FinestWorks/iStock via Getty Images

Mission Produce, Inc. (NASDAQ:AVO) operates in the growing avocado industry, and appears to be an expert in the distribution of products in many regions all over the world. In my view, further integration of its supply chain, the new facilities in the UK for the year 2023, and expected FCF make AVO a must-follow stock. Even considering risks from concentration of clients and lack of suppliers, the stock appears undervalued.

Mission Produce: Marketing And Distribution Of Avocados At An International Level

Mission Produce, founded in California in 1983 by experts in the cultivation of these foods, is a leading company in the trade of food products, mainly avocados.

Since its creation to date, it has had exponential growth that catapulted it to the export of avocados in Europe, Asia, Canada, and South America. The company does not only claim to produce avocados and mangoes, but also carries out logistics and distribution.

Currently, Mission Produce has two large segments, marketing and distribution of the products from the source of cultivation to international export and international cultivation. The latter means that the company is permanently making investments in the acquisition of new fertile and functional lands for the expansion of its business model.

A significant part of the company’s revenue comes from its marketing and distribution segment. There is a huge difference as compared to the revenue coming from the farming segment. With this in mind, I would say that Mission Produce is mainly an expert in marketing and distribution. I believe that Mission Produce’s business model directly depends on its sales capabilities as well as the economic conditions of each region, because if there were drastic changes in this phase of the marketing process, there would be drastic changes in its annual earnings.

Source: 10-Q

Although Mission Produce does not have declared goals or long-term objectives in relation to gas emissions, carbon footprints, or ethnic equality policies for its workers, it declares that it is developing a sustainable and environmentally friendly business model. This includes the re-packaging of products, the articulation of business policies with the regional governments where their cultivation territories are located, the reduction and intelligent management of waste from its production model, and the use of renewable energy among others. I believe that sufficient marketing of the company’s environmentally friendly business model could bring equity demand.

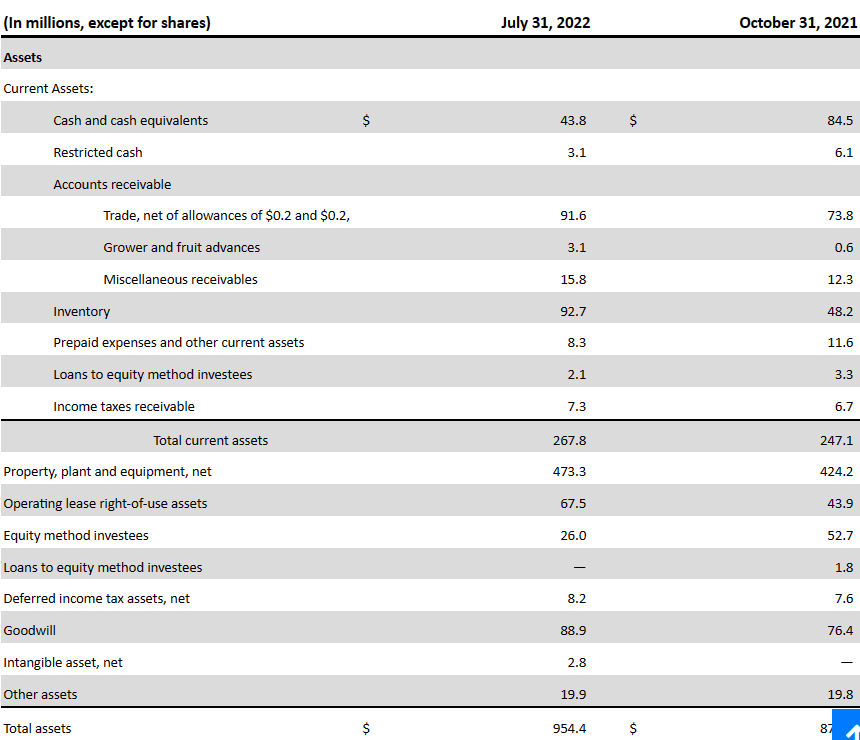

Balance Sheet

In the last quarterly report, Mission Produce reported cash of $43.8 million, accounts receivable of $91.6 million, and inventory of $92.7 million. Total current assets stood at $267.8 million, with property worth $473.3 million and goodwill of $89 million. The asset/liability ratio stands at close to 3x, so I wouldn’t be afraid of the total amount of liabilities.

Source: 10-Q

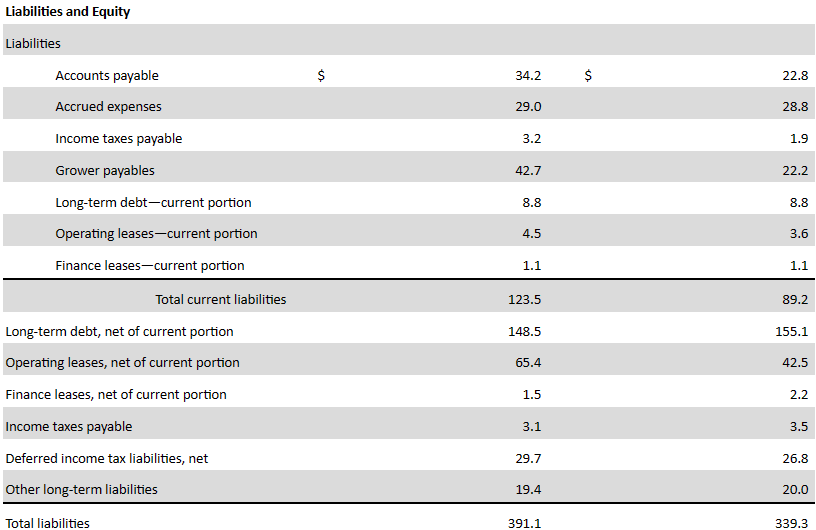

The list of liabilities include accounts payable of $34.2 million and total current liabilities of $123.5 million. Long term debt stood at $148.5 million with operating leases of $65.4 million. The company also reported deferred income tax liabilities worth $29.7 million, other long term liabilities of $19.4 million, and total liabilities worth $391.1 million. Considering the amount of EBITDA expected in 2023 and 2024, I am not afraid of the total amount of debt.

Source: 10-Q

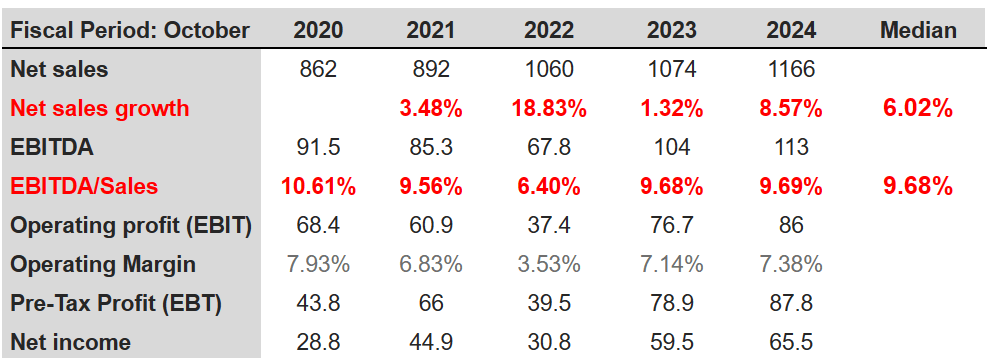

Market Expectations Include 18%-1.32% Sales Growth And EBITDA Margin Close To 6%-9%

Market analysts expect net sales of $1.166 billion accompanied by 2024 net sales growth of 8.57%. In addition, 2024 EBITDA would stand at $113 million with an EBITDA/sales ratio of $9.69%. Besides, analysts believe that 2024 operating profit will likely be close to $86 million with an operating margin of 7.38%. Finally, estimates include pre-tax profit of $87.8 million with a net income close to $65.5 million.

Source: marketscreener.com

Expectations also include free cash flow of $8 million with a median FCF margin of 0.69%. In my financial models, I used some of the figures that we saw in the past. Considering the company’s business model, I don’t think that the numbers are going to change a lot in the near future.

Source: marketscreener.com

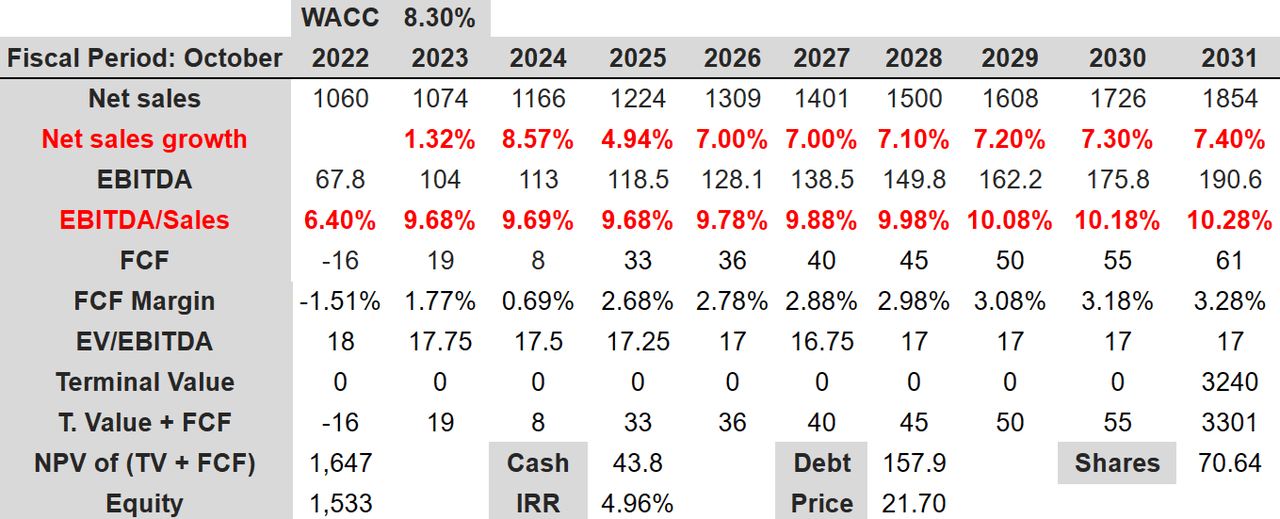

My Conservative DCF Model Leads To A Valuation Of $21.7

Under normal conditions, I would expect that the company’s efforts to vertically integrate its supply chain will likely lead to higher free cash flow margins. Besides, further diversification of sources and more connections at an international level would bring larger revenue growth than expected with less operating risks. Management discussed some of these strategies in the annual report.

Source: Investor Presentation

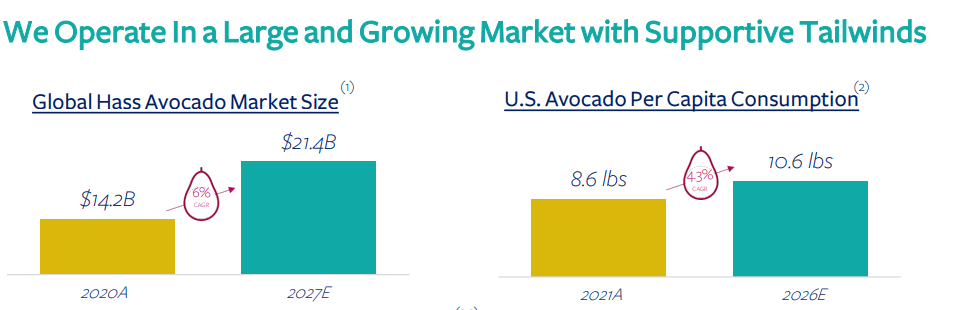

Besides, I would be expecting sales growth thanks to the company’s exposure to the Avocado market, which is expected to grow at a CAGR of 6% from 2020 to 2027. Let’s keep in mind that the U.S. Avocado per capita consumption is also expected to grow in the coming years.

Source: Investor Presentation

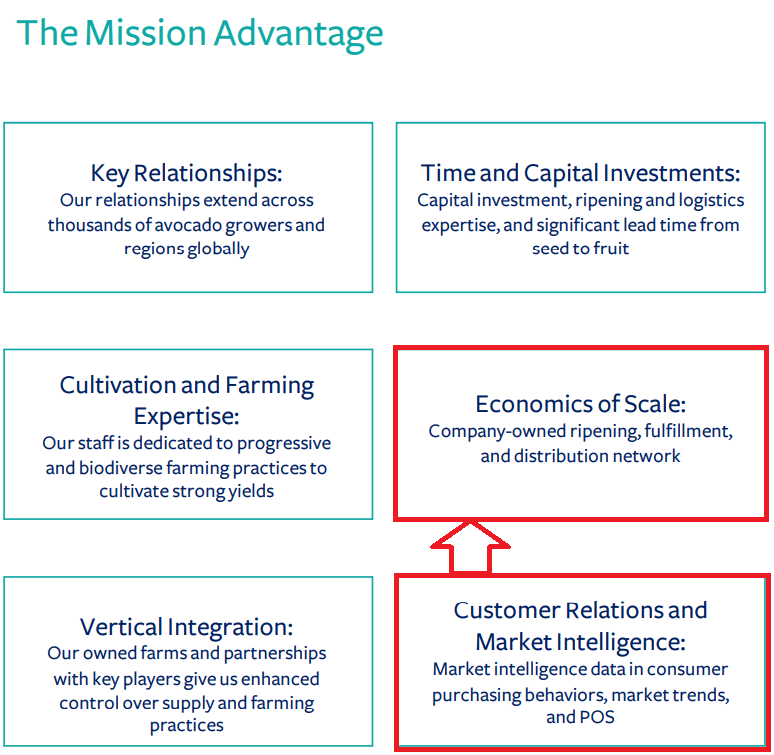

I also believe that Mission Produce will likely benefit from the increase in the avocado market in Asia and Europe. Let’s keep in mind that the company expects to open new facilities in the United Kingdom in 2023, which could, in my view, push revenue growth up.

Source: Investor Presentation

Finally, under normal conditions, I would expect economies of scale coming from the company’s distribution network and the company’s access to more international markets. Besides, more work with customers, market intelligence efforts, and data accumulation about consumers will likely bring further sales growth.

Source: Investor Presentation

I assumed 2031 net sales of $1.854 million with a net sales growth of 7.40%. In addition, I assumed 2031 EBITDA of $190.6 million accompanied by an EBITDA margin of 10.28%. 2031 FCF would stand at $61 million with 2031 FCF margin of 3.28%.

Besides, with an EV/EBITDA of 17x and WACC of 8.3%, I obtained a terminal value close to $3.24 billion. The sum of the NPV of the terminal value and the FCF would be $1.647 billion. Finally, with cash of $43.8 million and debt of $157.9 million, the equity would be close to $1.533 billion. The IRR would stand at close to 4.96% in addition to a fair price of $21.70.

Source: Author’s Work

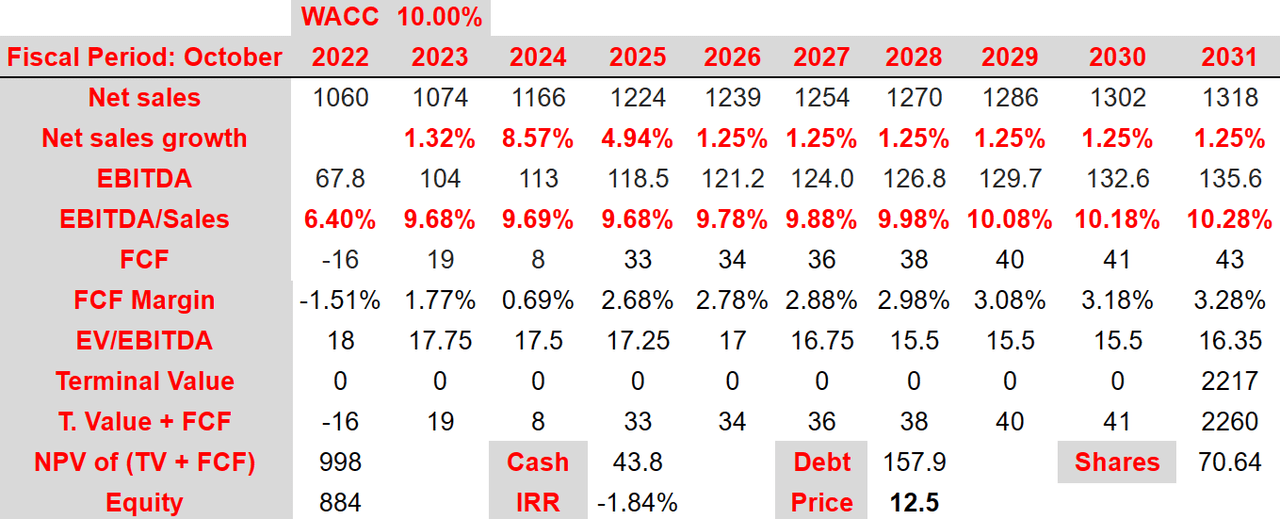

Bearish Case Scenario: Lack Of Supply, Lack Of Diversification, Or Adverse Weather Conditions May Lead To A Fair Price Of $12.5 Per Share

In my view, the largest risk for Mission Produce comes from a potential limited supply of avocados or other products from third-party growers. If third parties increase their prices, the company may have to invest in its own production capacity, which may take years and millions in capital expenditures. The company discussed these risks in the last annual report.

If we are unable to purchase sufficient volumes from third-party growers at acceptable prices or demand for our products were to increase in the future, we would need additional production capacity, which may take time, whether by purchasing additional fruit from third-party suppliers or by waiting for our younger avocado trees to bear fruit. These purchases may expose us to increases in short-term costs and additional production may expose us to additional long-term operating costs. Source: 10-k

Mission Produce also shows risks from the weather and natural disasters, as well as high temperatures that ruin crops. In addition to depending not only on the weather but also on regional economies besides having to constantly adapt to government requirements, the company has a fundamental and primary risk in its business model, because by dedicating itself exclusively to the production and distribution of specific food, it not only fails to diversify production, but also does not have a promising projection beyond the current demand for these products, both nationally and internationally.

Concentration of clients could also be quite detrimental for the company’s revenue growth. In the last annual report, management reported that sales to the company’s top 10 customers amounted to approximately 59% of the total sales for the year ended October 31, 2021. Under this scenario, I assumed that some of these clients may stop buying from Mission Produce, which would lead to less revenue growth than expected.

Under the previous conditions, I assumed 2031 net sales of $1.318 billion, net sales growth of 1.25%, an EBITDA of $135.6 million, and 2031 EBITDA/sales of 10.28%. I also included FCF close to $43 million with a FCF margin of 3.28%.

Source: Author’s Work

With an EV/EBITDA multiple of 16.35x, I obtained a 2031 terminal value of $2.2175 billion, which implied an enterprise value of $998 million. The equity would be close to $884.5 million, with a fair price of $12.5 per share and an internal rate of return close to -1.845%.

Conclusion

Mission Produce operates in the growing avocado market, and serves as a link between producers and consumers all over the world. I believe that further vertical integration of the company’s distribution and supply chain capabilities will likely bring free cash flow growth. I also believe that the new facilities in the United Kingdom to be opened in 2023 could serve as a catalyst for revenue growth. I obviously see risks from certain regulation of the sector, lack of third party suppliers or sources, and concentration of clients. With that, I believe that the company does look cheap at its current price mark.

Be the first to comment