Editor’s note: Seeking Alpha is proud to welcome Ryan Licwinko as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Solskin

The Company

Chemed Corporation (NYSE:CHE) is a company that operates in the United States. The headquarters are located in Cincinnati, Ohio. Since its start in 1970, the company has built out a vast network that aims to provide a number of services to patients, primarily hospice and palliative care services. The network helps patients get in contact with physicians, registered nurses or home health aides, and a number of other valuable professionals.

Besides the health care service part of the company, they also hold a number of different branches that help residential and commercial customers with drain cleaning, water restoration, or plumbing.

I think that Chemed Corporation is a well-run company but right now I think a hold is the best rating for them. There is an investment case to be made, but I think the current valuation needs to come down first.

Market Tailwinds

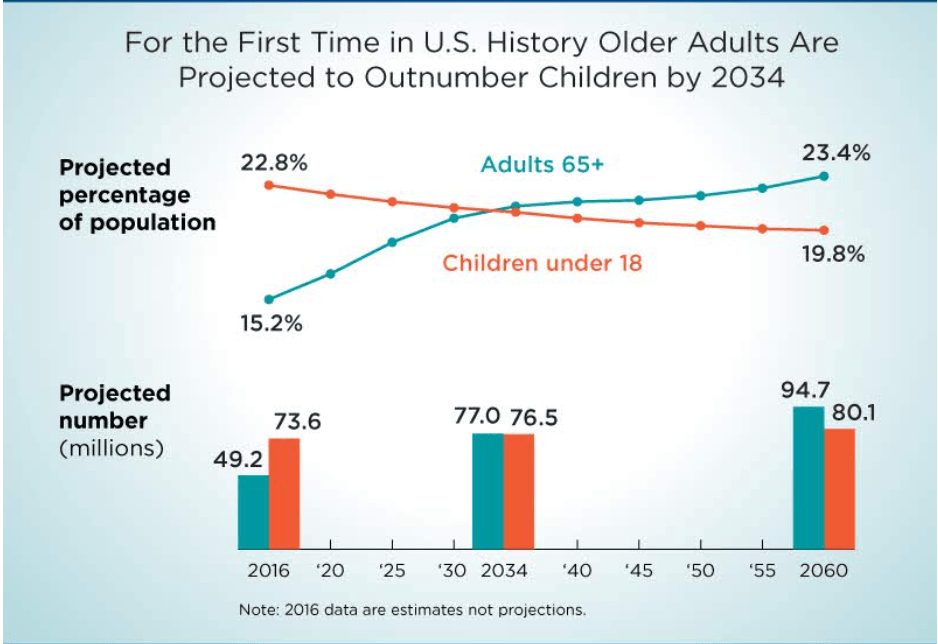

As Chemed Corporation operates one of the largest end-of-life care services called VITAS Healthcare Corporation it’s important to see what the market outlook might be. In the case of VITAS, they focus on the elderly population and help provide several important services.

Aging Population (census.gov)

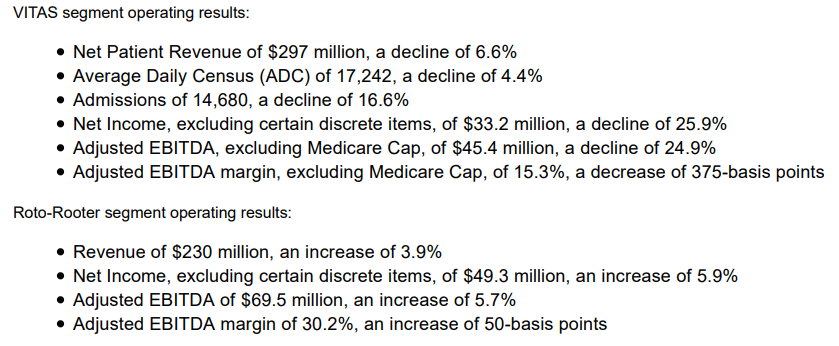

The company noted in the last earnings call that net patient revenues declined by 6.6%, a likely cause being COVID-19 being less prominent. Some might think this would be enough to disregard an investment in the company. But in my opinion, one of the biggest tailwinds for VITAS would be the aging population in the US. Right now 15% of the population is above 65. By the year 2030, this number is expected to grow to 21% instead. This means a lot more Americans than currently will be in need of the healthcare services that VITAS provides. It might seem like a long way out until then, but being early is sometimes good. Being an already established brand the likelihood for VISTA to increase revenues is very high in my opinion thanks to this large tailwind.

Revenue Breakdown

In the last earnings report the revenue breakdown between the two segments that make up Chemed was quite similar. VITAS generated $297 million in revenues, which was a decline YoY of 6.6%. However, Roto-Rooter, which is the plumbing and drain-cleaning part of the company, netted $230 million in revenues, an increase YoY of 3.3%.

Revenue Highlights (Earnings Report)

The management stated in the report that they expect a decline in revenues from VITAS by about 4.5% to 5% in 2022 compared to 2021. The pandemic and the need for the services they provide helped inflate the revenues to, quite honestly, unsustainable levels. A pullback is to be expected in my opinion. A positive is that the decrease is not nearly as large as a lot of other companies have reported.

Roto-Rooter is expected to grow by about 6.2% YoY and achieve an EBITDA margin of over 29%. I think however that the long-term tailwind for the company will be increased revenues from VITAS as the aging US population boosts the TAM the company is involved in. Going forward I will look closely at the way the revenues for VITAS develop and whether they can slow down the rate as the margins are decreasing.

Valuation

Right now Chemed Corporation is trading at a pretty high P/E of 25 compared to the sector median of 19. The bottom line has been growing at a good pace the last few years, a little bit all over the place but still an annual rate of 30% since 2017. The EPS has gone from $6.11 in 2017 to a TTM EPS of $17.46. This increase has further been helped by the outstanding shares decreasing almost 10% from 2017 until now, which would represent an annual decrease of 1.63%. I think this makes the long-term case more appealing as it brings more value to shareholders who stick around. I also believe this consistent trend of buying back shares justifies somewhat the higher multiple the company is currently trading at. A management team focused on prioritizing the shareholders will often result in a share price with a higher multiple.

EPS (Seeking Alpha)

As the growth and buying back of shares might be appealing, it’s worth noting the price/book right now is 10, which I think is a bit too rich. The lower this number is, the more value you could get for an investment. A reason for the increase in price/book is the cash position decreased by over $150 million in the last few years, which meant total assets decreased by just under 6%. But besides that, the company doesn’t generally hold that many assets in terms of facilities or properties, which inflates this number to the higher end.

Outstanding Shares (Seeking Alpha)

As a final valuation metric, I also want to showcase the net debt/EBITDA ratio which is 0.57. This is a great number as the probability the company won’t default on any debt is very small in my opinion. The company has maintained impressive free cash flows over the last several years. This is one of the fundamentals I look the most at right now. With higher interest rates on loans, companies that already have great cash flows will have an easier time taking on debt and expanding whilst competition has to halt.

Peers

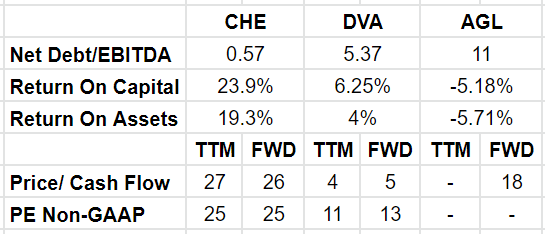

Within the healthcare service industry, there are plenty of different companies to choose from when making an investment. Looking at some peers to Chemed Corporation we have agilon health, inc. (AGL) and DaVita Inc (DVA).

Agilon might be the most similar to Chemed as they also focus on health care services niched towards seniors with primary care physicians. DaVita is a bit different as they operate centers and labs with a focus on chronic kidney failure.

Valuation wise, DaVita seems like the way to go with a p/e of just over 11. Agilon is yet to have a positive bottom line which makes any investment a risky one. Growth wise however I think that Chemed has the upper edge with tailwinds like the aging population that I mentioned previously. Even though DaVita might look appealing, moving to the price/book they have a very valuation at 14.

Company Comparison (My Own Comparison)

I think that from the chart I have above, the most enticing company to possibly invest in would be Chemed, let me elaborate a little bit. What draws me the most towards Chemed would be the much higher return on capital and assets that they have. With numbers like that, I think the higher p/e makes sense as the company has a proven track record of leveraging its holdings and generating good cash flows. In my opinion, I want to have a company with a high percentage of cash flow as this usually translates into the company either distributing a dividend or buying back shares. In the long term this makes my investment in the company much more worthwhile. To further boost the case for Chemed compared to the other two is the much lower debt they hold. It is unlikely in my opinion to become an issue anytime soon.

It’s difficult comparing companies like this to each other as the markets they are in are different. But I think it’s still valuable given that it can help broaden an investor’s horizons and perhaps find other opportunities within a broad sector like healthcare.

With that said, I think that Chemed still offers the best opportunity here for investing, primarily because of the major tailwind concerning the aging population in the United States. Long-term, I think there is a very good case to be made that Chemed will achieve faster-growing revenues than these two other companies I presented.

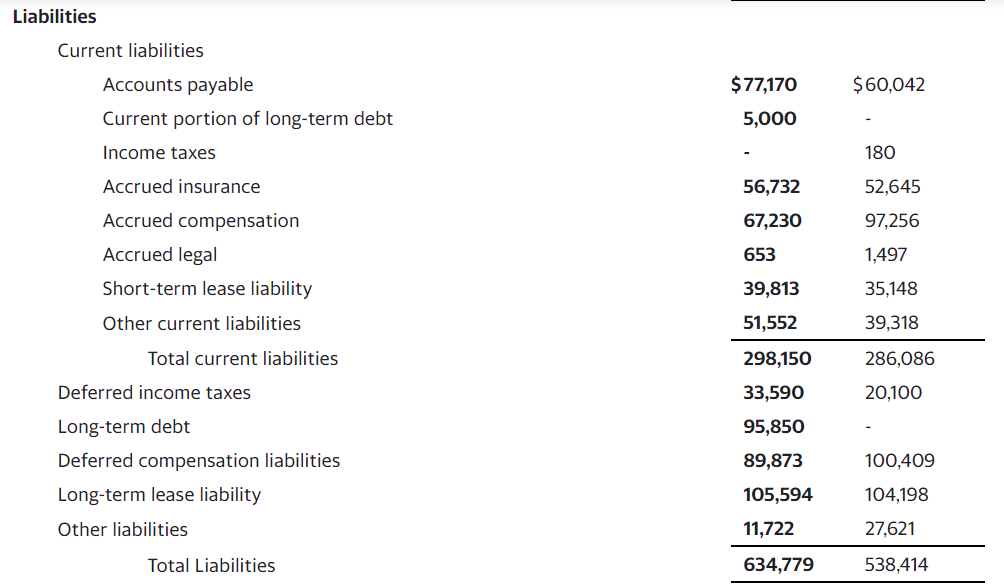

The Balance Sheet

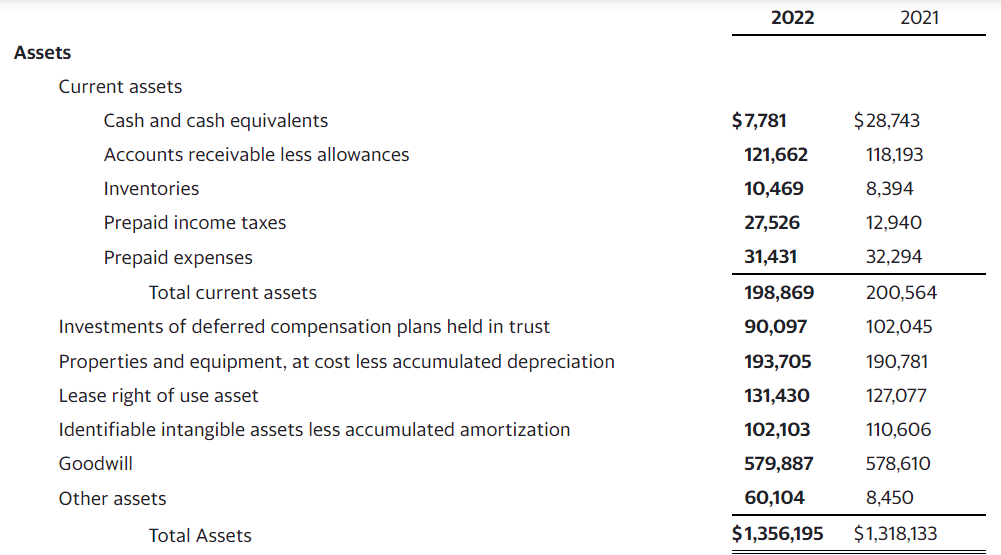

Looking at the balance sheet of Chemed Corporation they have seen a drastic decrease in the cash position over the last few years, going from a high of around $168 million to just under $8 million in the last report. But I don’t think it’s too worrying given that debt is manageable with $246 million in free cash flow in the last 12 months. This is plenty enough to handle the long-term debt of just under $96 million.

Assets (Earnings Report)

With this, I have to say Chemed is running a tight ship in terms of its financials. They aren’t worried about taking on some debt as the positive cash flows are more than enough to support it. With share buybacks happening consistently over the last few years it seems the management is equally as confident in their position to run the company and give back value to shareholders.

Liabilites (Earnings Report)

Moving forward, I would like to see the cash position seeing a steady increase whilst the accounts receivables also increase. This would indicate to me that the trend of more customers entering VITAS is happening. I like to see a strong cash position with all companies I invest in. If they can manage to pay down all their debt that is a big plus, but if the cash flows are high enough then a large cash position is not always necessary. But to conclude the balance sheet segment somewhat, I think that Chemed is in a good position with little debt that is very manageable. With a higher cash position, the price/book would go down and perhaps more investors would be enticed to start a position, me included.

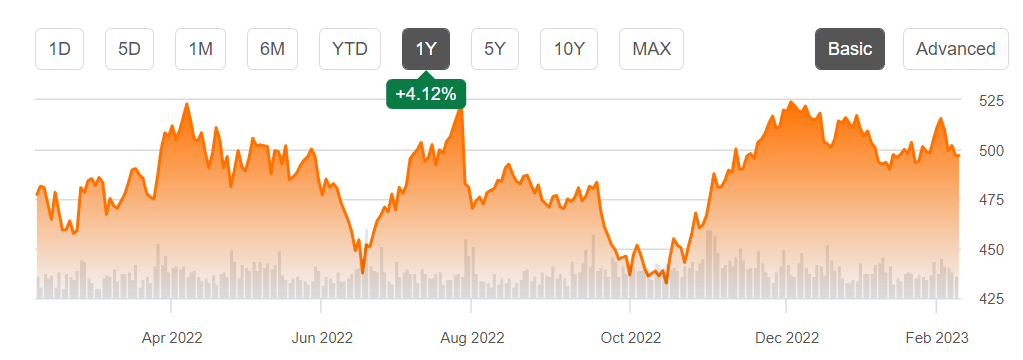

Price Chart

Right now Chemed Corporation is a fair bit above the 52-week lows of $430 per share. But it’s also a fair bit down from the highs of $528 per share. I think that the 52-week lows presented a great buying opportunity, but the current prices aren’t all that bad either.

Price Chart (Seeking Alpha)

The P/E is a bit high perhaps, but the major tailwind of an aging US population I think will offset this as more and more revenues can be generated and justify the multiple. With the shares being bought back almost 1.6% each year, I think share appreciation will happen to those who hold long-term. Looking at the way the company capitalizes from future tailwinds and what the management says about its future will be critical in the coming months.

Risks

With most companies and investments there are risks that come along. With Chemed I think that the biggest risk is that the company is not able to capitalize on the tailwind I mentioned of an aging population. If this can’t translate into increased revenues then the long-term growth could be lower than estimated.

Besides that, an increase in operating expenses could also hinder the bottom-line growth. As more and more demand is placed on services that Chemed offers, it might cause them to have higher operating costs in order to satisfy their customers. But I don’t think these risks are great enough to create a bear case for the company. The management seems competent and should be able to maneuver around this.

Conclusion

Chemed Corporation is a company primarily in the healthcare service industry with one of its branches being VITAS, a large and leading provider of end-of-life care services. With the population of the US expected to have a higher percentage of the elderly by 2030 compared to now, the market that Chemed can serve increases a fair bit. This is one of the major tailwinds going forward.

Besides a positive outlook, the company has managed to achieve a stable balance sheet with debt being no issue as cash flows are high. Shares being bought back at a good rate makes me think the management is confident in their position. But the share price has run up a little bit too much recently and I think a hold for the company might be the better option right now. Until the P/E decompresses to numbers more in line with the broader sector, I think there are better opportunities out there. But the long-term picture still seems bright for Chemed Corporation.

Be the first to comment