Editor’s note: Seeking Alpha is proud to welcome Djamel Hagedorn as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

zeljkosantrac/E+ via Getty Images

A snapshot of the dilemma

Mo-BRUK S.A. (OTCPK:MBRFF) (WSE:MBR) is a Polish company founded in 1985, primarily active in the waste management industry in Poland. The company operates in three main areas: incineration of waste (~42% of revenues), solidification and stabilization of waste (~30%), and Refuse-Derived Fuels (RDF) production (~19%). There have been great past Seeking Alpha write-ups on the company that I recommend reading to gain a deeper understanding of the business, its market, and the opportunities it provides. While past publications are rather bullish, I would like to provide a perspective on why I am more hesitant and currently see too many question marks for my personal investment appetite.

At first glance, Mo-BRUK S.A. appears to be an exceptional business with extraordinary economics, which probably make it stand out on many stock screeners. It has a rare combination of impressive growth, almost unbelievable profitability (for the waste industry), a strong balance sheet, and a seemingly attractive valuation. Additionally, the future prospects seem very favorable due to a significant waste problem in Poland and the structural mid-term shortages, especially of the incineration capacity. This in combination with strict restrictions for EU countries regarding landfilling of all waste that is suitable for recycling from 2030 onward provides the entire sector with great future tailwinds.

So, what could be the catch and why isn’t the market appreciating this opportunity yet (the stock has been flat for two years now)?

Reasons for my hesitation

There are two possibilities as to why the market is not appreciating the company’s potential value: either the stock was indeed overlooked during this period or the market sees more risk in the company than what can be recognized in a quick screening process.

From my point of view, the first possibility is quite unlikely by now. Of course, Mo-BRUK is still a small-cap company operating in an emerging market and is not covered by many analysts or traded in high volumes compared to a S&P 500 stock. However, there are already a few analysts covering the stock and the trading liquidity also seems sufficient. Moreover, nowadays all types of investors have access to many tools to find and analyze potential hidden gems, so I think there must be more to it if a stock goes sideways for that long. Even the language barrier is not an argument anymore, since the company’s investor relations website offers enough material in English for more than two years now.

So, in my opinion, the main reason why the stock is more or less flat for two years is that many of the attractive key components have been deteriorating a bit lately, and the uncertainty about the company’s further path has increased. In the following, I would like to provide a deeper look into my current concerns.

Past and future growth

Long- and mid-term growth in revenues of Mo-BRUK S.A. was exceptionally high, with a 10-year CAGR of ~20%, and a 5-year CAGR of ~36%, respectively.

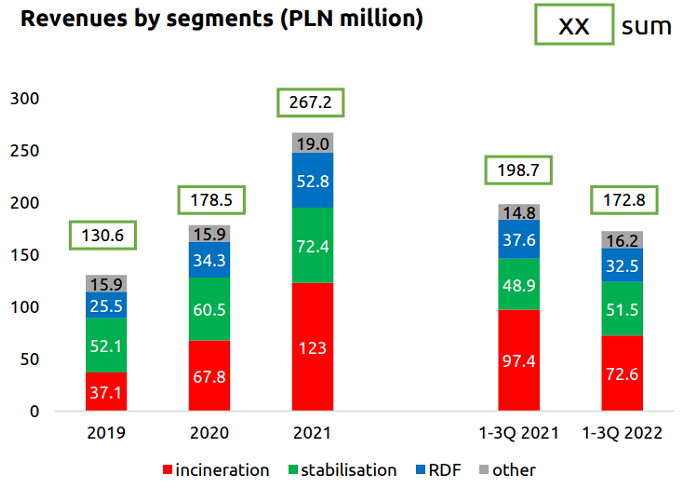

However, most recently, the revenues actually shrank in 1-3Q 2022 compared to 1-3Q 2021 by ~13%:

Mo-BRUK’s revenues (mobruk.pl: results presentation)

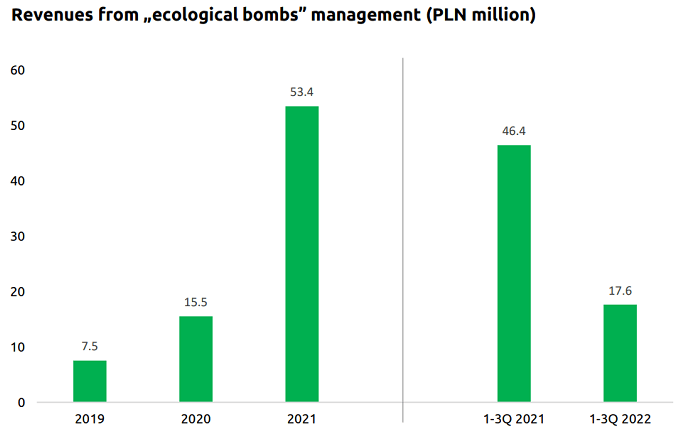

The decline in revenues mainly resulted from the incineration segment, more specifically, from significantly lower revenues (PLN 28.8 million less) due to liquidating the so-called “ecological bombs.” This is especially hazardous waste that requires special treatments and can therefore provide higher rates compared to other waste disposal categories.

Mo-BRUK’s revenues from “ecological bombs” (mobruk.pl: results presentation)

The main reason for the decline in revenues was an important project in Gorlice that was suspended by the National Fund for Environmental Protection and Water Management. This is a bit surprising given the importance of the “ecological bombs” to the Polish authorities due to outbursts from Polish citizens and EU requirements. However, it definitely indicates that Mo-BRUK’s success is very dependent on Polish politics. For the company, it is extremely important that the government maintains regulations for processing waste and that the company wins the resulting tender contracts for decommissioning of “environmental bombs,” which are obviously a very important growth driver for the company. Even though I think the general growth story of the company should still be intact, this dependency makes me a little uncomfortable and I wonder if the position of the company is truly this great or if it is the Polish government that fully sets the terms.

Profitability

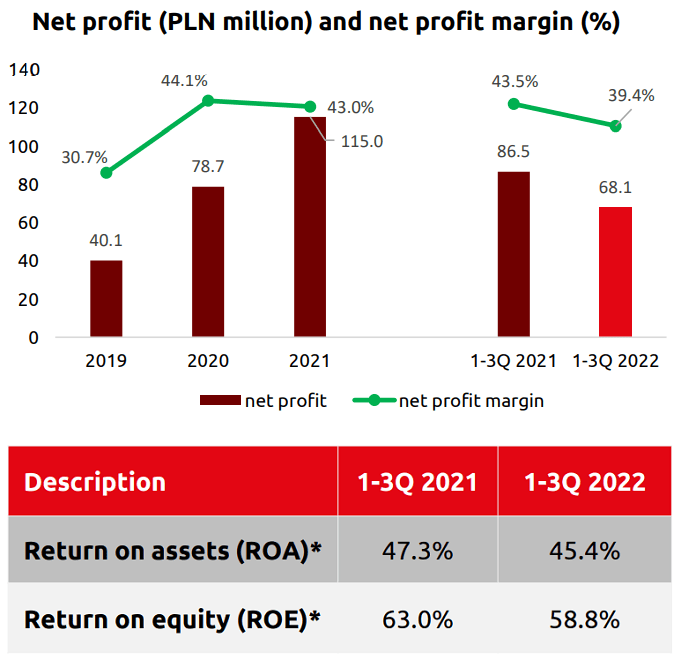

Looking at profitability, it still seems as if the company is in a comfortable position, although margins and returns have declined a few percentage points in the last quarters:

Mo-BRUK’s profitability indicators (mobruk.pl: results presentation)

This effect is also seen due to the decline in revenues of the very lucrative “ecological bombs”. In fact, they are crucial for the exceptional margins and returns that are way above international competition and Mo-BRUK’s challenging performance before 2018. It is worth noting that before the enforcement regarding the liquidation of “ecological bombs” by the Polish government, revenues, margins, and returns of Mo-BRUK were much lower. Return on equity was mostly in single digits and Mo-BRUK was even unprofitable in the years of 2014 and 2015, when the company almost went bankrupt.

Although Mo-BRUK is currently far away from this stage, I wonder if there could be a greater mean reversion and if the company’s margins and returns could come closer to competition’s in the near future. This would imply a decline to at least half of today’s net profit margin and return on equity. So far, we just see a minor hiccup for Mo-BRUK, which should nonetheless be closely monitored in the next quarters.

Financial health and capital allocation

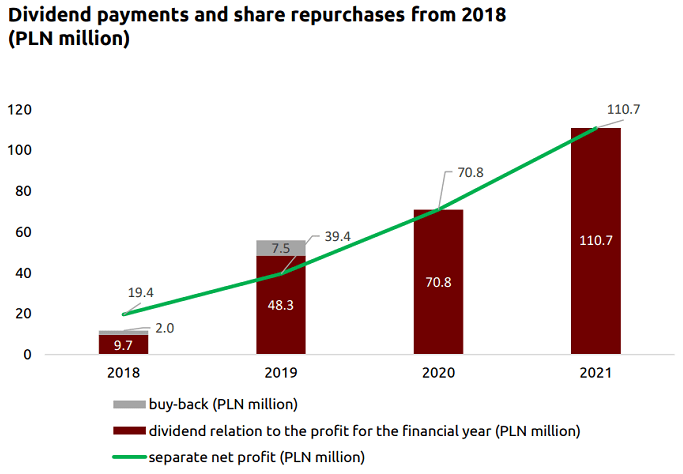

The current balance sheet of Mo-BRUK looks solid with almost zero debt. However, it is a little unconventional how the company is allocating capital during this expansion phase. They distributed 100% of the profits in dividends in the last two years and are not planning on reducing this in the near future:

Mo-BRUK’s dividend payments (mobruk.pl: results presentation)

Mo-BRUK wants to expand further and profit more from the favorable trend in the Polish waste industry. The company plans to spend around PLN 200 million in capex until the end of 2024 and would like to not only grow organically, but also through potential acquisitions. Interestingly, this undertaking should be mainly financed by debt while keeping the dividend payout ratio around maximum.

Even though leveraging is not necessarily a bad thing, and as a shareholder, high dividends are usually very tempting, I would prefer if the company would decrease its payout ratio to a level that there would be no risk that the debt surpasses the equity level. Especially because profitability was not always a given in the past.

Management and ownership

Next to the capital allocation, which could also be part of the management assessment, there was a major change in the company from Q2 to Q3 2022. Józef Mokrzycki, the founder of Mo-BRUK stepped down as CEO, explaining that the company is now fully prepared to function as an entity managed by professional managers. Although it is completely understandable that he steps down after 37 years as CEO, it is interesting that none of the younger family members who are also very familiar with the business succeeded, but someone outside of the family.

An even more crucial change one should keep an eye on would be if the founding family sold their remaining 35% stake of the company. The stake was locked up until the end of 2022, but there are rumors that they are planning to sell it entirely. Depending on the selling price, this could contradict their description of waste management in Poland as a business with “new opportunities on the brink of continuous expansion.” For me, it would probably be a negative sign, because if the company has such great prospects and the price is not very exuberant, why not let the children of the founder profit further from the great future cash flows?

Valuation

We all know that the market can sometimes be irrational for extended periods of time. However, I think that in this case, the market is also factoring in much higher risk premiums than it would for a larger company in a developed country that has a longer positive track record. Although the company’s current P/E ratio at around 11 is relatively low compared to international peers, it is not significantly below its own five-year average. That’s why I am afraid that the multiple could also not expand by much more than to 15 in the long run. The main reason for the market is most likely that Mo-BRUK is heavily reliant on the tender contracts in connection with the “ecological bombs” and, therefore, at the mercy of the Polish government granting them to the company and not allowing for cheap unregulated landfilling and dumping. Looking at the history of politics in Poland, there might be a risk of quick changes in course, which the market doesn’t like.

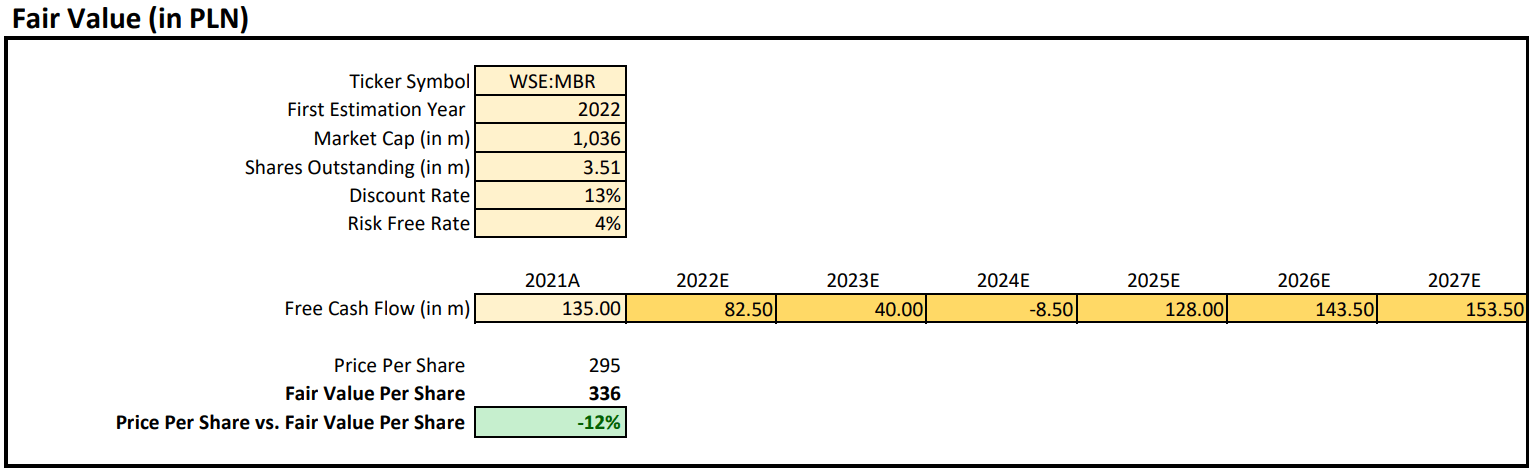

If I had to give a rough estimate for where I see the fair value of Mo-BRUK today, I would calculate it in the following manner:

DCF valuation (author’s spreadsheet)

In this simplified DCF calculation, I used analyst estimates until 2027. FCF is decreasing until 2024 due to the planned investments of the company. Taking the 2022 risk free rate of Poland at 4% and my required rate of return (discount rate) of 13%, I come up with a fair value per share of around PLN 336, which makes the stock slightly undervalued from my point of view.

Conclusion

Mo-BRUK is apparently one of the more attractive stocks out there. Otherwise, I wouldn’t have spent much time analyzing the company. It still has very attractive fundamentals and doesn’t appear as vastly overvalued. However, if one digs a little deeper, there are many question marks regarding the current status that I would like to get a clearer picture on. That’s why the stock can’t clear the hurdle for me at the moment.

Despite this, I will follow the company and its development, and I am especially excited about FY 2022 results and the outlook of the management, especially regarding the “ecological bombs.” For everyone who is already invested, I am happy if the thesis unfolds, even if this means the stock price is running away from me.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment