lcva2

Thesis

We updated investors in our previous Microsoft Corporation (NASDAQ:MSFT) article to consider waiting for a validated bullish reversal for a more conservative entry.

Unfortunately, the bullish reversal didn’t arrive. Instead, it only brought upon bears who correctly anticipated CEO Satya Nadella and team could release weak guidance, given the significant macro headwinds (coupled with the Street’s optimism).

Hence, further value compression in MSFT to de-rate its More Personal Computing segment was justified, with the segment’s execution likely significantly de-risked accordingly to Trefis’ sum-of-the-parts (SOTP) valuation.

The company’s guidance reflecting broad-based deceleration, particularly in its Cloud segment, demonstrated that MSFT’s valuation could continue to trade in a tight range. As a result, we assess that its valuation is close to the lows last seen in the 2018 and 2020 bear markets. Also, it’s re-testing its critical 200-week moving average, which should also attract long-term buyers to stanch further downside momentum from the bears.

Notwithstanding, we also observed that SaaS stocks had been broadly de-rated after recent poor releases from MSFT’s industry peers, as Fortinet (FTNT) and Atlassian (TEAM) got “destroyed,” given their poor guidance.

Therefore, the market is looking for MSFT to demonstrate market leadership in uncertain times to lift the buying sentiments of its software peers. With MSFT cautiously perched against its “final defense line” before a potential further selloff, a validated bullish reversal (still pending) in MSFT could telegraph confidence in software stocks after this week’s compression.

While we remain cognizant of the risks of a broad industry de-rating impacting MSFT, we believe the reward/risk of MSFT at these levels seems favorable.

Maintain Buy.

Microsoft Cloud Needs To Reverse Its Below-Trend Growth

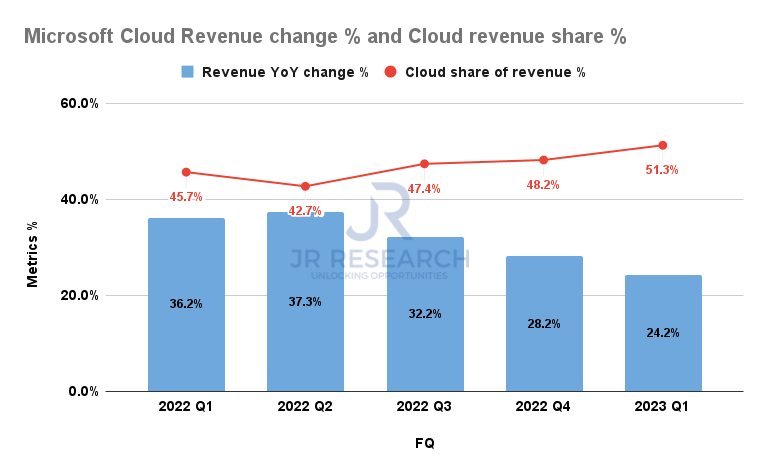

Microsoft Cloud Revenue change % (Company filings)

Microsoft Cloud accounted for 51.3% of FQ1’23 revenue, up from Q4’s share of 48.2%. Therefore, Cloud’s increasing importance to Microsoft’s valuation cannot be further emphasized and will be carefully parsed by the market moving forward.

With Nadella putting increasing emphasis on the interoperability of Microsoft’s Cloud ecosystem, it has helped Microsoft avoid even more pain as the PC market slumped significantly.

In a recent interview with Stratechery, Nadella highlighted his vision of why Microsoft is working closely with Meta Platforms (META) in realizing the broad concept of the metaverse. He accentuated:

I also want our application experiences in particular, to be available on all platforms, that’s very central to how our strategy is. For example, when I think about the Metaverse, the first thing I think about is it’s not going to be born in isolation from everything else that’s in our lives, which is you’re going to have a Mac or a Windows PC, you’re going to have an iOS or an Android phone, and maybe you’ll have a headset. So if that is your life, how do we bring, especially Microsoft 365, all of the relationships that are set up, the work artifacts I’ve set up all to life in that ecosystem of devices? – Stratechery

However, Microsoft Cloud’s revenue was not immune to the macro headwinds, as its growth decelerated to 24% in Q1, down markedly from Q4’s 28%.

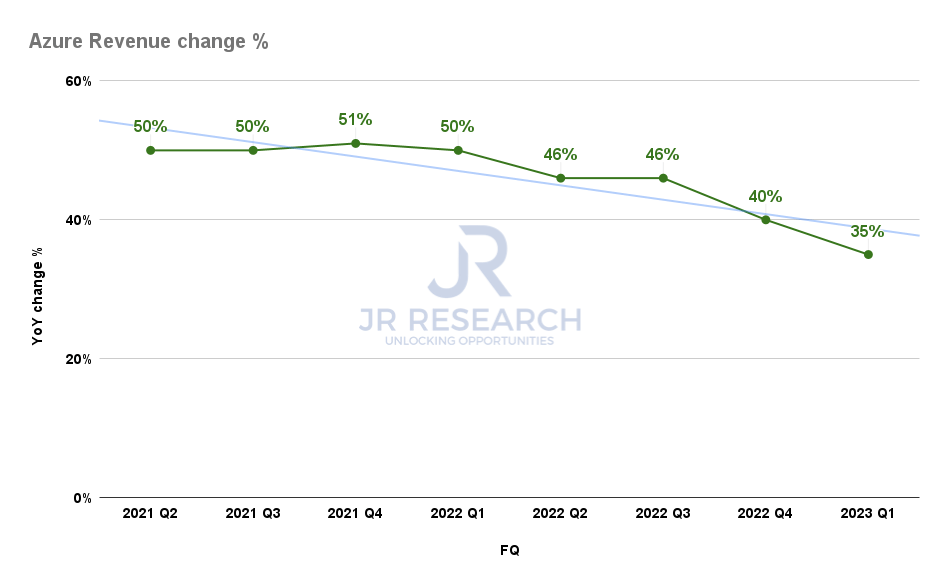

Azure Revenue change % (Company filings)

Notably, Azure’s Q3 growth of 35% YoY, down from Q2’s 40% YoY, markedly impacted the company’s momentum. As a result, it has placed Nadella’s Cloud-focused strategy under more pressure, given MSFT’s premium against the broad market.

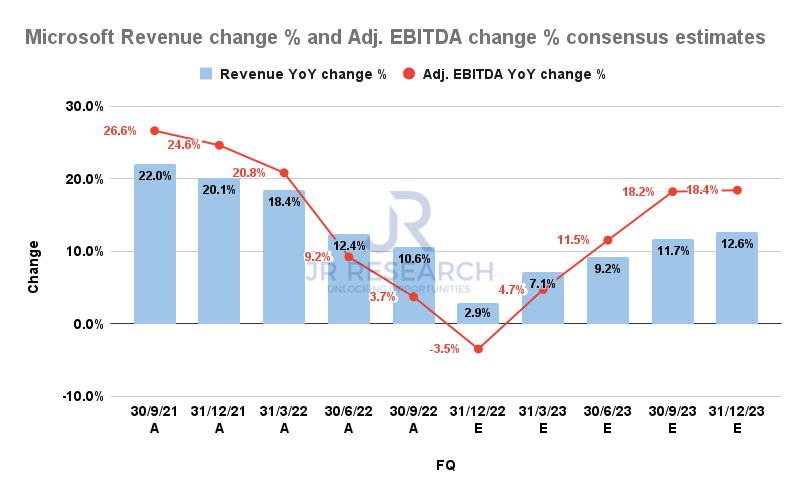

Microsoft Revenue change % and Adjusted EBITDA change % consensus estimates (S&P Cap IQ)

As a result, Microsoft’s FQ2 guidance (quarter ending December 31) implies total revenue growth of 2.2% on revenue of $52.9B (midpoint). In addition, the revised consensus estimates indicate topline growth of 2.9% YoY, down from previous estimates of 9.2%.

In other words, Microsoft and Street analysts were too optimistic about the headwinds that the company needs to navigate. Notwithstanding, analysts remain convinced that Microsoft’s growth could bottom out in FQ2 before recovering through 2023.

We think there are a few possibilities that corroborate the Street’s optimism. Energy costs, highlighted as a critical factor that impacted its Cloud margins, have continued to fall through October.

DXY price chart (weekly) (TradingView)

Furthermore, the dollar index has also pulled back from its September highs. Hence, it could mitigate the forex headwinds that impacted its growth cadence in the previous quarters.

However, assessing whether the pullback could be sustained is still too early. Still, it’s constructive to help mitigate the macro challenges that faced MSFT in FQ2.

Is MSFT Stock A Buy, Sell, Or Hold?

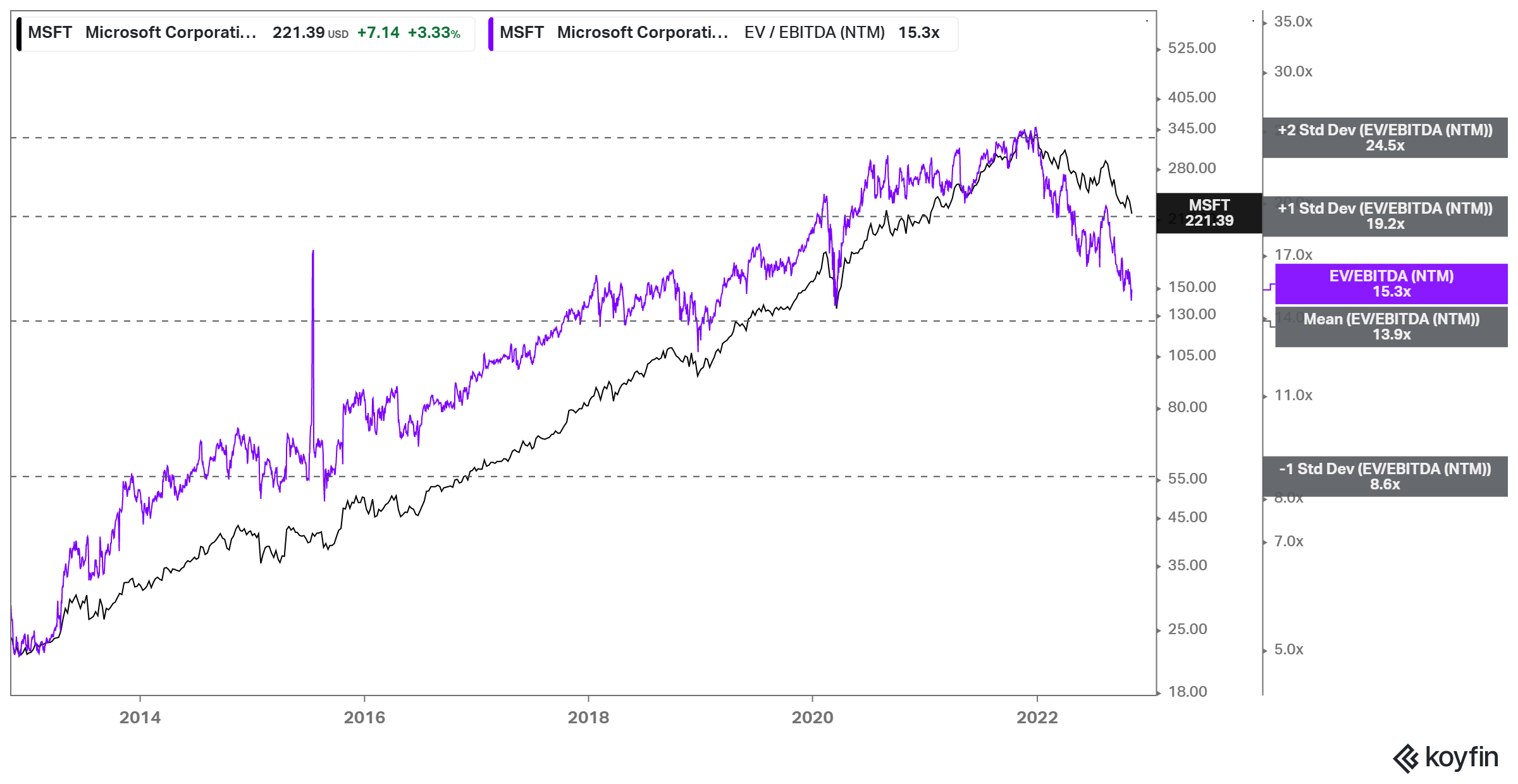

MSFT NTM EBITDA multiples valuation trend (koyfin)

With an NTM EBITDA multiple of 15.3x, it has fallen closer to its 10Y mean of 13.9x. We believe MSFT is no longer overvalued.

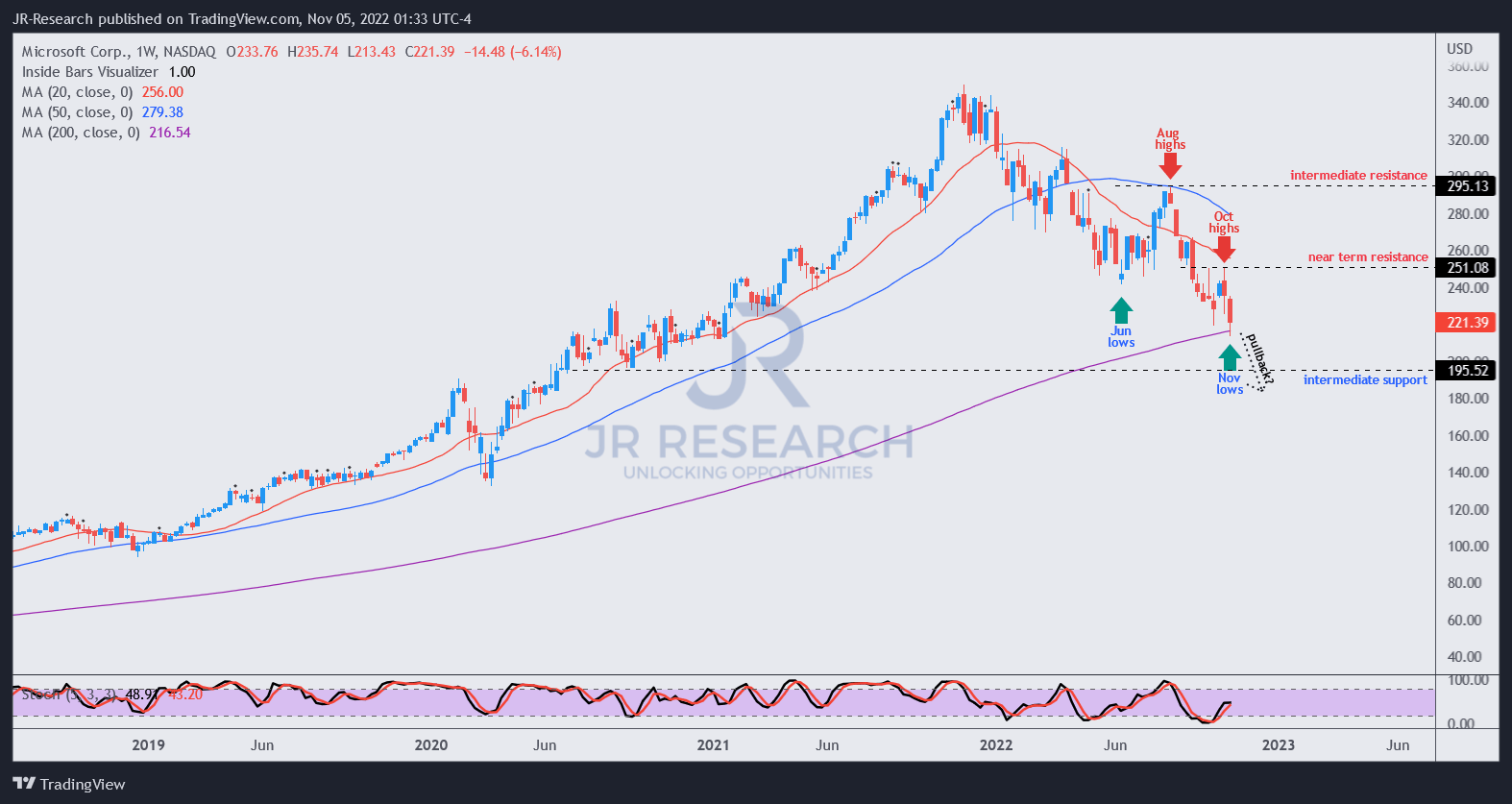

MSFT price chart (weekly) (TradingView)

But that doesn’t mean MSFT cannot face more value compression. Its valuation is more reasonable but still not undervalued. Hence, it’s possible for the market to de-rate its growth premium further if it anticipates a worse-than-expected recession that could hurt its cloud computing momentum further.

Notwithstanding, we gleaned that MSFT re-tested its 200-week moving average (weekly), a critical defense zone that long-term buyers are expected to hold vigorously.

Hence, we believe investors who can stomach near-term volatility should find it reasonable in anticipation of buying support at the current levels by adding exposure.

Despite that, a further pullback toward its intermediate support is possible, improving its reward/risk further, and justifying more aggressive buying.

Maintain Buy, but we urge investors to exercise prudent capital allocation strategies to capitalize on potential downside volatility.

Be the first to comment