arekmalang/iStock via Getty Images

The Federal Reserve appears to be doing a good job in tightening up on monetary growth.

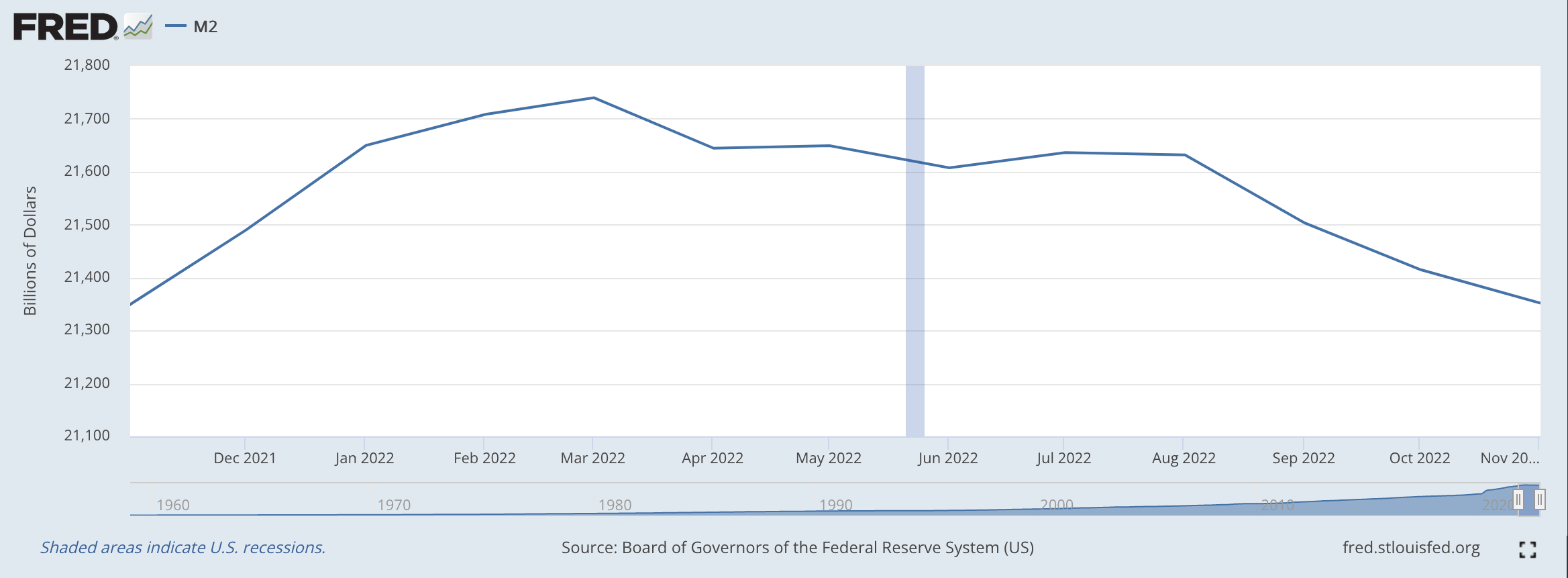

The November numbers on the M2 money stock indicate that the year-over-year rate of growth of M2 was 1.1 percent.

This is down from a 1.3 percent year-over-year rate of increase in October and a 2.6 percent year-over-year rate of increase in September

Take a look at the chart.

M2 Money Stock (Federal Reserve)

Given the Fed’s intent to continue on with its quantitative tightening, one can argue that the year-over-year rate of growth of the M2 money stock will turn negative for an extended period of time in 2023.

The Federal Reserve has tightened up its monetary policy!

The Recent Past

The Fed’s problem is dealing with the consequences of its actions over the previous two years as the Covid-19 pandemic spread throughout the United States and the subsequent recession that followed.

The Federal Reserve did just about everything it could to inflate the economy so as to avoid a major shutdown of the economy.

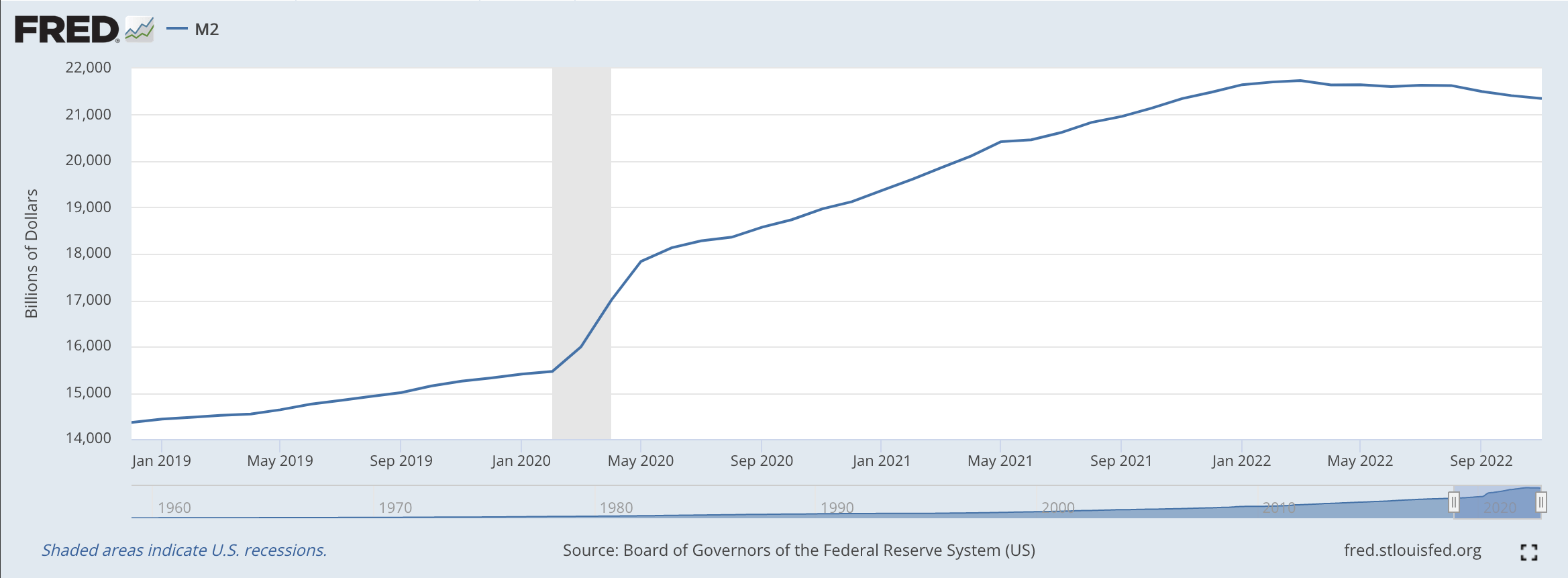

The Fed’s efforts can be shown in another chart going back into 2018.

M2 Money Stock (Federal Reserve)

In 2021, the Federal Reserve underwrote a 24.8 percent year-over-year increase in the M2 money stock, and in 2020 the year-over-year rate of increase was 12.4 percent.

In two years, the M2 money stock increased by almost 40.0 percent!!

No wonder there might be some inflation floating around in the economy.

Money Velocity

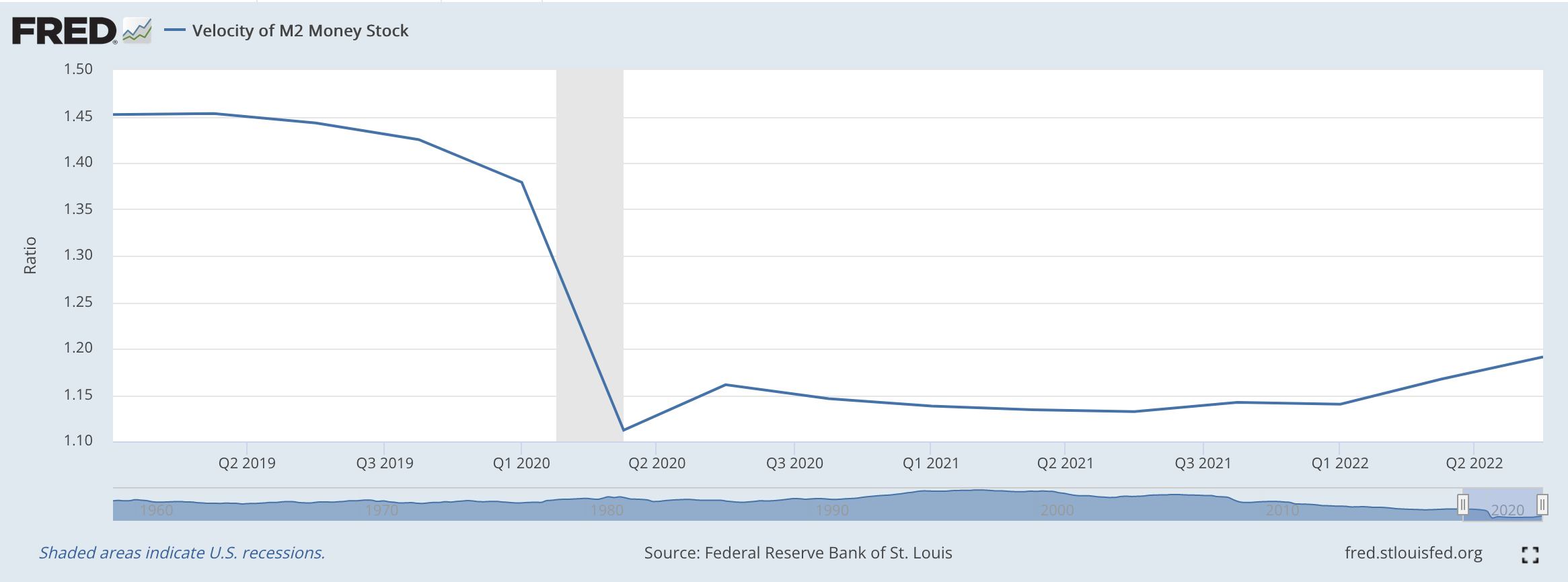

The question is, why didn’t the economy experience worse inflation during this time period, given the explosion of money into the economy?

Well, one reason was that the velocity of circulation of the money stock dropped during this time period and remained very low.

M2 Velocity of Circulation (Federal Reserve)

Where did this money go?

Well, I believe that the Federal Reserve created an asset bubble during this particular time, where money was flowing into different asset classes seeking high returns on their money.

This asset bubble included lots and lots of money flowing into the Cryptocurrency space and the SPAC (Special Purpose Acquisition Companies), as two examples. But, debt floated around all over the place and did not go into the “real” economy. I have written much about this phenomenon.

The velocity of circulation has not, so far, returned to previous levels.

In other words, people did not spend, or, “turn over” the money stock as fast as they had been doing before the Covid-19 pandemic hit.

There is one more thing I want to point out before we leave this subject.

The velocity of money had been declining in the United States for quite a few years before all this “Pandemic-stuff” took place.

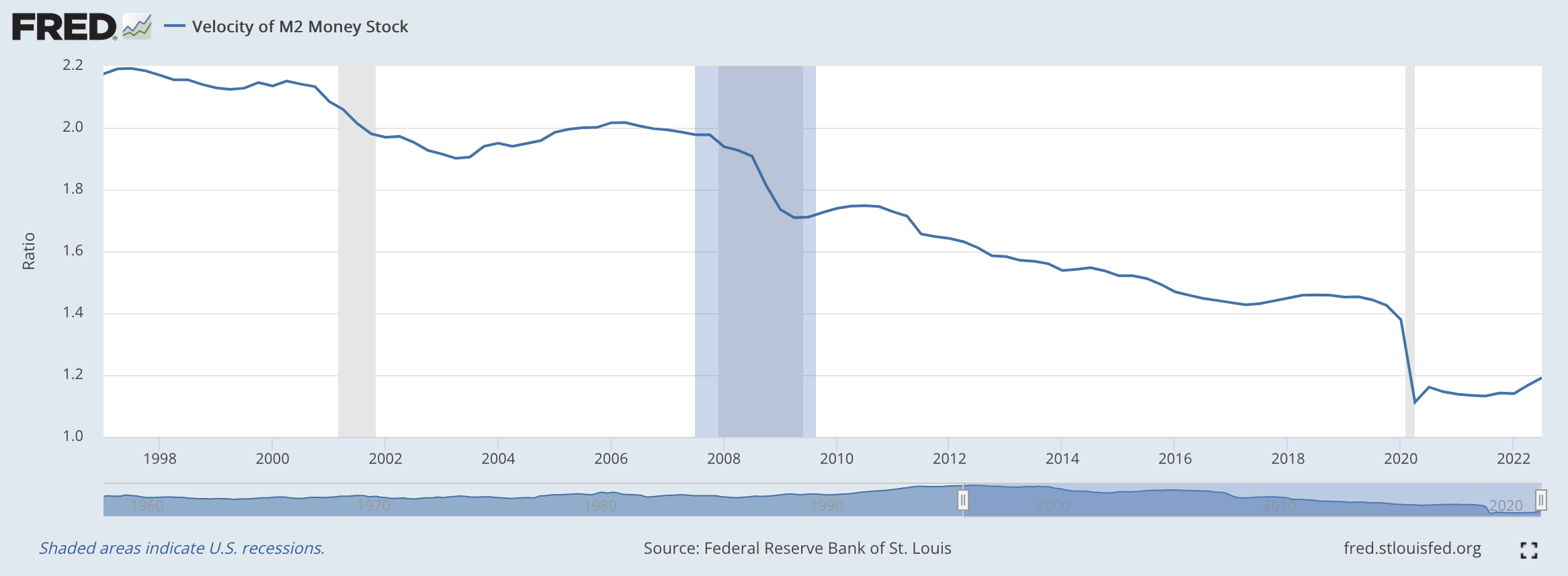

Check out this chart, for example.

Velocity of the M2 Money Stock (Federal Reserve)

Notice that the velocity of the M2 money stock has been declining since 1997.

This is consistent with all my research on the government’s economic policy I have called “credit inflation.”

In this policy, the government attempted to reduce unemployment further than “full employment” by using information from something called the “Phillips Curve.” The statistics associated with the Phillips Curve suggested to the government that a tradeoff existed between the unemployment rate and the rate of inflation.

A little more inflation could reduce unemployment by a little bit.

This, politicians believed, was worthwhile in pursuing, especially with elections coming up.

So, investors saw that the government was going to continuously support higher rates of inflation. This changed the investment equation, for now it could be seen that the government was supporting higher and higher asset prices, thereby reducing risk as well as providing higher returns.

So, investors put their money into assets rather than in helping corporations invest in real capital for improving production. Rising house prices provided better investment opportunities than helping a company by a new machine.

But, with money going into the financial circuit of the economy rather than into the real circuit, the velocity of circulation of the money stock dropped. And, as one can see, the velocity continued to drop during the 1990s, the 2000s, and the 2010s.

The experience of 2020 and 2021 just built upon what investors had learned over the previous thirty years.

The Consequences

The result of this type of behavior meant that movements in the money stock meant would not be as productive in stimulating the economy as it once had been.

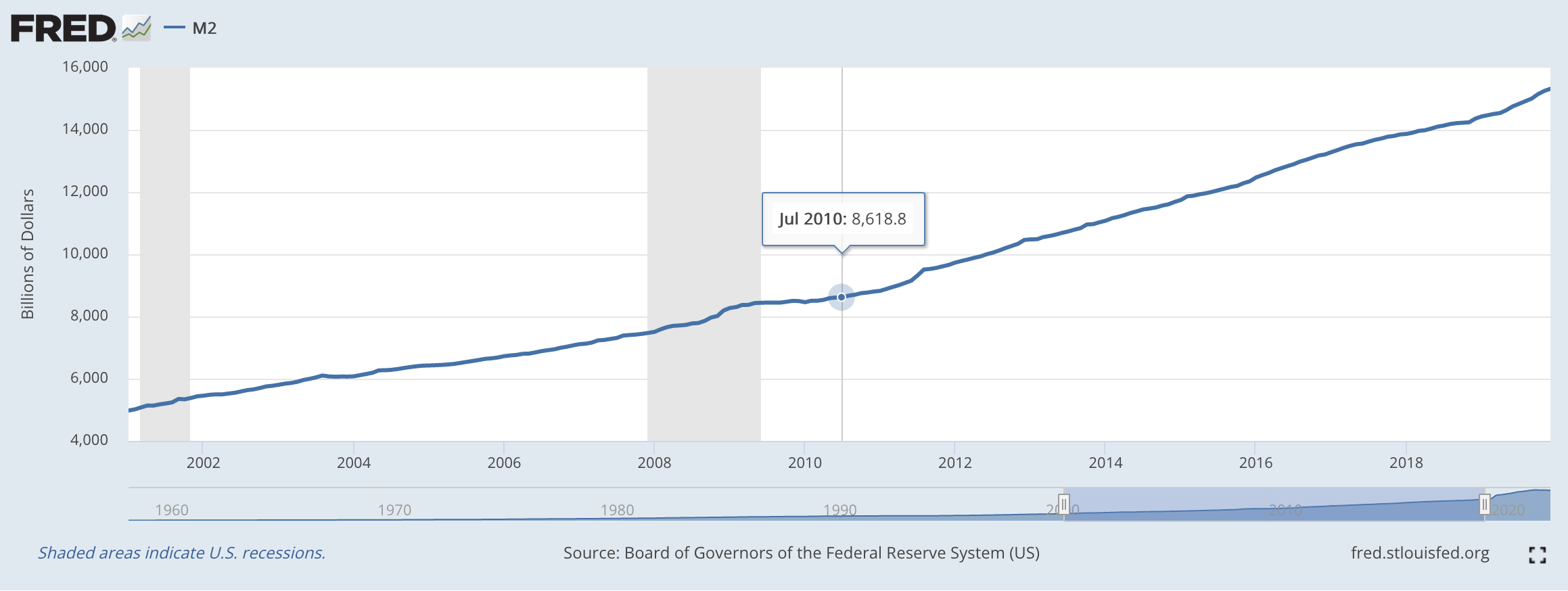

One can see that monetary policy was just aimed at providing a steady increase in the money stock during the first twenty years of the 21st century. That is, the money stock was just seen as a foundation for the economic growth of the country.

Money stock growth was not seen as something the policymakers wanted to play around with, moving the economy in one way or another.

M2 Money Stock (Federal Reserve)

Well, now the money stock is being impacted by the efforts of the Federal Reserve to control inflation.

And, the Federal Reserve seems to be causing the rate of growth of the M2 money stock to fall, heading for negative territory.

The M2 money stock is back in the news.

Hopefully, the Federal Reserve will achieve the results it wants.

If the Fed does achieve the results it wants, will the Federal Reserve move back to the policy of “credit inflation” that the government relied on before the current crisis?

Be the first to comment