 10-Q filing showed that a 200-basis points hike in interest rates could boost the net interest income by only 2.36% over twelve months.

3Q 2022 10-Q Filing

Following the 425 basis points hike in 2022, I’m expecting the Federal Reserve to increase the fed funds rate by 50 basis points in 2023. Considering these factors, I’m expecting the margin to grow by five basis points in the last quarter of 2022 and another five basis points in 2023.

Expecting Earnings to Grow by 7% Next Year

The subdued loan growth and slight margin expansion will drive earnings through the end of 2023. Meanwhile, I’m expecting the provisioning for loan losses to remain at a normal level. LCNB unexpectedly posted net provision reversals during the third quarter of this year. Following the significant reserve release, allowances were more than thirteen times as high as the nonperforming loans. In my opinion, this coverage is more than enough to compensate for the threats of a recession. As a result, I’m expecting the net provision expense to make up 0.04% of total loans in 2023, which is the same as the average from 2017 to 2019.

Overall, I’m expecting LCNB to report earnings of $1.85 per share for 2022, up 11% year-over-year. For 2023, I’m expecting earnings to grow by 7% to $1.97 per share. The following table shows my income statement estimates.

| Income Statement | FY18 | FY19 | FY20 | FY21 | FY22E | FY23E |

| Net interest income | 48 | 54 | 56 | 57 | 61 | 65 |

| Provision for loan losses | 1 | 0 | 2 | (0) | 0 | 1 |

| Non-interest income | 11 | 12 | 16 | 16 | 14 | 15 |

| Non-interest expense | 41 | 44 | 46 | 48 | 49 | 51 |

| Net income – Common Sh. | 15 | 19 | 20 | 21 | 21 | 22 |

| EPS – Diluted ($) | 1.24 | 1.44 | 1.55 | 1.66 | 1.85 | 1.97 |

| Source: SEC Filings, Earnings Releases, Author’s Estimates(In USD million unless otherwise specified) | ||||||

In my last report on LCNB Corp., I estimated earnings of $1.77 per share for 2022 and $1.84 per share for 2023. I have slightly increased my earnings estimates as I have tweaked all income statement line items following the third quarter’s results. I have not made any large, significant changes in any line item.

My estimates are based on certain macroeconomic assumptions that may not come to pass. Therefore, actual earnings can differ materially from my estimates.

High Total Expected Return Justifies a Buy Rating

LCNB has been increasing its dividend in the last quarter of the year since 2018. Given the earnings outlook, it’s likely that the company will maintain the dividend trend next year. Therefore, I’m expecting the company to increase its dividend by $0.01 per share to $0.22 per share in the fourth quarter of 2023. The earnings and dividend estimates suggest a payout ratio of 43% for 2023, which is close to the five-year average of 49%. Based on my dividend estimate, LCNB is offering a forward dividend yield of 4.9%.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value LCNB Corp. The stock has traded at an average P/TB ratio of 1.28 in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| T. Book Value per Share ($) | 13.0 | 12.6 | 13.8 | 14.3 | ||

| Average Market Price ($) | 18.7 | 17.4 | 14.8 | 17.5 | ||

| Historical P/TB | 1.44x | 1.38x | 1.07x | 1.22x | 1.28x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $13.3 gives a target price of $17.0 for the end of 2023. This price target implies a 2.1% downside from the December 16 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.08x | 1.18x | 1.28x | 1.38x | 1.48x |

| TBVPS – Dec 2023 ($) | 13.3 | 13.3 | 13.3 | 13.3 | 13.3 |

| Target Price ($) | 14.3 | 15.7 | 17.0 | 18.3 | 19.6 |

| Market Price ($) | 17.3 | 17.3 | 17.3 | 17.3 | 17.3 |

| Upside/(Downside) | (17.4)% | (9.7)% | (2.1)% | 5.6% | 13.2% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 11.8x in the past, as shown below.

| FY18 | FY19 | FY20 | FY21 | Average | ||

| Earnings per Share ($) | 1.24 | 1.44 | 1.55 | 1.66 | ||

| Average Market Price ($) | 18.7 | 17.4 | 14.8 | 17.5 | ||

| Historical P/E | 15.0x | 12.0x | 9.5x | 10.5x | 11.8x | |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $1.97 gives a target price of $23.2 for the end of 2023. This price target implies a 33.6% upside from the December 16 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 9.8x | 10.8x | 11.8x | 12.8x | 13.8x |

| EPS 2023 ($) | 1.97 | 1.97 | 1.97 | 1.97 | 1.97 |

| Target Price ($) | 19.2 | 21.2 | 23.2 | 25.1 | 27.1 |

| Market Price ($) | 17.3 | 17.3 | 17.3 | 17.3 | 17.3 |

| Upside/(Downside) | 11.0% | 22.3% | 33.6% | 45.0% | 56.3% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $20.1, which implies a 15.8% upside from the current market price. Adding the forward dividend yield gives a total expected return of 20.7%. Hence, I’m maintaining a buy rating on LCNB Corp.

Be the first to comment