RomoloTavani/iStock via Getty Images

The February 8 report by International Flavors & Fragrances (NYSE:IFF) was disappointing, but not completely unexpected given the economy. Based on the new guidance for 2023 it seems that they are not expecting an EBITDA improvement next year, which caused investors to sell IFF stock in after-hours trading. Based on the latest after-hours stock price, IFF is still up about 7% from my September 19 article when I rated the stock a buy for its current and future dividend income, but because of the latest report I have lowered my recommendation to neutral/hold.

New Guidance Numbers Tanked the Stock

The cause of the stock price to drop over $5 in after-hours trading, in my opinion, was their new guidance statement for 2023. According to their press release, “Comparable currency neutral adjusted operating EBITDA growth for 2023 is expected to be approximately flat versus prior year.” and “Comparable currency neutral sales growth for 2023 is expected to be approximately 6%”. The statement also included, “The Company expects full year 2023 sales to be approximately $12.5 billion, with an expected full year 2023 adjusted operating EBITDA of approximately $2.34 billion”. (Note: their numbers were adjusted for the expected sale of Savory Solutions.)

These guidance numbers compare to a December 7 Investor Day statement about 2023 EBITDA of “preliminarily mid single-digit currency neutral growth”. The reduced guidance is especially troubling given that many economists have become more positive about the 2023 economy since early December and that it seems China, one of their biggest markets, continues to open up.

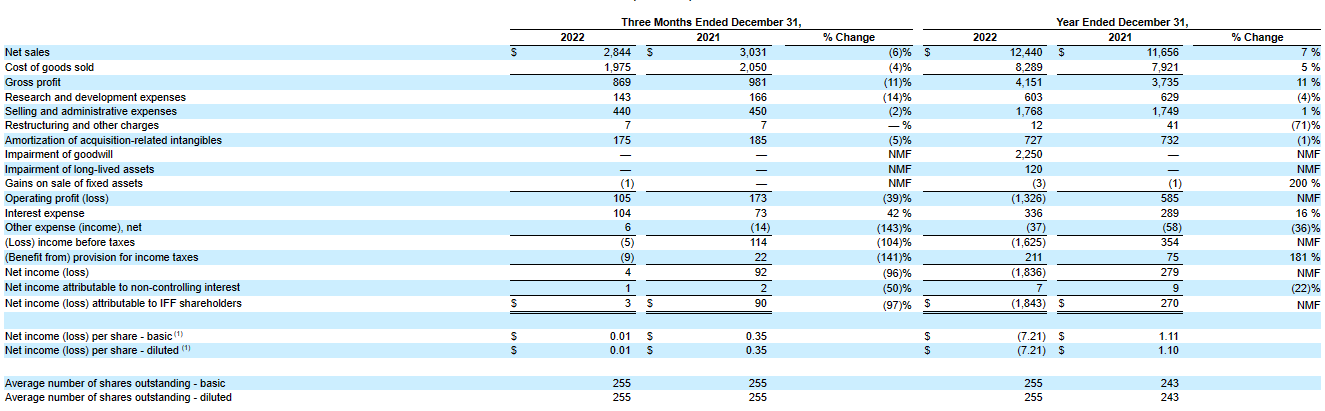

Latest 4Q and 2022 Results

The 4Q results were close to expectations. Investors needed to adjust the annual 2022 numbers for the $2.25 billion or about $8.80 per share goodwill impairment charge taken earlier last year.

4Q and Annual Income Statements 2022 and 2021

sec.gov

I was not surprised that unit sales declined. I suspected that some customers were ordering more earlier in the year than they actually expected to be needing because of so many reports of supply chain problems and they did not want to be caught short. As the supply chain problems decreased these same customers then cut back on their purchases/orders in 4Q. In addition, I think final consumer demand for many products has declined because of higher prices. Consumers might still be buying a specific product, but in a smaller size or smaller quantity. For example, instead of buying a 20-ounce bottle of soda they buy a 12-ounce can. This has a negative impact on IFF. This also may help explain why their inventory level remains so elevated at $3.151 billion compared to $2.516 billion at the end of 2021. This was also a slight increase from $3.122 billion at the end of 3Q.

Year-End Balance Sheets 2022 and 2021

sec.gov

This inventory number had a sharply negative impact on cash generated by operations in 2022. Net cash provided by operating activities in 2022 was only $345 million compared to $1.443 billion in 2021. This $345 million number compares to $810 million cash paid in dividends in 2022. It is a yellow flag and hopefully we don’t see sharp price declines over the next few months that would result in a large loss on the value of the inventory before it is sold.

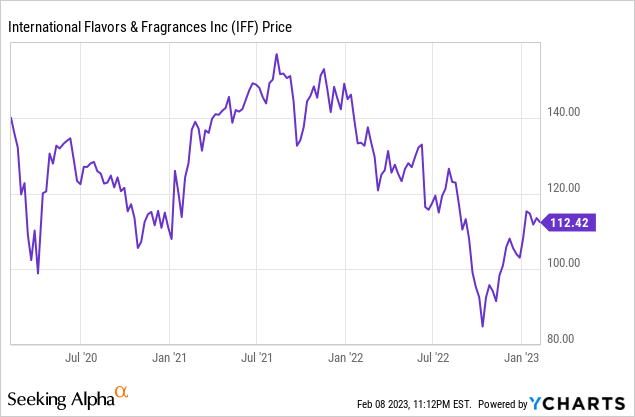

IFF Stock Price – Three Years

Why I Am Still Holding

I am still holding my IFF stock after buying additional shares at lower prices after my September article for two reasons. First, I think the dividend will continue to increase over time and the stock already has a modestly favorable current dividend yield of 3%. Second, Carl Icahn owns 644,510 shares or about 4% of IFF. He recently also negotiated to have one of his employees sit on the company’s board of directors. At the same time that Icahn getting a seat was announced, it was announced that the current chairman of the board, Dale Morrison resigned. Perhaps Icahn can “shake things up” to get improved decisions by management.

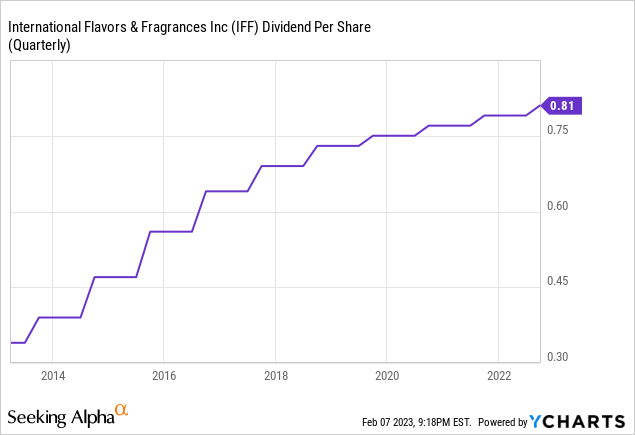

Quarterly Dividends – Last 10 Years

Selling Assets to Deleverage

I was encouraged late last year about a potential improving balance sheet because IFF announced it was selling their Savory Solutions Group for $900 million cash to PAI Partners. According to the announcement, the price was about 14x the last 12 months EBITDA and had revenue of $475 million. The 14x multiple implied an EBITDA of about $63 million. It is expected to close in 2Q 2022, and the cash will be used to paydown debt. (See below.) I expect additional asset sales in 2023 based on prior comments made by management.

Wednesday’s guidance included a statement that the “guidance excludes approximately $350 million in sales and approximately $50 million in adjusted operating EBITDA for the anticipated Savory Solutions divestiture”. I read this statement to mean that total company guidance numbers include Savory Solutions for 1Q and for a portion of 2Q until the sale is completed.

Too Much Debt

IFF has way too much debt. Their S&P rating was lowered last October to BBB- from BBB mostly because of their high debt/EBITDA multiple. BBB- is the lowest rating in the investment grade category. If it gets lowered again to be below investment grade a lot of investors would be restricted from owning the lower quality notes/bonds.

Their latest debt multiple is 4.14x based on $2.523 billion credit adjusted 2022 EBITDA and $10.452 net debt. Assuming that the asset sale is completed and all $900 million is used to pay down debt, I estimate the multiple will be approximately 3.86x. (Note: the operating EBITDA is not usually the same as the credit adjusted EBITDA.) This is still too high, but at least it is moving in the right direction.

Doing a very simple back of the envelope approach of adding long-term and short-term borrowings at the end of the year divided by the annual interest expense, IFF only paid an average interest rate on their total borrowings of 3.06%, which is very low relative to current interest rates. They have notes maturing in 2023 with a 3.3% coupon, a 1.88% coupon in 2024, and a 1.22% coupon in 2025. They need to pay these down with cash from asset sales and/or cash from operations, in my opinion, instead of planning on refinancing them with notes that most likely will have much higher coupons given the outlook for interest rates over the next few years.

I strongly disagree, however, with a statement from their December 7 Investor Day Presentation: “to reauthorize a share buyback program once <3.0x leverage target realized (Target 2024)”. They should continue to reduce debt and/or increase the cash dividend instead of irrational stock repurchases, especially if there is some new tax on share repurchases, as President Biden has suggested.

Conclusion

After this latest report I expect there will be downgrades by some Wall St. analysts. I am changing from a “buy” to a “neutral/hold” recommendation. IFF has too much inventory heading into a possible recession and the potential for declining prices because of decreased demand.

I averaged down after I bought IFF shares in September, so I am currently sitting on a very nice paper profit. I am holding because I still expect, over a long time period, that IFF will continue to raise their cash dividend and I expect Carl Icahn will force some type of improvement in management. I also expect additional asset sales that will help to decrease leverage.

Be the first to comment