carlosgaw/E+ via Getty Images

Natural Alternatives International (NASDAQ:NAII) is a contract manufacturer of nutritional products, and the owner of a brand of beta-alanine.

As a contract manufacturer, it suffers from low competitive advantages, volatile revenues, low margins and high operating leverage. Its SG&A structure is relatively controlled, but its manufacturing facilities are located in high cost areas.

Although NAII is trading at a price to 5-year average earnings below 10, and a TTM P/E ratio of less than 7, I don’t view NAII as a good investment opportunity. In addition to the relatively unattractive competitive conditions of the business, I believe NAII will suffer in the mid-term from increased unutilized CAPEX, compounded by lower revenues and margins generated by bullwhip effects on its downstream markets.

Note: Unless otherwise stated, all information has been obtained from NAII’s filings with the SEC.

Historical operations and competitive conditions

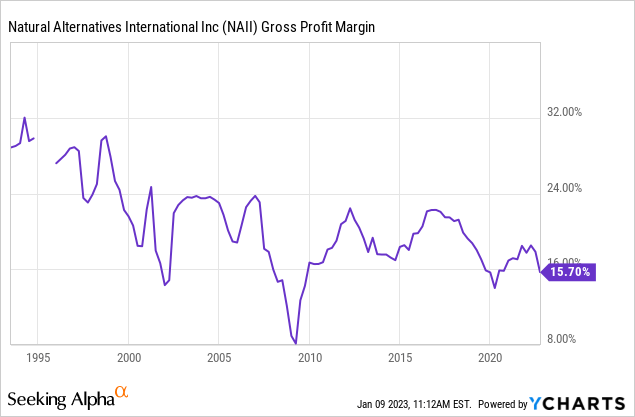

Low margin contract manufacturing: 90% of NAII’s revenues are generated by its contract manufacturing operations. The company manufactures pills, tablets and powders for other companies.

This business has very low and volatile margins. The company’s combined gross margins rarely reach 20%, and have consistently moved in the 10% to 20% range. This signals a lack of competitive strength.

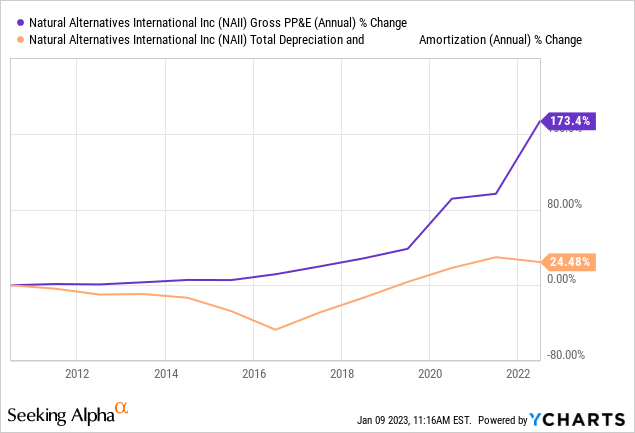

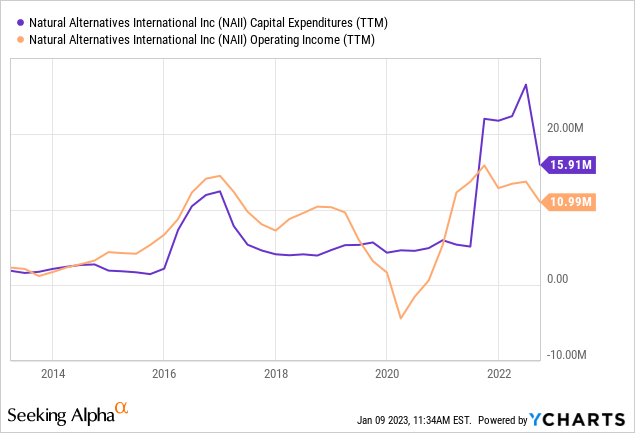

Underestimated depreciation as a percentage of PP&E: Despite the company’s CAPEX spurs of 2016 and 2021, NAII has not increased its depreciation expenses, which may signal an overstatement of its accrual profits.

High cost manufacturing locations: NAII’s products do not seem to be high tech. Despite being nutritional supplements, it seems that their production does not differ from general food production (rather than the more strict drug manufacturing process). For that reason, it surprises me that NAII has its manufacturing facilities located in Switzerland and California, two of the most expensive markets on the planet. This probably contributes to NAII’s low gross profit margins.

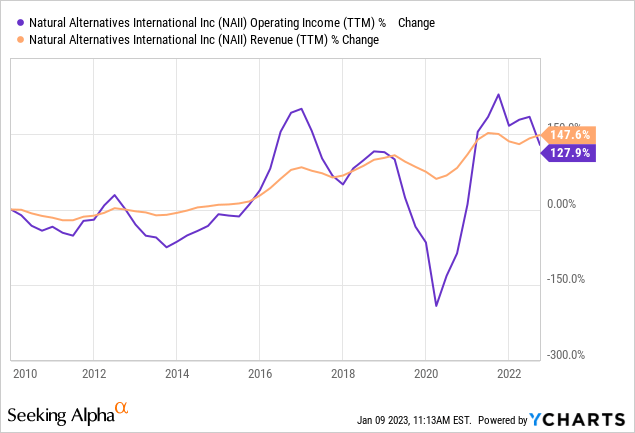

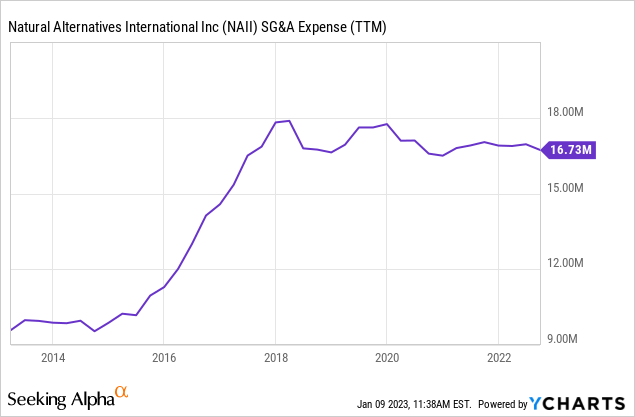

Operating leverage despite small SG&A structure: Despite the low gross profit margin, NAII’s operating margins are not as low as one would expect. The reason is that the company has relatively lean SG&A operations, of some $16 million yearly. The company’s salesforce consists of only 16 people, against 350 employees in manufacturing or 50 employees in R&D.

However, the low gross profit margin, combined with the SG&A expenses, generates operating leverage.

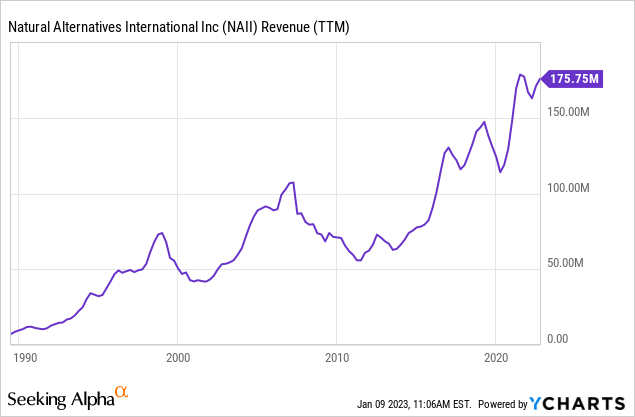

Volatile revenues tending to bullwhip effect: NAII’s revenue history shows a positive trend, although punctuated by boom and bust episodes. Reading the MD&A section in the 2010 and 2015/17 period, the main factor mentioned is inventory buildups downstream. With heavy customer concentration (reaching as much as 50% in FY21 and 35% in FY22) NAII is exposed to bullwhip effects.

A somewhat more protected beta-alanine business: NAII also commercializes its own brand of beta-alanine (10% of the company’s revenues), a nutritional product used mainly by athletes and gym enthusiasts. Although the company puts a lot of emphasis on its patents, they do not enjoy a monopoly on the product. The segment’s operating margins, also capped at around 10% (before unallocated corporate expenses) also signals lack of a competitive advantage in this business.

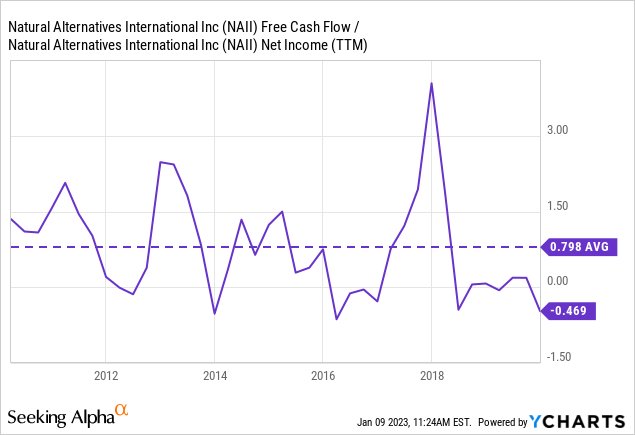

Not great FCF conversion: Considering the underestimated depreciation expenses, and lack of competitive strength, which makes the company prone to accumulate working capital, it is not surprising that NAII’s FCF conversion has not been in line with its reported earnings.

Relatively protected financial condition: Against current cash holdings of $12 million, plus inventories and receivables for $54 million, the company has $17 million in payables and $10 million in debts, hedged at a 2.4% rate. NAII also has access to a credit facility for up to $20 million, that is undrawn as of 1Q23.

Not fantastic capital allocation: NAII’s CAPEX decisions have coincided with record revenues, followed by lower revenues generated by the mentioned bullwhip effect. This signals lack of prevision of the industry’s capital cycle.

The company has continued investing in its high cost manufacturing regions, for example with the acquisition of a facility in Carlsbad for $18 million last year.

Fortunately, the company has not diluted its shareholders and has not engaged in value destroying acquisitions.

Perspectives

Higher depreciation after CAPEX increase in 2021: The company started a new capital investment cycle at the end of 2021 that has increased its gross PP&E. Although I showed a lack of correlation between depreciation and PP&E, the former should rise to reflect the higher level of the latter. This will increase NAII’s operating leverage.

Probable downturn ahead caused by inventory bloating downstream: If history is to repeat, we should see a decrease in NAII’s revenues caused by inventory buildup on its downstream markets. As Nassim Taleb says “There is never a shortage without a glut”. A revenue decrease, added to new capacity will contract gross margins, aggravated by operating leverage at the SG&A level.

Conclusions

NAII’s prospects are not great, and my understanding is the company will go through a cyclical downturn. Overall historical performance is not particularly attractive, given the lack of a competitive advantage, and no signals of managerial ability to invest capital to gain those advantages.

Although NAII trades at a discount multiple (P/E ratio of 7x to current earnings and P/E ratio of 10 to 5-year average earnings), I prefer to wait and buy in a cycle trough, or closer to it, than now.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment