simonkr

Introduction

Livent Corporation (NYSE:LTHM) is the world’s lithium king, producing high-grade lithium for use in electric vehicles (“EVs”). With EVs becoming more popular as ESG-conscious governments act quickly to invest in alternatives to reduce greenhouse gas emissions, lithium could be regarded as the new oil of this century.

The lithium total addressable market is expected to grow at an 18% CAGR from 2022 to 2030, making Livent Corporation stock an appealing investment in a high-growth sector.

While revenue and earnings have fluctuated in recent years, and the company does not pay a dividend, LTHM stock is for investors with a high-risk appetite. However, for long-term investors, this stock could be a clear winner.

Company Overview

The Livent Corporation is a leading producer of lithium compounds like lithium hydroxide and lithium carbonate. These chemicals have many practical uses, such as in electric vehicle batteries, electronic device batteries, and grid storage.

Livent operates production facilities in the U.S., Argentina, and China and distributes its products worldwide. The company is dedicated to providing its customers with the highest quality lithium for EV and battery use, and as a result, it has become one of the world’s leader in lithium technology.

Lithium Total Addressable Market Growing At A CAGR Of 18%

The metal lithium is widely utilized in the battery industry, and is especially important to the development of the electric vehicle market. Since they can store a large amount of energy in a relatively small volume, lithium-ion batteries are frequently used in EVs. Due to their higher energy density and longer driving ranges, lithium-ion batteries are increasingly being used in these types of applications. They have a low rate of self-discharge, so a charge can be hold for a long time.

Lithium-ion battery demand is being fueled in part by the growth of the electric vehicle market. The report by Grand View Research, Inc. predicts that the global lithium-ion battery market will grow to $183 billion by 2030. Through 2030, its CAGR is predicted to average 18.1% annually.

Lithium mining and production have skyrocketed in recent years to meet the soaring demand for electric vehicles and energy storage systems. The increase in demand is also due to the increased use of:

- Market expansion is also anticipated to be fueled by the development of integrated charging stations, green power-generation capability, eMobility service providers, battery manufacturers, and energy providers.

- Energy storage systems, including lithium-ion batteries, are used in residential homes, businesses, and utilities to mitigate the impact of intermittent renewable energy sources like solar and wind.

The world’s electric vehicles and energy storage systems rely on Livent Corporation’s high-quality lithium products. BofA raised Livent’s rating to buy from hold because it believes the stock price reflects a too-low lithium market price over the cycle.

LTHM Financial Performance Is Strong

As a result of Livent Corporation’s exceptional performance in the third quarter of 2022, the company raised its adjusted EBITDA guidance for the full year 2022.

For the quarter, both revenue and adjusted EBITDA were up significantly year-over-year by 124% and 644%, respectively. Revenues outlook for the entire year of 2022 were increased by $15 million. The results were particularly strong due to the positive impact of high realized prices and increased volumes.

As global expansion projects near completion and high-grade lithium production can initiate, Livent is well-positioned for continued expansion and earnings growth.

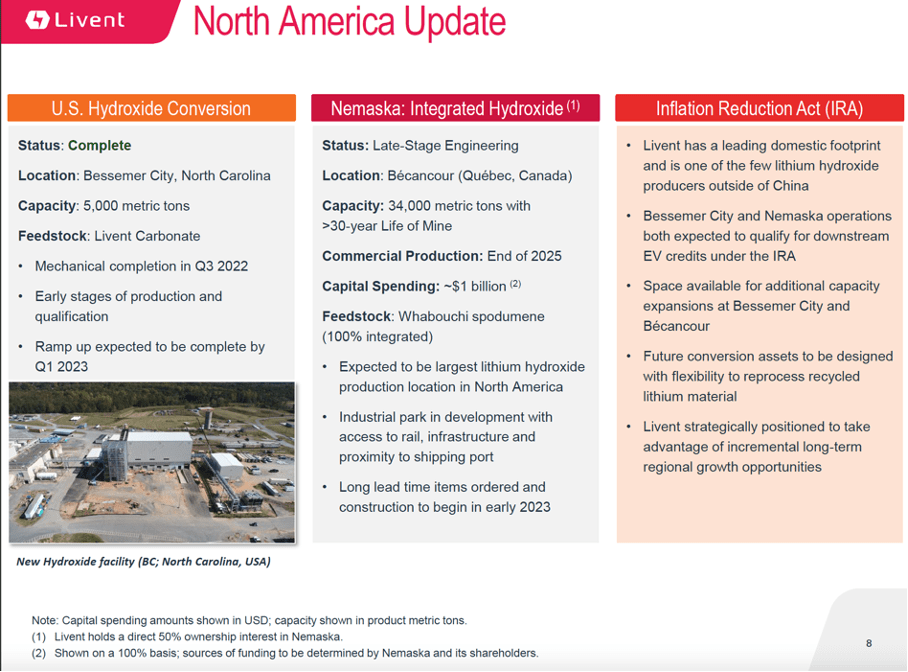

North America Update (Livent 3Q22 Investor Presentation)

The company’s expansion projects continue to make significant headway, and all planned timelines and capital expenditures are on track. The third quarter saw the completion of the United States Hydroxide Conversion project (a 5,000 metric ton lithium hydroxide expansion facility), allowing the company to increase revenue from product sales.

A new 15,000-ton hydroxide facility will be operational in China by the end of 2023, and the company’s lithium carbonate expansion in Argentina will be fully operational after two phases.

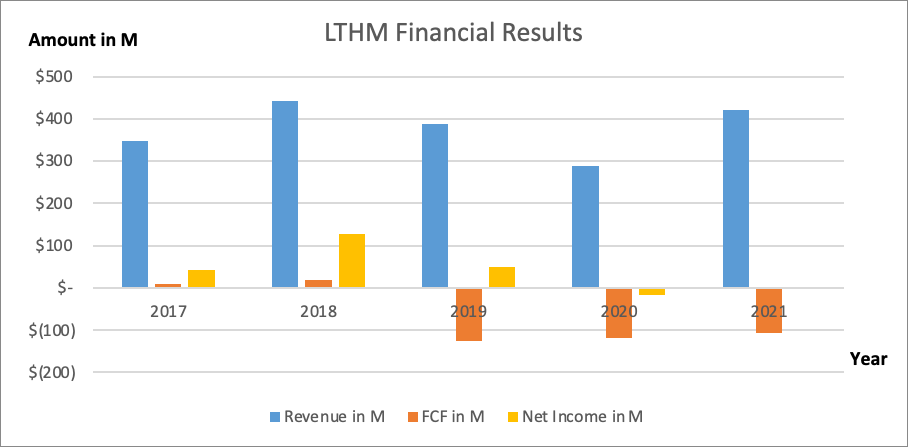

Looking at the big picture, revenue has been somewhat volatile over the past few years, with demand declining during the coronavirus crisis. As of 2019, Livent Corporation’s free cash flow (“FCF”) has been negative as a result of increased capital expenditures for use as investments in growth initiatives. The $218M in CAPEX for the third quarter of 2022 was split between growth-related expenditures of $195M and maintenance expenditures of $23M.

Livent Financial Results (SEC and Author’s own graphical representation.)

Although some investors may be concerned that the rise of the work-from-home culture poses a threat to the demand for electric vehicles, I don’t see this as a significant threat because many companies require employees to work at the office. As a means to lessen the world’s reliance on fossil fuels, cut down on greenhouse gas emissions, and enhance air quality, many governments are encouraging the use of EVs.

Financial incentives (tax credits, rebates, or grants), investments in charging infrastructure, fleet mandates, and so on have all been implemented to promote EV adoption. Livent Corporation is riding a wave of secular growth, which bodes well for its future.

Forward Stock Valuation Extremely Favorable

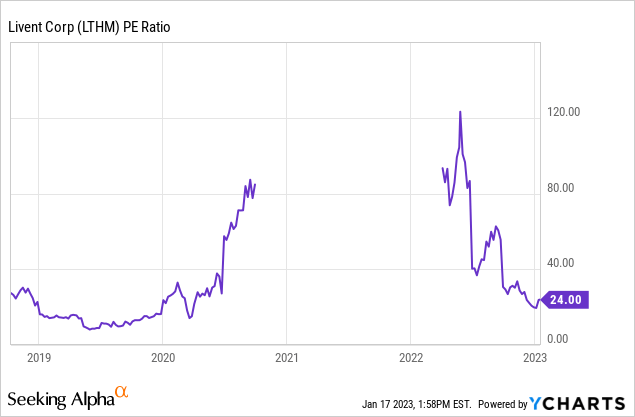

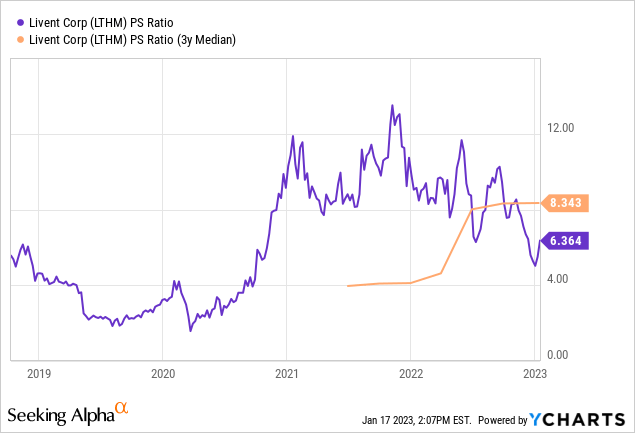

The P/S ratio and the P/E ratio are useful metrics for evaluating a stock’s price. Both paint an accurate picture of the stock’s past and present worth. While revenue has been fluctuating over the years, I think the P/S ratio is more useful. Profit margins are currently not at their highest, but the company is still expanding rapidly.

Based on data presented by YCharts, the non-GAAP P/E ratio is currently 24. In 2019, when the stock price was clearly depressed due to the anticipated decreased demand for lithium in EVs, the P/E ratio hit its lowest level. The stock is currently a bit expensive right now, as indicated by the P/E ratio of 24, but the company anticipates rapid growth in the future. Let’s next take a look at the P/S ratio.

The P/S ratio compares a company’s market value to its per-share sales. The stock’s valuation was at historically low levels in 2019, as shown by the chart. The current P/S ratio of 6.4 is 23% lower than its average level over the preceding three years. In addition to Livent Corporation’s low stock valuation, sales growth is anticipated to be substantial over the next few years.

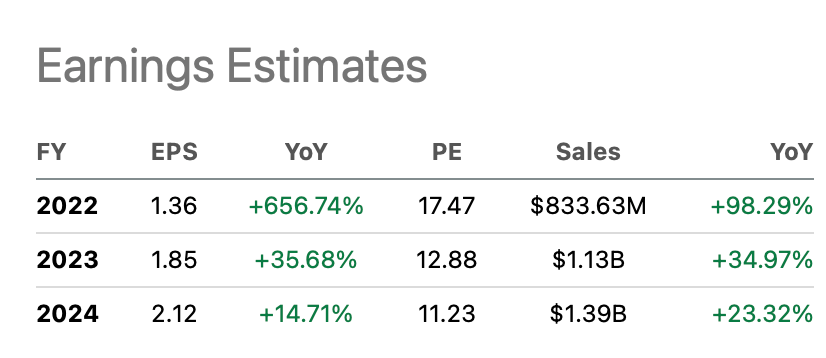

The outlook for the stock’s future earnings and revenue is mixed among analysts. There is still an optimistic outlook for future revenue and earnings. As a result, analysts anticipate a 35% increase in revenue and a 36% increase in EPS for 2023. With a forward P/E of 11 for 2024, Livent Corporation stock is cheap relative to its current price.

In 2024, sales are projected to hit $1.4 billion. By multiplying this by the three-year average P/S ratio of 8.3, we arrive at a market cap of $11.6b. This is equivalent to a 170% increase in share price. An absurdly high (and unrealistic?) figure, but if sales and earnings are growing at the expected fast rate, the Livent Corporation share price seems undervalued both by P/E ratio and P/S ratio at 2024 levels.

Livent’s Earnings Estimates (Seeking Alpha LTHM Ticker Page)

The lack of a dividend and the volatility of the company’s earnings could make LTHM stock unattractive to some investors. However, I rate Livent Corporation stock as a strong buy because of its promising growth potential and reasonable valuation.

Risk To Mention

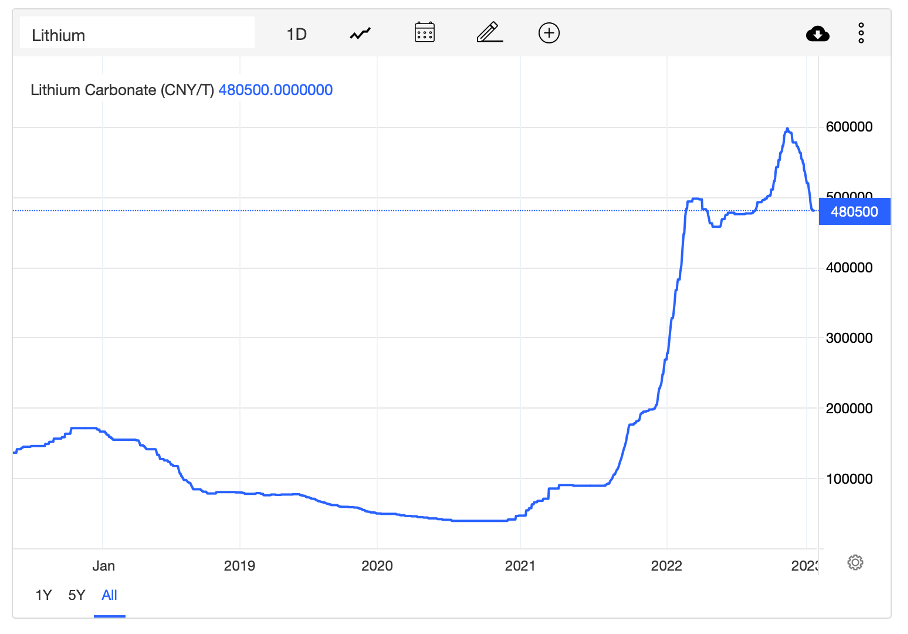

Although the future looks bright for Livent Corporation, there are still risks to mention. Changes in supply and demand can affect the price of lithium, as with other commodities. Looking at the graph of lithium prices, we can see that they have increased dramatically from the year 2021 onward. However, I don’t think this is sustainable in the long run.

Lithium Carbonate Price Chart (tradingeconomics.com)

Even though the advent of EVs will boost demand generally, the demand may soon be destroyed by an impending recession. Lithium, in my opinion, is the new oil, so I still think Livent Corporation stock is a good long-term investment. Those looking to buy Livent Corporation stock should have a high-risk tolerance.

Be the first to comment