Lemon_tm

Meta Platforms (NASDAQ:META) reported large-scale layoffs on Wednesday Nov. 09 morning, affecting roughly 10% of the company’s almost 90 thousand employees. That’s on the back of the company’s valuation dropping roughly 75% in just over year, from a seemingly unassailable position as recently as September 2021.

Undeniably, while economic concerns and Apple’s privacy changes have affected the company, the number one cause of that share price decline is Meta Platform’s focus on the metaverse. Mark Zuckerberg has admitted that himself.

Voting Shares and History

The problem that Meta Platforms has is that Mark Zuckerberg’s hand can’t be forced. He owns almost 55% of the voting rights despite having 13% of the outstanding shares of the company. Despite a purported fiduciary duty of CEOs, it’s an incredibly high bar to prove a CEO isn’t operating in shareholder’s best interests. In the meantime, Meta Platforms continues to spend.

The company’s operating loss from the metaverse is expected to be a massive ~$13 billion in 2022. The company has said it expects that to expand substantially in 2023. For a company with roughly $40 billion in annual operating income that’s enormous. The company’s continued hiring of AR/VR employees highlights that the recent layoffs aren’t focused on stemming the specific losses of the metaverse business.

The company’s expenses are expected to expand substantially from ~$86 billion in 2022 to $98-99 billion in 2023. The company’s guidance for Realty Labs operating losses to grow significantly year over year implies almost $20 billion in likely operating losses for 2023. Due to Mark Zuckerberg’s infatuation and voting share ownership, shareholders can’t stop it.

Metaverse Is A Fictitious Dream

The company’s problem is that the metaverse doesn’t exist in any true form. Even optimistic predictions about Metaverse adoption, such as that the majority of the population will be using it in some way, have 2030 as the earliest date. It’s worth noting that for a number of other game changing technologies, like self-driving, adoption has consistently been slower than expected.

Our view has always been that full self-driving wouldn’t be a game changer for any company’s financials until it completely replaced the need to use a steering wheel. So far that has proven to be correct. Our view is the same for the Metaverse where, until it becomes a place, technologically, that people can emulate real life, it won’t be game changing.

So far, there’s no indication of that happening. The company’s operating loss continues to increase as it works to create a technological marvel, but so far, the company has given no indication of turning that to profits. The company has announced that will expand substantially into 2023.

While it’s clear that the company dominates in this emerging market, with its Oculus headset, the company is spending a substantial amount of money to grow the metaverse. So what’s fictitious here besides your legs in the metaverse? A game plan, clearly laid out, to ever come close to achieving the dream Mark Zuckerberg has.

Core Platform Results

Meta’s financial performance is based on the continued strength of its core platform.

Meta Investor Presentation

Meta Core Platform – Meta Investor Presentation

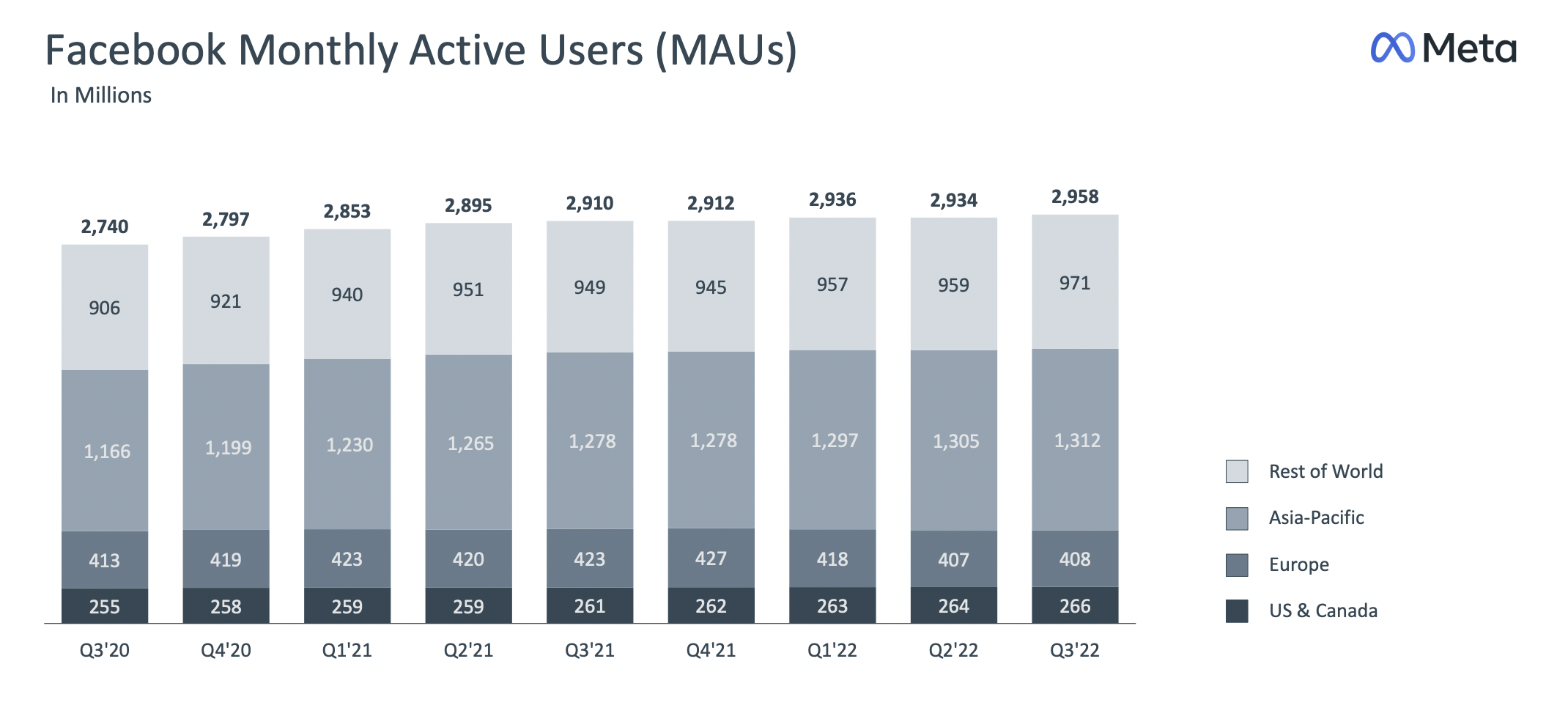

Facebook’s monthly active users in the most recent quarter was almost 3 billion users, representing almost half of the world’s position. As is clear from the above chart, the company’s properties are remaining strong with steady 5% YoY growth for each of the last 2 years. Facebook itself remains the core platform for users generating substantial user activity.

That growth has been seen both in incredibly profitable markets such as in the US & Canada along with faster growing markets such as Asia-Pacific and the Rest of World.

That continued growth in active users is seen across the company’s platforms. Some like Instagram are growing much faster. That continued strength along with reasonable financials (discussed below) highlight how in a normal environment the company could drive substantial shareholder returns.

Financials

The company’s financials continue to remain strong, but it’s clear of the impact that the Metaverse is having on the company.

Meta Platforms Investor Presentation

Meta Financials – Meta Investor Presentation

Meta Platforms made another mistake when it spent on $10s of billions of buybacks at a much higher price per share, before it started losing massive amounts of money. The company’s total revenue in the most recent quarter were $27.7 billion a 5% YoY increase. However, looking at the 4th quarter, the company’s 2022 revenue will likely be more than 2020 but below 2021.

The company’s reality labs isn’t changing its revenue substantially, nor is other revenue, but what’s remaining incredibly strong for the company is its advertising revenue performance. Unfortunately, what’s hurting the company is what’s happening with that revenue. Costs are going up, dragging down operating income even before increasing Reality Labs losses show up.

The company is still profitable, that’s clear. But its operating margin has dropped from the mid-40s % to 20%. Current operating income still gives the company a P/E of roughly 15 indicating how profitable it is, however, the forecast is for profits to drop further. We’d like to see the company tone down Reality Labs associated spending substantially, and focus on share repurchases.

Our View

The answer here is clear.

Regardless of the long-term potential of Reality Labs, there is a problem when the CEO (Mark Zuckerberg) owns 55% of the voting shares with a much smaller % of the equity shares. There’s especially a problem when that CEO is costing the company $15 billion in losses annualized through forcing investments in the metaverse, a number that he says is going to grow substantially in the next year.

That’s for a business that’s barely earning $2 billion in revenue annualized. It might be expandable but in the past 2 years, it’s lost more than $20 billion while failing to expand revenue. The metaverse’s active users are roughly 40% of the company’s target, and the company hasn’t provided a path to turning around that struggle to increase revenue and profits.

It’s time for Mark Zuckerberg to have voting shares proportional to his ownership and to let the shareholders and other employees focus on investing for expansion. Until that changes, or his strategy changes, the company we once thought had enormous potential is almost untouchable.

Thesis Risk

The largest risk to the thesis is Meta can always revamp its business. The company can always tone down its Realty Labs business substantially along with capital investments, substantially improving profits and shareholder returns. That could mean that investors who don’t take advantage of the current valuation would miss out.

In a normal environment, this is a $300 billion company, earning $50 billion in annual operating income.

Conclusion

Meta Platforms has a unique portfolio of assets and despite the impacts of privacy changes etc., the company has, impressively been able to bounce back. Revenue numbers in advertising especially are actually remaining stronger than Realty Labs, for example, where the company is spending $10s of billions.

Going forward, we expect Meta Platforms to be able to increase shareholder rewards but Mark Zuckerberg needs to back up his thesis for VR/AR and focus on the core platforms. We’d like to see his voting percentage pushed down to be commensurate to his market share. Until that happens or he dramatically changes his focus to be long-term returns, we expect Meta Platforms to struggle as an investment.

Be the first to comment