Nikada

Dell Technologies (NYSE:DELL) is a global American end-to-end technologies provider with TTM revenues of $104.37bn and TTM EBITDA of $8.48bn.

Though higher interest rates present a material risk to the highly-leveraged company, I believe that Dell’s leadership in consumer and infrastructure hardware, growth across high margin businesses like cloud and virtualization, and ability to navigate high-debt position the company for long-term success.

Introduction

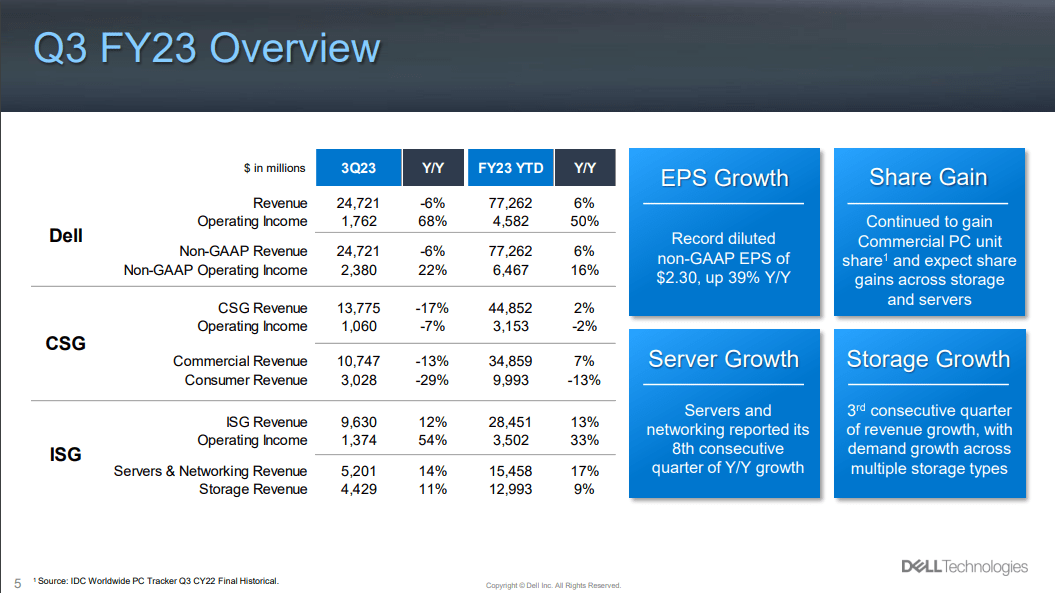

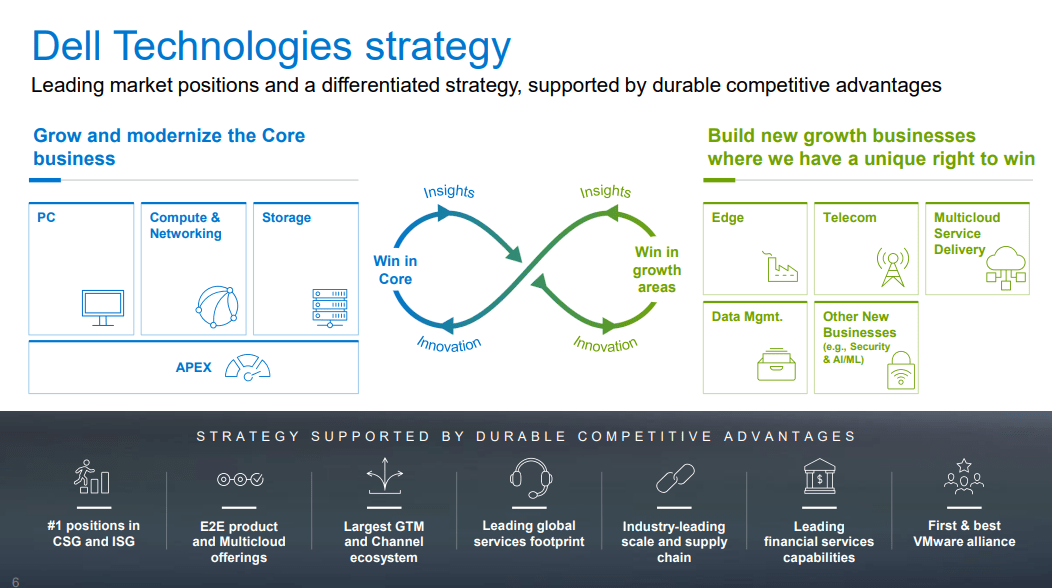

Dell can be segmented into two distinct parts; the Client Solutions Group- which encompasses their core consumer products, such as Dell computers, Alienware products, and peripherals- accounting for $13.78bn and $1.06bn in Q3 revenues and operating income respectively; and the Infrastructure Solutions Group, including server hardware solutions, computing and networking products, storage, and the Dell APEX platform.

Dell Q3 Investor Presentation

The company’s long-term aim to achieve value generation between the two aspects is both via developing a rollup sales strategy for enterprise, and penetrating the edge market for hybrid, multicloud products.

Valuation & Financials

General Overview

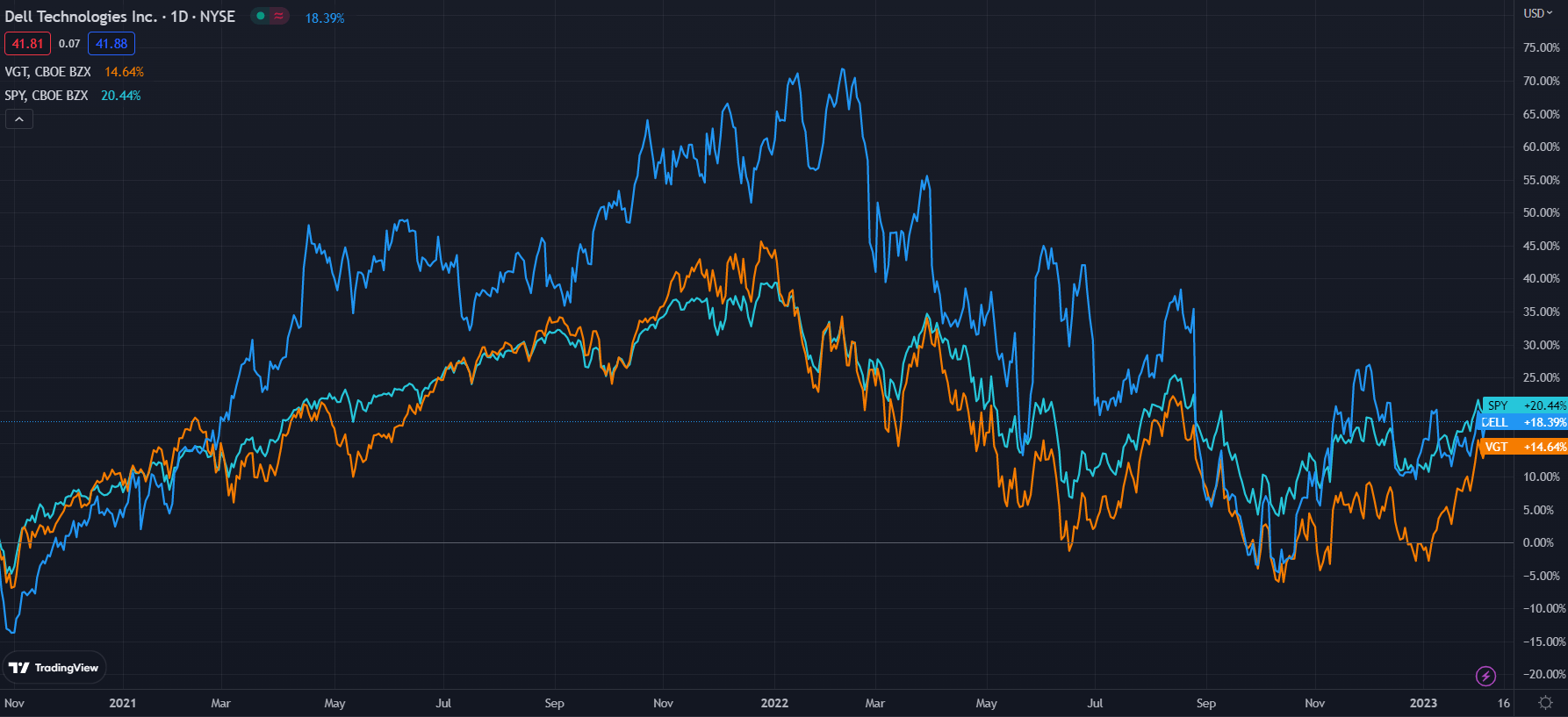

As aforementioned, Dell has trailed both the VGT and SPY significantly- due to the fact that Dell has not rallied alongside the rest of the market, and a relative discount of the company’s future potential, I believe Dell is fundamentally undervalued.

Dell (Dark Blue) vs Industry and Market (tradingview.com)

Dell’s depreciation, though, is defensible, as it has faced downward pressure on revenues and an upwards pressure on debt-servicing due to fiscal and monetary tightening.

Comparable Companies

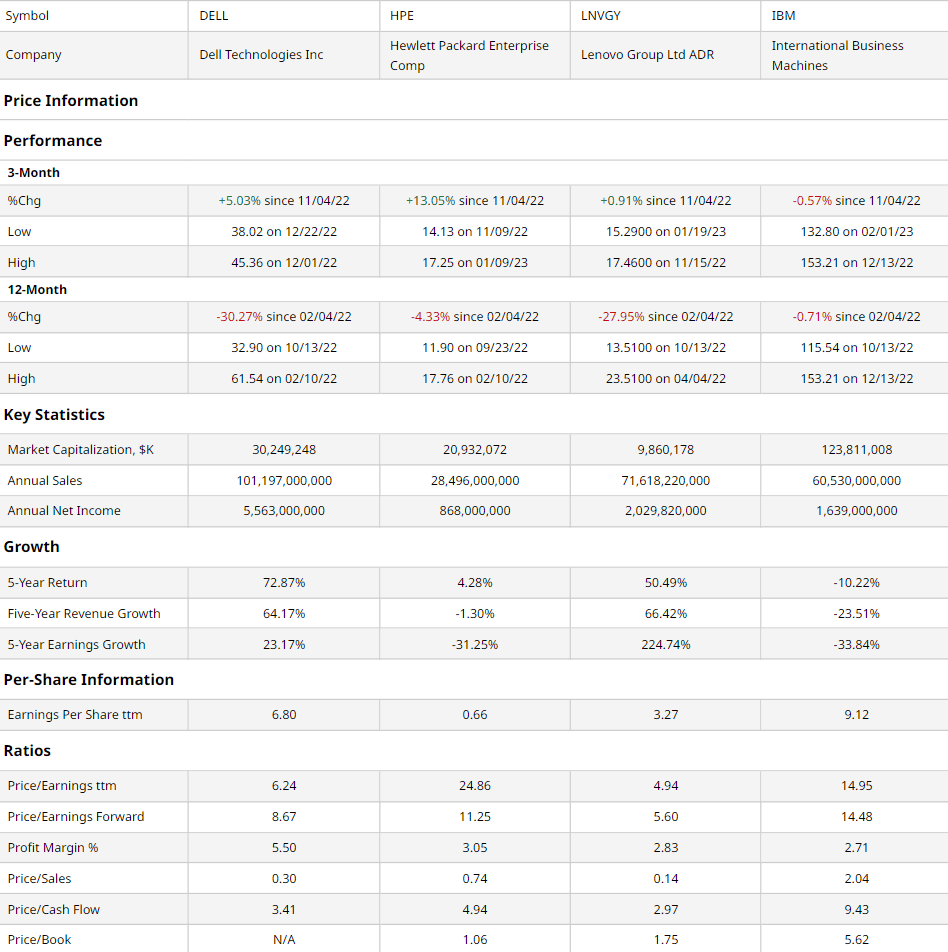

Due to the wide array of businesses Dell situates itself in, it has no one-to-one competition. Therefore I chose companies who operate in either both client and infrastructure products, though not necessarily offering the exact services Dell does or companies who are direct competitors of similar size, but not necessarily covering both segments. Hewlett Packard Enterprise (NYSE: HPE), through is a global leader in edge and hybrid cloud products; 83% of Lenovo’s (OTCPK:LNVGY) revenue comes from client sales, though they do have a footprint in infrastructure as well; International Business Machines (NYSE: IBM) has themselves accelerated their foray into cloud and hybrid cloud settings.

barchart.com

Dell demonstrates a superior inherent value proposition to its competitors through both stronger margins and the second-best multiples-based value after Lenovo.

It is worth noting, however, that Lenovo’s relative undervaluation is a symptom of a geopolitical risk premium, being based in Hong Kong, rather than an intrinsic undervaluation such as what I believe Dell is experiencing.

Additionally, Dell’s TTM price decline only signals their regression from the mean and thus more room to grow into.

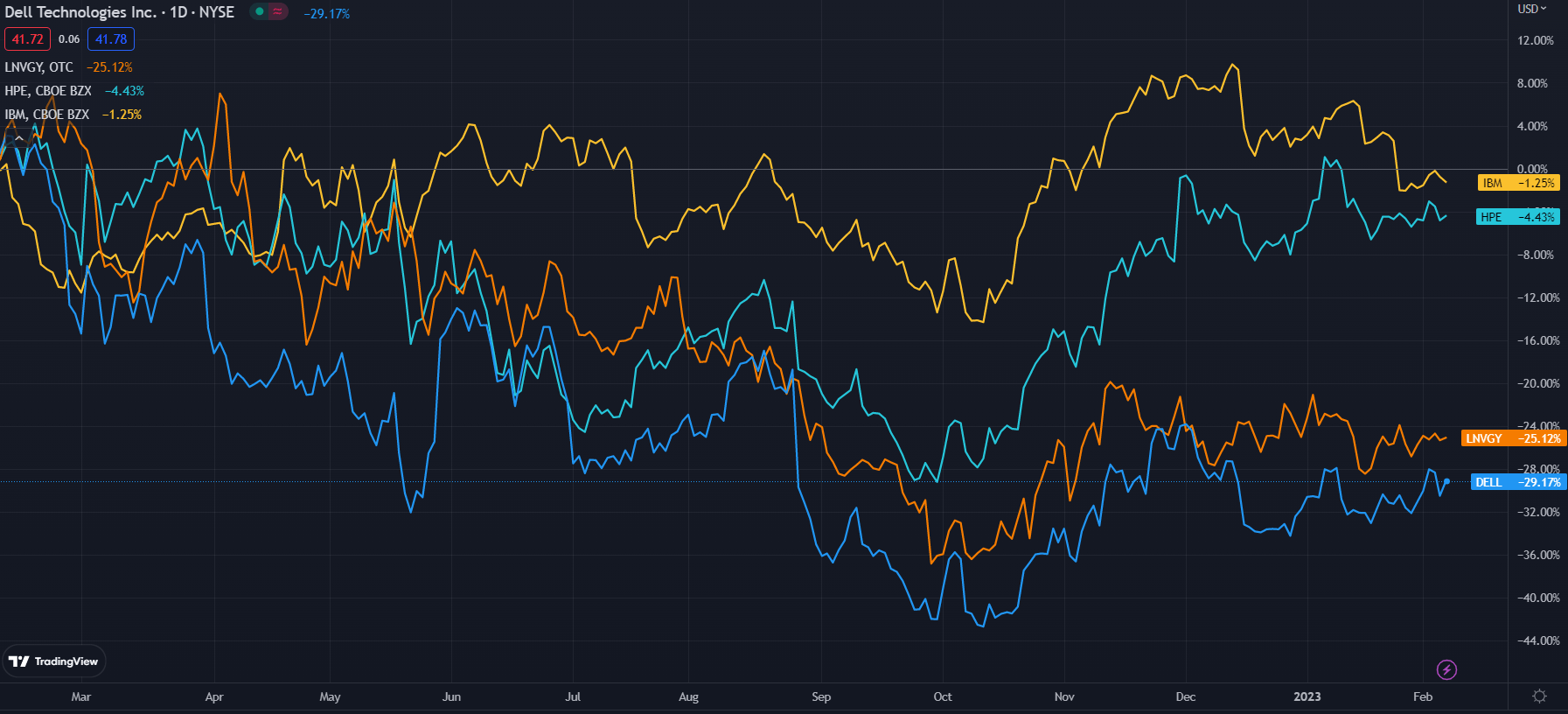

Dell (Dark Blue) vs Comparable Companies (tradingview.com)

Valuation

According to my DCF model, at its base case, Dell is undervalued by 37%, with a fair value of $66.23. The model operates on a net income basis and assumes a discount rate of 12%, which is Dell’s 10.6% WACC with a risk premium associated with its high debt levels.

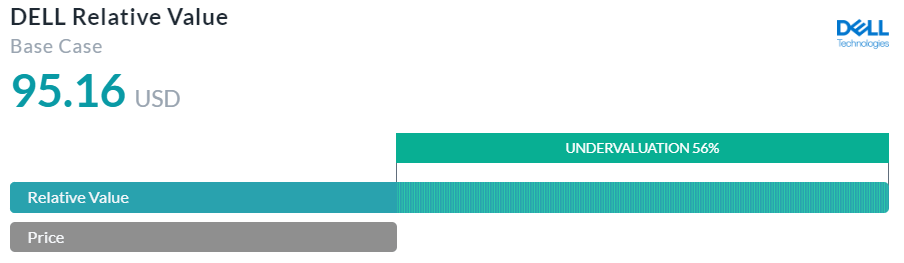

AlphaSpread

The company’s undervaluation is further supported by a multiples-based relative valuation tool, which employs multiples such as P/S, P/E, and P/B. In its base case, it estimates an undervaluation of nearly 56% at a price of $95.16. However, this valuation fails to account for Dell’s highly leveraged position.

Thus, using a weighted mean, which gives more value to the DCF, Dell should be valued at ~$75.87.

Positioned for Synergetic Infrastructure Success

At the core of Dell’s revenue and margin growth lies the growth of its Infrastructure Solutions Group – combined with the underlying strengths of its client business, Dell has the ability to generate synergetic revenues and growth.

For instance, Dell has a large global services footprint due to a pre-existing enterprise client install base- this can then be leveraged for the implementation of hybrid cloud services.

Dell Q3 Investor Presentation

Moreover, as the macro computing cycle reverts to decentralized products and IoT, edge computing becomes of increasing significance; with Dell providing goods and services at both ends of the data and computing spectrum, they have the ability to generate complementary value for clients.

And Dell recognizes these opportunities. With their APEX platform, Dell unifies their technologies and creates consumer lock-in with higher-margin software servicing. This accelerates Dell’s ability to access its $720bn core business TAM.

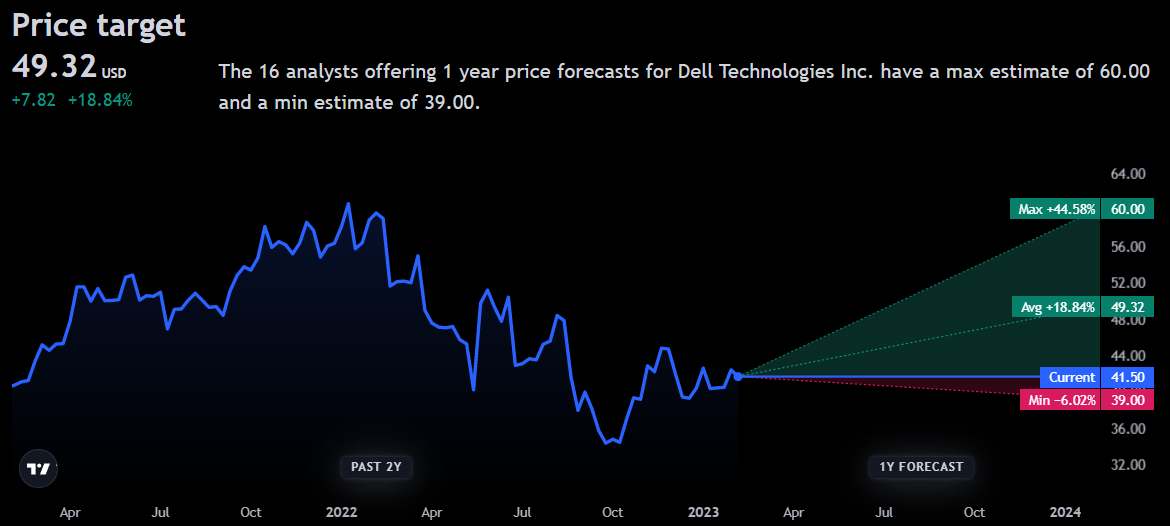

Wall Street Consensus

Analysts echo my positive view of the company, forecasting an average 1Y price target of $49.32, up 18.84% from today.

tradingview.com

Even at its minimum price target, Dell is only forecasted to face a price decline of -6.02%, which, relative to macro conditions and internal financial constraints, demonstrates low sensitivity.

Risks

High Debt Still a Risk

Not only do high debt-levels exacerbate the effects of rising interest rates on the company itself, but they also materially impact Dell’s input costs and ability to conduct R&D. Thus, as a late-joiner in the multicloud game, despite aggressive and impressive growth, this may affect their ability to compete in the long-term.

Company Risks Disconnect Between Businesses

Although there is high potential to achieve synergies between their two principal business segments, if Dell does not successfully integrate them, they risk spreading their resources too thin, compressing already stagnant margins.

Recessionary Pressures are Material

Induced by higher interest rates and contractionary fiscal and monetary policy, a potential recession, or recession-like conditions may lead to a large decline in demand for enterprise products, since large businesses tend to be more sensitive to recessions than SMEs. As a majority of Dell’s profit is associated with enterprise, this is a significant risk.

Conclusion

In the short term, Dell’s relative undervaluation, strength in core retail segments, and continued dominance in infrastructure hardware will ensure share price appreciation.

In the long-term, I believe that Dell’s position enables them to achieve synergetic growth between their two principal segments, especially considering their higher margins in the APEX platform working to connect the two via a multicloud enterprise approach.

Note: As of writing this article, Dell has announced a ~6,650 employee layoff; beyond addressing macro trends, this further demonstrates the company’s ability to nimbly adapt to shifting financial circumstances.

Be the first to comment