courtneyk/E+ via Getty Images

Investment Thesis

New Relic (NYSE:NEWR) put out its fiscal Q3 2023 earnings that took investors by surprise.

There’s some good news and some pesky elements that we should consider.

Overall, I’m quite bullish on this company’s prospects, even at my estimated 45x forward fiscal 2024 EPS figures.

Before we go forward, note that New Relic’s fiscal year and calendar are misaligned. I’ll only refer to its fiscal year.

What’s Happening Right Now?

There’s no doubt that the present environment is highly uncertain for companies of all shapes and sizes.

NEWR Q3 2022

However, this didn’t prevent New Relic from adding 1,100 new active customers in the past year. So, it could be said that its freemium business model appears to be working. At least on the surface.

However, this doesn’t detract from the fact that over the past 5 years, its shares haven’t gone anywhere. At least not meaningfully.

Personally, I lay the blame on its business model and how New Relic has a ”usage-based” revenue stream.

This type of business model puts New Relic on the opposite side of the table from its customers.

This business model quite literally says to the customer, the more ”use” you find from our observability functionality, the more you’ll pay for this use. Realistically, on this front, I believe that Cloudflare’s (NET) business model and value proposition are superior.

For their part, New Relic’s CEO Bill Staples addressed this as one of New Relic’s strengths,

New Relic’s success in growing new paying customers is a result of our unique product-led growth motion, which starts with a perpetual free tier that allows customers to use the product and fall in love with it at their own pace and then pay with a credit card as they begin to scale usage.

Let me put it this way, the verdict is still out on the virtues of this way of charging customers. However, to be clear, there’s ample good news in these earnings results.

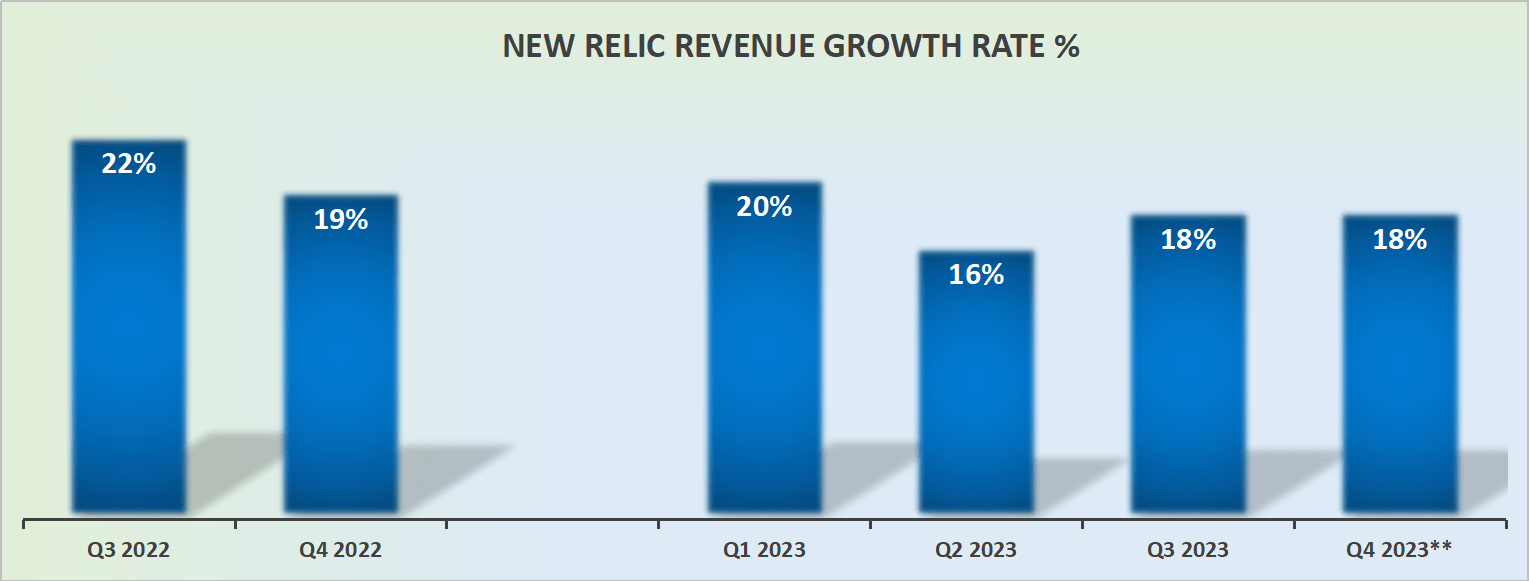

Revenue Growth Rates Reaccelerate

NEWR revenue growth rates

New Relic’s guidance for fiscal Q4 2023 is expected to come in at somewhere close to +18% y/y CAGR. For investors, this guidance implies that New Relic’s full-year revenues will end up coming in stronger than investors previously expected back in fiscal Q2 2023.

Given that analysts had already pretty much written up New Relic’s fate as a mid-teens CAGR company, this reacceleration in revenues towards the high teens’ CAGR unexpectedly changes the tone of the conversation around the company’s prospects.

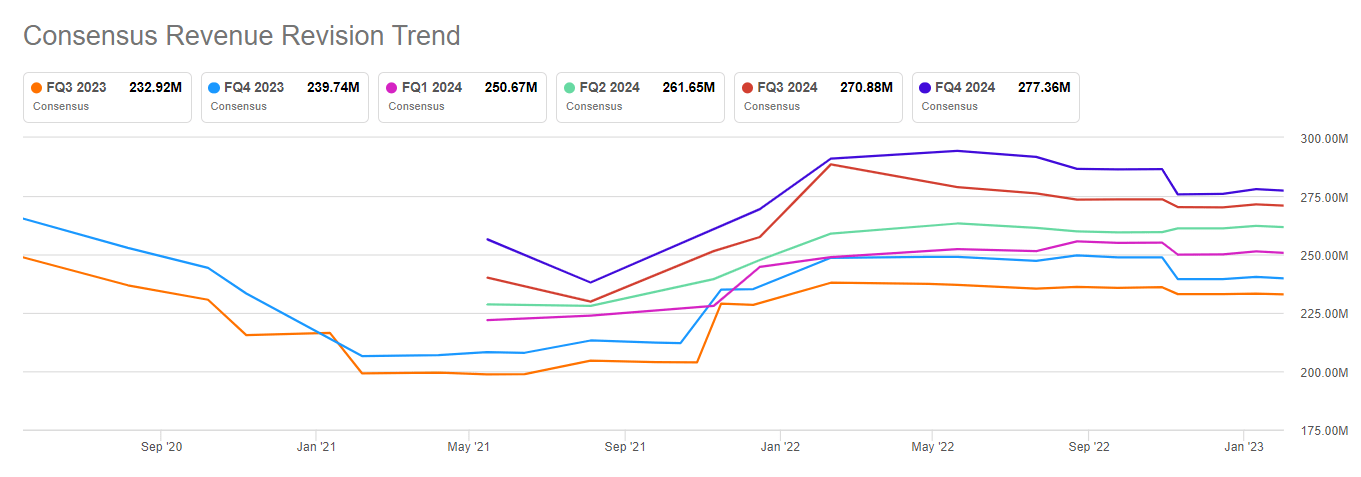

SA premium

The thing with tech companies is that the market struggles to price in those companies that are not growing particularly fast.

The ”middle ground” between hyper-growth and single-digit growth is ”no man’s land” for tech investors, as it’s difficult for investors to figure out the lasting terminal growth rate of the company and how far away from the present time that could be.

On the other hand, where New Relic has excelled right now is in making strong profitability, which we’ll now discuss.

Earnings Turn Positive

Both GAAP and non-GAAP operating margins increased by 13 percentage points. That’s truly something. This saw New Relic’s non-GAAP adjusted EPS go from negative $0.18 last year to positive $0.32 this time around.

Needless to say that any time a company goes from reporting negative EPS figures to positive EPS figures, investors take notice. That point of inflection is something that investors find attractive.

But what’s really quite impressive with New Relic is the magnitude of the swing in profitability.

On the other hand, one minor blemish to keep in mind is that New Relic’s negative working capital continues to drag back New Relic’s full free cash flow potential.

That being said, over the trailing twelve months New Relic’s free cash flow reached positive $9 million, an increase of $47 million from the prior year.

In sum, even though New Relic is clearly seeing its free cash flows moving in the right direction, there’s still more work to be done.

NEWR Stock Valuation — Approximately 45x Forward EPS

It’s difficult to make the assertion that New Relic stock is particularly cheap. Presently the stock is priced at my estimated 45x forward EPS (once we adjust for its fiscal year).

Hence, on the surface, a business that’s growing at just under 20% CAGR shouldn’t really ”undervalued” at more than 45x forward EPS.

That being said, given the tremendous progress in profitability that New Relic has put in this quarter, I’m inclined to give this company the benefit of the doubt.

Key Takeaway

- Sentiment for New Relic is depressed.

- The company clearly has some hair on it.

- But this quarter was nothing short of impressive.

Be the first to comment