adventtr

Northern Dynasty Minerals (NYSE:NAK) has entered into an agreement that potentially gives it up to US$60 million over the next two years in exchange for a portion of the gold and silver production from the Pebble Project. Northern Dynasty has already received US$12 million and the investor has the option to put in additional US$12 million increments.

I previously thought that Northern Dynasty would end up issuing a significant number of shares to continue funding its operations. Raising US$60 million via equity offerings would have added around 200 million shares at its current share price, which would have resulted in a 38% increase to its current share count.

This royalty agreement (if the full US$60 million is invested) gives Northern Dynasty funding for a bit over four years of operations. At base case prices, the royalty agreement (with US$60 million in investments would result in only a modest 3% reduction to Pebble’s NPV7 (from the 2021 PEA).

Thus, the royalty agreement appears to be beneficial to Northern Dynasty. I still remain quite skeptical about Pebble’s chances of ever becoming an operational mine, but this deal at least reduces the need for Northern Dynasty to issue shares while it tries to find a way forward for Pebble.

Royalty Agreement

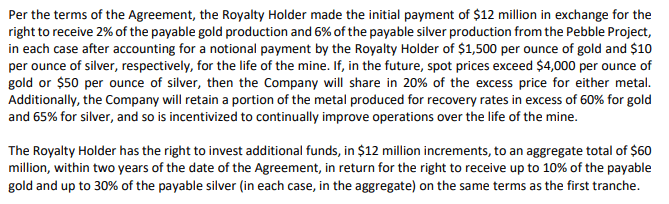

The royalty holder has so far paid US$12 million for the right to receive 2% of the payable gold production and 6% of the payable silver production over the life of the Pebble mine. The royalty holder will pay US$1,500 per ounce of gold and US$10 per ounce of silver.

The agreement could result in the royalty holder paying as much as US$60 million to receive 10% of the payable gold production and 30% of the payable silver production. Gold is the second biggest revenue source for Pebble (after copper), while silver is a relatively minor revenue source that accounts for around 2% of total revenues.

Royalty Agreement Northern Dynasty Minerals

Effect On Pebble Economics

The following calculations look at what the royalty holder is receiving for an initial investment of US$12 million.

The estimated NPV7 of the gold and silver production due to the royalty holder at base case prices of US$1,600 gold and US$22 silver (along with a 20-year mine life) is approximately US$15 million. This also assumes that Pebble starts construction in the near-term. A five-year delay in construction start (to 2027) would reduce the estimated NPV7 to approximately US$11 million.

At base case prices and a 20-year mine life, the royalty holder isn’t getting a great return even if Pebble goes ahead. From Northern Dynasty’s perspective, it is selling a share of Pebble production at around 0.8x NPV7 (based on base case prices and a 20-year mine life), so the deal makes good sense from its perspective.

The royalty holder is taking a bet that Pebble will eventually become a producing mine, and that gold and silver prices will be much higher if/when Pebble starts producing. The royalty holder would also benefit in the scenario that Pebble becomes a producing mine with a mine life longer than 20 years (since the agreement involves production over the life of the mine).

At prevailing prices of US$1,800 gold and US$24 silver along with a 20-year mine life, the NPV7 of the gold and silver production due to the royalty holder increases to US$29 million (with a near-term construction start) or US$20 million (with a 2027 construction start).

At US$3,000 gold and US$40 silver instead (also with a 20-year mine life), the NPV7 of the gold and silver production due to the royalty holder increases to US$111 million (with a near-term construction start) or US$79 million (with a 2027 construction start). The undiscounted value of the cash flows due to the royalty holder in this scenario is estimated at US$273 million. This would be roughly 23x the initial investment. Thus, the royalty holder is essentially taking a long-shot bet that could result in a substantial payoff if things (commodity prices, mine approval) work out in their favor.

Cash Position

Northern Dynasty was down to approximately US$10 million in cash and cash equivalents at the end of Q2 2022, while its burn rate is approximately US$14 million per year. The initial US$12 million from the royalty agreement gives Northern Dynasty enough cash to last until early 2024 before its cash balance dwindles to nothing. If the royalty holder invests the full US$60 million, Northern Dynasty would have enough cash to last until mid-2027 at its current burn rate.

Conclusion

The royalty agreement doesn’t address Northern Dynasty’s main challenge, which is trying to fight an EPA veto as well as considerable federal and local opposition. However, the royalty agreement does help reduce Northern Dynasty’s risk of dilution while it continues to advocate for Pebble.

Northern Dynasty is only taking a 3% hit to Pebble’s NPV7 (based on base case pricing and the 2021 PEA) if it receives the full US$60 million investment, which is a much better result that the 38% additional shares it would need to issue to raise that much from an equity offering.

While the royalty agreement is a positive for Northern Dynasty, I still remain bearish on its stock due to the immense challenges it faces to get Pebble into operation.

Be the first to comment