enot-poloskun/iStock via Getty Images

As the world’s leader in industrial enzymes, Novozymes (OTCPK:NVZMF)(OTCPK:NVZMY) is a very interesting company worth following. It is based in Denmark, and its enzymes affect the characteristics and performance of several classes of end products, including household care products, food, and beverages. Its enzymes and microbes also have applications in bio-energy, agriculture and feed, and even pharmaceutical products.

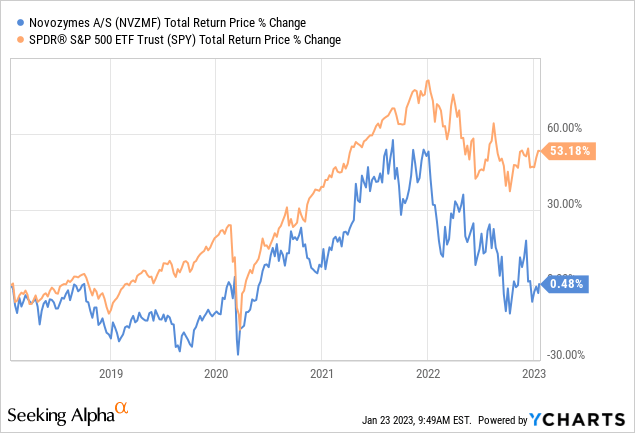

It is a wonderful business operating in an attractive industry, and with a strong competitive moat. As a result investors tend to overpay for the shares, and that is the main reason why we believe that despite decent operational performance, the shares have returned very little over the past five years. Investors were paying high multiples five years ago. Today the valuation looks a little bit more reasonable, but we would still not call the shares undervalued. Still, we believe this is a company worth having on the watch-list to potentially buy on a dip.

Company Overview

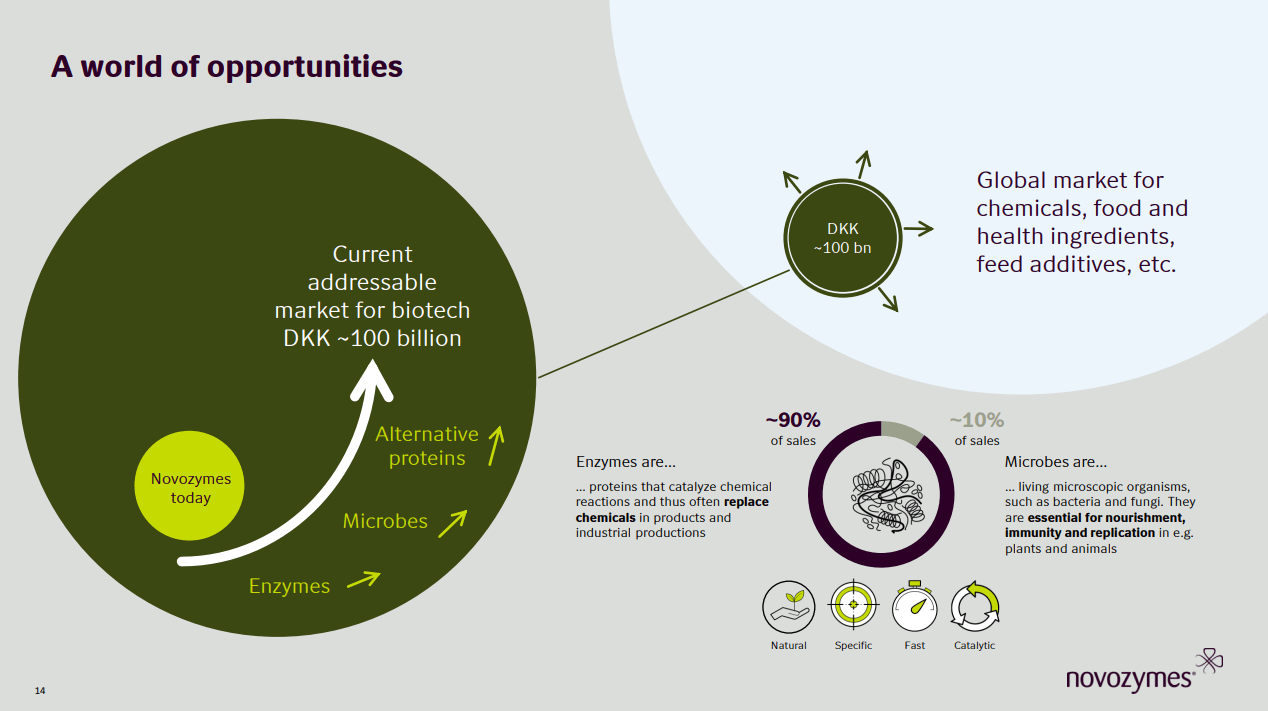

Most of Novozymes’ revenue, around 90%, comes from the sale of enzymes. The other ~10% comes from microbes, including bacteria and fungi.

Novozymes Investor Presentation

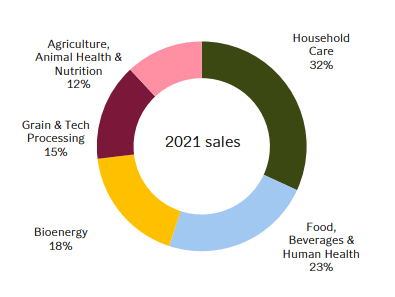

To give an idea of the types of applications the company’s products have, they help reduce the environmental impact of synthetic fertilizers by offering biological alternatives. They produce ingredients used in renewable and biodegradable detergent, and apply enzymes and microbial science to improve plastic recyclability. They also offer solutions that reduce the need for sugar and salt, improve the taste and the texture of protein and eliminate additives in food. Similarly, they have products that help enable ethanol production. As can be seen, Novozymes has a clear role to play in the transition to a greener economy. The company is well diversified, addressing several different markets, with Household Care being their main segment.

Novozymes Investor Presentation

9 Months Results

Novozymes delivered strong results for the first nine months of fiscal year 2022, with organic sales growth of 9%. The company also reported a decent EBIT margin of 27.2%, despite facing higher raw material, energy, and logistics costs. Pricing is expected to be positive for the full year 2022 and even more so for 2023.

Novozymes introduced 13 new products in the first nine months of the year, including innovations for the companion animal segment in China, the laundry softener market, and products to extend the lifetime of textiles.

Merger with Chr. Hansen Holding

The company announced in December that it is going to merge with Chr. Hansen Holding (OTCPK:CHYHY). Chr. Hansen focuses more on enzymes and microbes for the food sector, while Novozymes’ largest segment is household products. We’ve covered Chr. Hansen in another article, and it is another company we consider to be very high quality with a strong competitive moat, but that usually trades at very high multiples too. The merger is expected to be completed by the fourth quarter of 2023. The combined company is expected to have an annual revenue of ~€3.5 billion and generate annual revenue synergies of more than €200 million.

Competitive Advantages

Novozymes is a company with a very strong competitive moat, which is the result of several factors. It was unique technology and more than 6,500 patents, and spends significant resources on R&D and innovations. It re-invests ~13% of sales into R&D projects and productivity improvement. Another reason for the strong moat is that there is a high customer switching cost, as Novozymes has a big impact on end products quality and characteristics, so customers will be reluctant to switch suppliers. What’s more, Novozymes’ ingredients only represent a small percentage of the end products total cost, making it even less likely that customers will switch to another supplier for slightly lower prices and compromise the quality of their products.

Financials

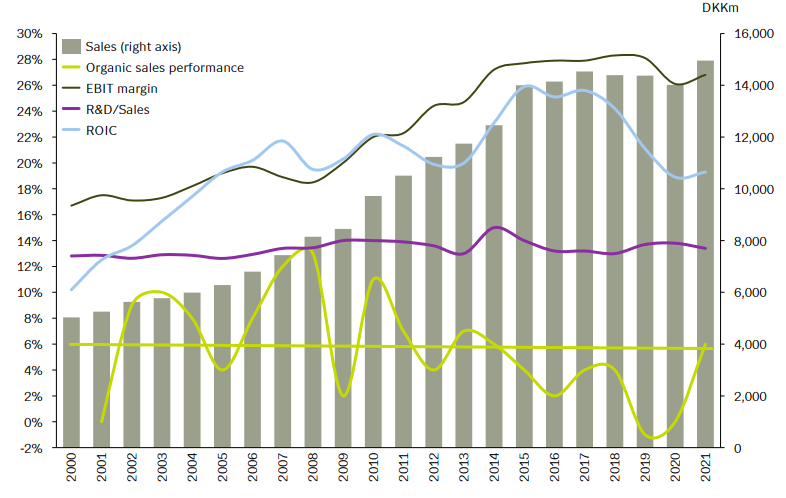

The company’s financials reflect the competitive moat, as profit margins and returns on invested capital are excellent. Organic sales growth used to be good too but disappointed the last few years. It has been improving lately, but it is too early to be confident that the sales growth recovery will continue for a few more years.

Novozymes Investor Presentation

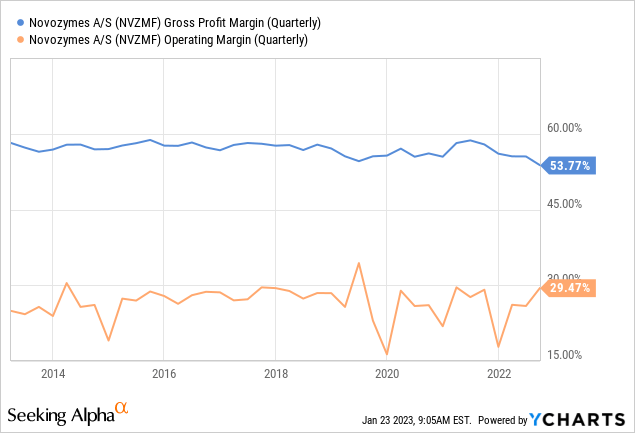

In any case, there are few companies with the operating margin that Novozymes has of ~29%. The company has been consistently profitable even during some very tough years, such as 2020.

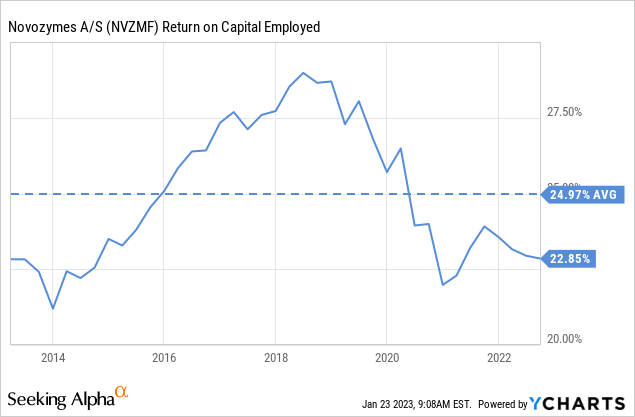

The company also has an enviable return on capital employed, another sign that it has strong competitive advantages that allow it to earn superior returns.

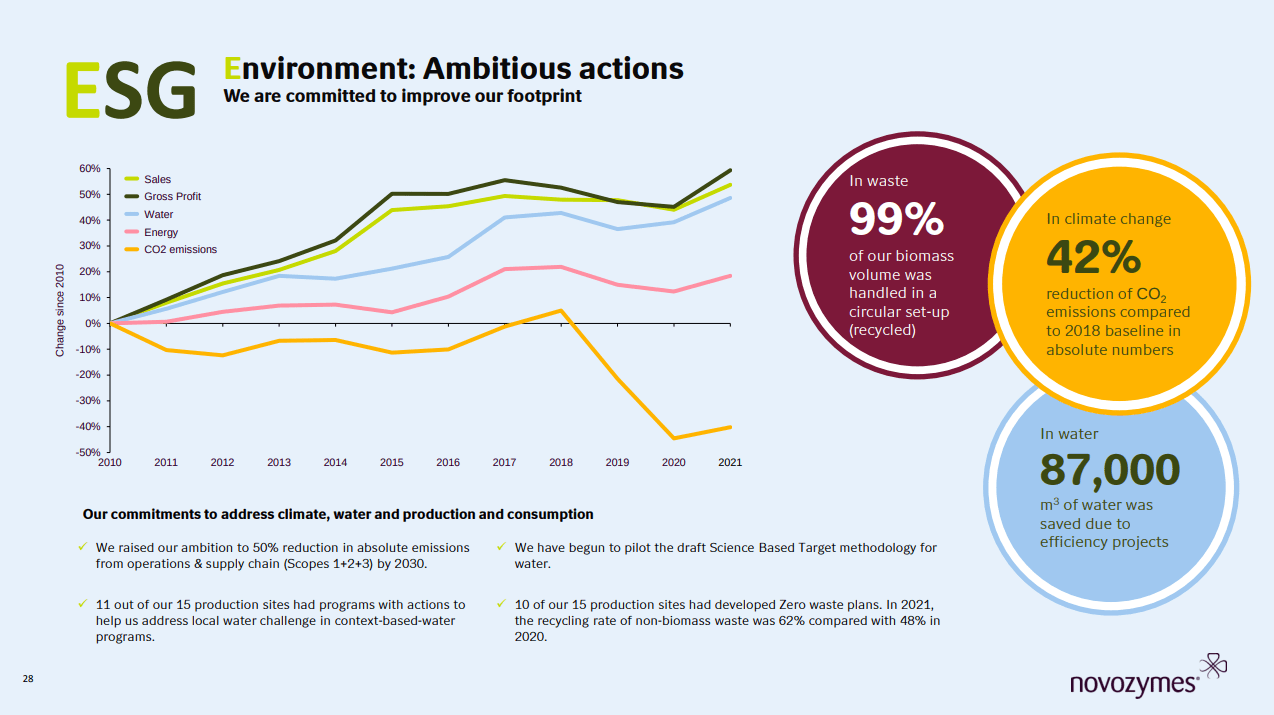

ESG

The company is considered one of the most sustainable corporations in the world, ranking in the prestigious Corporate Knights in position #23 out of the top 100 in the world. Its merger partner Chr. Hansen Holding is found in position #18.

Novozymes Investor Presentation

Valuation

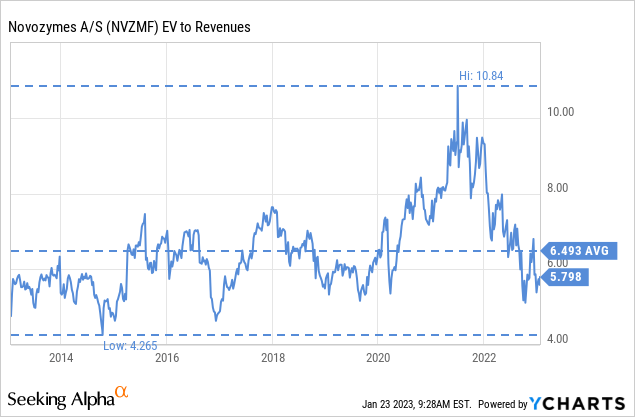

If we have one problem with Novozymes is its valuation. Shares are almost always expensive, trading at very high valuation multiples. At least right now they are trading below their ten year average EV/Revenues multiple.

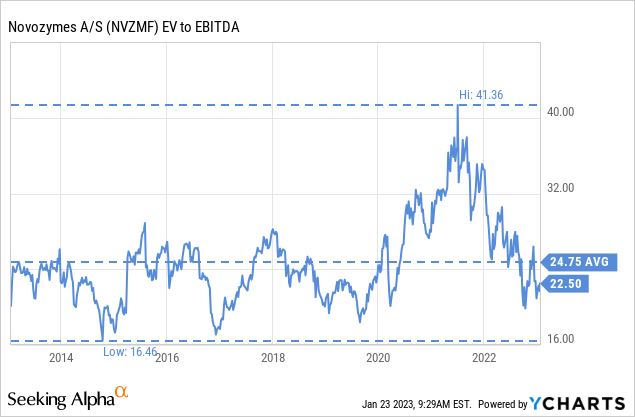

The EV/EBITDA is also below the ten year average of ~24.75x, currently at ~22.5x. Still, this is a very high multiple, even for a high-quality business.

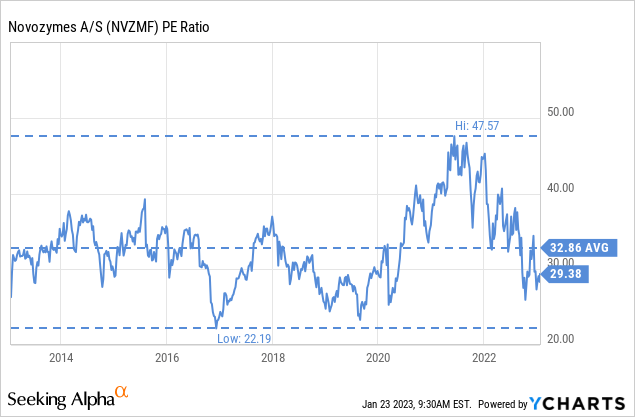

The price/earnings ratio is also currently below the ten year average of ~32.8x, currently at ~29x. This is a multiple more appropriate for a growth company in our opinion, but it is understandable that investors are willing to pay a premium for quality and stability. Given the quality of the business, we find the p/e ratio almost reasonable.

Based on relatively optimistic earnings estimates we calculate the net present value of its future earnings stream at ~$38 per share. With shares currently trading at ~$51 we believe they are overvalued by ~34%. We used, however, a relatively high discount rate of 10%. Another way to see it is that shares are probably valued right now to deliver mid to high single digit returns for long-term investors.

| EPS | Discounted @ 10% | |

| FY 23E | 1.84 | 1.67 |

| FY 24E | 2.13 | 1.52 |

| FY 25E | 2.32 | 1.38 |

| FY 26E | 2.53 | 1.45 |

| FY 27E | 2.76 | 1.44 |

| FY 28E | 3.01 | 1.43 |

| FY 29E | 3.28 | 1.42 |

| FY 30E | 3.57 | 1.40 |

| FY 31E | 3.89 | 1.39 |

| FY 32E | 4.24 | 1.38 |

| FY 33E | 4.63 | 1.36 |

| Terminal Value @ 3% terminal growth | 69.68 | 22.20 |

| NPV | $38.05 |

Risks

There are two important risks to consider with Novozymes. One is the integration risk with Chr. Hansen Holding, and whether the company will deliver on the promised synergies that are necessary for the acquisition to be accretive to earnings per share. The second important risk we see is that the valuation is high, so it is likely shares will perform very poorly if sales growth disappoints.

Conclusion

Novozymes is a wonderful business with strong competitive advantages, operating in an attractive industry, and with excellent profit margins and returns on employed capital. The company rarely trades at an attractive valuation, but it currently is approaching what we would describe as an almost reasonable valuation. In any case, it is a very interesting company that is worth following, and maybe buying if there is a dip in price. We are rating shares a ‘Hold’ and will keep it on the watch list for the time being.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment