dszc/E+ via Getty Images

This article continues my recent series on water utility stocks, the rest of which can be found at the links below:

1) American Water Works: The Short-Term Pain May Be Over

2) Essential Utilities: Despite Some Risks, The Name Says It All

3) Consolidated Water: Inconsistent Desalination and Wastewater Play

4) Artesian Resources: Time To Lock In Gains After A Great Run

MSEX: Small Size But Dependable Growth

Middlesex Water Company (NASDAQ:MSEX) is a small-cap water utility that has serviced New Jersey and Delaware since 1897. Through both regulated and non-regulated operations, it provides water treatment, distribution, and wastewater services to approximately 150,000 customers in New Jersey and Delaware with TTM revenue of $157M and a current market cap of $1.44B.

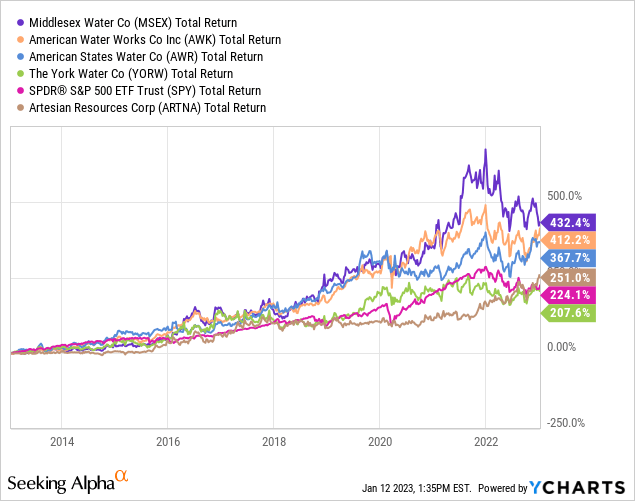

MSEX has been an absolutely fantastic performer over the past decade, besting all of its peers in total returns. While its valuation has gotten steeper over time, it’s helpful to understand that it deserves to trade at a premium multiple based on its historical performance.

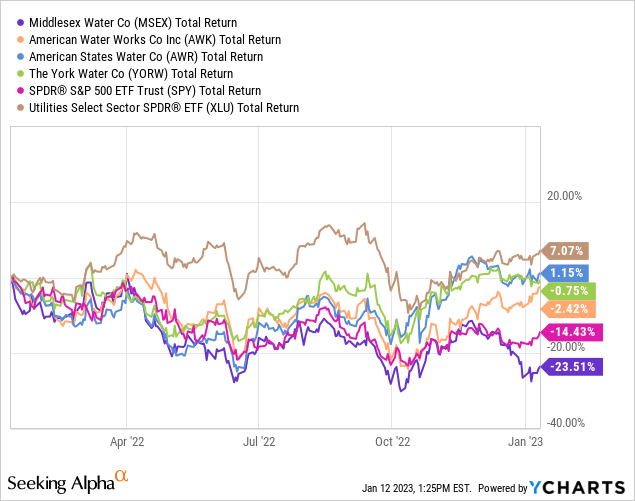

However, a slow-growth stock with a relatively low yield and a steep valuation isn’t a winning combination in a rising rate environment, so 2022’s rapid interest rate and Treasury yield increases finally forced MSEX’s price back down to earth. In addition to underperforming its peers over the past year, it has been the only water utility stock that has underperformed the S&P 500 (SPY) as well.

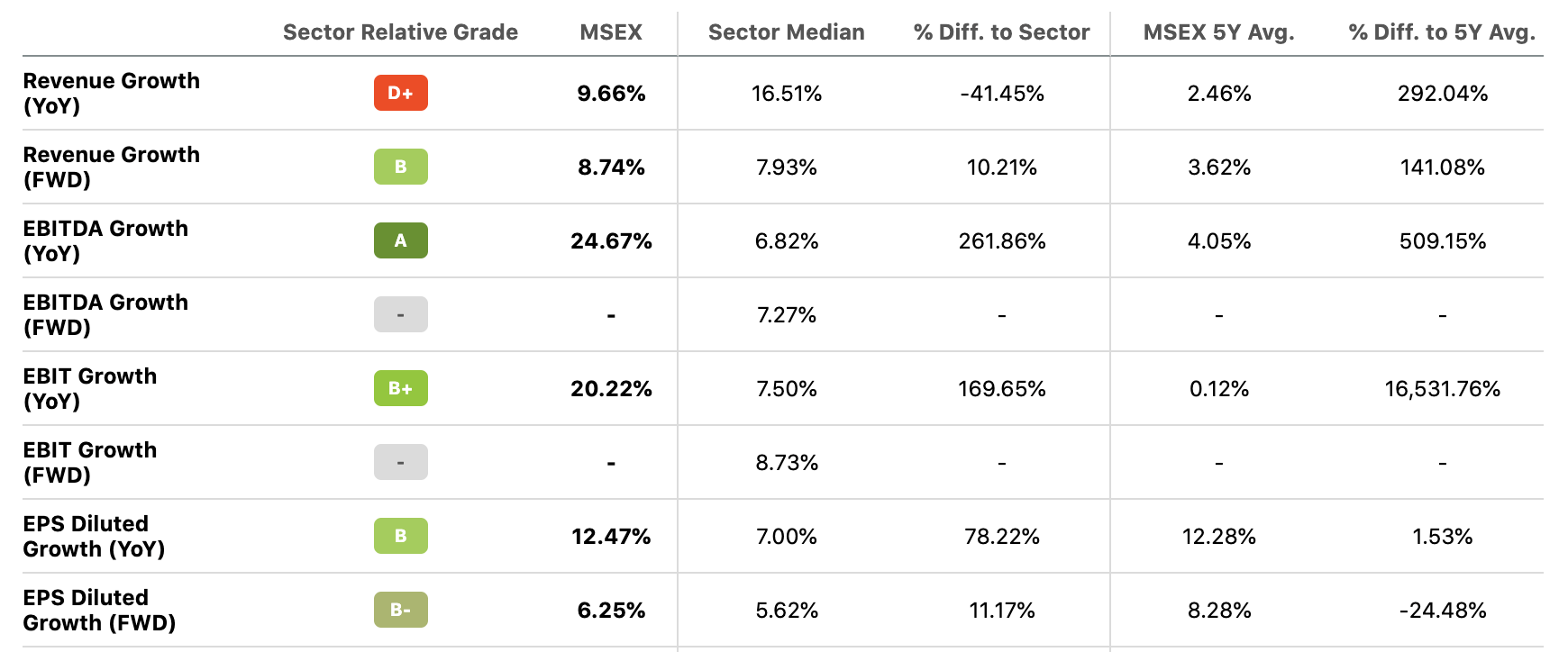

Despite the poor share performance, MSEX has had an excellent year, delivering nearly 10% revenue growth and 12.5% EPS growth YoY, compared to average annual revenue growth between 2-3%.

MSEX 2022 Growth (Seeking Alpha)

Furthermore, its most recent Q3 2022 results were even stronger, with operating revenues up almost 20% YoY and net income up 24.5% YoY. But now heading into a recession with inflation likely having peaked already and on the downslope, I think it’s likely that these results could mark peak growth for MSEX in this economic cycle.

Valuation

This begs the question of whether MSEX is finally trading at an attractive valuation given its strong TTM results and forward growth outlook amidst a significant dip in its share price.

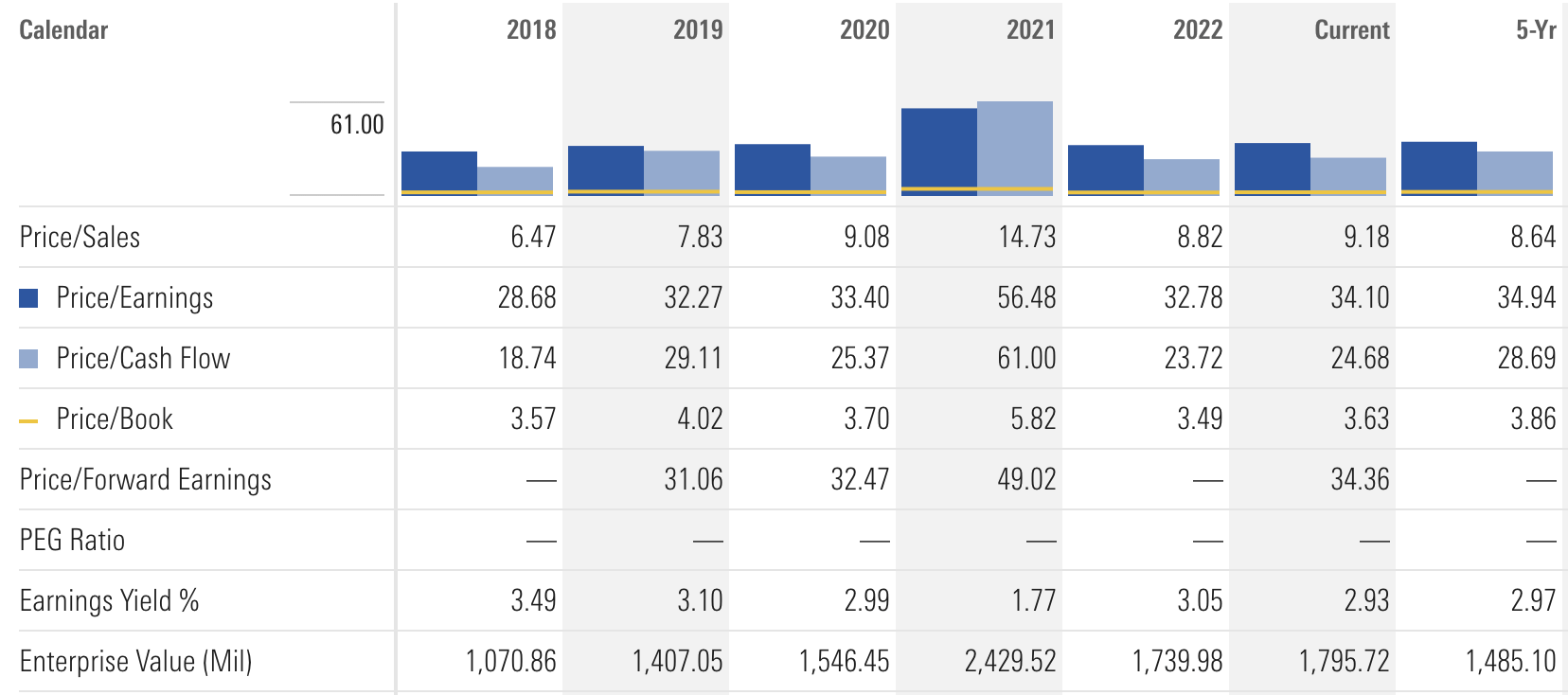

MSEX 5-Year Valuation (Morningstar)

Looking at the numbers, we can see that MSEX’s price to sales ratio skyrocketed from 6.47x in 2018 to 14.7x in 2021. Even after 2022’s 24% share price drop, MSEX’s current 9.18x sales multiple is approximately 6% higher than its 5-year average of 8.64x. On the plus side, its PE and PB levels are slightly below those averages, although in this case the 5-year averages themselves don’t give us a great idea of MSEX’s fair value simply because the 2021 figures are so elevated and therefore disproportionately skew the averages upward.

Of course, all of these numbers are high for a relatively slow-growth water utility,

Considering MSEX’s strong revenue growth outlook, at nearly 9% forward revenue growth and 6% forward EPS growth, which places it ahead of most of its water utility peers, I’m inclined to view shares as about 5-10% overvalued at their current level around $81.

Dividend Strength

MSEX’s current yield supports the case for overvaluation as well, with its 1.54% yield sitting at the lower end of its long-term historical levels and possibly on an uptrend, which would be bearish for MSEX’s share price but would make sense as investors demand higher yields from defensive equities when risk-free Treasury yields are so much higher.

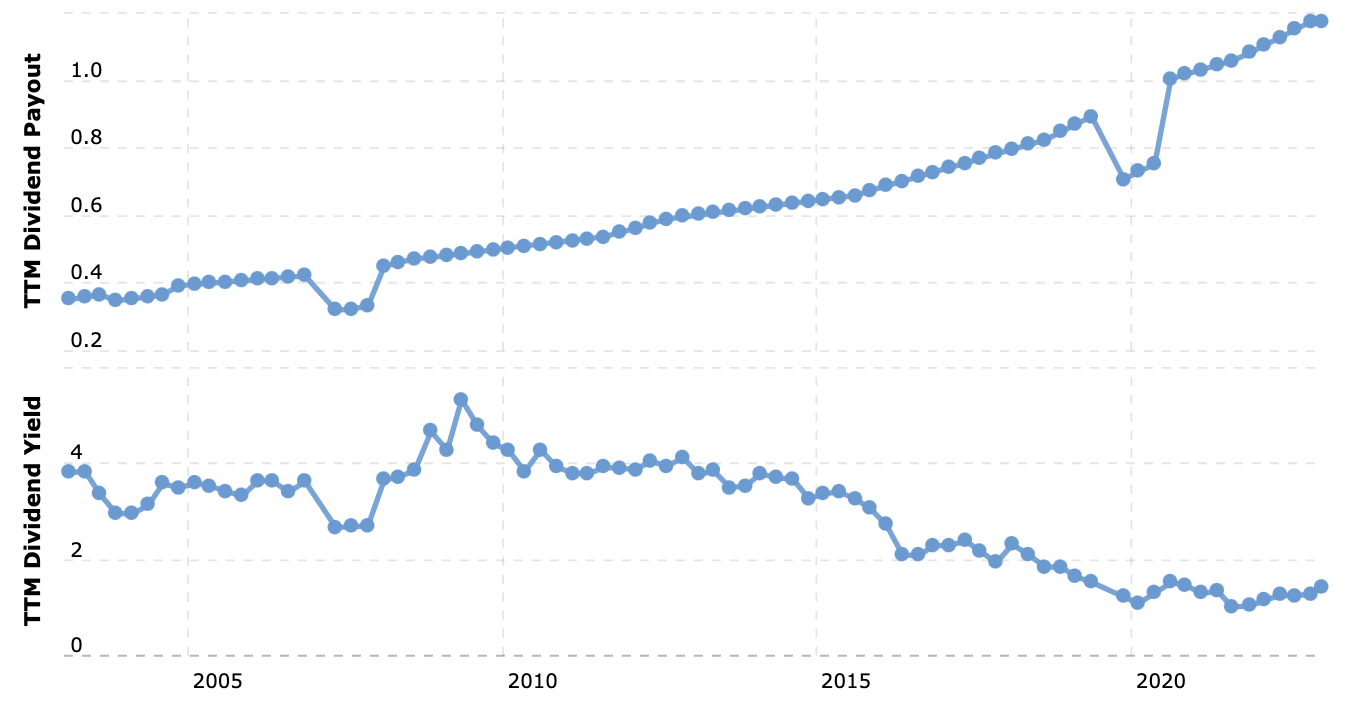

MSEX Historical Yield (macrotrends.com)

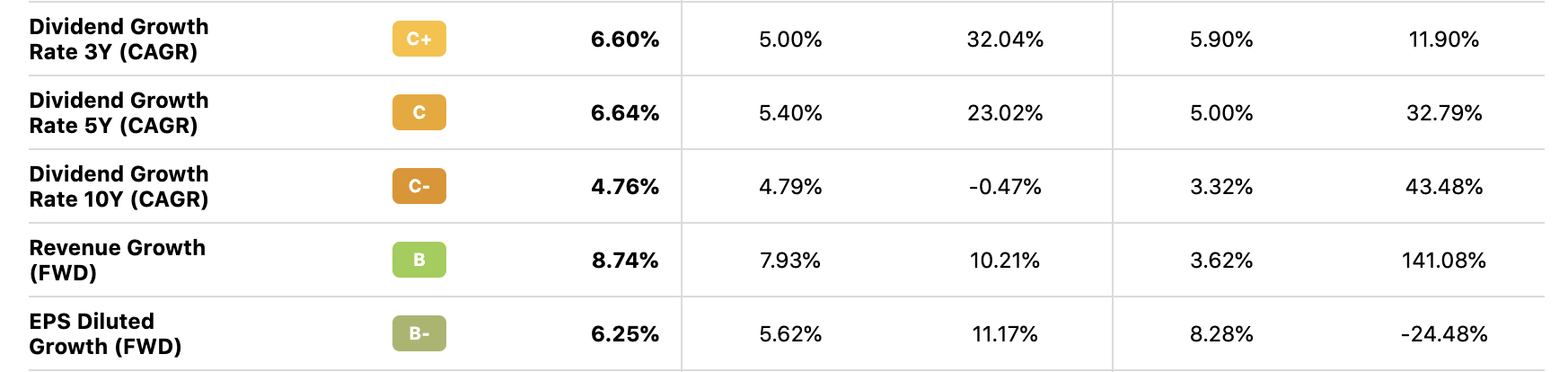

Perhaps unsurprisingly given Middlesex’s EPS growth, the dividend is well-covered with a sector-standard payout ratio of 62%, similarly acceptable long-term debt (relative to its market cap) of $300M, and its recent 6-8% dividend hikes are much higher than its 10-year average dividend CAGR of 6.64%.

MSEX Dividend Strength (Seeking Alpha)

In a pre-2022 ultra-low interest rate environment, these dividend stats might have led me to view MSEX as fairly valued, since its higher recent dividend growth might warrant a premium over its historical valuation. But in the current environment with the Fed funds rate projected to rise to 5.25%, unfortunately a ~1.5% yield can’t put a strong floor below MSEX’s stock price like it used to, regardless of how strong its dividend growth rate might be.

Conclusion

With a low dividend yield and an expensive valuation, I can’t recommend buying MSEX at current levels even with its strong growth outlook. But with its 50-year history of dividend hikes, market-beating long-term performance, and a low risk profile, I certainly think it warrants a hold rating for long-term investors on the current drawdown, with a margin of safety to add shares at fair value below $75 (7.5% below the current price) and a strong buy rating below $70.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment