alexsl

Co-produced with Beyond Saving.

When I talk to my friends and family, they often talk about their homes.

It makes sense in many respects for that to be on the forefront of one’s mind. A home is where most of us live, it requires frequent work to keep it clean, tidy, and repaired. It should be little surprise that the largest single investment the average person makes in their lives is their home. For most people, that means taking out a mortgage, which is usually their largest loan.

Mortgages are often the largest monthly expense of a consumer, and the first priority to get paid, often closely followed by a car note or utilities. These essentials or basic needs enable us to work and live, thus they get our focus.

Many retail investors don’t realize they can go out and own the mortgages of others – or perhaps their own mortgage!

When a bank creates a mortgage, it is usually sold. Mortgages are bundled together in a package called a mortgage-backed security (“MBS”) and sold in pieces to investors. This allows banks to recycle their capital effectively, while also enabling more mortgages to be created. You can go to your brokerage accounts fixed income area and buy them yourself.

MBS come in two distinct types: “agency” and non-agency. Agency mortgages have a principal guarantee, while non-agency has no guarantees at all. With recession risk rising, I greatly prefer agency MBS today.

Today, I want to talk about one of my favorite vehicles to invest in Agency MBS on a leveraged basis.

My Favorite Agency Mortgage REIT

Annaly Capital Management, Inc. (NYSE:NLY) yields 16% and is in the business of owning residential mortgages. Specifically, NLY buys “agency” mortgage-backed securities. These mortgages come with a guarantee from Fannie Mae or Freddie Mac. If a borrower defaults, the agency buys back the mortgage at par.

Due to this guarantee, agency MBS prices tend to correlate strongly with U.S. Treasuries. Owners of agency MBS are predominantly banks, insurance companies, governments, and the U.S. Federal Reserve. These very conservative institutions buy them because they are seen as having no credit risk.

Agency MBS are viewed as minimal risk and are accepted as collateral in the overnight “repo” market. This market is where institutions go when they need cash or when they have excess cash. Your bank doesn’t know how much money you will spend today. It doesn’t know when you will write a big check or make a large withdrawal or wire transfer. Yet, in today’s world, when you transfer $50,000 from your checking account, the bank will process that quickly.

Banks must have cash available on short order to fulfill whatever requests come in. You aren’t going to be pleased if you request a transfer and your bank says, “Yeah, we don’t have the cash. We’ll do this next week.” That would cause a panic, and cause everyone who hears about it to rush to their bank to withdraw cash – causing a good old-fashioned “bank run.”

So a bank must have access to enough cash to satisfy any withdrawal request, even if the volume is well above average. On the other hand, cash sitting around doesn’t earn much of a return. Banks want you to deposit cash so they can lend it out at a higher interest rate than they are paying you.

How does the system find balance? The overnight repo market. This is a market that the Federal Reserve has become intricately involved in, frequently borrowing or lending money. The overnight repo market is where institutions go to settle up whatever cash needs they have for the day. Banks that need cash go there to borrow, banks with excess cash go there to lend, and the Federal Reserve frequently steps in to make up for any imbalance. Of course, banks aren’t going to make unsecured loans. All these loans take place as “repos”; the lender buys U.S. Treasuries or Agency MBS from the borrower, agreeing to sell them back at a specified later date.

This system allows banks to buy long-term Treasuries and agency MBS, receiving a higher yield while also knowing they can access cash whenever they need it through the overnight repo market.

What does all this have to do with NLY? NLY buys agency MBS for investment purposes, and since the asset itself has no credit risk, NLY can obtain very high levels of leverage at low-interest rates through the repo markets.

While there is no credit risk – if a borrower defaults, NLY will receive par value – there is interest rate risk. NLY frequently is leveraged from 7x to 11x equity. When you are leveraged that much, even small price movements can have a meaningful impact on book value.

To hedge against that risk, NLY buys agency MBS and shorts U.S. Treasuries. Since both have zero credit risk, the two assets usually correlate. So by being long MBS and shorting U.S. Treasuries, the gains from the short position help offset any losses from the long position.

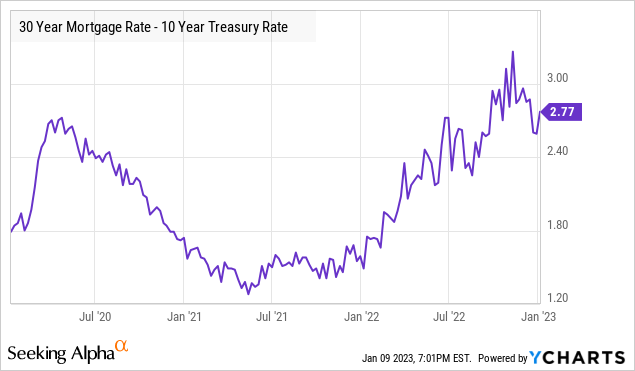

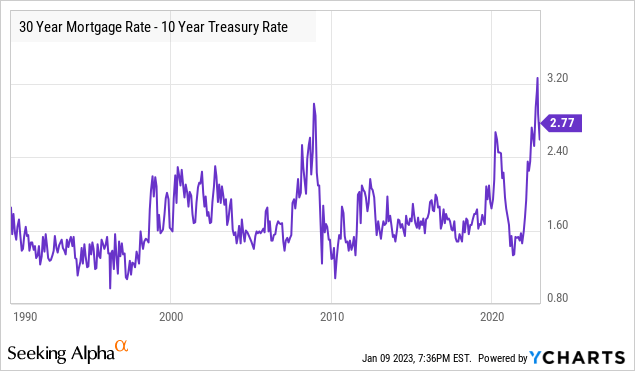

In 2022, that strategy didn’t work out so well. NLY’s losses from MBS prices falling significantly exceeded NLY’s gains from its short positions. The reason is that mortgage rates went up far more than Treasury rates. Here is a look at the spread:

The higher this spread, the lower NLY’s book value. It peaked in early November and has started falling, but is still at levels not seen since March 2020. This spread is the driver of NLY’s fall in book value, and the share price has followed.

Yet these losses are unrealized. While MBS prices have fallen, NLY increased the par value of its agency MBS holdings from Q2 to Q3 2022 by approximately $10 billion. With leverage at only 7.1x at the end of Q3, NLY has ample room to leverage up more.

Meanwhile, the spread between mortgage rates and Treasury rates is reverting to the mean. Historically, these large spikes have not lasted long. This spike in the spread was the highest in modern history, exceeding both the COVID turmoil and the Great Financial Crisis (“GFC”).

As this spread declines, NLY’s book value will rise. More importantly, as NLY leverages up at elevated rates, NLY’s cash flow will increase. Yields on mortgages are very high relative to NLY’s cost of funds. After accounting for hedging costs, NLY’s forward returns on MBS purchases are higher than they have ever been since the company went public.

While there is the risk that something happens that causes the spread to widen again and puts more pressure on NLY’s book value, the historical experience is that these wide spreads are not maintained for long and it certainly appears that the current strength in the MBS market is sustainable. After all, many institutions are looking to MBS as an alternative to Treasuries. If this spread tightens as it did during the GFC and following COVID, it will create a substantial upside for NLY’s price. If the spread remains wide, it will be a significant driver of higher earnings and dividends.

Shutterstock

Conclusion

Are you worried about a recession? Worried about the ability of companies to survive higher interest rates? Worried about defaults?

What if you could own an investment that gets PAR value for its investments back, even if the debtor doesn’t pay and goes bankrupt? Sounds like a great idea when the economy is slowing and weakening, doesn’t it?

NLY’s positions are guaranteed by the agencies and its debtors are vast in number. Your neighbor, or even yourself, might be a debtor to NLY’s vast MBS holdings.

These reasons are why MBS are considered exceptionally low-risk investments. They are highly diversified and backed by a governmental guarantee.

So when it comes to your retirement, your income stream, and your risk tolerance, you should prepare for a recession by looking for income from sources that get paid in a place of high priority.

Mortgages are such a place.

That’s the beauty of being an income investor, your friends and family are paying your bill without you having to collect it from them directly.

Be the first to comment