imaginima

After a strong performance in 2021, National Storage Affiliates (NYSE:NSA) shares have plunged 48% over the past year, underperforming the broader REIT index/ETF (VNQ) which was down 28%. While interest rates have risen and rental growth has slowed from the blistering pace seen over the past 18 months, self-storage has proven to be a high growth industry over the long term and has exhibited strength even in economic downturns.

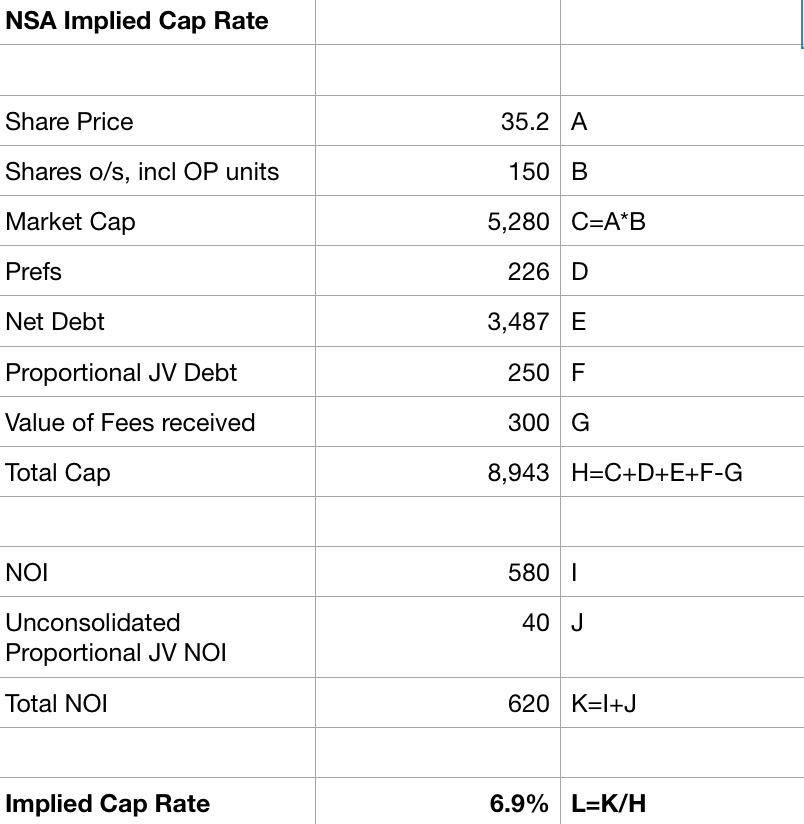

NSA offers investors the opportunity to buy a leading self-storage REIT for a very attractive price. At $35 per share, NSA trades at less than 13x FFO, an implied cap rate of 6.9% and a dividend yield 6.2%. The company has a strong balance sheet (net debt + preferred are ~6.0x EBITDA) and is poised for continued growth over the next decade. I believe this is a compelling opportunity for long-term, conservative investors seeking growing dividend income.

What’s to Love about Self Storage?

Quite a bit as it turns out – consider:

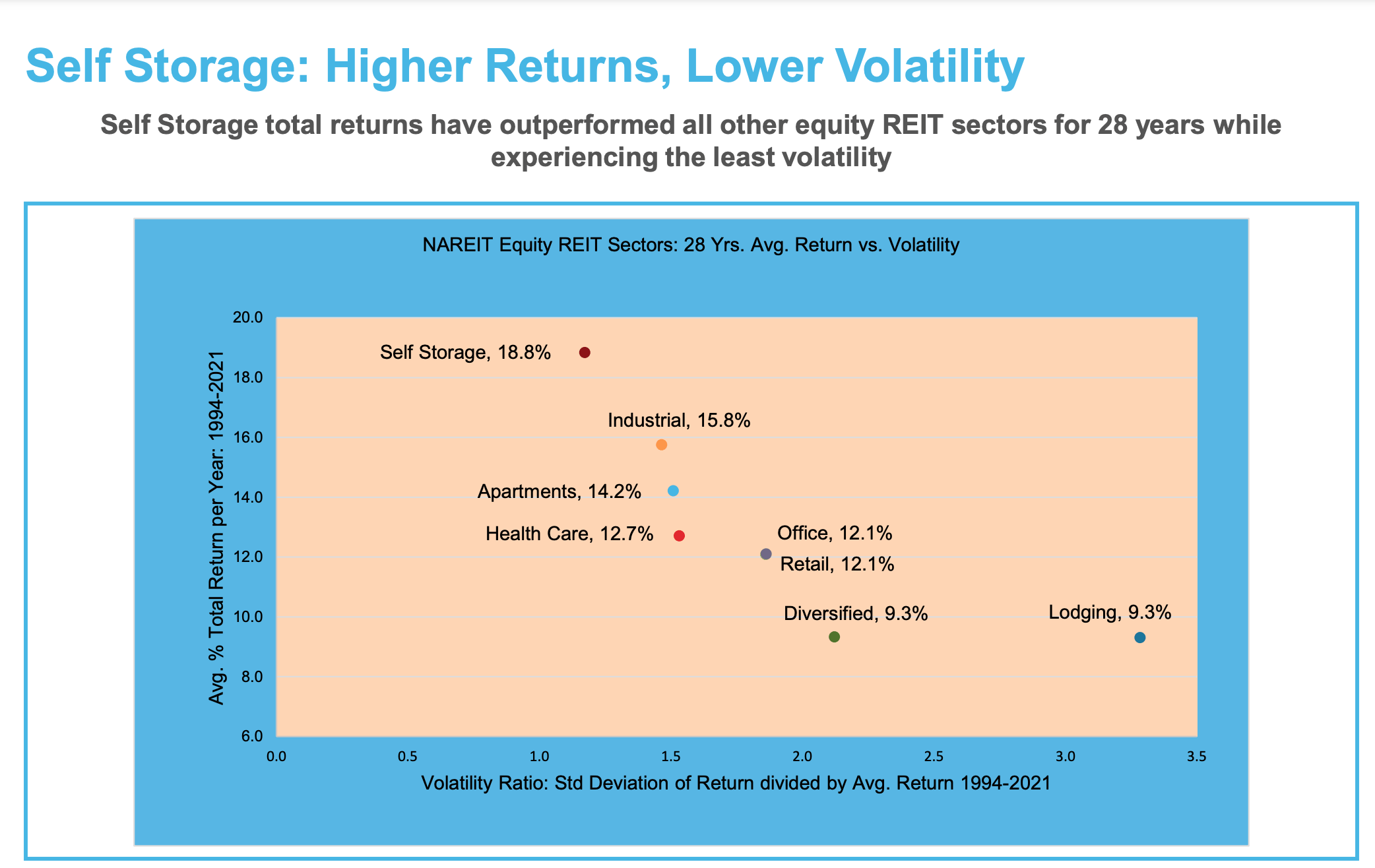

Long-term Outperformance (NSA Investor Presentation)

As shown above, self-storage REITs have created tremendous wealth for shareholders over the past 28 years.

Limited capital maintenance capital expenditure requirements – unlike malls or offices which require significant tenant incentives and capital spending to remain attractive to tenants/shoppers, self-storage facilities are simple structures that require limited refurbishments. While capital expenditures generally soak up 30% of NOI for malls/offices, self-storage properties consume just 7-8% of NOI. This means more funds available for dividends, debt pay down, and investment in new properties.

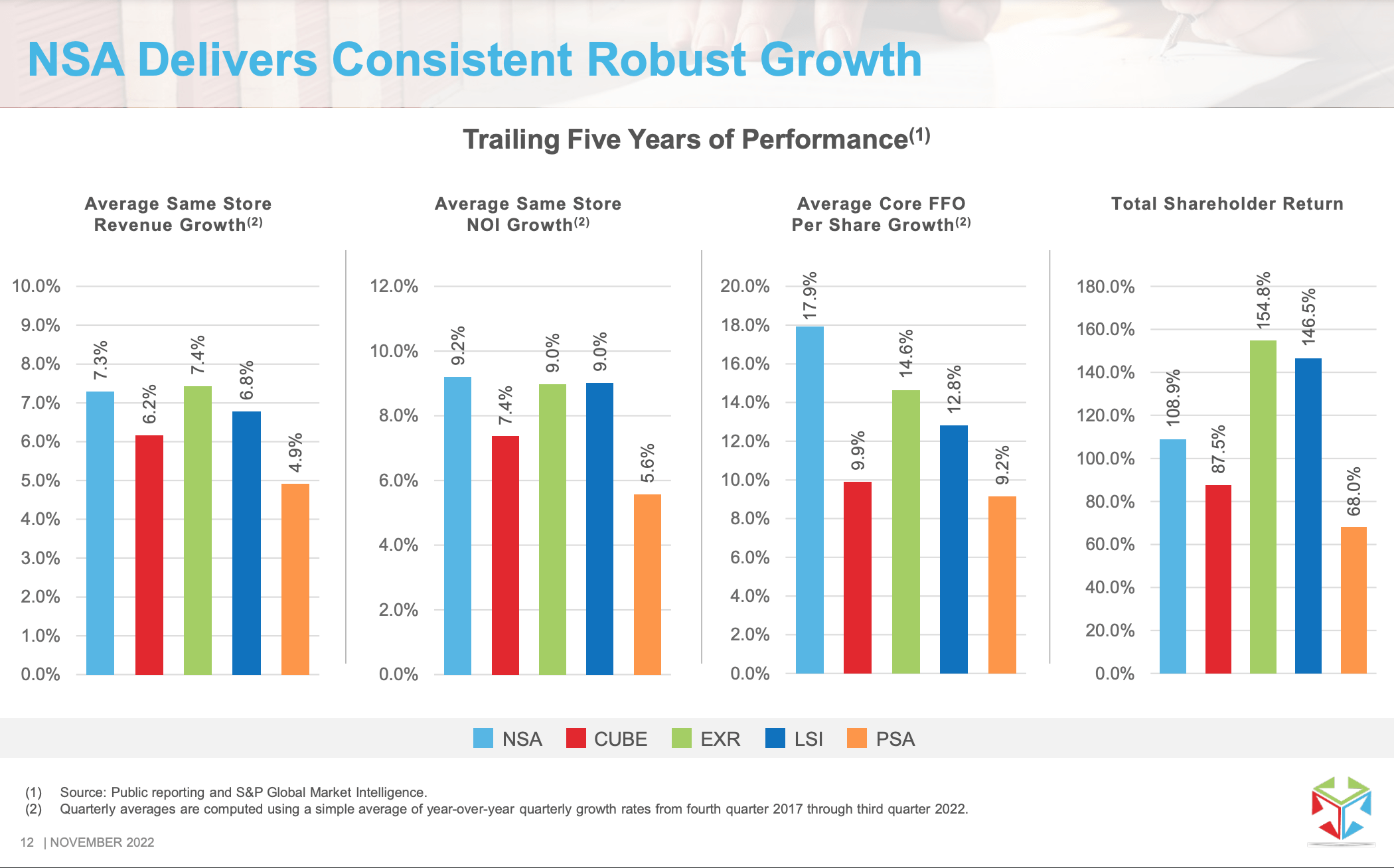

Strong pricing power for renewals – while ‘street rents’ (rents offered to new tenants) often see price competition, rents almost always increase for existing customers (termed ECRI, Existing Customer Rent Increases) for the simple reason that moving is unpalatable to most customers. This is aided by the fact that storage unit rents represent a relatively small household budget item unlike apartment rents (which typically consume 18-25% of a person’s income). This has led to strong growth in same store NOI as shown below.

5 Year Performance Metrics (NSA Investor Presentation)

Recession-resistant – the industry has performed well during periods of economic downturns. Household downsizing typically benefits self-storage as people choose to store items when moving to smaller residences (irrationally in many cases as the cost to store exceeds the value of the items stored).

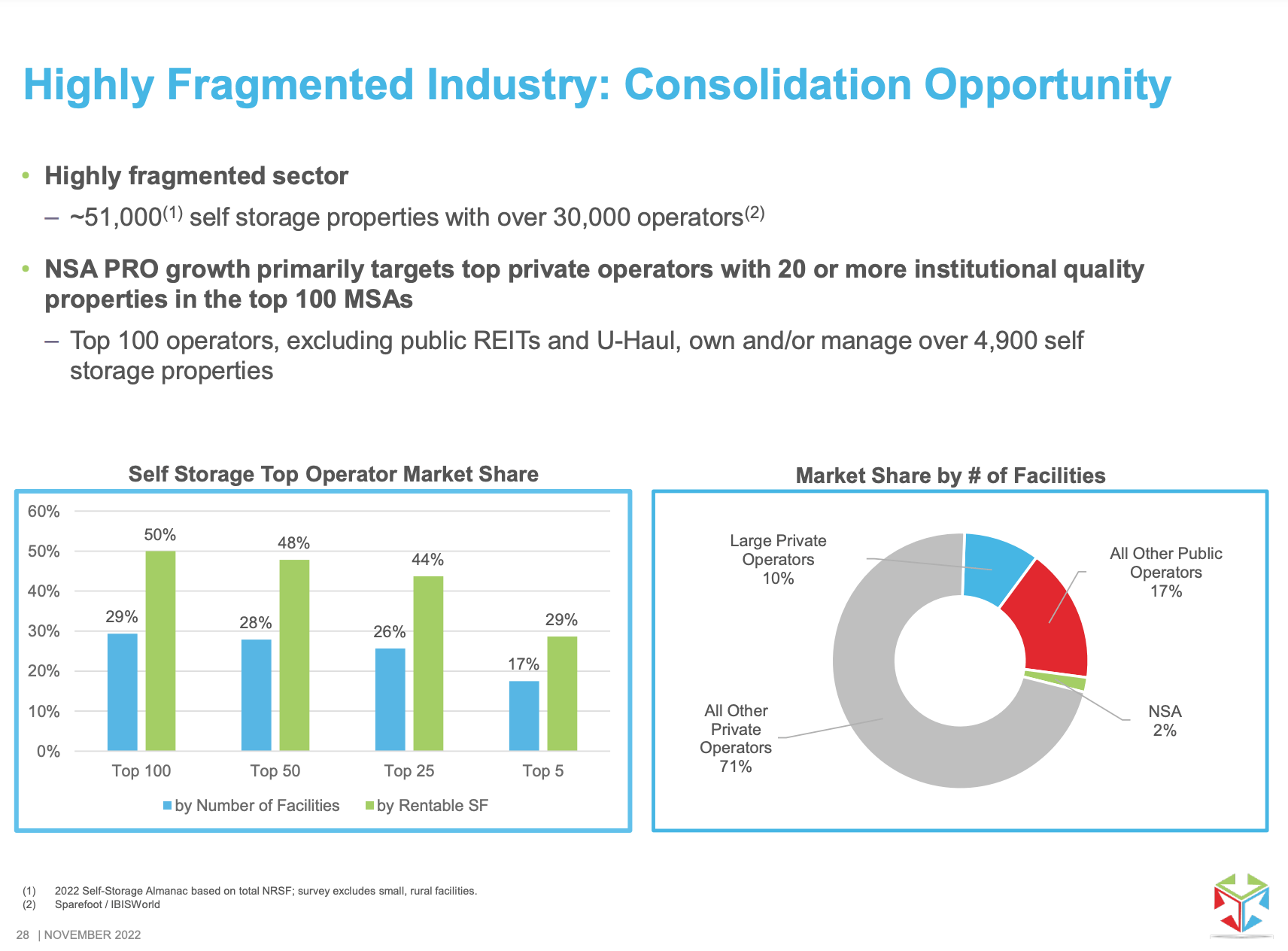

Industry consolidation is an ongoing source of external growth – as shown below, the self storage industry is highly fragmented with public REITs owning just ~19% of total facilities (and ~30% of industry square footage). This has allowed the self storage REITs to accretively acquire properties and grow per-share FFO and NAV.

Self Storage Industry Structure (NSA Investor Presentation)

Why I’ve chosen NSA

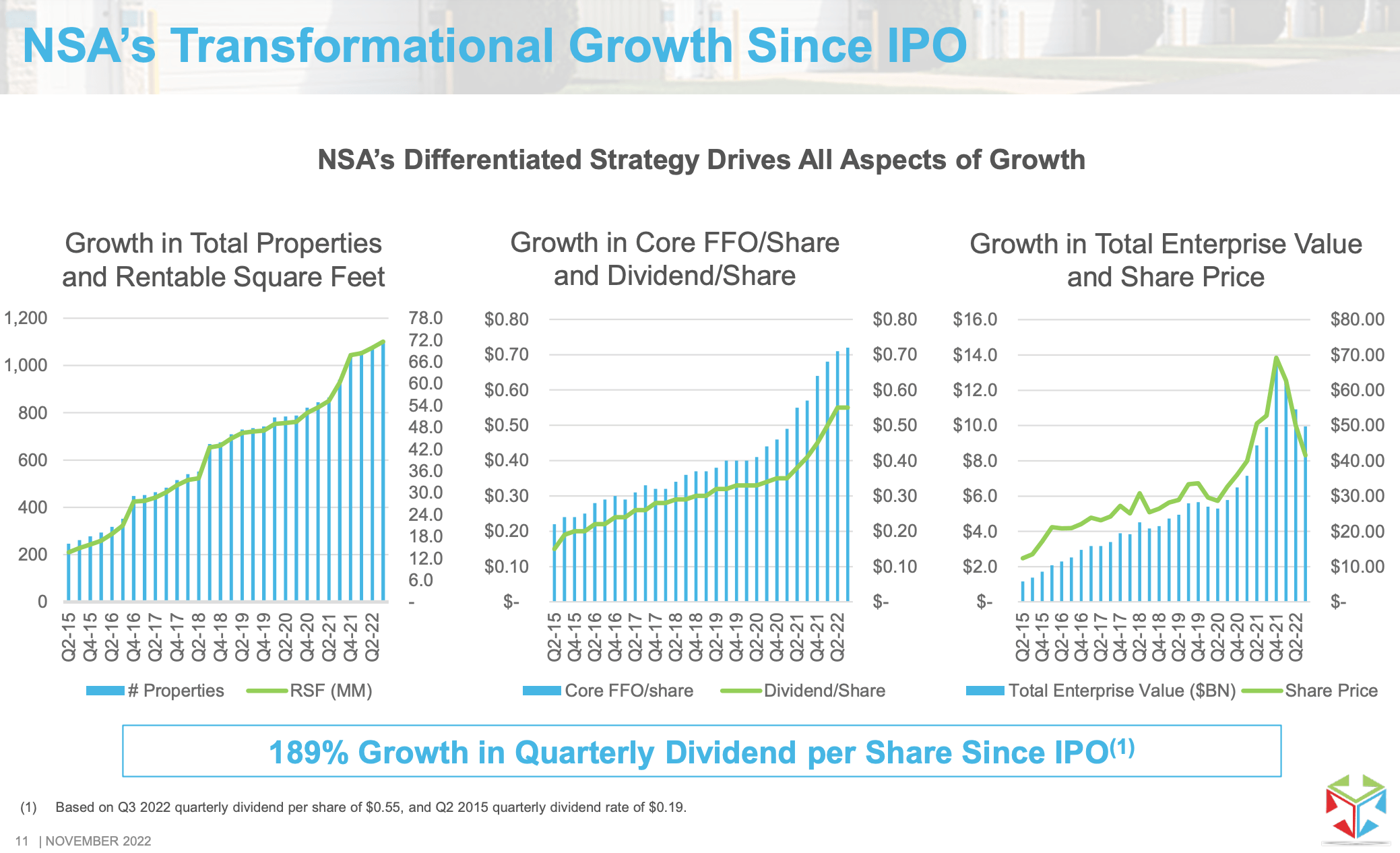

NSA Performance since IPO (NSA Investor Presentation)

As shown above, NSA has an excellent track record of growing both same store NOI (+9.2% annually over the past 5 years) as well as creating value for shareholders through acquisitions (FFO/share has steadily outpaced same store NOI growth).

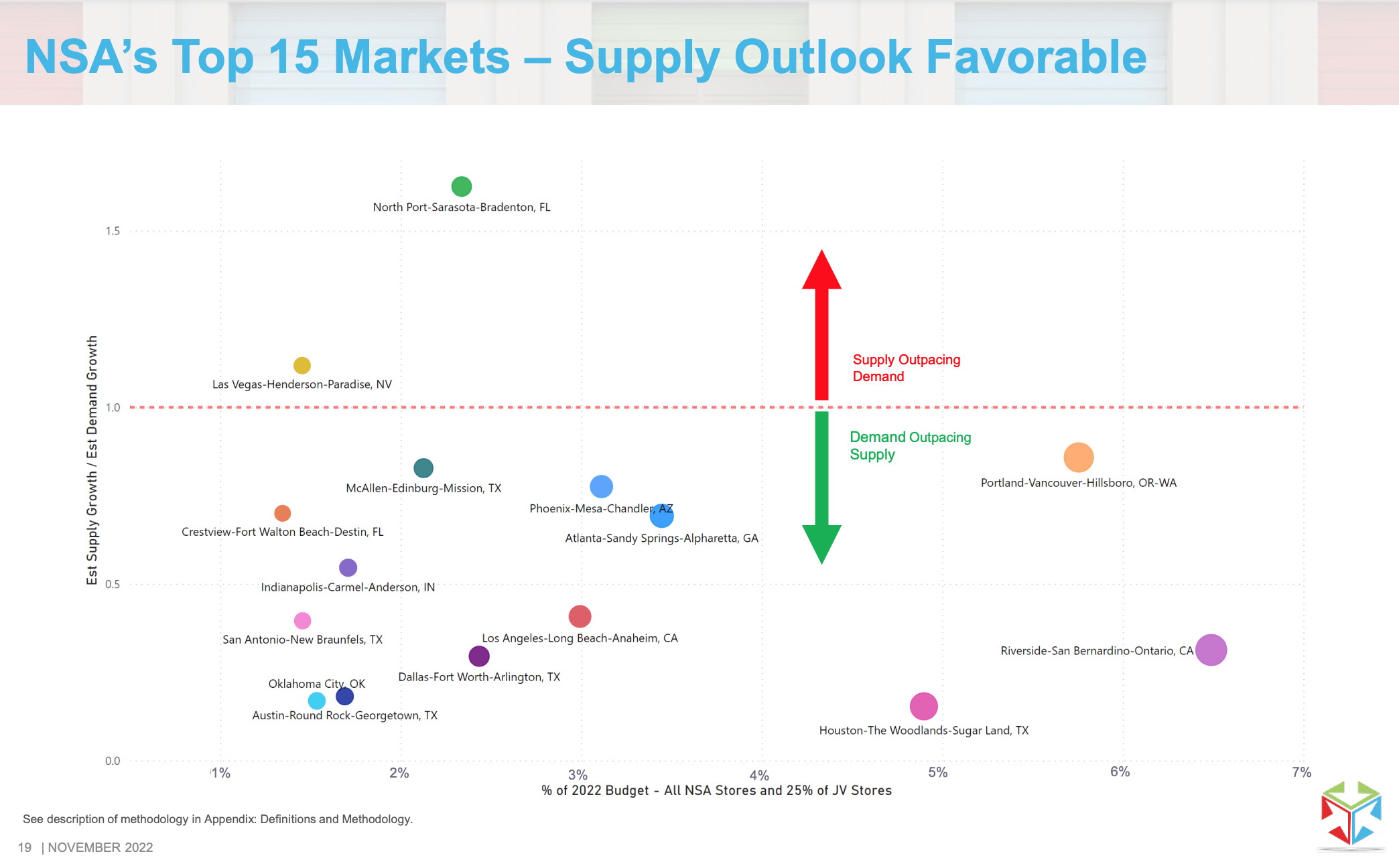

While supply increases from new developments are a fact of life for the self-storage industry, NSA’s portfolio is relatively well positioned as shown below which bodes well for continued growth in rent and NOI going forward.

Supply Outlook (NSA Investor Presentation)

Moreover, NSA trades at an attractive valuation. At 12.5x FFO, NSA trades 16-20% below peers like Extra Space (EXR) and Public Storage (PSA) and as shown below has a 6.9% implied cap rate (60-90 basis points above EXR and PSA). Over time I expect this valuation gap to narrow, if not disappear altogether. At 16x FFO, my expected fair value for NSA is $45 per share (+28% versus current price).

NSA Implied Cap Rate (Company Filings; Author Estimates)

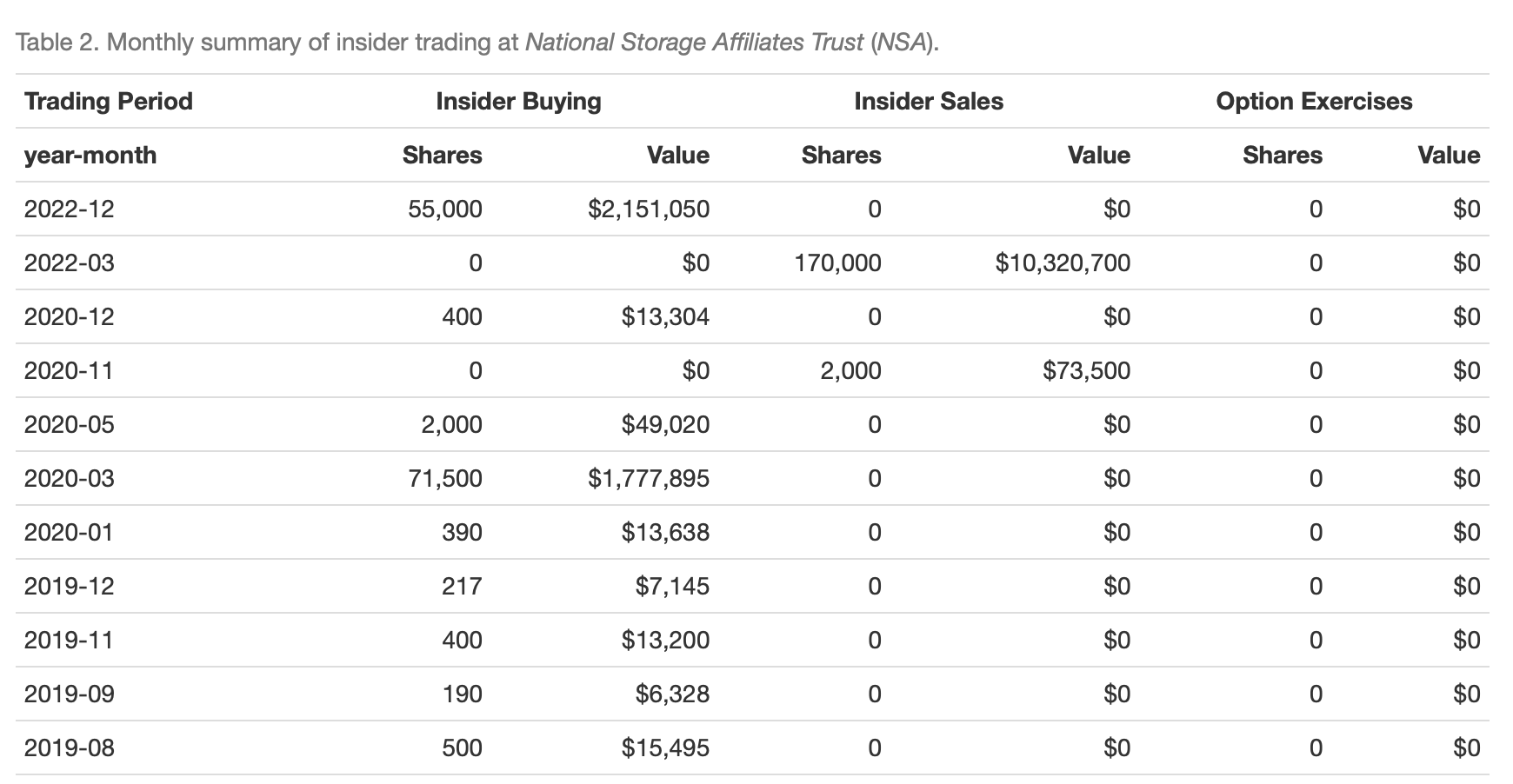

Moreover, insiders seem to agree that NSA is an attractive investment opportunity as evidenced by $2 million worth of recent insider purchases (shown below) at roughly the current share price.

NSA Insider Buying (Insider-Monitor.com)

Conclusion

I see the decline in NSA shares as an excellent opportunity to buy a great collection of assets at a discounted price. The company has a strong balance sheet (net debt + preferred are ~6.0x EBITDA) and is poised for continued growth over the next decade. I believe this is a compelling opportunity for long-term, conservative investors seeking growing dividend income.

Be the first to comment