AzmanJaka/E+ via Getty Images

I maintain two 25-position, equal-weight dividend growth portfolios for my personal investing goals, one with an offensive orientation (my “Ultra High DGI” portfolio) and one with a defensive orientation (my “Defensive DGI” portfolio). Each portfolio has been painstakingly constructed and backtested to maximize risk-adjusted returns and dividend growth based on its respective aim, with the defensive portfolio seeking to minimize drawdowns during difficult periods and thus be as “recession-proof” as possible, and the offensive portfolio seeking to maximize long-term dividend and capital growth. This article marks the second entry in two series examining the holdings of each portfolio.

WM: Economically Sensitive But Essential

Waste Management (NYSE:WM) has been a favourite stock of dividend growth investors for years, and I view waste management as perhaps the least vulnerable utility-like industry to existential disruption by future technologies. Regardless of how much of our trash is able to be recycled or not, someone will always need to collect it, process it, and dispose of it. Solid waste management is estimated to grow at a 3% CAGR globally from 2023-2035, and while recycling prices can fluctuate wildly and pressure margins, new recycling, waste processing, and energy production technologies may present trash companies with future growth opportunities as well.

Waste Management’s revenues and earnings have risen sharply over the years as it has grown via acquisitions into the largest US company in its industry, but that doesn’t mean it hasn’t had its share of ups and downs. A look at its historical revenues below shows that its revenues may indeed be at a peak heading into a likely recession in 2023, with its 2009 year-end revenue (and earnings) having fallen about 15% from their 2008 levels.

WM Historical Revenue (companiesmarketcap.com)

Valuation

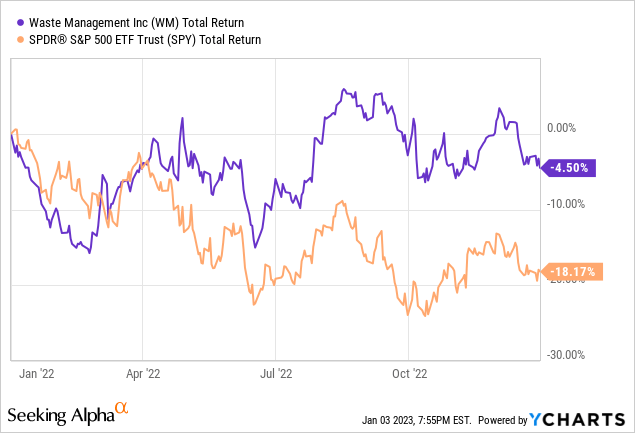

Current economic indicators show that this year’s recession may be far milder than the Great Recession and the retail sector hasn’t blinked yet, but I still think it is wise to treat waste management stocks with caution at current levels given their historic sensitivity to recessionary environments. WM has performed quite well since recovering from its COVID selloff in 2020 and served as a relative safe haven over the past year in the face of inflation and rapid rate hikes.

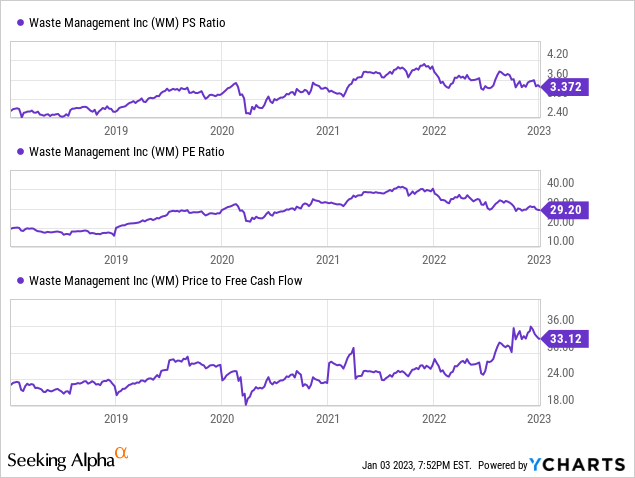

Given the size and essential nature of its business, it’s no surprise that when we zoom out to a 5-year chart, WM’s current valuation appears quite high on a PS, PE, and Price to Cash Flow basis. It’s not quite as expensive as it was a year ago, but still trading at a significant premium to its 5-year averages.

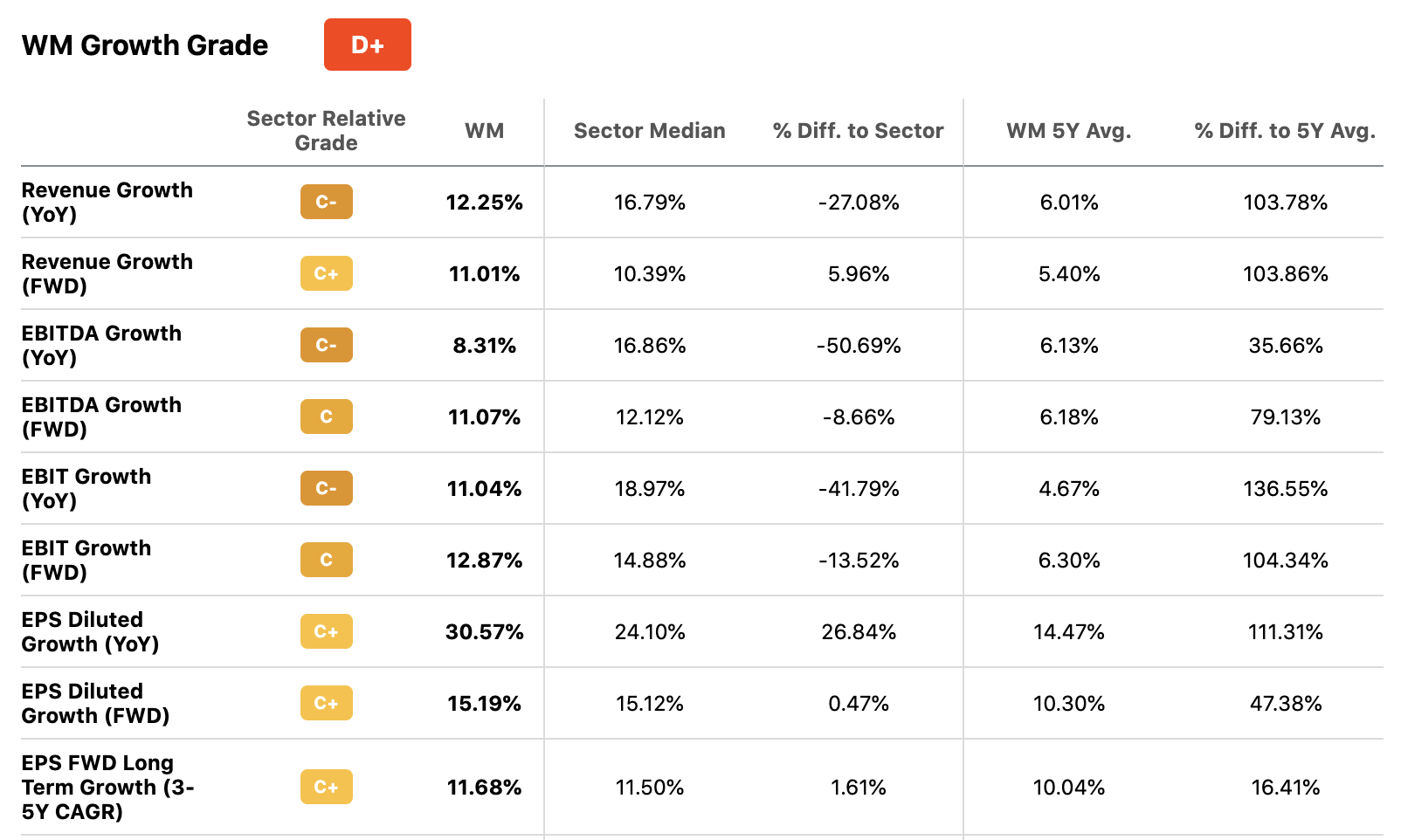

Looking closer, we can see that WM’s current valuation premium is also due to its significantly higher-than-average revenue and EPS growth rates in 2023 as well as optimistic forward estimates of 11% revenue and long-term EPS growth.

Seeking Alpha

Balancing its current explosive growth and rosy outlook with the likelihood that forward revenue and earnings estimates for the waste management sector may darken in the coming 2-3 quarters if economic indicators begin to show more signs of recession, I view WM as approximately 5% overvalued at its current $157 share price. This is supported by its 5-year comparison as well, where it is overvalued on PS, PE, and cash flow metrics but undervalued on forward earnings and growth metrics.

WM Current Valuation (Morningstar)

Dividend Strength

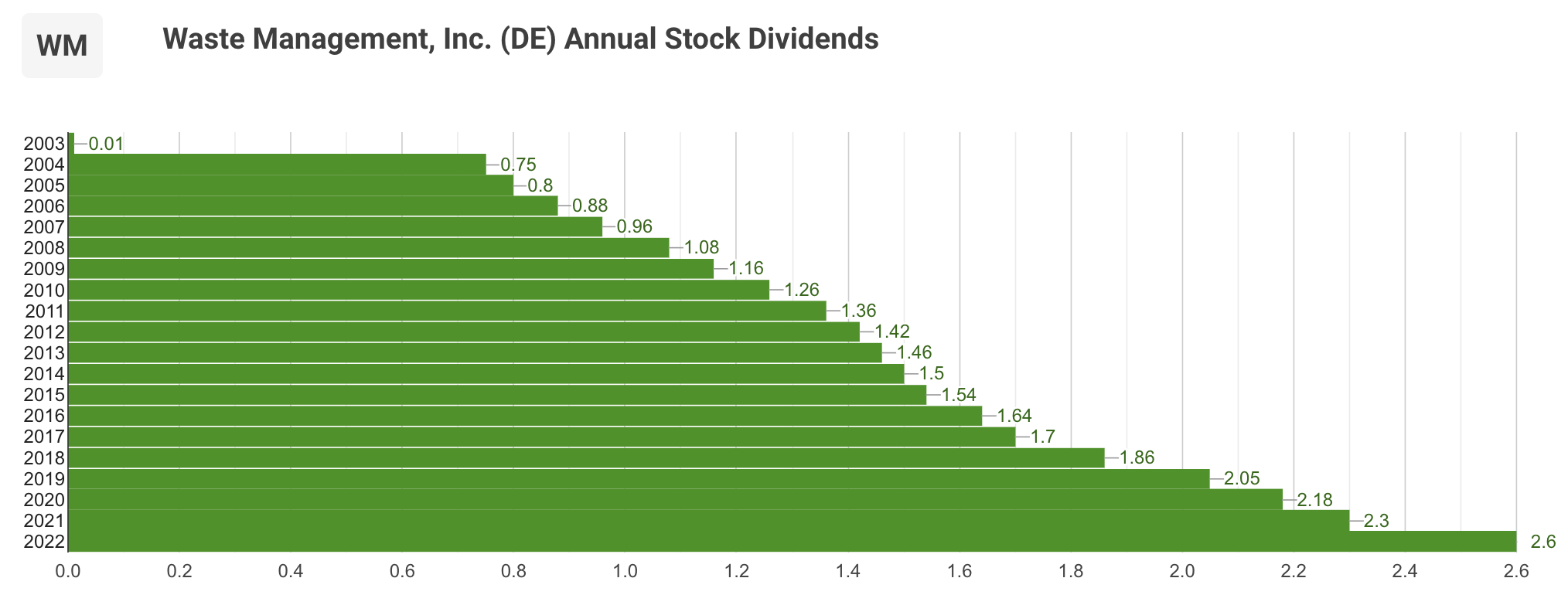

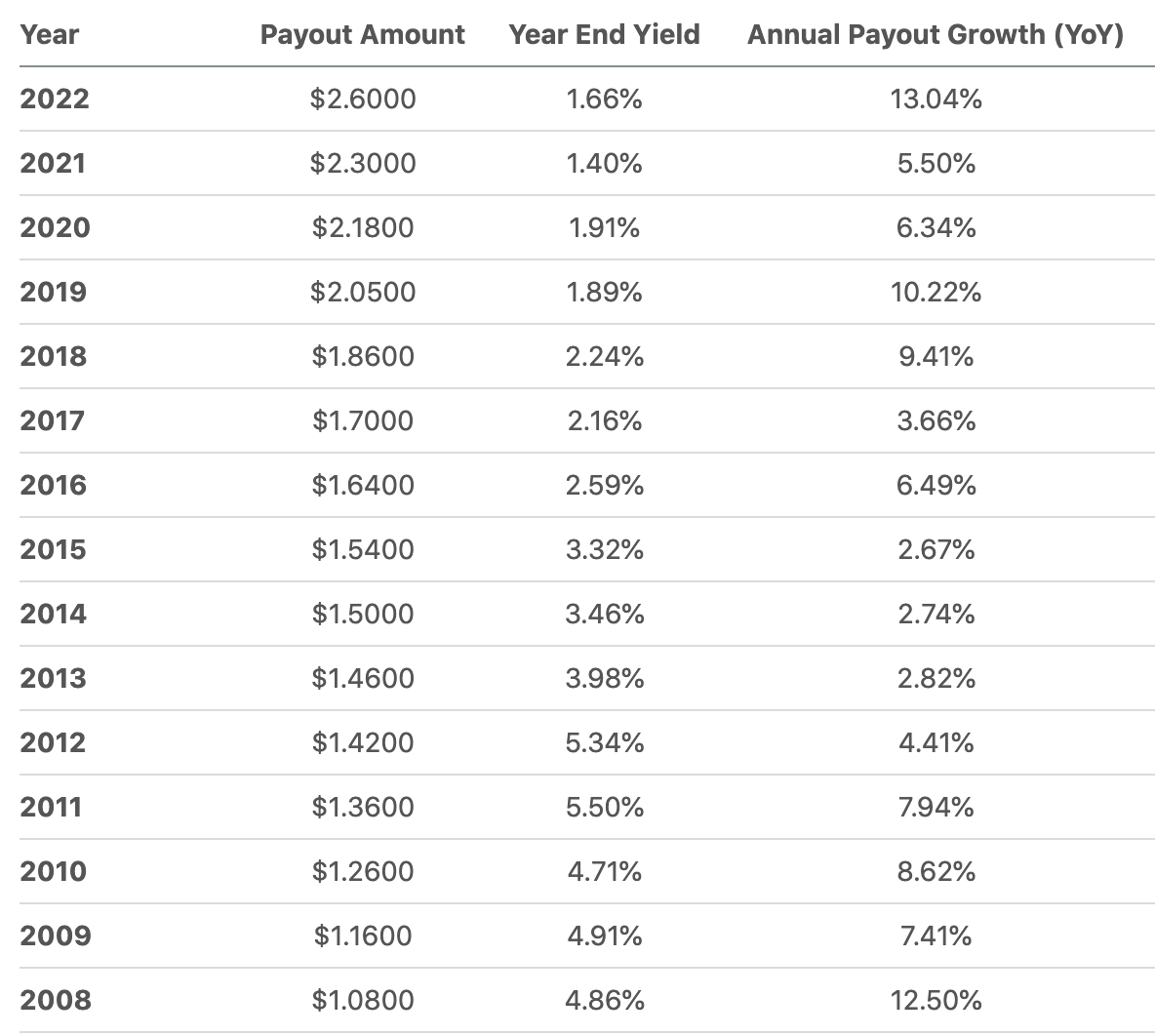

Because I intend to hold this portfolio until my wife and I retire in 20+ years, I take a long-term view of the dividend growth potential in each of the stocks we hold. Fortunately, Waste Management has a 19-year record of dividend growth to consider.

dividendinvestor.com

When looking at dividend visualisations like the above, ideally I hope to see an exponential payout curve where the annual growth rate or CAGR is either held at a constant percentage or increases over time. Neither of these are true in WM’s case as we can see that its dividend CAGR has fluctuated over time, so instead I look to see how the current dividend trend compares to its overall history.

This paints a better picture, since we can see that WM’s dividend growth rate has sped up significantly since 2018 after a much slower period from 2012-2017 where annual hikes mostly hovered around a paltry 3%. Had its dividend CAGR remained at those levels, it would not be strong enough to qualify for my Defensive DGI portfolio, as I generally require a minimum of 5% long-term dividend growth per stock.

In the past five years, however, WM’s raises have ranged from a low of 5.5% during peak-COVID lockdowns to a relatively massive 13% in 2022, with the most recent dividend boost for 2023 clocking in at a healthy 7.7%. As mentioned above, their current 11% forward revenue and earnings growth estimates more than support the company’s ability to maintain at least a 5-6% dividend growth CAGR in future years, and potentially for them to continue hikes in the 7-8% range if the Fed can indeed achieve a soft economic landing. So for now they are not only safe in my book, but are doing better than most waste management and utility stocks in terms of recent dividend growth.

WM Historical Yield (Seeking Alpha)

While traditional utilities often pay higher dividends and target payout ratios in the 60-80% range, waste management stocks (these days at least) pay lower dividends and typically target payout ratios in the 25-50% range, as a significant part of their growth strategy relies on acquiring smaller competitors and earnings tend to fluctuate more, necessitating more earnings headroom to maintain their dividend growth streak. WM sits at the upper end of this payout range at 45.5%, which is mostly in line with its closest peer Republic Services, Inc.’s (RSG) payout ratio of 38.9% given that WM’s current yield of 1.66% is also about 7% greater than RSG’s 1.54% yield.

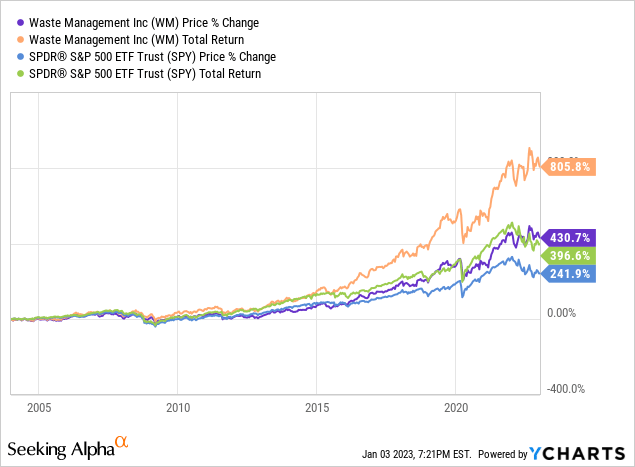

Of course, such a small yield doesn’t contribute much to total gains in the short term, but over a long-term holding period we can see how WM has become a top-tier wealth compounder. Reinvesting its dividends since its dividend growth streak began would have nearly doubled an investor’s returns and trounced the S&P. Don’t discount the power of trash!

Conclusion

As the largest player in the essential trash industry and a blue-chip dividend growth stock, I view Waste Management as an easy hold at current levels considering that shares are trading right in the middle of the $140-175 range they have bounced between since mid-2021.

WM may be at peak revenue and earnings in this cycle, but its recent large dividend hikes totalling 20% over the past two years show me that management is confident the company can weather a potentially difficult economic environment in 2023 and beyond.

In light of its ~15% annual revenue and earnings decline during the last major recession in 2009, and considering that it is already 10% off its all-time high, I view WM as 5% overvalued at its current price of $157. As such, I would be comfortable adding shares below $150 and would rate the stock a strong buy below $140, or 10% below the current share price.

Be the first to comment