LUNAMARINA/iStock via Getty Images

Investment Thesis

U.S. Steel (NYSE:X) is a boring company. But it’s profitable and cheap. That’s the core of the thesis.

But once we dig further, we can see that demand for steel is a lot more sticky and less recessionary sensitive than many believe, even analysts.

There are key trends that I believe will be unfolding in 2023 that steel investors should know about.

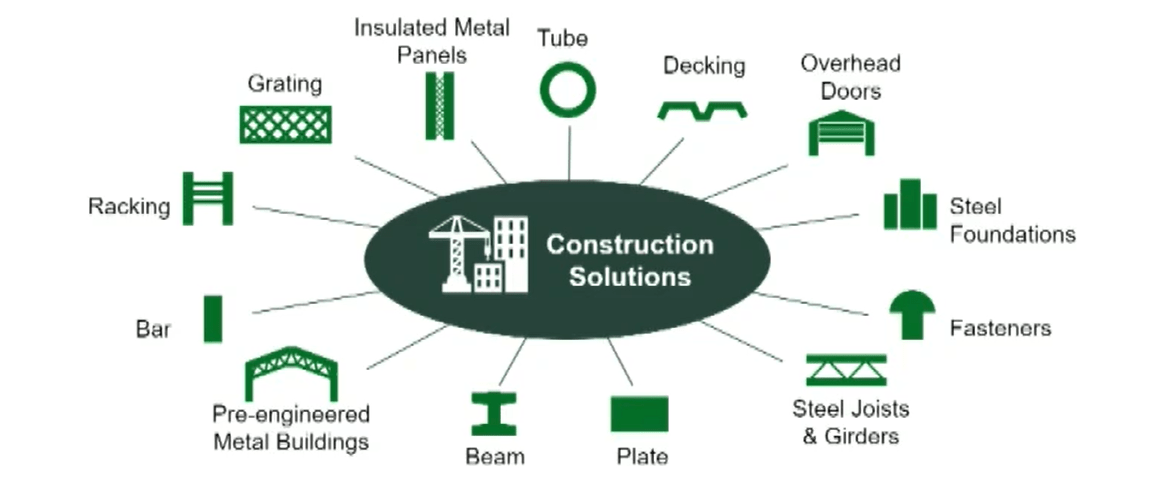

Nucor’s Investor Day

Not only is the US going to see significant government stimulus packages from the Infrastructure Investment and Jobs Act, aimed at modernizing roads, bridges, and rail, but also, the onshoring of supply chains.

But there is onshoring chip manufacturing too.

Nucor’s Investor Day

For this, we should look no further than Apple (AAPL) and its efforts to reduce its reliance on China. Also, German manufacturers considering moving to the US since energy prices are significantly lower, allowing these businesses to increase their profitability with lower feedstock prices.

So, as more and more companies re-shore in the US, there’s going to be a lot of construction going on in the next several years.

So, with that framework in mind, let’s get to these preannounced Q4 earnings.

Q4 Earnings, Beats Analysts’ Expectations

Recall, for the first nine months of 2022, U.S. Steel’s adjusted EPS reached $8.98. And Q4 EPS is expected to come in around $0.61. That means that the full year 2022 will come in at around $9.59 of EPS per share.

Previously, I believed U.S. Steel’s full-year 2022 would reach approximately $10.13. This figure was clearly too aggressive on my part (versus $9.59 now expected).

That being said, Q4 2022 EPS figure clearly came in substantially higher than the Street’s expectations of $0.40.

So, What’s Next?

There are two contradictory arguments. On the one side, there’s the bearish argument that we are going into a recession, and in a recession demand for steel will fall.

Or, put another way, steel is highly sensitive to the global macro environment. So, if we end up in a global recession in 2023, demand for steel would be curtailed.

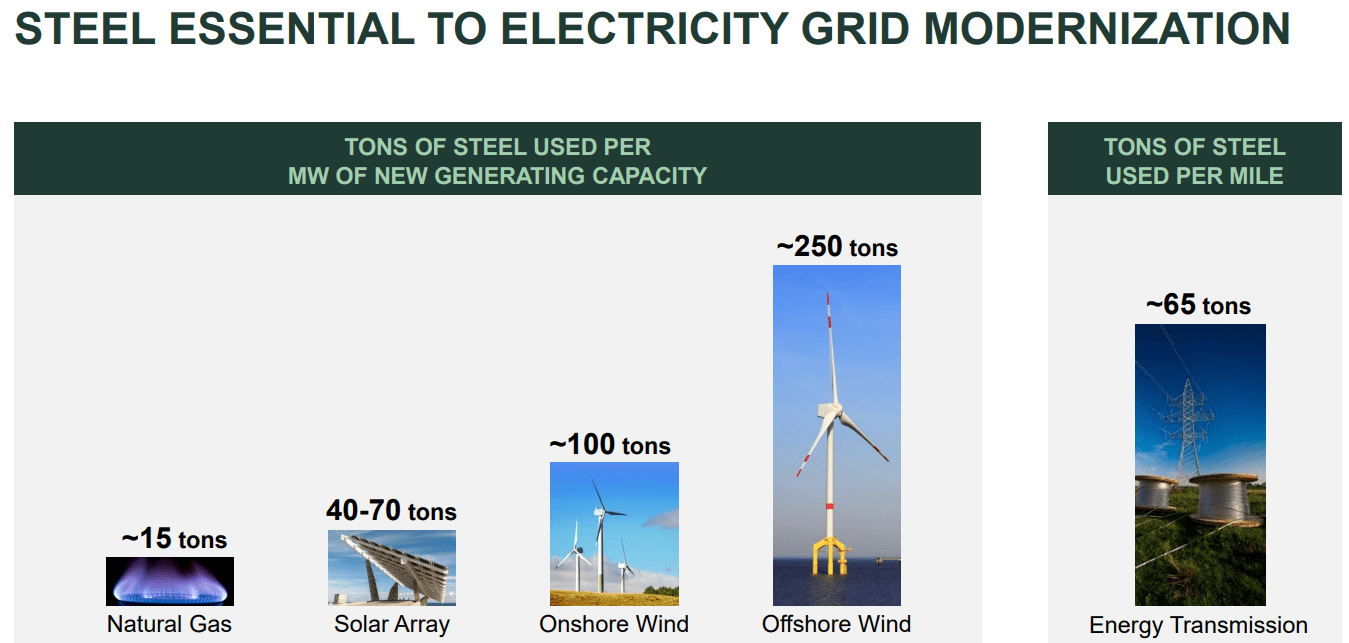

And then there’s the bullish argument. And the bullish argument is that for the green energy transition, we are going to need a lot of steel. And that’s going to add fundamental support for steel demand that we did not have in prior downturns.

Nucor’s Investor Day

Not only do we need a significant amount more steel to build solar panels and onshore and offshore windmills, but other infrastructure that’s needed for the modernization of our energy infrastructure.

On top of that, there’s the other bullish driver, and that is China.

Trading Economics

China’s real estate market substantially contracted in 2022.

But with China very slowly reopening in 2023, there’s hope that this will see demand for steel increasing from the low levels that steel is priced at presently.

With that in mind, let’s get into U.S. Steel’s valuation.

X Stock Valuation – 7x Next Year’s EPS?

Before we go further into U.S. Steel’s valuation, I want to highlight the graphic below, showing U.S. Steel’s debt profile.

U.S. Steel Q3 2022

Over the next several years, U.S. Steel has no significant maturities. Indeed, 80% of its debt is due in 2029 or later. The company’s balance sheet is very strong. There’s no material risk of bankruptcy.

Now, we know that U.S. Steel is priced at 3x this year’s EPS. But the question is whether or not 2023 will be as brutal as analysts expect.

For their part, analysts expect U.S. Steel’s EPS to drop by 75% from 2022 to approximately $2.26. That would put U.S. Steel priced at 10x next year’s EPS.

However, I don’t buy this argument that U.S. Steel’s EPS will drop so substantially. In the first instance, as we touched on already, steel prices appear to have to stopped falling.

Secondly, China’s real estate market has been a headwind throughout 2022. With the Chinese government being more lenient toward the Chinese real estate sector, this could actually provide a tailwind in 2023.

So, what was a headwind, will be a tailwind in 2023.

The Bottom Line

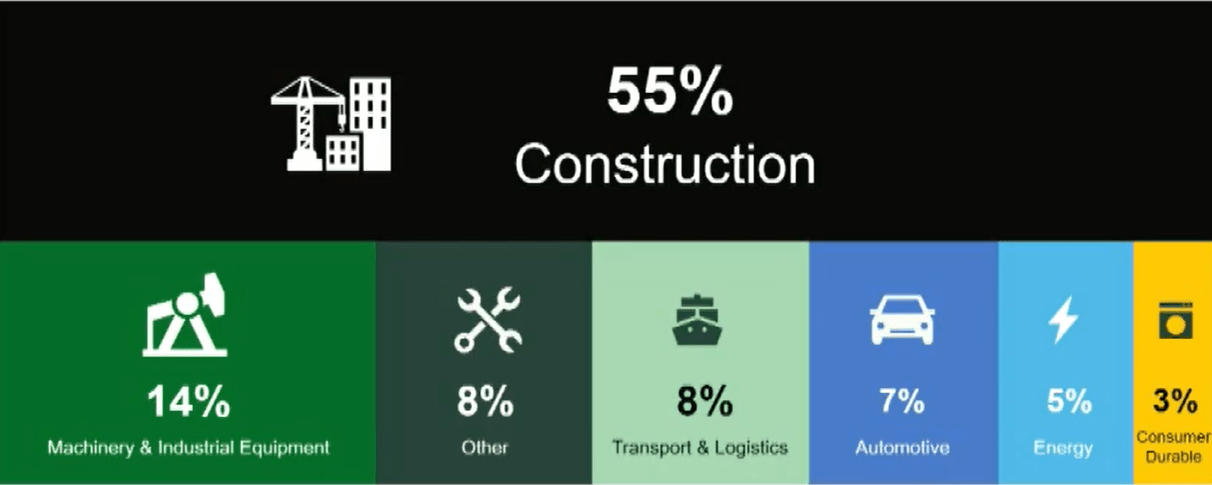

Nucor’s Investor Day

Note, I’ve taken many graphics from Nucor’s recent Investor Day presentation since U.S. Steel hasn’t had one.

And even though both companies have slightly different end markets, I highlight these slides because they neatly show where steel will be used going forward in the coming few years.

It’s difficult to imagine, but U.S. Steel is priced for a recession. But it could actually end up having a really strong 2023.

Be the first to comment