InfinitumProdux

Star Bulk Carriers (NASDAQ:SBLK) has received flak recently from investors (see here and here), and deservedly so.

After benefiting from the pandemic-driven supply chain disruptions and reopening surge, the over-optimism led to a dramatic bust in its operating performance, as we discussed in our previous update.

Despite that, SBLK has outperformed the S&P 500 (SPX) since our late November update, posting a total return of nearly 19% relative to the SPX’s 1.4% uptick.

Recall that the operating environment worsened through January (as highlighted in our January article), likely confusing some bearish investors about the behavior of market operators.

Didn’t the company report a poor Q3 release, with its Q4 release likely also going to be horrid? Star Bulk is scheduled to release its FQ4 and FY22 earnings report on February 16, so investors will get clarity soon.

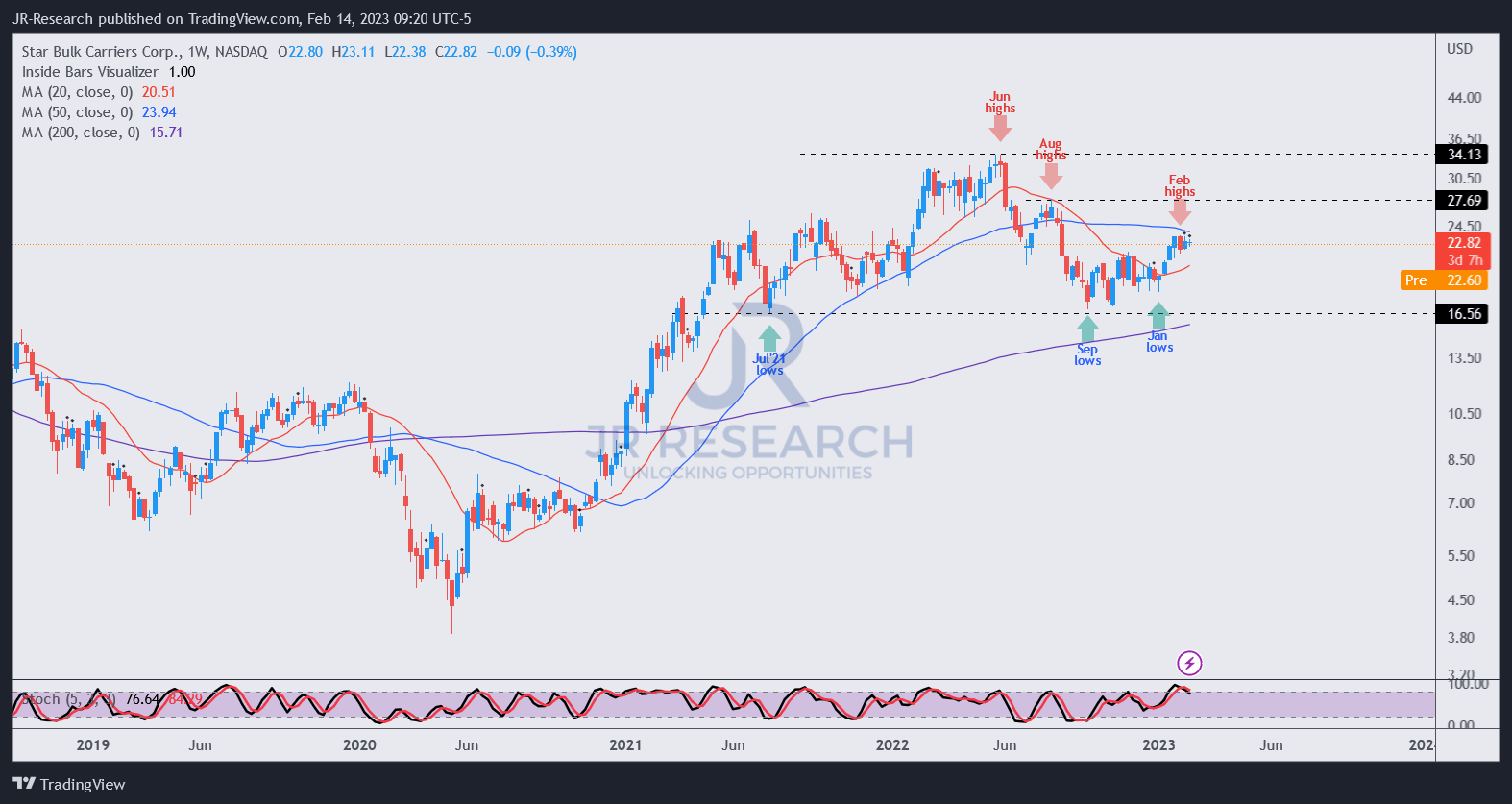

Notably, SBLK rallied from our January update, almost hitting our price target (PT) of $24, before pulling back recently. As such, we believe the $24 price level is a critical resistance zone that has proved its mettle against further buying upside.

We think that SBLK could continue to face stiff resistance at the $24 level, which would generally suggest caution on adding more positions. However, we believe the cyclical headwinds on further downward momentum against Star Bulk and its dry bulk peers have shifted favorably.

We urged investors to watch China’s reopening closely as it could be a “game-changer.” Therefore, we believe savvy market operators have likely leveraged its late 2022 lows to accumulate “quietly” before pushing the recovery upward toward its recent highs.

China’s recovery has proved to be faster than expected, with economists upgrading their forecasts from their initial estimates. Although China posted a 2.1% decline in steel output in 2022 due to its property market malaise, it’s important to note that it’s already “old’ information.

It’s essential for investors to always bear in mind that the market looks ahead and anticipates. Hence, it’s more important to assess the forward cyclical and structural tailwinds that could help SBLK recover from its battering relative to the headwinds that could hamper its progress.

Moreover, India has continued its robust coal imports, driving its industrial needs. India plans to uplift its manufacturing engine as global companies seek to diversify their production capacity away from China. Therefore, the recovery of China’s demand for commodities and raw materials could bolster India’s aims to “boost manufacturing to 25% of GDP.”

The freight index has also seen a boost recently, lifting investor sentiment. However, we believe investors must focus on forward projections for SBLK, which could help investors assess whether the analysts could have overstated Star Bulk’s ability to recover its momentum.

Accordingly, analysts expect the company to post a revenue decline of 19.3% in FY23, revised further from January’s projections of an 18.7% decline. Star Bulk’s adjusted EBITDA is expected to fall by 26.4% in 2023 before recovering by 16.5% in 2024.

We believe China’s recovery in H2’23 is critical toward bolstering Star Bulk’s ability to meet those estimates, particularly if the world’s economy is expected to post lower GDP growth in 2023.

Notwithstanding, it’s clear that analysts don’t expect Star Bulk’s decline to be structural but a well-deserved normalization phase after an unsustainable pandemic surge.

However, investors need to consider whether SBLK’s price action is constructive or indicative of a further decline moving ahead.

SBLK price chart (weekly) (TradingView)

As seen above, SBLK closed in against our previous PT of $24 at a price level that coincides with the 50-week moving average or MA (blue line) and faced significant resistance.

Hence, we believe some investors could have used the opportunity to lighten up some exposure ahead of SBLK’s upcoming FQ4 release.

There’s little doubt that SBLK is in a medium-term downtrend and needs to regain control over its 50-week MA before a sustained recovery can be observed.

More conservative investors could wait for a pullback or until a medium-term uptrend has been confirmed. Or wait until the all-clear is seen in its operating performances, suggesting a clear inflection point.

However, the drawback of such an approach is that SBLK could have moved much higher as the market looks ahead. Hence, the reward/risk profile would likely be much less attractive if you wait for the stars to align “perfectly.”

High-conviction investors should use pullbacks to add more exposure if they believe that China’s recovery and India’s ongoing industrial drive would be robust enough to mitigate the risks from the West’s economic fallout.

Rating: Buy (Reiterated, PT upgraded to $26.)

Be the first to comment