Khosrork/iStock via Getty Images

Investment Thesis

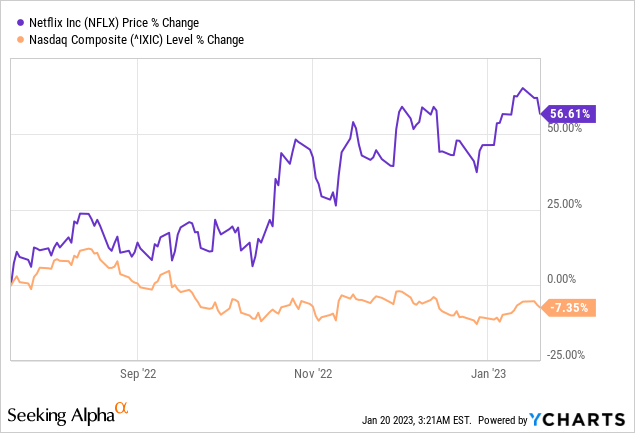

Netflix (NASDAQ:NFLX) sees its stock pop after earnings. Investors welcome the fact that subscriber figures once again shine strongly. What’s more, with the stock traded off its previous highs, many investors are hoping that the playbook of 2022 is done and dusted and that the bull market can resume.

For my part, I struggle to make much sense of the appeal in these results. The business is clearly not growing all that strongly. And Netflix’s use of excess cash to repurchase also leaves me in doubt.

Altogether, I remain on the fence.

Subscriber Numbers, Again?

Back in Q3 2022, Netflix’s shareholder letter stated:

[…] starting with our Q4’22 letter in January of 2023, we’ll continue to provide guidance for revenue, operating income, operating margin, net income, EPS and fully diluted shares outstanding for the following quarter, but not paid membership.

Of course, Netflix felt that it was struggling to grow its user base, so it needed to move the narrative beyond this key metric and to other metrics, where Netflix believed it could excel.

More specifically, Netflix had lost its growth multiple on its stock and it needed to move the narrative to its revenue growth story.

But since its revenue for the quarter ahead points to less than 10% CAGR (including F/X changes added back, guided for +8% y/y), Netflix spent the bulk of the guidance in its shareholder letter discussing the intricate movement of how its subscriber figures will unfold in its upcoming quarters.

[…] modest positive paid net adds in Q1 ’23 (vs. paid net adds of -0.2M in Q1’22). Our expectation of fewer paid net adds in Q1’23 vs. Q4’22 is consistent with normal seasonality and factors in our strong member growth in Q4’22, which likely pulled forward some growth from Q1’23.

Essentially, Netflix presumed at the time of its Q3 results that its Q4 net subscriber addition figures would come in at around 4.5 million, while the final number actually came in at 7.7 million.

Does Anyone Care?

In the past 6 months, Netflix’s stock is up more than its peers in the Nasdaq. Does anything anyone say about Netflix, matter? Clearly, the bears have been wrong about this stock.

There’s no point in trying to justify what Netflix should be valued like, the fact is that this is much more than a ”hope” trade. A hope trade is when the stock is up a few percentage points in a short period of time.

This is performance clearly much more than just a hope trade. But what about its valuation?

NFLX — 30x Earnings, Does it Matter?

Netflix trades back at 30x forward earnings, so what? Yes, there is a ton of competition in streaming. Yes, the business is clearly not growing its bottom-line even close to 20% CAGR. But this is clearly over-rationalizing.

Netflix declares that it can get its free cash flow to at least $3 billion in 2023. Knowing Netflix’s history of consistently underpromising and over delivering, I believe that it’s very likely that Netflix’s run-rate in twelve months could be closer to $4 billion of free cash flow.

This puts Netflix priced at 35x 2023, exit run rate. Does this strike anyone as particularly cheap?

Cheap Enough for Buybacks?

Netflix states that any excess cash flow that the business holds beyond 2 months of revenues, after reinvesting into the business or acquiring potential bolt-on businesses, Netflix will use to resume repurchasing shares.

Given that in 2022, when the stock was traded at substantially lower prices than Netflix trades for right now Netflix did not buy any shares. Consequently, I have to question Netflix’s ability to be a good capital allocator.

Similarly, back in 2021, when Netflix’s shares were being priced at higher than $500 per share, Netflix was very active in repurchasing shares and deployed $600 million towards buybacks.

The Bottom Line

Rather than fight and twist the facts for what we wish they were, it’s time for bears to just accept that some stocks don’t make sense.

While I believe that Netflix is overvalued, I have to admit that Netflix’s ability to continue to build an alluring narrative is something that ”value investors” struggle to adequately price.

Put another way, growth investors simply ”get it” and see a moat where value investors don’t see the free cash flows that support its valuation. And clearly, in the past 6 months growth investors have been absolutely right about this stock. Let’s not overthink that in the past 3 years, anyone that bought the stock is probably holding onto a loser.

Be the first to comment