Masha Zolotukhina/iStock Editorial via Getty Images

In no huge surprise, Macy’s (NYSE:M) updated holiday quarter forecasts to the lower end of prior estimates. The department store retailer faced a tough retail environment, but investors need to not over extrapolate on the quarterly results knowing the impacts of covid altered the results. My investment thesis is ultra Bullish on the stock trading near $20.

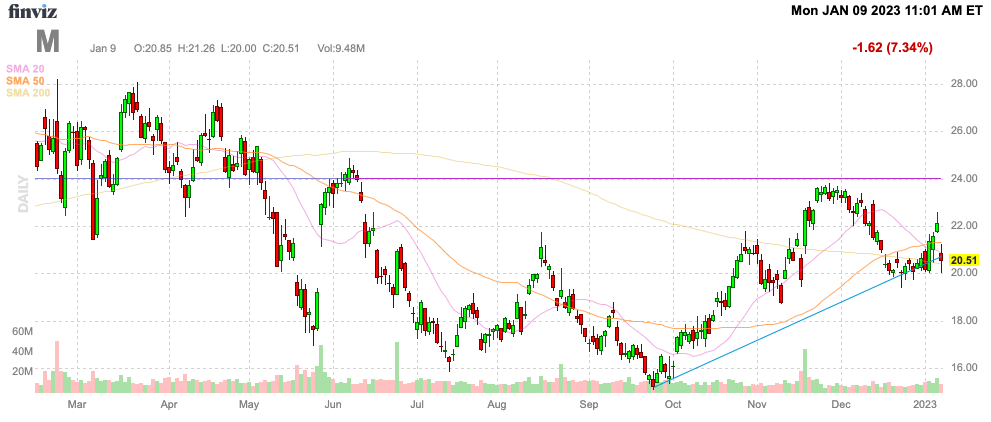

Source: FinViz

Dreary Holidays

Prior to the ICR Conference this week, Macy’s updated guidance for the holiday quarter. The department store now forecasts the following results for FQ4’22:

- Net sales at low-end to mid-point of the previously issued range of $8,161 to $8,401 million.

- Adjusted EPS in the previously issued range of $1.47 to $1.67.

- Inventories are on track to be slightly below last year and down mid-teens relative to 2019.

Macy’s earned $2.45 per share on $8.7 billion in revenues last January, but the retailer faced a very promotional environment this year with competitors having excess inventory. The good news is that the department store expects to end the quarter with inventories down somewhere in the range of 15% from back in 2019 when revenues were at similar levels.

Even with the tough year, Macy’s is still on pace to earn $4+ per share in FY22. The stock weakness isn’t valid based on this weak earnings stream, yet the company should be poised to return to the levels of the prior year.

The market is very confused on how to handle retailers that showed improving results during covid lockdowns, though Macy’s didn’t generate any excessive revenue gains in FY21. The businesses were vastly approved during covid via a strong focus on e-commerce and improved delivery options, such as curbside. In addition, the department store has made a conscious shift into off-price and premium beauty store formats to expand the business beyond the traditional premium apparel sector.

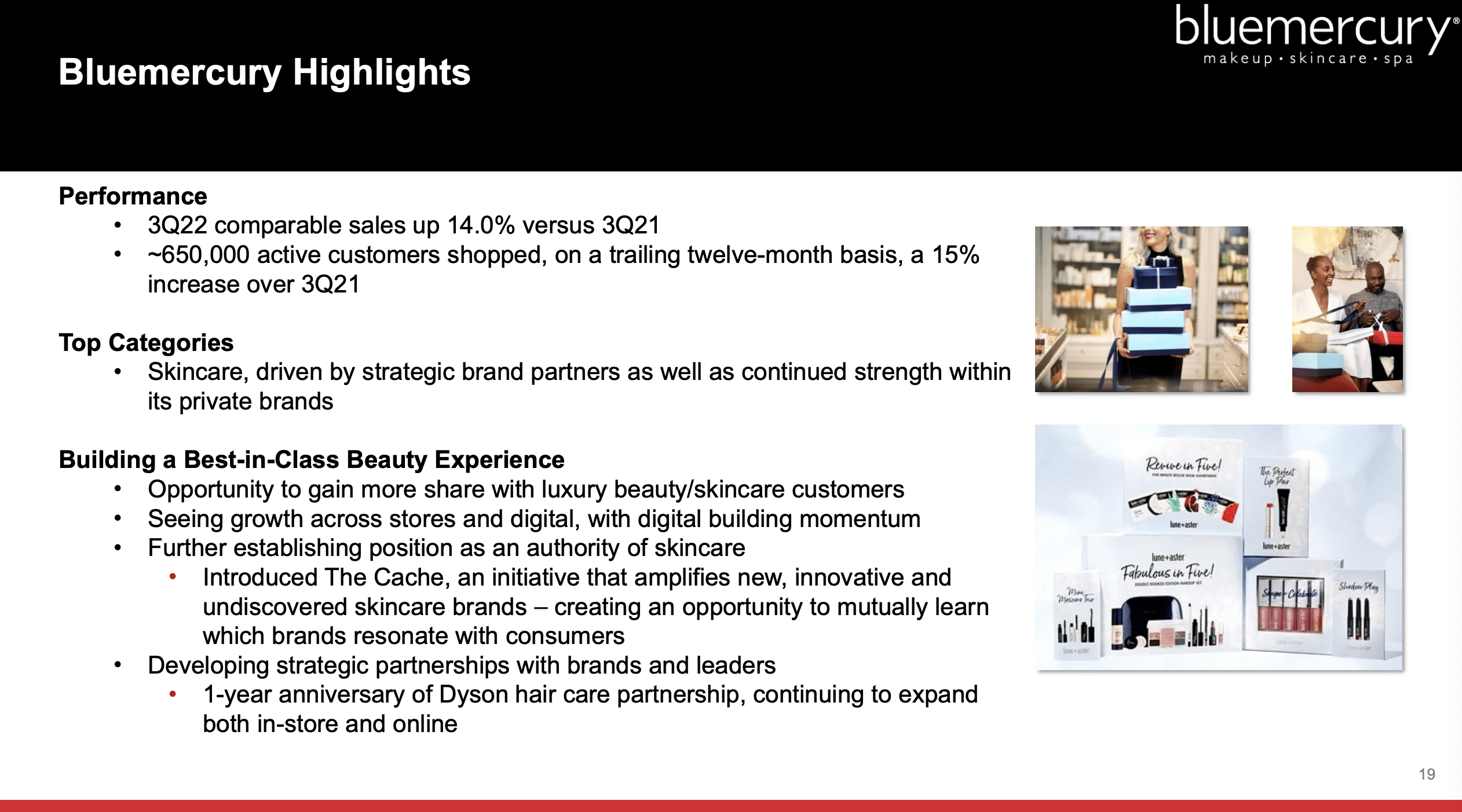

As an example, Bluemercury reported a strong 14.0% comp sales boost in FQ3’22 while the Macy’s brand store struggled with sales down 4.0%. The premium beauty and health store concept even grew active customers by 15% to ~650,000.

Source: Macy’s FQ3’22 presentation

The company is moving forward with new concepts like Market by Macy’s and Bloomie’s. Both examples of the company exploring how to grow the business versus sitting on past success in prior years.

Extreme Value

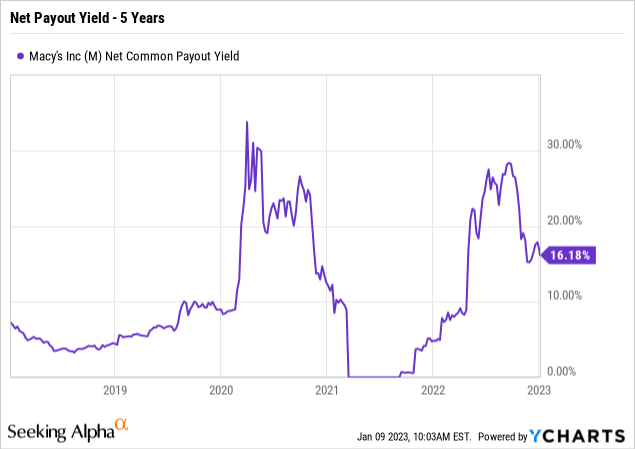

The market is valuing Macy’s based on a continuation of the tough 2022. The department store has still repurchased $600 million worth of stock and paid $130 million in dividends for the year. Even without any FQ4 buybacks, the company will have returned $770 million to shareholders for FY22 for a stock with a market cap of only $5.5 billion.

The net payout yield measures stock valuation beyond the basic dividend yield. A high combination of the dividend yield and net stock buyback yield provides a strong signal when Macy’s has returned 16% of the current market cap to shareholders in the last year.

Regardless of this value, the stock has fallen 7% in early trading on news that revenues will hit the lower end of the prior range. Management didn’t even cut the full-year EPS targets, though investors clearly view a more likely outcome of earnings falling to the lower-end of the prior target of $1.47 to $1.67 for FQ4.

Macy’s still forecasts reaching a low end EPS target of $4.07 for the year and the stock only trades at $20. The company has an easy path to boosting earnings at this stock valuation with the cheap share buybacks.

In just the last year, the diluted share count dipped from 314 million in FQ3’21 to 278 million shares at the end of October. The end of period share count was only 271 million.

Investors aren’t appreciating how just similar net income in a future period will lead to a far higher EPS. The FY21 EPS reached $5.31 and Macy’s produced net income of $1,668 million for the fiscal year.

The company had a diluted share count of 305 million. Macy’s had already reduced the share count by 10% during FY22 and the remaining $1.4 billion share buyback authorization would help reduce the share count by a significant amount going forward.

A further 10% reduction in the share count to 240 million shares outstanding would lead to an EPS of $6.95 based on just repeating the FY21 net income level. As an important note, FY21 results weren’t at unsustainable levels with gross margins for the fiscal year at 38.9%, up just 70 basis points above the FY19 levels. The FQ4 gross margin were actually down 30 basis point below the 2019 levels.

Macy’s has the potential to both grow revenues from the new store concepts while repeating the margins from prior peak level. The department store appears to have a stronger future than the market thinks.

Takeaway

The key investor takeaway is that Macy’s is far too cheap at $20. The apparel sector has faced a tough year due to inventory excess in the sector and investors are being far too gloomy about the future. The stock should be rewarded with a far higher multiple based on hitting a $4+ EPS in a tough year and a repeat of the FY21 success will elevate Macy’s to far higher stock levels.

Be the first to comment