SweetBunFactory/iStock via Getty Images

On Wednesday, Micron (NASDAQ:MU) issued a press release stating it would further reduce CapEx, wafer starts, and bit supply after realizing the medium-term outlook has further deteriorated. This has brought about many questions. First and foremost, is the FQ1 guide in danger? Secondly, what does this mean for the recovery investors were expecting in FQ3? And finally, can Micron maintain its market share and technology leadership with such drastic actions? These are all perfectly legitimate questions to ask, and I intend to address them all. In the end, Micron is not only doing the right thing, but the other end of this bottom will be something for the ages.

Memory Cycles Need Contrast

I never get political in my articles, but some political science is relevant today. With the results of the midterms in the US showing expectations were misplaced on both sides in various corners of the election world, it brought about some basic political principles. One such principle is the quality of a candidate, but more specifically, the contrast between two opposing candidates. When the non-incumbent candidate is brought forth and doesn’t have a severe contrast (read: is more middle-of-the-road) from the other candidate, it doesn’t create an enthusiastic base. Instead, it becomes a vote for the “lesser of two evils” or simply the status quo (incumbent). Disappointment for the challenger soon follows.

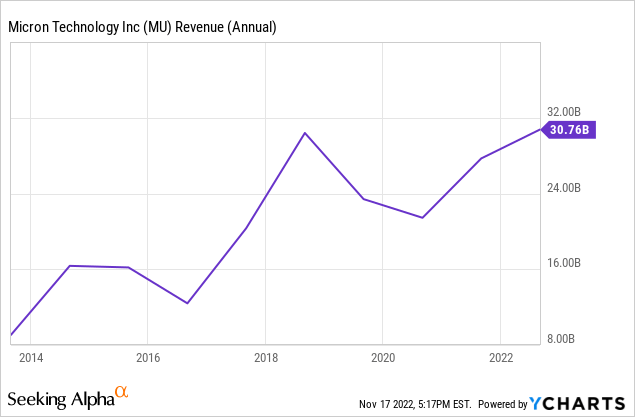

The same thing has been playing out for Micron over the last few years. There hasn’t been a complete cycle one can point to since 2018. Instead, there’s been very little contrast between the highs and lows, but, more importantly, the cycle’s amplitude flattened. And this would be a good thing if not for the forecast for FY23 from the company for an expectation of less than $20B in revenue. Typically we see higher revenue highs and higher revenue lows through the course of a cycle compared to the last. But new revenue and financial highs were not in the cards; they only matched the last highs

While Micron’s stock saw new highs, it wasn’t because of a multiple rerating; it was because book value continued to climb – only the valuation input changed.

No one could point out where the ‘oompf’ for a new cycle high would come from; it was more lukewarm than in the past.

This produced little contrast with the preceding cycle and, thus, no business momentum to carry the stock or the company’s book value much higher. It was only the status quo candidate of cycles.

Of course, we can blame the pandemic, supply chain constraints, and the resulting lack of downstream components. There was a lot of give and take for why it didn’t happen, and it was all pretty much out of the hands of the executives at Micron.

But now, we’re seeing a more clear-cut downcycle emerge. Just six weeks ago, it was set to be pretty steep, but it was going to be rapid. A two, maybe three-quarter bottom was in the cards when management said, “Following a weak first half of fiscal 2023, we expect strong revenue growth in the second half of fiscal 2023 as bit demand rebounds.”

This would set the company and industry for a quick but contrasting cycle, providing a bit of momentum to push the next up-cycle into orbit above the ~$30B ceiling.

This Week’s Press Release Created Needed Contrast

But this is where Micron’s latest press release comes in; the outlook has now gotten worse.

The key parts of the press release include the following:

…in response to market conditions, the company is reducing DRAM and NAND wafer starts by approximately 20% versus fiscal fourth quarter 2022. These reductions will be made across all technology nodes where Micron has meaningful output. Micron is also working toward additional capex cuts. In calendar 2023, Micron now expects its year-on-year bit supply growth to be negative for DRAM, and in the single-digit percentage range for NAND.

Recently, the market outlook for calendar 2023 has weakened. In order to significantly improve total inventory in the supply chain, Micron believes that in calendar 2023, year-on-year DRAM bit supply will need to shrink and NAND bit supply growth will need to be significantly lower than previous estimates.

There’s quite a bit to unpack here. First, a 20% reduction in wafer starts is a considerable amount. It’s hard to understate this. In FQ2 ’19, the company idled 5% of its wafer starts, then 10% in FQ3 ’19 before returning to full utilization. So 20% is a considerable amount and is quite meaningful.

The impact on Micron won’t be trivial. Partially idling fabs is a massive hit to costs of goods sold through the effect of overhead costs. A fab runs at full capacity to overcome the fixed overhead costs associated with running a fab. The lights and electricity stay on regardless of 99% or 80% utilization. Workers and techs are still needed to run the equipment.

FQ1’s Guidance Risk

However, what needs to be considered is whether this move was already baked into the guide they presented on the FQ4 call. Why wasn’t there any mention of a guidance revision in the press release if it wasn’t?

But take a step back for a second.

For starters, the company had less than two weeks left in FQ1 when it issued the release. Therefore, even if they immediately pulled back utilization by 20%, it already has the bits it needs to fulfill the quarter’s orders. At this point, the quarter is on autopilot, and the timing of customer payments comes into play to determine exact revenues.

Additionally, CEO Sanjay Mehrotra already foreshadowed this three paragraphs into his prepared remarks on the FQ4 earnings call.

We are responding decisively to this weak environment, by decreasing supply growth through significant cuts to fiscal 2023 CapEx and by reducing utilization in our fabs.

It likely wasn’t 20% at the time because it wasn’t for all nodes, as noted further into the prepared remarks, but it was floated, nonetheless.

…we are reducing utilization in select areas in both DRAM and NAND.

A Worse FQ2/FQ3 And Pushing Out The Recovery

But this utilization rate will certainly affect FQ2.

Initially, the company guided FQ2 to be sequentially flat to FQ1 by saying, “we currently expect revenue [in fiscal Q2] to be in a similar range as fiscal Q1 with bit shipments up.”

This will no longer be the case.

Therefore, FQ2 is in for a sequential decline.

But instead of filling up inventory, the company simply won’t be producing those chips. When you run full utilization and utilize inventory, it makes whatever is brought off the lines and shipped more expensive because no one is paying for the inventoried product, not yet, at least. Reducing wafer starts has the same impact, except instead of placing it in inventory, it just never gets manufactured.

The negative is you don’t get to make it back up when you sell that bloated inventory later. But the positive is you don’t have to work down inventory in two or three quarters; you immediately start shipping a fully utilized production line.

So it’s a near-term hit for a quicker and more pronounced recovery.

This brings about the concern for FQ3, where the recovery was supposed to take place according to details from several weeks ago.

In the latter half of the press release, it’s clear Micron is pushing the recovery from FQ3 into FQ4 or FQ1 of ’24.

It seems this was to get out in front of a revision of estimates for FQ2 and FQ3.

Less Inventory Leads To A Steeper Recovery

However, this remains to be seen as the actions being taken may contribute to a shorter downturn, as counter-intuitive as that sounds. First, it’s not building up its inventory as much as expected. As customers work down their inventory, Micron is not working its inventory up. In a sense, Micron is pinching the hose at the source. Whatever water is left in the hose is the only water remaining until it decides it’ll open up the conduit. Therefore, when it’s time for customer demand to return after downstream inventory is used up, Micron will be working down far less inventory.

This is how the down cycle gets limited and how pricing can turn on a dime. Customers won’t be able to order and get something out of inventory; instead, Micron says, “Well, you’ll have to get in line. There isn’t much available; you’ll have to wait for us to manufacture it.” This puts pricing back in Micron’s hands much more quickly.

CapEx Reductions Emphasize This

Couple these utilization changes with further CapEx reductions, and things really bring the up cycle into view. Not only will Micron shorten the down cycle by limiting its inventory carry, but when demand returns, bit growth will be some of the lowest and most divergent to demand we may ever see (remember that political candidate contrast).

Management will either delay building construction or delay WFE shipments. But, there isn’t much choice, as it already said, “CapEx would be lower if it were not for more than doubling our construction CapEx, year-over-year… to meet the demand for the second half of this decade, [and] for EUV lithography systems to support 1-gamma node development.” So I don’t expect them to go lower than $7B in FY23 CapEx, which I planned for in a worse situation in my FQ4 earnings analysis.

What About Risking Its Technology Leadership?

This begs the question about technology leadership.

I don’t expect the company to risk its 1-gamma node development with these CapEx cuts. That will be a spending priority and the last to go. However, it will slow its 1-beta node ramp to limit bit growth (which comes naturally with each progressive node).

WFE CapEx will decline nearly 50% year-over-year and reflects a much slower ramp of our 1-beta DRAM and 232-layer NAND versus prior expectations.

– Sanjay Mehrotra

Don’t confuse a slower ramp with a slowing of node transitions. Development, tape out, WFE shipments, and larger cleanrooms will continue for 1-gamma node-needed initiatives. The company can add fewer lines to make up for the additional floor space in the cleanroom needed to transition to advanced nodes. This creates a natural wafer start reduction process when transitioning (you can read more about that process here). However, this isn’t the best approach as it puts the company behind when demand does inevitably return.

More to the point, technology leadership isn’t necessarily about how much overall CapEx is spent; it’s about where it’s spent. The leadership part comes from being able to engineer smaller bits, crazier pitches, and the ability to make the lithography happen at show time. Micron has been able to do that through R&D and well-in-advance experimenting with EUV. These cuts and actions are about reducing bit supply growth and available bits on the market.

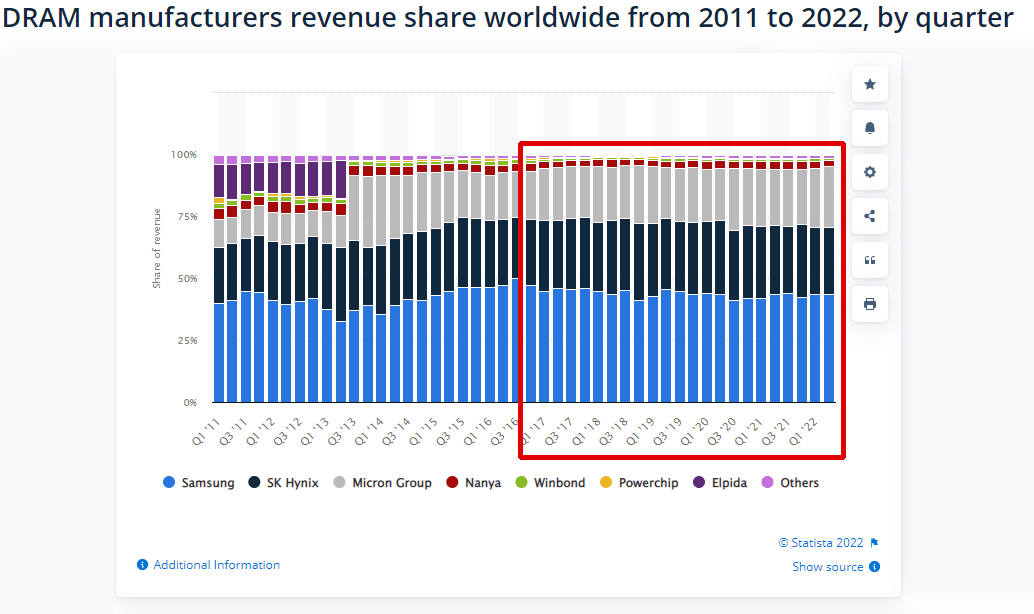

The risk is cutting too many bits from its supply and losing market share, as I alluded to with the fewer lines a second ago. The company had sided on reducing bits from the market in the last five years (when the oligopoly’s power emerged) but has still maintained or gained market share. SK Hynix has suffered the most through these years regarding market share.

statista.com

There Are Pros And Cons To This Extreme Strategy

While bulls do not appreciate the news as the memory outlook has worsened and Micron is taking more drastic supply measures, the same painful actions may allow Micron to surge back when demand returns. The problem for the stock in the near-to-medium term is the market looks two-to-three quarters out, and it was in the window to be pricing the recovery expected in FQ3 and FQ4. However, this puts 2023 on notice for the majority of the year.

Micron may be using this press release to signal to its competitors and its clients as a warning for what’s to come. This would be especially true if FQ2’s guidance isn’t revised down at all or at least meaningfully. It may have been an excellent tactic to change some client decisions in the coming months. That being said, the likelihood Micron’s fiscal year is revised down further than it was initially forecast is the probable outcome.

The goalposts move now to the recovery, which has been traded off for a well-prepared, more severe upturn from Micron’s perspective. Managing inventory with drastic moves outlined in the press release will allow the company to bring itself closer to ramping up bit shipments, as the “last” leg of inventory in the supply chain will not be bloated. So while the stock and fundamentals have been pushed off, the angle of attack for the recovery has just increased quite a bit, making the stock and financials set for a rapid take-off when it does happen.

Be the first to comment