Wirestock/iStock via Getty Images

Author’s Note: This article was published on iREIT on Alpha before Christmas of 2022.

Dear readers/followers,

By now you know that I’m a pretty diversified sort of investor. I invest both in EU stocks and US stocks. I invest in companies from across the board in terms of sectors geographies, and even different currencies.

My core portfolio is large – and it’s not the only one I manage either, as I manage a corporate portfolio as well as a few others as well.

At the same time, I keep track of and write about a multitude of companies – over 100 at least. That takes time – and that’s obviously why this and the stock market became my full-time job.

One of the more common questions I get from native investors here who aren’t as well-versed in the international market is why such large portions of my portfolio, and hundreds of thousands of dollars are invested in something called “REITs” – which by the way, most of them have never heard of.

Now, I don’t need to go through what a REIT is – we have resources and far better articles for that.

But I often explain exactly that to other people here in Europe – the latest time was dinner only 2 weeks back.

Europe only has limited exposure to the concept – Sweden has none. the structure doesn’t exist here. I myself only had limited knowledge of the concept prior to 2013, but when I started to understand it more, I became interested very quickly and started studying.

Why REITs?

The reasons to invest in REITs are something we cover quite often here. The simple fact is that REITs have historical trends that are extremely favorable, and there are very few reasons to expect that there will be a material, broad-based difference going forward.

On a historical basis, REITs on general basis have delivered competitive total returns due to among other things high and steady dividend incomes, and long-term capital appreciation.

This is only part of it though.

Because what’s equally excellent is the low correlation with other assets, which serves as a portfolio diversified and reduces overall risk and beta. Another thing is what I see as the relative dividend safety even in the face of temporary adversity. This is not unique for REITs – just because a company drops for a long time, doesn’t mean the dividend will be cut – but high-quality REITs have incredible dividend safety, and even in the case of a temporary reduction, usually goes right back up – see Simon Property Group (SPG).

A REIT investment is a total return investment – but the strong dividend incomes they offer make them important for people who rely on strong income generation – such as retirees and retirement savers. Through REIT investments, achieving a “safe” 4-5% yield is a lot simpler than say, doing the same through blue-chip non-REIT stocks. Or, at the very least, this can be a component in such a portfolio.

REITs (Passive Investing)

REITs, while almost unknown in Europe, is the third-largest asset class in the US investment market. It’s 39% bonds, 41% equities, and 15% commercial real estate (and 5% cash).

The dividends from REITs are, as you know, provided by a safe stream of contractual rent payments from tenants in their properties. While there is a possibility of decline or issues here, you must realize that the safer of these REIT subsectors – such as the Residential Apartment/House subsector, have contractual stability that goes beyond that of most companies – and therefore dividend stability on the same level.

There are REITs with plenty of more volatility. B-mall type REITs, Office REITs, Mortgage REITs – there are plenty. But that’s the good thing.

Being a member of iREIT, you get the “best of the best”, and you can choose what sort of risk exposure you’re looking for.

A common misconception is that REITs decline when interest rates rise, or somehow do poorly. This is false, even if we’ve seen some of the opposite for this time around.

Historically speaking, REITs tend to outperform during higher interest rates, the reason being that higher interest rates typically coincide with a growing economy which in turn increases the underlying value of the assets that make up most REITs – real estate. That’s why REITs don’t outperform, typically, during periods of economic slowdown.

The relationship between REITs and interest rates is typically one of positive correlation – in that they move in the same direction. This is bolstered by arguments and data from most periods studied, including six periods starting in the 1970s.

This time around it’s slightly different, as you may have noticed. Interest rates go up while REITs have tended to underperform a bit. Why?

Because this period of rising rates coincides with potential/expected economic slowdown and tightening, which is atypical – but necessary, given how the market and the data as well as interest rates are looking. There’s a lot of fear, but also a lot of data that exposes some of the weaker or more volatile sectors – such as Office, Mortgage, or others.

But safe REITs are not in any way spared either. Residential REITs like AvalonBay (AVB) and Essex (ESS) are down 33% and 38% for the 1-year period. Typically, this implies massive instability and lack of safety in a REIT like this – but anyone who believes that any of these companies will have fundamental difficulties should take another look at those fundamentals.

Because they’re solid, I consider them to be about as likely to fall as a non-REIT blue-chip stock with a 40-year dividend tradition.

Why am I Upsizing my REIT allocation by 100%?

As I said, I typically have a 10-15% sector target allocation. For REITs/real estate, I’m currently at 12.5%.

Upsizing would therefore imply a 25-30% allocation target, and that’s what I’m confirming here for 2023.

Question: Why haven’t I done this yet?

Answer: FX has been absolutely horrible. We’ve been looking at SEK/USD EUR/USD pairings that, for buying dollars, have been some of the highest in 10+ years. While I tend to ignore most FX and consider it more at a normalized currency level, I will neither ignore extreme ups nor extreme downs, but instead, shift allocation to non-USD currencies, or heavily towards USD currencies during times of respective extremes.

It’s therefore not just that I’ve under-allocated REITs, my USD exposure is down 4% on an annual basis despite the positive FX because most of my investable capital of 2022 has gone to non-US investments. I’ve been pushing SEK, NOK, DKK, and EUR as well as GBP above USD.

Question: Why am I doing, or planning to do it now?

Answer: A few reasons. First off, valuations for these companies that I follow are currently so low that even on a higher FX basis, the upside in the case of normalization is significant. Furthermore, we’ve seen FX pairings drop slightly, which makes this a better play now than what it was 2-5 months back.

So, both the valuation and the FX going into early 2023 is far better.

None of the companies and REITs I’m pushing into here or considering adding to are in any way materially unsafe investments. Some of the REITs that I’m considering in the office sector have gone down as much as 45% – and I view such declines as unjustified given the sort of fundamentals they come at or the coverage ratios they’re working with in terms of dividends.

Which positions/REITs am I upsizing/going into?

Several.

I will say that I sometimes work in the speculative REIT sector, and even position myself bullishly for some of the names that have a bit higher than average risk exposure – but I always size my position in accordance with conservative risk management.

In this case, that means that over 90% of the REITs I buy are BBB+ rated, they have well-covered yields of 3.5% or above, and they have significant upsides.

I’ve covered Office REITs and Residentials, as well as a few mixed ones.

Here I’m giving you the top 5 REITs that I’m upsizing for 2023 – as long as their valuations stay tip-top.

1. AvalonBay/Essex

I’ve covered the companies before – recently – and I will continue to push them for as long as it takes until I have made all but certain that you know, and consider these investments for the long term.

Residentials are superb and solid. These companies are equally solid – conservatively leveraged, 3.5-4.2% current, well-covered yield, and an upside of at least 20% annually if we consider the premium anything close to valid – market-beating returns even if that’s not the case.

There is no real conservative downside to these investments, as I see it – that’s why they are at the top of my list.

I’m buying AvalonBay and Essex hand-over-fist for both of my private and corporate accounts, and my allocation targets are high – 2-3% for each of them, in both accounts.

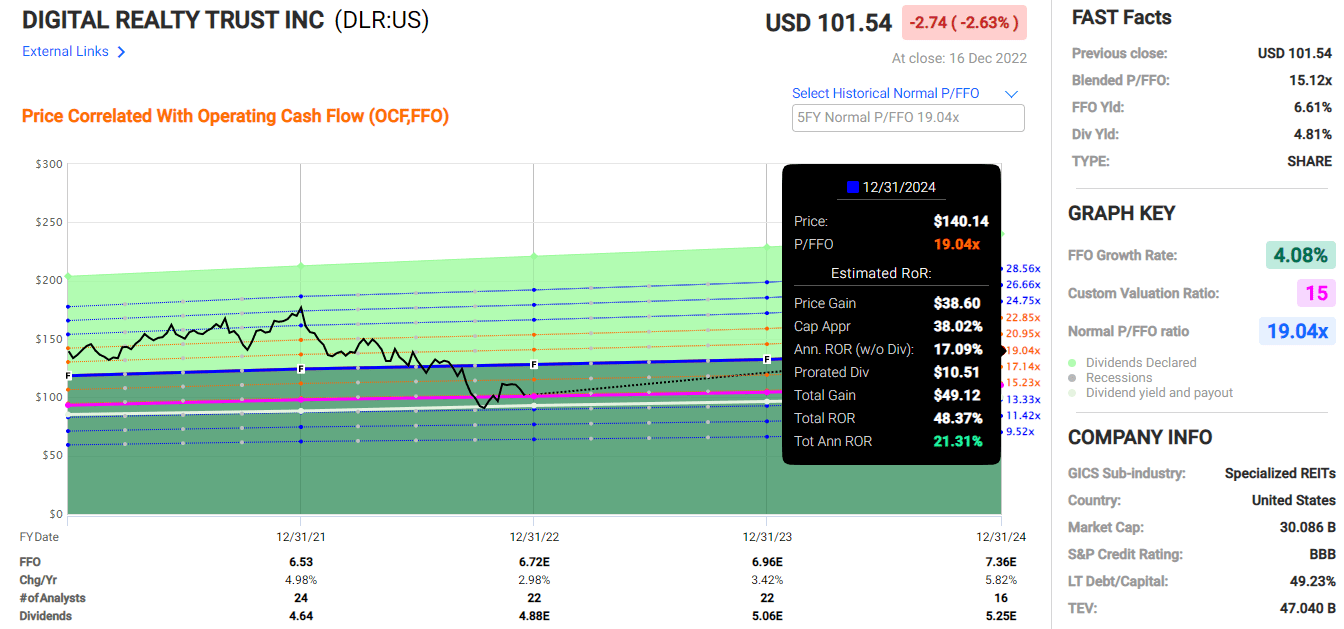

2. Digital Realty Trust (DLR)

DLR is my second choice. While I have been neutral on company for years at this point, I finally went positive a few months ago and opened my first position. I have been slowly filling it ever since, and at this valuation, I don’t think we can do anything wrong.

The company is currently trading close to 15x P/FFO, with a yield close to that elusive 5%. What’s more, the company is BBB rated, and the upside on 15-19x P/FFO is 9%-21% annualized – very much within the sort of market-beating returns that we’re looking for.

DLR Upside (F.A.S.T. Graphs)

The growth is going to be limited here – in fact, most of the FFO growth in these companies I’m mentioning here isn’t above 4-5%. There are REITs with good growth and expected growth, but these ones aren’t that.

That’s okay for me – we have safety and value instead.

Take a look at the next one.

3. Boston Properties (BXP)

Feel free to tell me how the office market is declining across the nation, and how occupancies are slowly sinking. How the FFO is slowly declining. Because you’re right – these next 3 companies that I’m telling you I’m buying are Office REITs.

However, at the same time, I will tell you that Boston Properties is BBB+ rated, with a yield close to 6% despite trading at no more than 9x P/FFO. This implies that the dividend is conservative in the first place – which is entirely true – and that the company safety here is massive.

Again, this is also true.

The upside, even if the company doesn’t touch double-digit multiples until 2024E, is still 8.5% annualized RoR until that time. At any recovery to 10-19x /FFO, with 19x being the 5-year premium. The company might not get back there in the near term, nor the 48.46% annualized RoR that would entail under current forecasts, but at the 8-46% range on an annualized basis, you’re extremely protected in terms of downside based on these fundamentals.

That’s why I want at least 1.5-2% in BXP until the end of 2023.

4. Highwoods Properties (HIW)

Now, the advantage with Highwoods is generally lower overall multiples than BXP. The premium (or discount) is close to 13x P/FFO, the current valuation is closer to 7x, and the yield is higher – almost 7.2%.

However, HIW is BBB, in terms of FFO, the payout isn’t in any sort of danger, and HIW has some of the most solid asset portfolios out there.

This is a very similar thesis to BXP – it’s undervalued quality with very little of a downside, even on a forward 7.5x P/FFO.

The upside range here, from 7.5x to 13.1x is 11% to 40.5%. That means the upside is higher on the lowest point, but lower on the highest point – but the highest point is also significantly lower – below 15x P/FFO.

So, Highwoods is my fourth choice – but it’s still definitely as solid as BXP.

Are there headwinds? Yes, of course.

Do they justify an over-40% drop in the company’s valuation, and essentially trading like dirt?

No, don’t make me laugh.

I’m targeting 1.5-2% in HIW until the year-end of 2023.

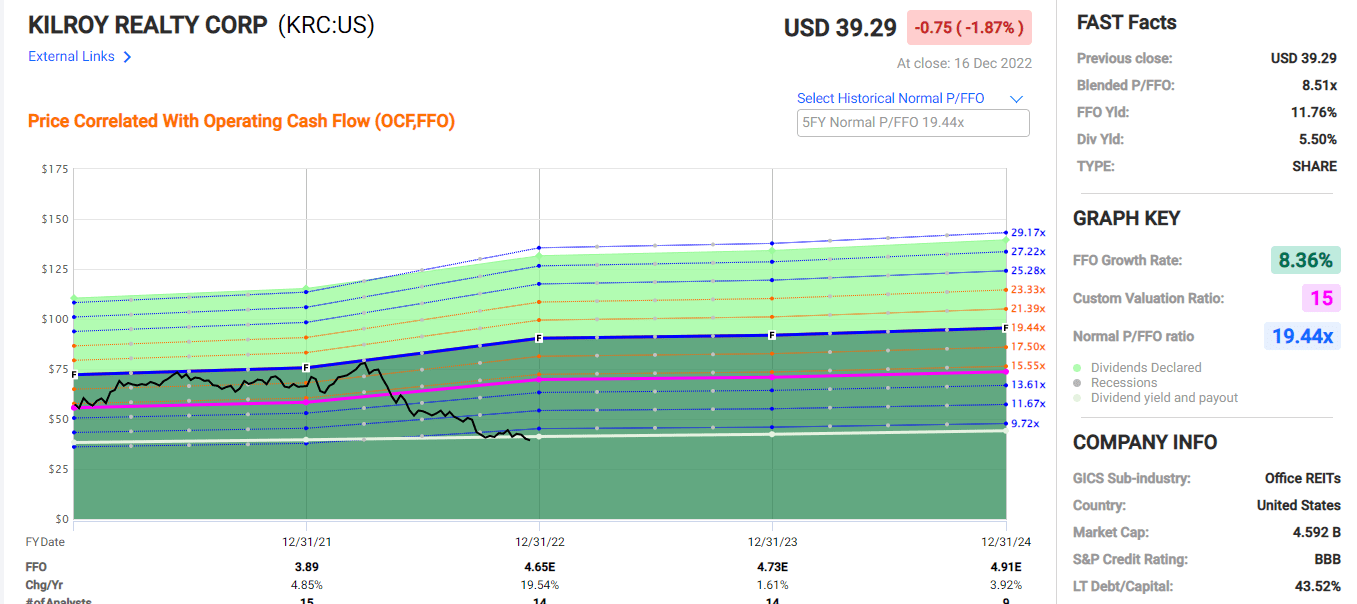

5. Kilroy Realty Corporation (KRC)

The last on this list is an office REIT as well – BBB rated like the others, a good yield of over 5.5%, and it has the highest valuation range – meaning its current valuation is the lowest relative to its 5-year P/FFO average.

What’s more, the current forecast for the company’s next few years is positive – no declines are forecasted at this time.

F.A.S.T. Graphs KRC upside (F.A.S.T. Graphs)

Again – yes there are headwinds in the space. These headwinds are not likely to disappear anytime soon, but these headwinds are also exaggerated when looking at this valuation. It’s ridiculous – 8.5x for this company?

That’s not something I can agree with.

The lowest 9.2x P/FFO gives us an upside of 15% here – so the lowest forecast on the range gives us the highest upside of all these three REITs – with the higher-end upside being around 58% for the 19.44x.

The company was valued at over 19x less than 9 months ago.

Will it revert back in 9 months?

I don’t believe that’s the case – but I do believe your downside to be protected here. Enough so that I’m going in heavy-handed here for the next year.

My target for Kilroy is a 1.5-2% allocation here.

Which positions am I not going into/upsizing?

At the same time, you may ask yourself why I’m not buying certain other stocks – so here is my list of the companies I’m not targeting to expand at this time.

What’s more important, is the reasons for it.

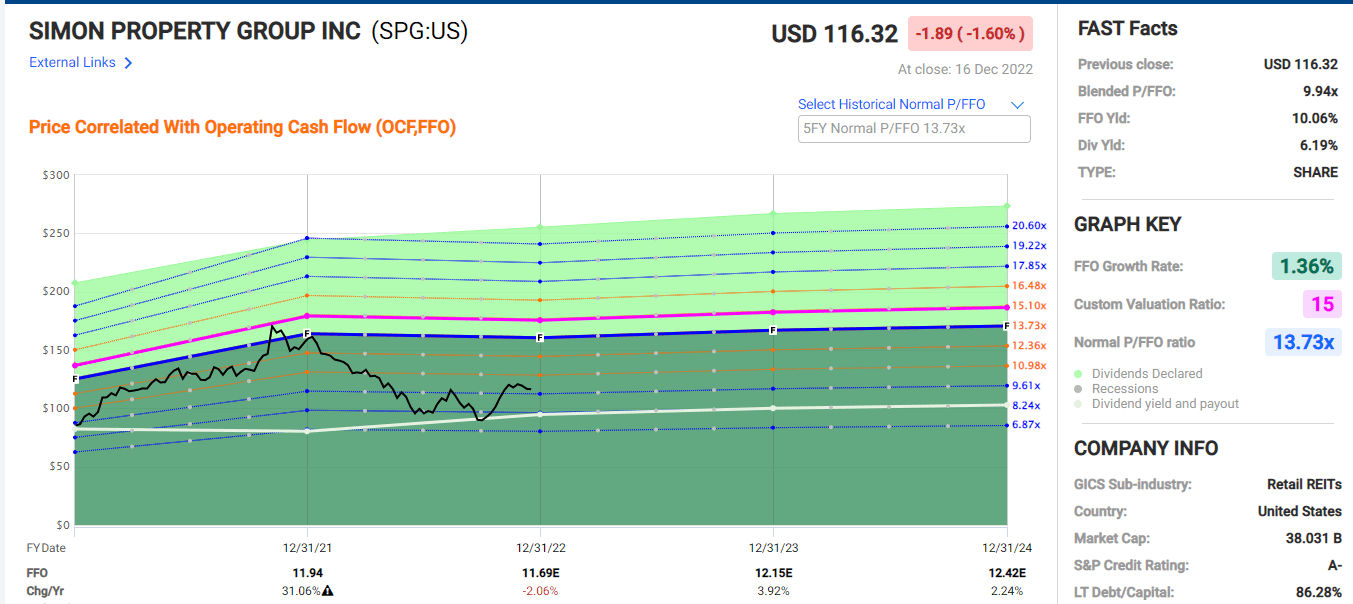

1. Simon Property Group (SPG)

Surely you ask yourself why I’m not pushing capital into SPG. It’s an undervalued, A-rated quality REIT with a 6.2% yield that’s still trading below 10x at this time.

And the upside is most certainly there.

F.A.S.T. Graphs SPG valuation (F.A.S.T. Graphs)

However, the reason I’m not taking advantage of this opportunity is very simple.

I’m already overexposed. SPG is 5.8% of my private portfolio with a cost basis of below $80/share. This is an investment where I’m “waiting for the pop”, so to speak, and just enjoying the returns in the meantime. SPG is safe, I’m not selling until it hits over €$160, which is where I sold about 30% of my original position, and I’m happy to hold till then.

That’s why no Simon Property Group.

2. Realty Income Corp (O)

Maybe even more of a question – why not more Realty Income? Monthly dividends are not a bad valuation at all at this time with a 20% annualized upside to the premium 20x P/FFO.

So, why not more O at 16x average P/FFO, and a 4.7% annual yield?

Same reason as with SPG – but with O, I’m even more overexposed – I’m in at 6% in my private, and 8% at my corporate portfolio. Both of these positions are significantly in the green – and I won’t touch the “SELL” button until we’re above $90/share.

If you are not overly long for these two REITs, then they should also be on your list of considerations.

Wrapping Up

So, there are REITs that are “BUY” today even here on IREIT that come in at significantly higher yields. But you will notice the conservative quality of all of these companies. Investment grading, dividend safety, and history, all things that I value.

It’s all about risk tolerance, of course.

Most people when their net worth and their portfolio sizes increase, increase their risk tolerance, lever and dial up the risk and take on more yield but higher uncertainty.

Me, I’ve been doing the exact opposite.

As things have gone higher, my portfolio has gone up, I’ve been lowering my risk basis. At this time, I have 8 investments in my portfolio with yields of less than 2%. 5 years ago, the same number was zero.

Today, every investment I make is vetted not only in terms of the basics and long-term, but I also try to look at the potential for how it goes in the medium term and how instability would impact my overall portfolio development.

5 years ago, I would take on 8-10% in a single company.

Today, that limit is 5%, with a preference for 3%.

If my YoC was the same as it was 5 years ago, my annual income from dividends would be 32% higher today.

But I would also be owning significant instability and volatility – if you go back and look at some of my investments and articles way back when you’ll see that the mix of companies I wrote about and invested in was different – at least some of them. Even the EU ones.

My entire strategy was a bit different back then. 5 years ago, the idea of selling certain companies wasn’t on my list. I was the pure-bred “Buy-and-hold-forever” investor.

That’s not me anymore.

Every company I have has a Trim/divestment target – and I’m no stranger to rotating, trimming, and optimizing.

My portfolio back in 2014-2015 was solid.

My portfolio now? That one’s much better.

And unlike you might expect, it doesn’t matter all that much the specific companies that are part of that portfolio, or the allocation that these companies have. At this point, you’re not able to “BUY” most of the companies I have allocated to, at the prices I paid, which makes most of what I have irrelevant to your own goals – because the theses for them are no longer there, or as good as they were when I pulled the trigger.

Be forward-thinking. What matters aren’t company specifics that I bought a year ago, or two. Those companies may be in the green for me now, but the opportunities are gone. What matters is specific allocation targets, and what companies I go for now.

That’s what I focus on in these articles – what matters now.

And these are my 2023 REIT targets.

Questions? Let me know!

Be the first to comment