waleed ahmed

Investment Thesis

CNH Industrial (NYSE:CNHI) reported its Q3 2022 results on Nov. 8, 2022. The company finished the quarter with record revenues of $5.9 billion and an Adjusted EBIT from Industrial Activities up $250 million compared to Q3 2021. According to the guidance provided CNH Industrial expects its net sales to increase between 16% and 18% for FY 2022. The results were satisfying and the company’s stock is up approximately 20% since then.

The long-term outlook for CNH Industrial looks definitely promising. The company is continuously undertaking business initiatives in order to fuel its growth amidst favorable macroeconomic conditions. The acquisition of Raven Industries is expected to help CNHI tap into new opportunities in the precision agriculture field while the acquisition of Sampierana is expected to boost the growth of its construction equipment business. In addition, the company’s available liquidity of $8.6 billion enables CNHI to make more acquisitions, if needed. In the meantime, the company is also focusing on improving its margins through mainly operational efficiencies and continuous brand improvement. Moreover, and besides the spin-off of Iveco Group, Scott Wine is taking initiatives to increase company’s popularity among US investors. CNH Industrial has already announced a $300 million share buyback plan along with its intention to report its results in accordance with US reporting standards. A rising world’s population, robust farmers’ income and significant infrastructure investments both in EU and USA make up an ideal environment for companies like CNHI that possess considerable pricing power.

On the other hand, there are also certain risks that investors should consider before investing in CNHI’s stock. If Raven’s integration fails, the company won’t be able to capitalize on the Precision Ag opportunity and will be left significantly behind its competitors. Moreover, failure to expand its margins will most probably lead to the stock’s underperformance in relation to its peers. Furthermore, its loyalty voting structure could potentially decrease the necessary decision-making flexibility. Last but not least, any tightening of the emission standards could severely impact CNHI’s financial performance.

To sum up, I don’t believe that the market has fully priced in CNHI’s long-term growth potential, the company’s transformation and the favorable macroeconomic environment. Additionally, an investment in the company’s stock would serve as an inflation hedge and it would be suitable for those looking for both value and growth outlook. Hence, we rate CNH Industrial a buy.

Favorable Macroeconomic Environment

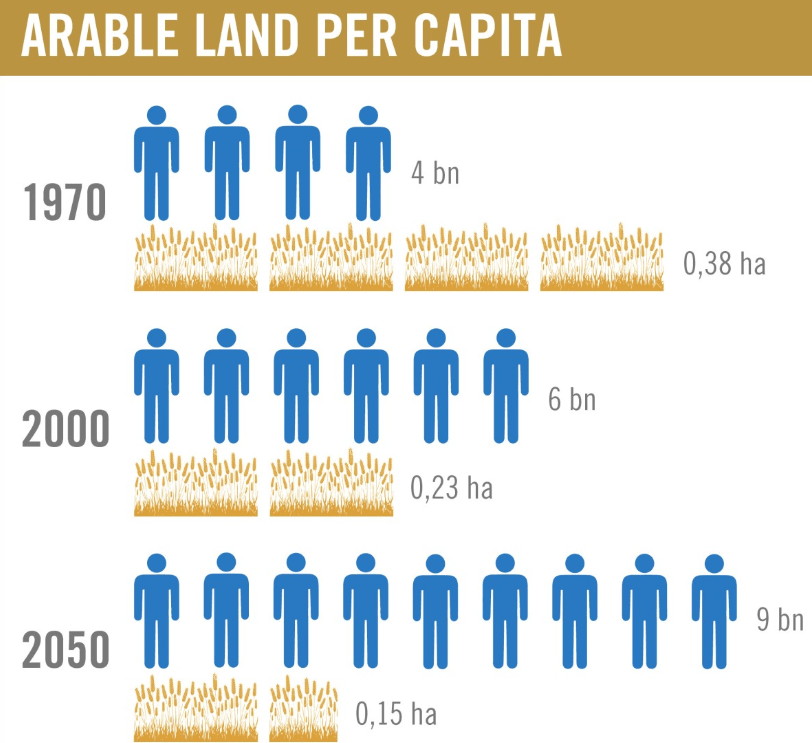

Agriculture is undoubtedly one of the most complex macroeconomic themes, especially when it comes to making short and mid-term predictions. The reason for this is that it is being impacted by countless factors like economic and population growth, energy prices, weather conditions and disruptions in supply chains. But one thing is more or less certain. The world’s population will keep rising and it is estimated to reach 9.8 billion in 2050. At the same time food per capita consumption is also expected to increase due to the improving economic conditions in the emerging countries. According to OECD estimations, agriculture’s supply growth will hover around 1.1% whereas demand is expected to grow 1.4% per year till 2030. So, it is becoming crucial for humanity to increase its food output. This can be done only in two ways: either by increasing arable land or by an increase in land’s productivity.

Source:Heraeus

Since the latter seems impossible the only viable way to increase productivity is the wider adoption of precision agriculture and automation solutions. Following this path, the farmers will be able to boost crop yields while at the same time they will save on input costs. Speaking of costs, what needs to be highlighted is that except the increase associated with costs like fuel, seeds and fertilizers there is also a surge in regulatory costs associated to labor. According to a research, between 2005 and 2017 there was a 795% increase in costs related to labor rule changes, healthcare and food safety practices.

In addition to the above, we should also take into account the continuous and consistent governmental support towards the agricultural sector. The majority of governments worldwide provide generous financial assistance towards farmers mainly in the form of subsidies and loans with favorable payment conditions. This fact has traditionally played an important role in the growth of the agricultural equipment sector. According to OECD, between 2018-2020, 53 countries worldwide provided an average of USD 728 billion each year in direct assistance to farmers.

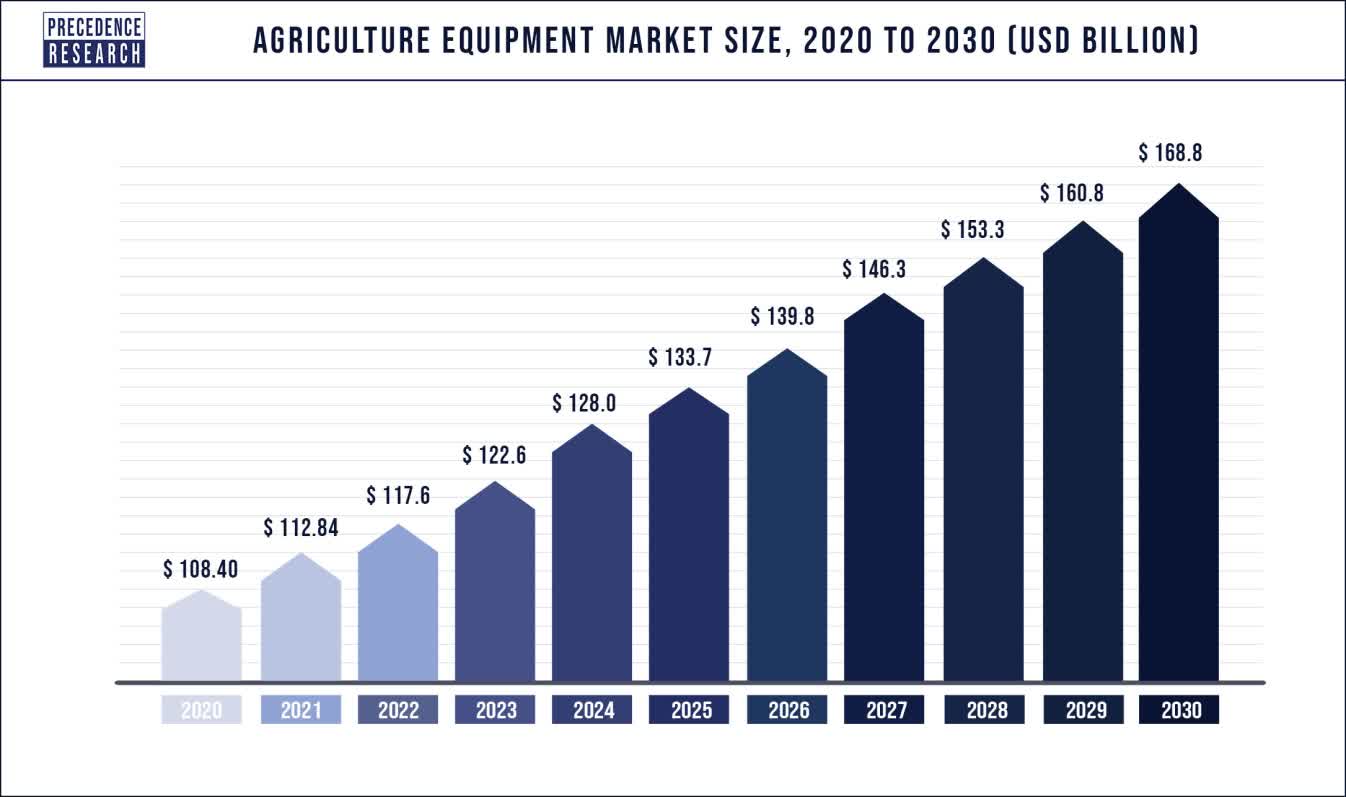

As a result, it is not a surprise that the global agriculture equipment market is about to boom. Its market size is expected to reach USD 168.8 billion by 2030 with an estimated CAGR of 4.6% between 2020-2030.

Source:Globenewswire

The increasing importance of key crops in the energy production process is expected to be another one major driving factor for the entire agricultural sector. Almost 40% of the overall corn output is currently used in the production of ethanol. Around 30% of the US soybean oil production is also used to make bio-diesel. It is worth noting that the introduction of the Renewable Fuel Standard in USA has caused an increase in corn and soybean prices of 30% and 20% respectively. So, as long as the global energy crisis won’t subside the pressure in the crop prices will remain and will lead to higher farmers’ income, boosting this way agriculture equipment sales.

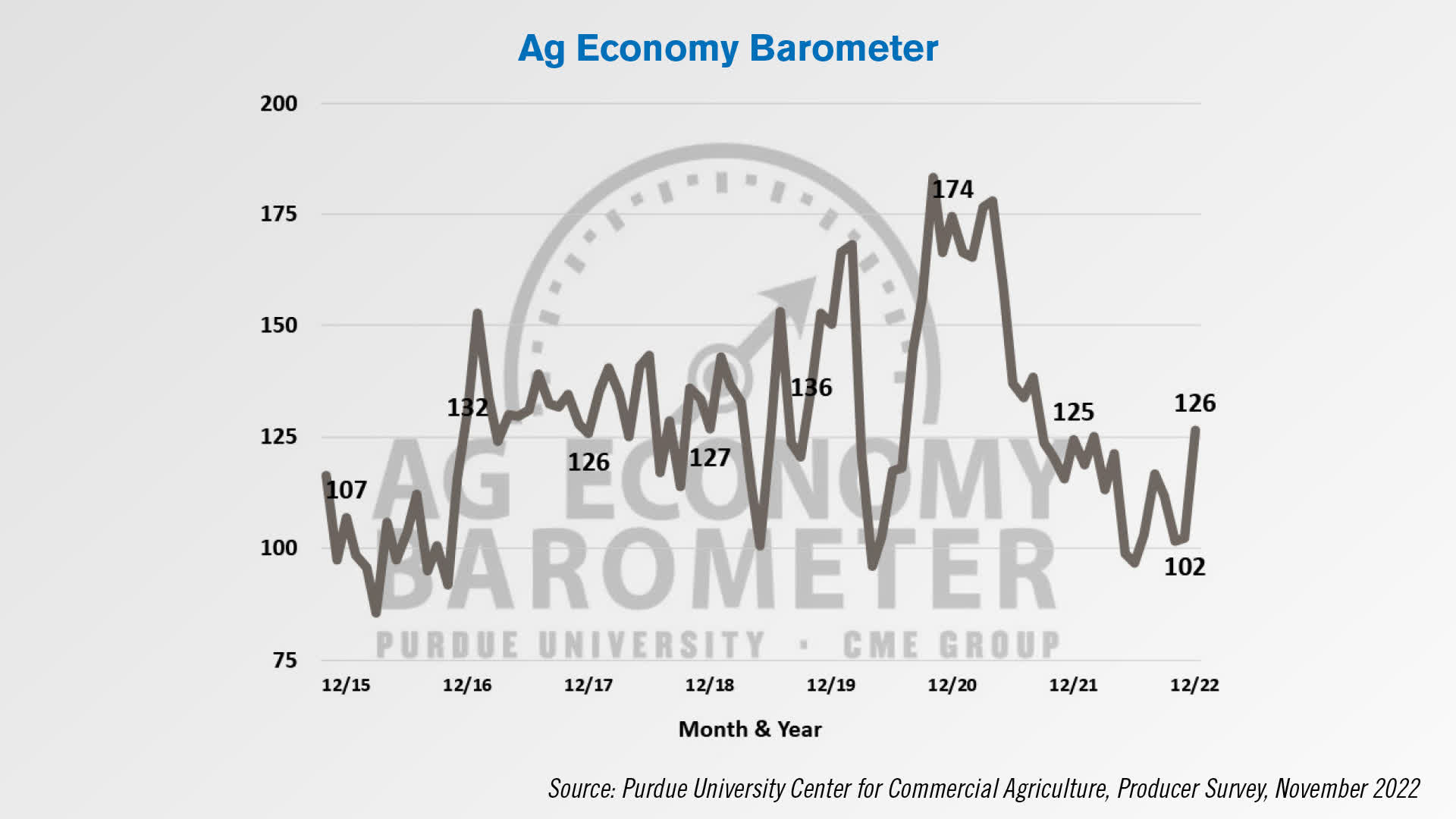

When it comes to market momentum, probably the biggest determinant of agriculture equipment purchases is the farmers’ perception of current economic conditions. It is evident from the chart below that farmers’ sentiment improved substantially in December 2022. Also, net farm income for FY2022 is expected to reach record levels. As fuel and fertilizers’ prices will start to normalize due to governmental intervention and market adaptation, the ongoing war in Ukraine will keep crop prices high. It is estimated that the disruption in the supply of key crops due to the war will last for at least another 3 years. Hence, we expect an additional minor improvement in the farmers’ profit margins for the years ahead.

Source: FarmEquipment

Last but not least, the intersection of lower used equipment inventory, the change in farmers’ buying habits and the ongoing effects of the limited production between 2021-2023 is expected to keep agriculture equipment prices elevated. More specifically and according to the latest update, a significant number of dealers still report that their inventory levels are “too low”. Furthermore, the buying habits of farmers seems to have changed due to the spike in the price of used farm equipment. Farmers are now more willing to pay higher prices for new equipment. Finally, the limited production and supply of farm equipment in the previous years is expected to be reflected in the future prices.

CNH Industrial’s Moat

CNH Industrial was formed in 2013 after a series of mergers and acquisitions and it is listed both on the NYSE and on the Borsa Italiana. The company owns a portfolio of 5 well-respected brands. This is comprised of Steyr Traktoren, New Holland Agriculture, Case IH, Case Construction Equipment and New Holland Construction. It is considered the market leader in Europe and it is the second biggest player in the NA Agriculture market.

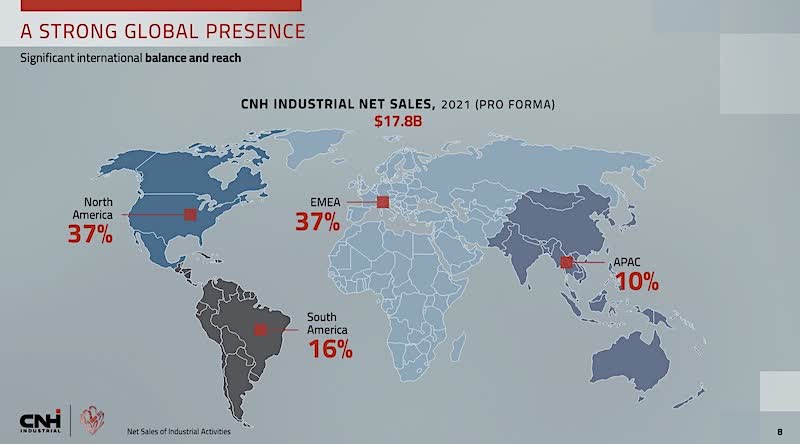

Thanks to its global presence, CNH Industrial’s top-line is well-diversified. This fact gives the company greater stability and resilience in case of regional economic slow-downs.

Source:Meccagri

It is widely known that farmers don’t like to change their equipment’s brand unless they have serious reasons. The most prominent of them seem to be spare parts and service’s availability along with their quality. With a presence to over 200 countries and with a network of thousands dealers/service centers, CNH Industrial is ideally positioned to maintain its customers’ loyalty. We consider the well-established relationship between farmers and company’s dealers as a crucial part of CNHI’s moat, especially when it comes to its effort to fend off competition from low-cost manufacturers.

With an inventory comprised of millions of SKU’s and a genuine commitment to customer service excellence, it is crystal clear that the management of CNH Industrial’s supply chain is not an easy task. Turning the problem to an opportunity, the company started experimenting with an Additive Manufacturing strategy back in 2019 with the help and guidance of Materialise. CNHI started printing tools and spare parts to support its operations. This way it managed not only to reduce the volume of its inventory but also improve the whole customers’ service experience. It is estimated that currently around 50% of CNH Industrial facilities use 3D printing with great success. This may not seem so important but according to a research conducted by McKinsey, supply chain disruptions have changed farmers’ purchasing behavior. Approximately 30% of them state that brand loyalty is not so crucial anymore when it comes to purchasing new equipment. So, by excelling in this area CNHI could boost further its market share and widen its moat.

According to our opinion the most critical factor in CNHI’s long-term effort to win market share and improve its margins will be its ability to win over the technology race in the industry. Or at least to not be left significantly behind John Deere. The company’s management has not only recognized this imperative but has clearly stated that CNHI’s strategic focus is on technology leadership. And fortunately, there are many proofs for its strategic commitment. In the previous December and during its Tech Day, CNHI “revealed the New Holland T4 Electric Power, the industry’s first all-electric light utility tractor prototype” and T7 Methane Power LNG which is according to the company currently the only available methane powered tractor worldwide. When the “T7 tractor will be integrated within Bennamann’s on-farm liquid fugitive biomethane production process“, farmers will be provided with new opportunities to increase their revenues and lower their costs through the management of their waste. Hence, their switching costs and brand loyalty will be increased. Speaking of the company’s brand, it is worth to be mentioned that CNHI is constantly receiving awards for its equipment. Recently its Straddle Tractor Concept won the gold medal for its design at the German Design Awards 2023 and its brands, Case IH and New Holland, won four 2023 ASABE awards. The aforementioned developments will definitely strengthen CNHI’s brand and its pricing power. Regarding the alternative propulsion tractors, they are not expected to help the company steal market share in the short term but they would definitely give it the first mover advantage in a promising market.

Valuation

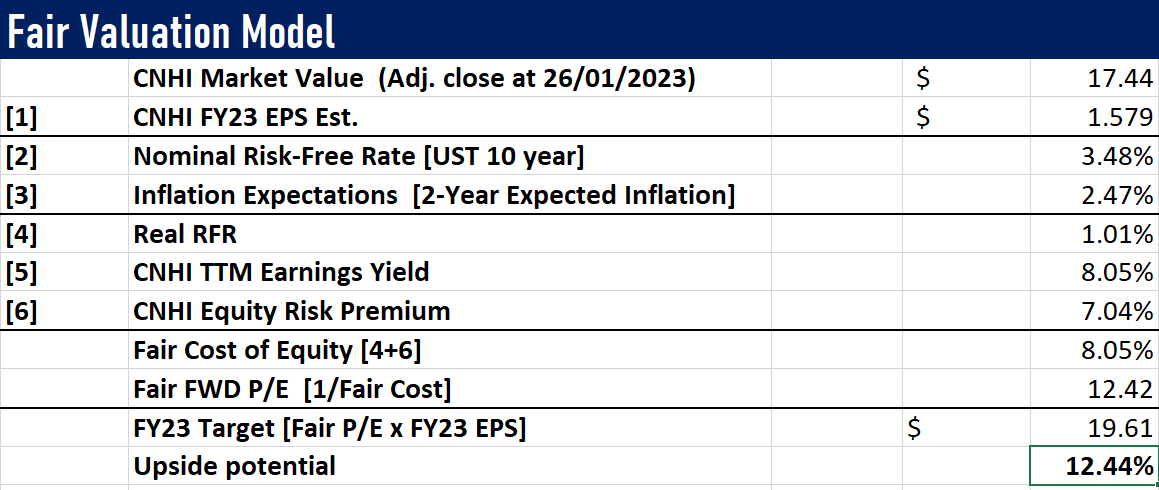

According to analysts’ consensus estimates CNHI will achieve a $1.579 EPS in FY2023. At current levels, CNHI has a TTM earnings yield of 8.05% , and investors are compensated with a 7.04% real equity risk premium. We believe that CNHI is fairly priced around 12.42x earnings, implying a price of $19.61 per share. This suggests a potential upside of 12.44%.

Source:Author’s Calculations

Risks

No investment comes without risk, so before any placement in CNH Industrial’s stock the potential investors should take into account the below risk factors.

To begin with, if the integration of Raven won’t be successful that would be a major long-term blow for the company. CNH Industrial will be left behind its competitors and won’t be able to capitalize on the Precision Ag opportunity. Such a development would be detrimental since Precision Ag seems to be the biggest trend in the industry. According to our opinion this is not very likely to happen.

Moreover, the company’s loyalty voting structure poses a significant yet often neglected long-term risk. In a fast-paced economic environment which requires utmost flexibility, the gradual concentration of voting power could make the decision-making process less effective and management’s decisions suboptimal.

Last but not least, rapidly evolving emission standards could negatively impact the global market for agricultural equipment. They could not only limit the potential revenues of manufacturers but also significantly increase their R&D expenses hurting this way their bottom line. It is estimated that the production of agricultural machinery compliant with Euro Stage IV emission standards would increase its price by at least 10-15%.

Conclusion

CNH Industrial possesses a widening moat in the global agricultural equipment industry which experiences high-growth. We don’t expect it to become the market leader in the near future but it is already taking decisive steps to close the gap with John Deere. Raven’s integration, company’s loyalty voting structure and the potential tightening of emission standards pose the main risks associated with an investment in the company’s stock. The long-term probability of outcomes is positively skewed. We rate CNHI a buy with a FY23 target price of $19.61.

Be the first to comment