bunhill

Medical Properties Trust, Inc. (NYSE:MPW) has pulled back sharply from its recent November highs after fending off the initial bear attack that led to the capitulation toward its October lows.

Once again, the mention of Steward Health Care has encouraged bears to intensify their thesis as S&P Global Ratings placed MPW on watch for a rating downgrade. Accordingly, the caution was driven by Medical Properties Trust’s increased exposure to Steward and “the heightened concerns around Steward’s indeterminate credit quality.”

Now, it doesn’t mean that MPW has been downgraded yet, even though the market hit it last week. But, note that MPW remains well-supported above its October bottom, as buyers returned to bet against the move by S&P Global Ratings.

Interestingly, S&P Global Ratings also attributed its move to Steward’s inability to submit its 2021 audited financials and the delay in “failure to address its ABL facility in a timely manner.” Why the credit rating agency decided to put MPW on watch now, even though the issue has been known for some time, is unknown.

Furthermore, Steward recently managed to secure the extension of its ABL despite not having submitted its audited financials. Notwithstanding, Steward CEO Dr. Ralph de la Torre articulated that “the extension of our ABL coupled with our re-engineered structure position us extraordinarily well for the coming year.”

Of course, it’s still too early to tell how the market would react from here, as MPW has not been downgraded by S&P Global Ratings yet. But, we believe the steep pullback from its recent highs has likely reflected a downgrade to some extent, as the market is forward-looking. Therefore, we think Steward’s move to extend its ABL has likely helped shore up investors’ confidence, despite the bad news on the potential rating downgrade.

A rating downgrade is, of course, significant. Besides a loss of investor confidence, it could degrade the REIT’s ability to secure additional funding and also increase its financing costs. As such, its continued association with Steward has likely not been met with approval from the rating agency.

But, before investors throw in the towel, we believe it’s critical to reassess noteworthy commentary by management on its confidence in Steward’s progress moving forward.

Management noted that Steward has continued to optimize its contract labor and forecasted unadjusted EBITDA of $350M in 2023, up from 2022’s projection of $65M (midpoint). Hence, Steward’s profitability is expected to improve. Coupled with its ABL extension, it should add further confidence in Steward’s ability to tide through 2023.

Furthermore, MPW has also not ruled out the possibility of partially selling its equity stake in Steward (packaged with real estate). Notably, the company highlighted “a high level of interest.”

Hence, that could also help MPW to potentially reduce its exposure to Steward, improving investors’ confidence. Therefore, we believe the company remains on top of the current uncertainties, even though the market appeared to have de-rated it first.

Therefore, the critical question is whether investors have the confidence to take the plunge into MPW now if they expect significant pessimism has been reflected.

MPW NTM Dividend yields % valuation trend (Koyfin)

MPW last traded at an NTM dividend yield of 10.5%, well above the two standard deviation zone over its 10Y average. Hence, it’s arguable that the market has likely reflected massive execution challenges for MPW through 2023.

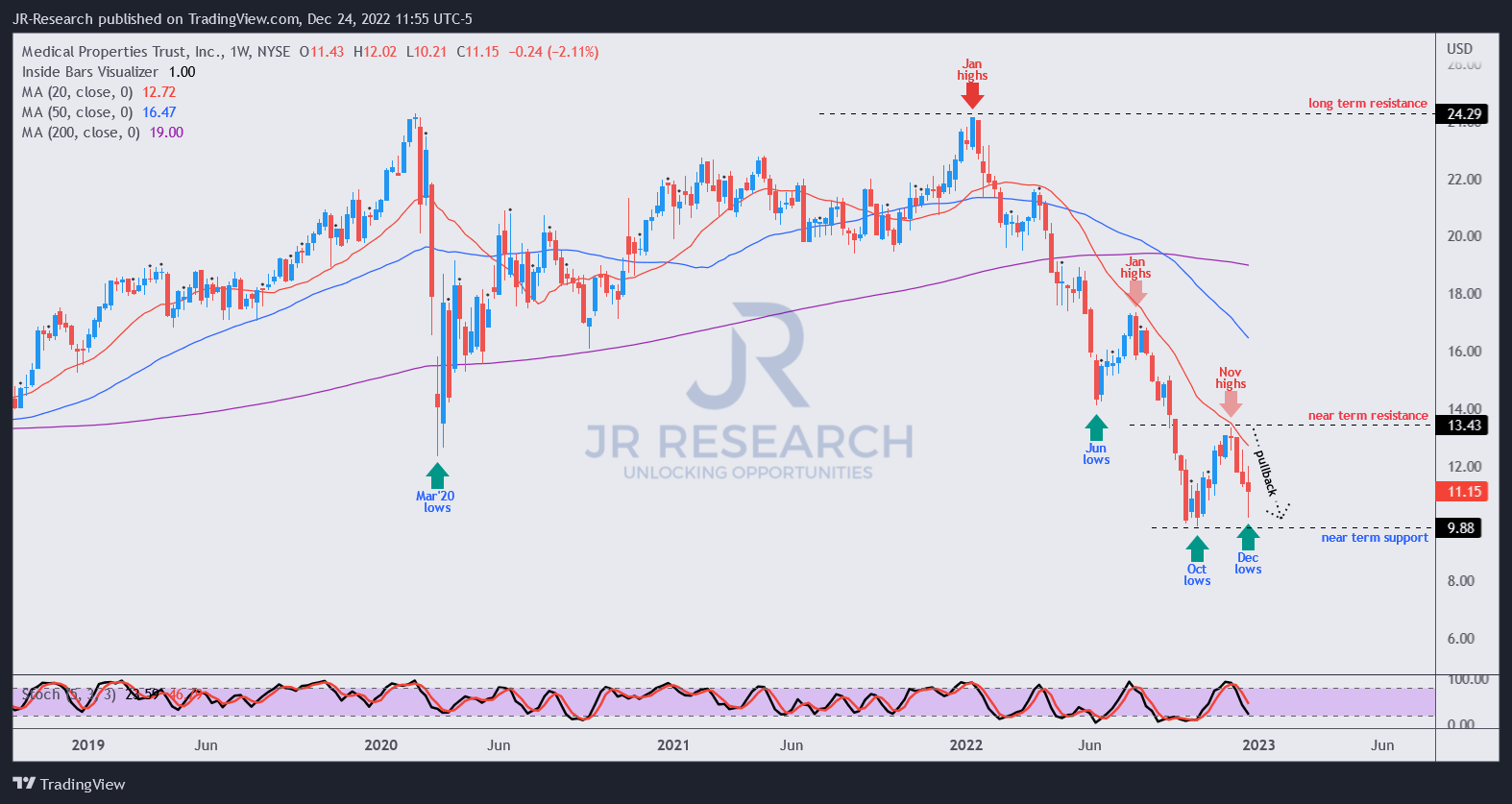

MPW price chart (weekly) (TradingView)

In addition, we gleaned that buyers returned to defend the steep selloff to finish the week. As such, it prevented the bears from taking it below its October highs, which is constructive for MPW’s consolidation thesis.

Hence, we assessed that investors who missed their previous lows should find the current entry levels attractive.

Rating: Maintain Buy.

Be the first to comment