Hulton Archive/Hulton Archive via Getty Images

This article was coproduced with Mark Roussin.

The human spirit can be amazingly resilient, taking hit after hit after hit…

Yet refusing to give up in the long run.

History wouldn’t be what it is otherwise.

Take Wilbur and Orville Wright, the brothers who pioneered so much of our understanding of airplanes. To quote Scientific American:

“A journalist told [Orville 31 years after his famous flight] that he and his brother embodied the American dream. They were two humble boys with ‘no money, no influence, and no other special advantages’ who had risen to the heights of fame and fortune.”

Orville said this wasn’t quite true, pointing to how his parents encouraged their children to think and explore and dream. But the rest of it is accurate.

If anything, it downplays the situation they were in, perhaps especially for Wilbur. History.com describes how:

“In the winter of 1885-86, an accident changed the course of Wilbur’s life. He was badly injured in an ice hockey game when another player’s stick hit him in the face.

“Though most of his injuries healed, the incident plunged Wilbur into a depression. He did not receive his high school diploma, canceled plans for college, and retreated to his family’s home. Wilbur spent much of this period at home, reading books in his family’s library and caring for his ailing mother, who died in 1889 of tuberculosis.”

Yet he overcame all of that to become one of the world’s greatest inventors.

Trials and Errors Galore

When we think of the world’s greatest inventors, we usually know somewhere in the back of our minds that most of them didn’t succeed right away.

They had their obstacles. They had their setbacks. They had their detractors.

But those details all read so quickly on the pages of an informative article or even a biographical book. So, let’s see if I can make the Wright brothers’ journey a little more real, as summed up from Wright-Brothers.org:

- Winter and spring 1899 – The Wright brothers begin envisioning a viable aircraft but can’t come up with an idea they can get behind despite numerous attempts.

- June 1899 – Wilbur gets inspiration from an empty box, of all things.

- July 1899 – The brothers design a successful biplane kite with a six-foot wingspan and control lines.

- Spring and summer 1900 – They build their first glider.

- September 1900 – They travel to Kitty Hawk, North Carolina, after spending months researching the best place to try out their glider.

- October 1900 – The wind smashes their glider to pieces. Later on in the month, they send a 10-year-old up on the rebuilt aircraft, flying it like a kite. Ultimately, they can’t get the lift they’re looking for, though.

- Early 1901 – The brothers plan building another glider with a much larger wingspan and schedule another trip to Kitty Hawk.

- July 1901 – The base they set up on the island is plagued by mosquitoes, and their second set of attempts aren’t any more successful than the first.

- August 1901 – Discouraged to the point of quitting, Wilbur and Orville leave North Carolina.

Yet they didn’t quit. Later that year, they built their own wind tunnel to continue their experiments. They revised their thinking.

And they tried again.

Build. Crash. Repeat Until You Succeed.

This led to more crashes in 1902 – but also greater understandings of what to do and not do. And there were even more advancements and setbacks in 1903.

Yet it wasn’t until that December – eight days before Christmas and almost five full years since their first detailed discussions – that Orville made “the first powered flight in a fully controllable aircraft capable of sustaining itself in the air.”

Five years equals 60 months… 1,825 days… 43,800 hours… and plenty of time to give up. And then you add in the next several years of disappointing reception.

Returning to that History.com article:

“The Wright brothers soon found that their success was not appreciated by all. Many in the press, as well as fellow flight experts, were reluctant to believe the brothers’ claims at all. As a result, Wilbur set out for Europe in 1908, where he hoped he would have more success convincing the public and selling airplanes.”

Which equated to even more time to quit. Yet they persevered again.

That’s the kind of spirit – coupled with intelligence and humility (i.e., a willingness to acknowledge errors and correct them) – I like to encourage in investors. It’s a long-term focus that gets the job done, even while everyone else is saying it can’t or shouldn’t be done.

I’m hardly comparing the Wright brothers’ advancements with personal portfolio gains, mind you. But I am saying their ability to see past seeming setbacks is something worth modeling.

If you emulate them in that, you’ll be in a better position to spot the learning opportunities as they come.

And the buying opportunities too.

Underappreciated REIT #1 – Simon Property Group

When it comes to real estate investment trusts (“REITs”), it’s important to understand the quality of their assets, their management teams, and the primary sector(s) in which they operate. In which case, Simon Property Group, Inc. (SPG) checks off all those boxes.

The lead mall landlord on the market today, it’s worked hard to achieve the status it has. The company has been through numerous economic downturns and always seems to bounce back stronger.

That’s in large part thanks to CEO David Simon, one of the best leaders around.

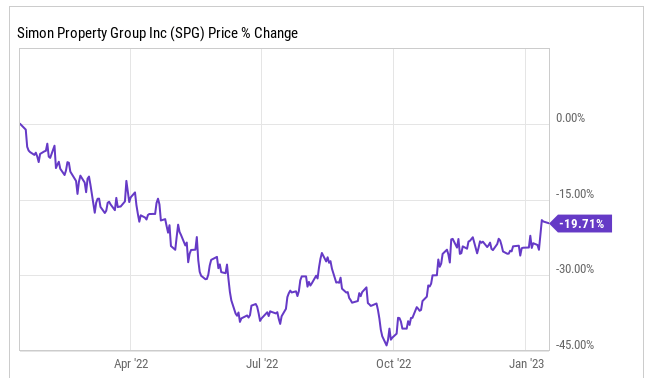

Shares are down roughly 20% over the last 12 months. But things were MUCH worse last summer and fall, when shares were down as much as 45%.

yCharts

Bear markets can be a rough time for shareholders. But long-term investors know they can provide amazing opportunities in some of the best businesses around.

I’m confident this time around will prove the same.

Malls have been under siege for a while now for some very good reasons. The U.S. has too many of them, plain and simple. And so malls were already closing left and right in the years leading up to the pandemic.

That’s naturally put pressure on Simon.

Yet the thing the market keeps missing is that SPG isn’t just a regular mall landlord. It’s the premiere mall landlord.

So it was seeing strong sales per square foot regardless and growing net operating income (NOI) in the process.

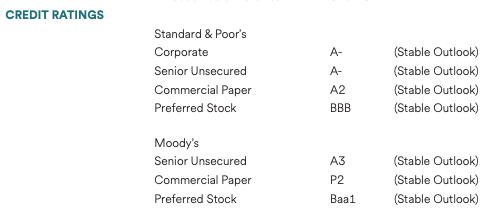

It also knows how to balance a sheet. SPG is very high quality in terms of credit, sporting an A- credit rating that should not be underestimated – especially when going through a rough economic period like we are today.

SPG Q3 Investor Presentation

As of September 30, 2022, Simon owned or had an interest in 230 properties comprising 184 million square feet in North America, Asia, and Europe. The company also has an 80% interest in The Taubman Realty Group, which owns 24 regional, super-regional, and outlet malls in the U.S. and Asia.

SPG also has a 22.4% ownership interest in Klépierre SA (OTCPK:KLPEF), a publicly traded, Paris-based real estate company. That entity owns shopping centers in 14 European countries. So, it should be clear to see that Simon is well-diversified both here in North America and internationally.

But what about the e-commerce threat?

That’s been the bear thesis around Simon Property Group for many years. And to be fair, it’s true that e-commerce continues to grow with no signs of fading away.

That’s not an automatic death sentence for physical stores though. Consumers still enjoy visiting shops in person, and malls are a great social environment as well.

SPG currently pays an annual dividend of $7.20 per share, which equates to a dividend yield of 5.7%. It’s well covered with a payout ratio of just 60%, meaning there’s plenty of room for the REIT to increase the dividend, something it’s been doing aggressively the past few quarters.

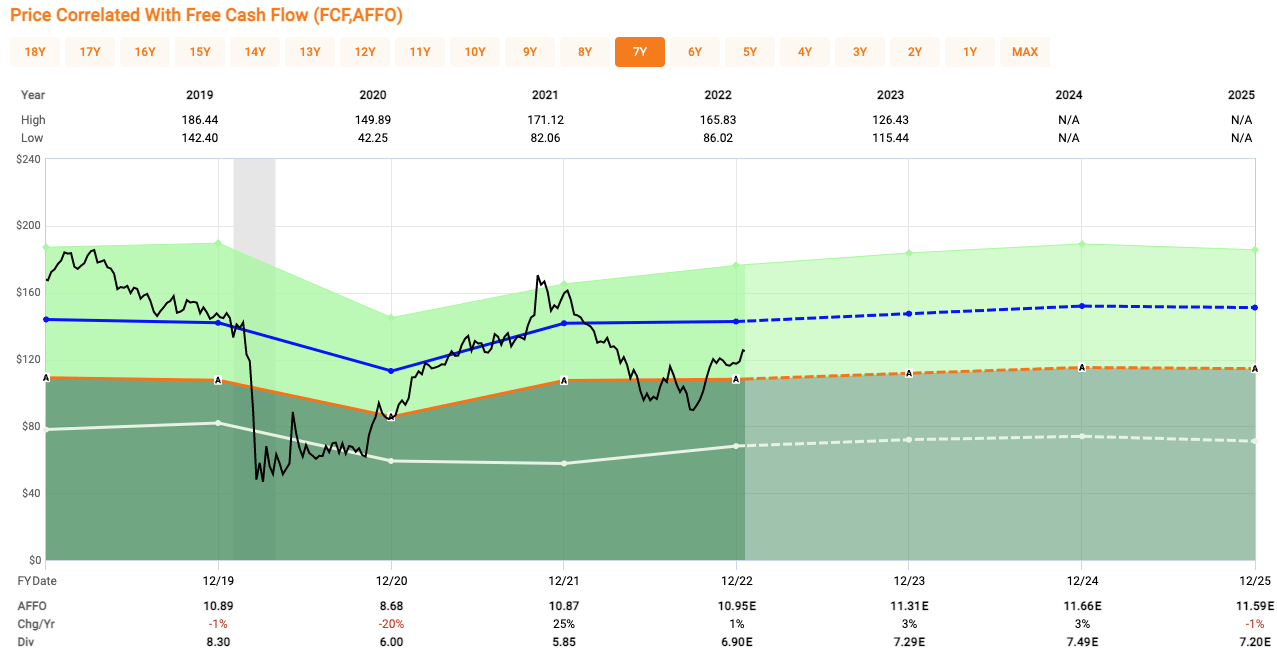

With the stock down roughly 20%, investors can add shares of SPG at a forward adjusted funds from operations (AFFO) multiple of 11x, which is below its five-year average of 13x.

FAST Graphs

At iREIT on Alpha, we rate shares of SPG a Buy.

Underappreciated REIT #2 – Federal Realty Trust

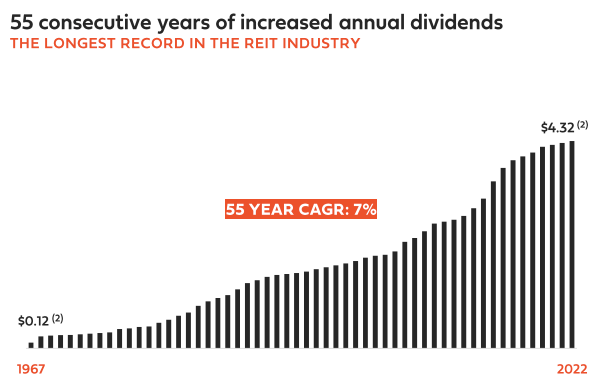

Another underappreciated REIT is Federal Realty Investment Trust (FRT) – the only REIT on the prestigious dividend king list, which is comprised of companies that have raised their annual dividends for 50 consecutive years or more.

Federal Realty has done so for 55 consecutive years. And counting.

FRT Q3 Investor Presentation

Over the past 12 months, shares of FRT are down 16%. But like we saw with SPG, shares of FRT have recovered in a strong way since being down roughly 35% in October.

yCharts

Given its dividend king status, it goes without saying that the company has been through all sorts of markets. Federal Realty has endured rate hikes and cuts, recessions and economic crises, bull and bear markets. Yet the company is as resilient as ever.

Federal Realty is a diversified REIT with retail and shopping center properties making up roughly 75% of its annual base rent. The remainder comes from its office and residential properties.

FRT Q3 Investor Presentation

Now, I will remind you that FRT lost its A- credit rating after it increased its debt load during the early parts of the pandemic. But S&P Global expects its credit metrics and debt situation to continue to improve through this year:

“We expect credit metrics will continue to improve organically over the next several quarters upon accretion of EBITDA [earnings before interest, taxes, depreciation, and amortization] from redevelopments, acquisitions, and stronger operating performance. As a result, we estimate debt to EBITDA will improve to the low-to-mid-6x area by 2022 and around [the] 6x area by 2023.”

Shares of FRT currently pay an annual dividend of $4.32 per share, which equates to a dividend yield of 4.0%. The dividend is well covered by a payout ratio of 69%.

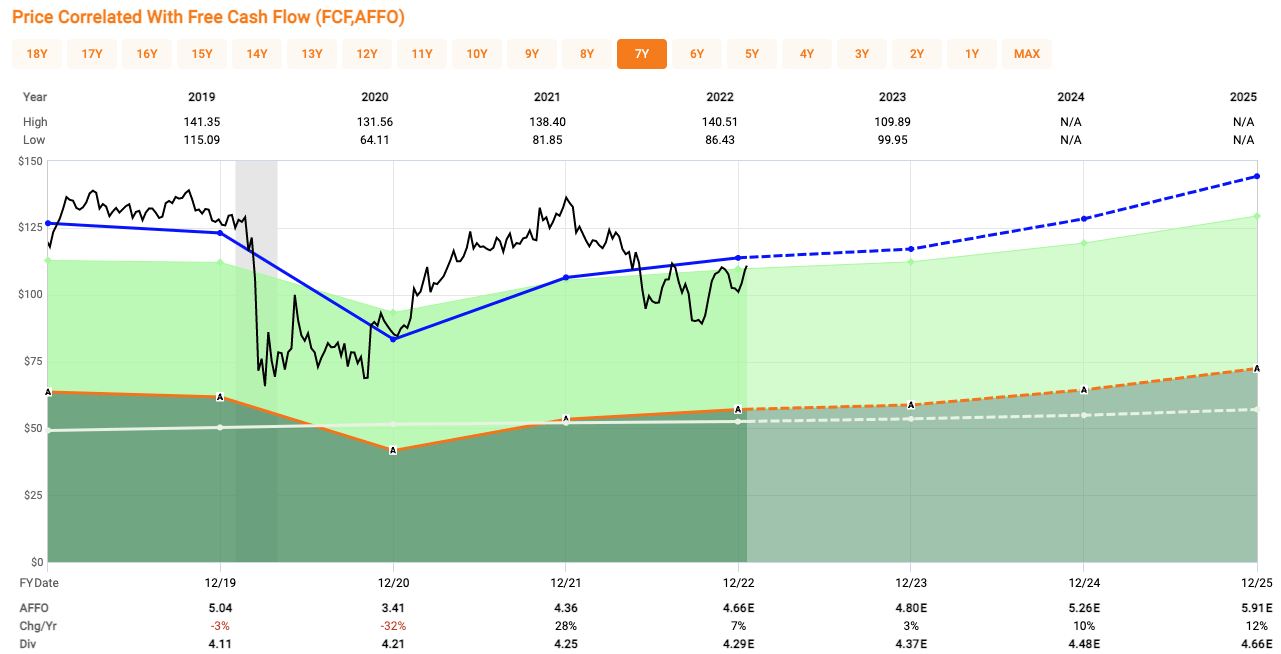

FRT looks undervalued at current levels, with shares trading at 23x next year’s AFFO estimates. Its five-year average is 24.4x.

FAST Graphs

At iREIT on Alpha, we rate shares of FRT as a Buy.

Underappreciated REIT #3 – Essex Property Trust

Essex Property Trust, Inc. (ESS) is an underappreciated apartment REIT. Much of the attention in that sector is given to the two major players, AvalonBay Communities (AVB) and Equity Residential (EQR).

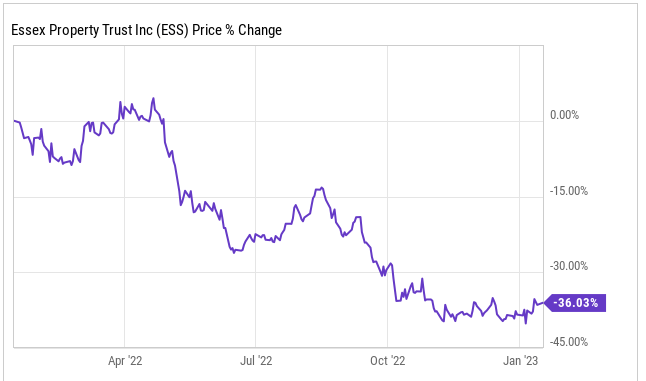

Over the past 12 months, shares of ESS are down over 35%. Admittedly, many of its peers are struggling, too.

yCharts

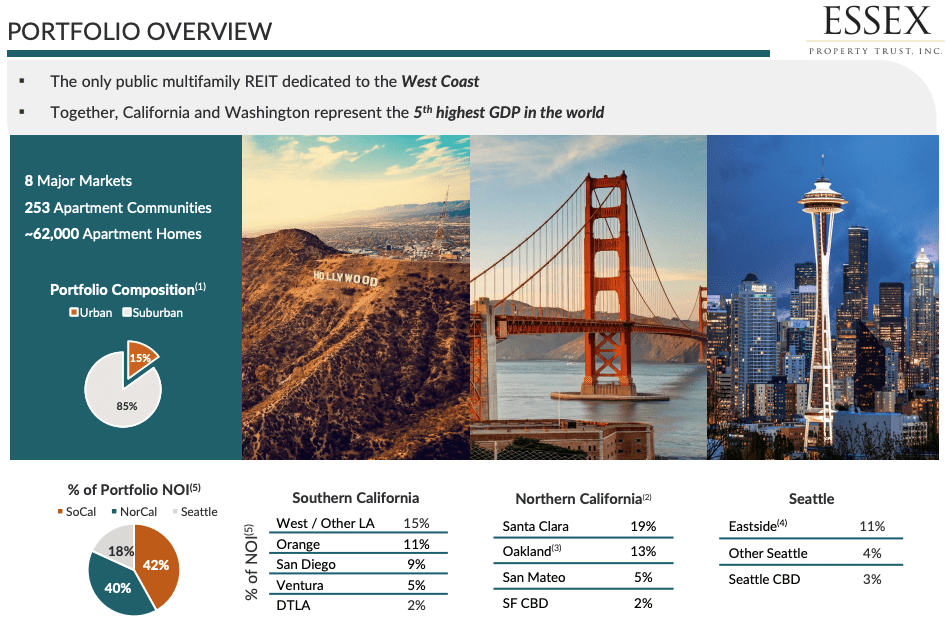

But Essex is unlike the major apartment REITs, which are more broadly located. Essex, meanwhile, is a pure-play coastal apartment REIT with properties in Northern and Southern California as well as Seattle, Washington.

ESS Q3 Investor Presentation

The West Coast has largely boasted a strong and predictable job market, and higher-income households. It’s also known for its lack of affordable housing, which plays nicely into Essex’s hands.

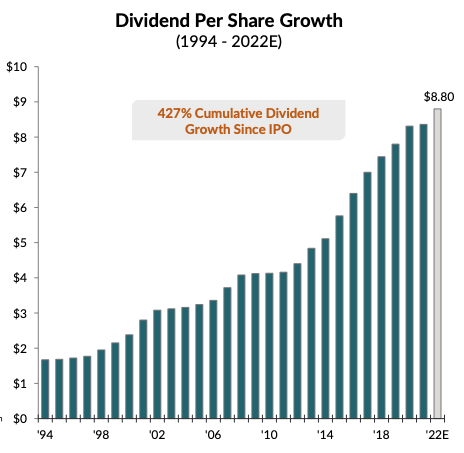

ESS isn’t up to par with FRT yet when it comes to its payouts. But it’s still impressive as a dividend aristocrat (25 years or more). The company has been growing its dividend for 28 consecutive years for a cumulative 427% since its initial public offering (IPO).

ESS Q3 Investor Presentation

The company currently pays an annual dividend of $8.80 per share, which equates to a dividend yield of 4%. ESS has a low payout ratio of just 60%.

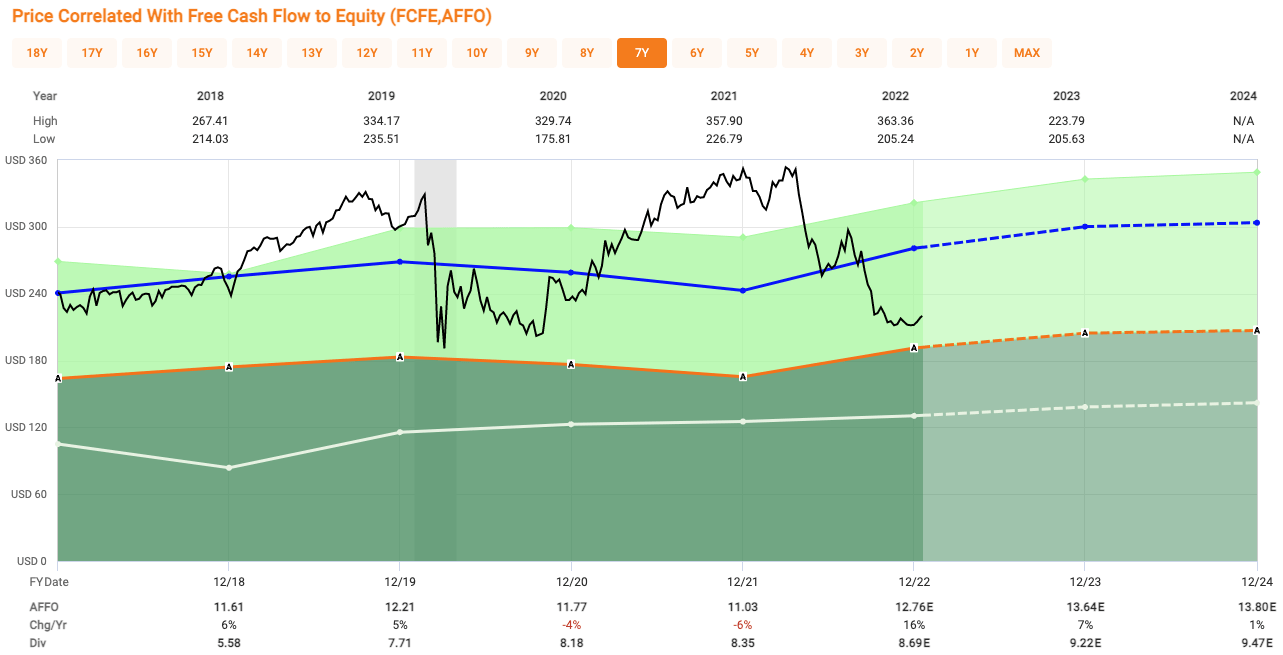

Essex is the biggest bargain on our list today, with shares currently trading at just 16.1x next year’s AFFO estimates. That’s well below its historical five-year average of 22x.

This is a huge opportunity to buy into an underappreciated blue-chip apartment REIT.

FAST Graphs

At iREIT on Alpha, we rate shares of ESS as a Strong Buy.

In Closing…

As many of my regular readers know, I’m somewhat of a comeback story myself, after surviving a brutal partnership split up in 2004, the Great Recession of 2008, and then being fired from my job in 2011 “for writing on Seeking Alpha.”

I enjoy posting motivational commentary on Twitter:

Twitter (@rbradthomas) Twitter (@rbradthomas) Twitter (@rbradthomas)

Just a few days I posted this on Twitter:

Twitter (@rbradthomas)

As it turns out, writing on Seeking Alpha has been the best thing that I’ve ever done, because I’ve been able to build a large audience (most followed on Seeking Alpha), meet many new friends, and sharpen my skillset as an investor.

Just like the Wright brothers, the secret to success is to never give up and to always fight for what you believe in, especially if “your facts and reasoning are correct.”

Benjamin Graham, who witnessed adversity before becoming wealthy, said it best, “investing isn’t about beating others at their game. It’s about controlling yourself at your own game.” He added,

“intelligence has nothing to do with IQ or SAT scores. It simply means being patient, disciplined, and eager to learn.”

Happy REIT Investing!

Be the first to comment